Keeping faith

In June, faced with the task of replacing its longstanding portfolio manager, Alastair Mundy, Temple Bar Investment Trust’s (TMPL’s) board reiterated its commitment to a value style of investing. The board has now opted to hand the management contract to Nick Purves and Ian Lance of RWC Partners, two managers with considerable experience of managing income portfolios using a value-style approach.

Value investing, where managers buy stocks that are valued more cheaply than market averages – based on measures such as price/earnings, price/book and yield – is deeply out of favour. The RWC team says that value stocks have never looked more unloved in the 30-odd years that they have been managing money. In their view, this makes it imperative that TMPL investors keep faith with the strategy and it also means this is an attractive entry point for new investors.

One important change, however, is a cut to TMPL’s dividend to a level that the RWC team believes will be more sustainable.

UK equity income and capital growth

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

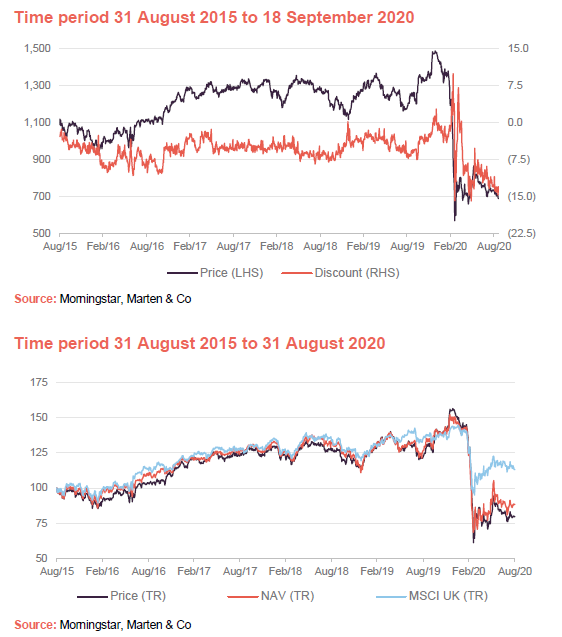

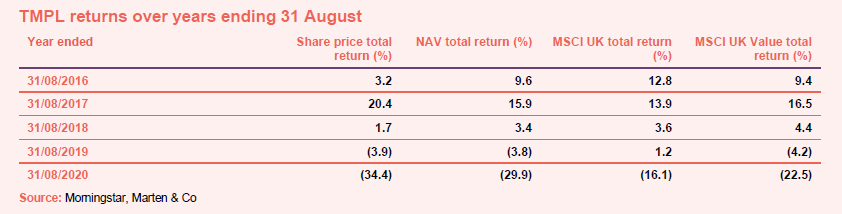

Both TMPL’s share price and discount were hit hard by the panic that set into markets in March 2020, as the effects of COVID began to be felt on the economy. TMPL’s discount is now the widest it has been in more than a decade.

Early in 2020, following a decisive result in the UK election in December, TMPL appeared to be gaining some ground against the index. However, the sharp falls in markets in March 2020 hit the trust disproportionately hard. Investors shunned value stocks in favour of a narrow group of growth stocks.

Summary

The board has announced that:

- TMPL will continue to be managed with a value style;

- RWC Partners will be appointed as the investment manager;

- the dividend will fall by about 25% to 38.5p, equivalent to a yield of 5.9%; and

- the management fee is essentially unchanged at 0.35% of net assets, but RWC will not charge a fee until July 2021. The incumbent manager’s notice period ends in April 2021. There is no performance fee.

Background to the management change

Launched in 1926, TMPL has a long history. It aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

TMPL is an AIC Dividend Hero, having increased its dividend every year for 36 years. For 18 years it was managed by Alistair Mundy, who was head of the Value Team at Ninety One UK. He stepped down as manager in April 2020. Shortly thereafter, TMPL’s board served protective notice on Ninety One UK and instigated a review of the trust’s management arrangements. For the time being, responsibility for the trust’s portfolio passed to Ninety One UK’s Alessandro Dicorrado and Steve Woolley.

On 9 June 2020, the board announced that it had appointed Stanhope Consulting to assist in the review. The parameters of the review were “to establish the most effective management arrangements for Temple Bar Investment Trust to fulfil its objective of outperformance of the FTSE All Share index, whilst investing with a sustainable value tilt, in the changed environment of pandemic and long- term global climate change”.

On 23 September 2020, the board announced that, it had selected RWC Partners as TMPL’s new investment manager. Within RWC Partners, responsibility for managing TMPL’s portfolio will rest with Nick Purves and Ian Lance. The expectation is that they will take on full responsibility for the portfolio from the end of October 2020.

The new managers

RWC was established in 2000 and now employs 155 people, including 57 investment professionals. RWC manages around $18bn for clients across a range of strategies, from offices in London, Miami and Singapore.

Nick and Ian each have over 30 years’ experience and have worked together for 13 years. The two co-manage over £3bn of assets across a number of income funds.

Nick Purves joined RWC in August 2010 from Schroders where he was a senior portfolio manager with responsibility for both Institutional Specialist Value Funds and the Schroder Income Fund and Income Maximiser Fund, together with Ian Lance. Nick worked at Schroders for 16 years, having moved from KMPG where he qualified as a chartered accountant.

Ian has 30 years of experience in fund management and started working with Nick at Schroders in 2007 before joining RWC in August 2010. Whilst at Schroders, he was a senior portfolio manager managing the Institutional Specialist Value Funds, the Schroder Income Fund and Income Maximiser Fund, together with Nick. Previously, Ian was the head of European equities and director of research at Citigroup Asset Management and head of global research at Gartmore.

Long-term, value-oriented investment approach

Nick and Ian will manage TMPL with the same long-term, value-oriented investment approach that they apply to their other portfolios. The shape of the portfolio will be driven by their stock selection decisions. They operate a high-conviction style and expect that TMPL’s portfolio will comprise about 30 positions. Index weights will have no influence on portfolio construction and the portfolio will have a high active share.

Stock selection is driven by fundamental research. They are looking for stocks that are trading at a discount to what the team believes is their intrinsic value. When assessing the potential for stocks being considered for their portfolios, the team takes a five-year view. They apply a long-term average valuation multiple to their view of what they think the company should be earning from its normal activities at the mid-point of an economic cycle.

The managers say that they are cognisant of the economic environment when making investment decisions, but make no attempt to second-guess the direction of markets.

The managers are keen to avoid so-called value traps and so, while these companies may have short-term issues, they should be on a medium- to long-term growth trajectory. Business should also be managed in line with sustainable or responsible principles. Companies should also be robust enough, in terms of balance sheet strength, to survive whatever short-term problems they are facing.

The underlying ethos behind the approach is that, just as investors become over-exuberant about some stocks, they become overly pessimistic about others. These investors then extrapolate from short-term setbacks and apply very low valuation multiples to trough earnings.

This presents an opportunity for value managers such as the RWC team, but they have to be patient. This means that turnover on their portfolios is usually quite low. Often, there is no obvious catalyst, but improved fundamentals, an influx of new management, reduced competition or recognition by the market that it has overlooked the company’s growth potential may trigger a re-rating.

TMPL has the flexibility to invest up to 30% of its portfolio overseas and they intend to take advantage of this in areas where the UK market is underrepresented or does not offer sufficient diversification.

Track record speaks to disparity between growth and value

RWC supplied us with some performance data for one of their funds that they say is representative of the approach that will be applied to managing TMPL’s portfolio.

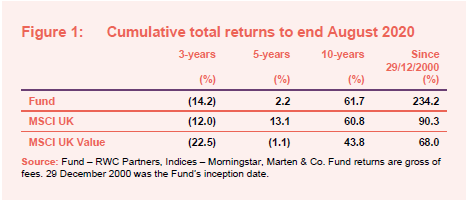

The fund’s long-term returns are very good and, over 10 years, the fund has just managed to beat the MSCI UK index. However, over shorter time frames, while beating the MSCI UK Value index, the fund lags the MSCI UK index by some margin. The value investing style has not delivered sustained outperformance for many years.

Value investing never more out of favour

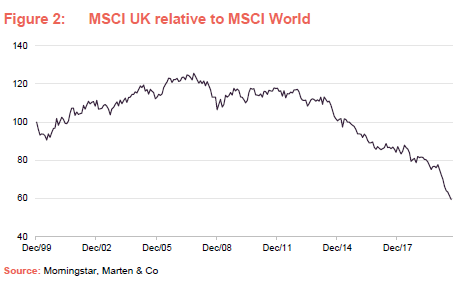

The RWC team believe that value stocks and UK value stocks in particular are trading at compelling valuations. They highlight that the UK market is deeply out of favour with global investors as is evidenced by Figure 2, which shows the performance of the MSCI UK index relative to the MSCI World Index over the past 20 odd years. The UK market has been underperforming for over five years now and the degree of that underperformance has accelerated this year.

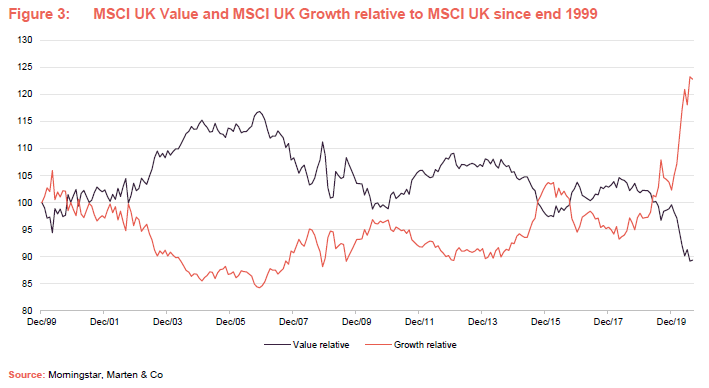

Furthermore, for well over a decade now growth stocks have outstripped value stocks, as evidenced in Figure 3, which shows two lines – the MSCI UK Value index divided by the MSCI UK index and the MSCI Growth index divided by the MSCI UK index. The pink, growth line has moved sharply higher this year as growth stocks have outperformed.

Ian and Nick highlight three periods in their careers where value investing has struggled. The first of these was the tech boom around the year 2000, the second was the run-up to the financial crisis in 2008 and we are now in the third. In their view, value investing has never been more out of favour. COVID-19 has only exacerbated the situation.

The team is often asked why value’s decline relative to growth has been so pronounced and what might the catalyst be for a reversal of this.

The macroeconomic backdrop since the financial crisis has been one of low/no economic growth, very low interest rates and low inflation. The team say that growth stocks are often perceived as long duration assets – their valuations are usually based on a discounted cash flow analysis, which gives higher outcomes when discount rates are low. By contrast, value stocks tend to be perceived as short-duration assets – valued on multiples of last year’s or next year’s earnings or cash flow.

Low interest rates have also aided the survival of so-called zombie companies, whose debt burdens would not been sustainable if interest rates normalised. This prevents much-needed rationalisation of some industries and depresses margins.

In addition, technological change has allowed the emergence of new aggressive competitors in many sectors, adding to margin pressure for existing companies.

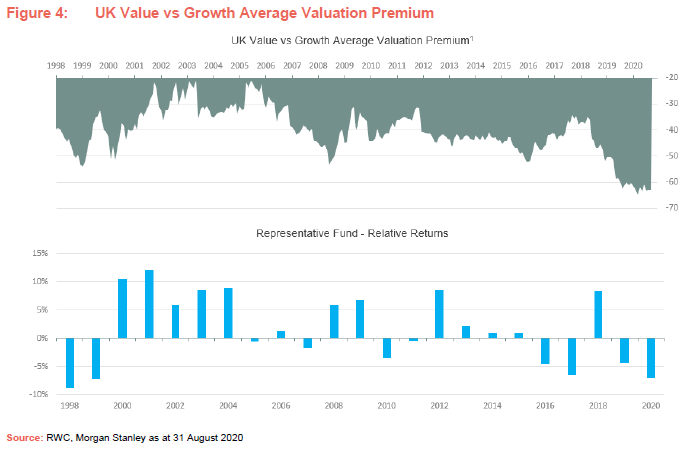

Figure 4 shows the relative performance one of the funds managed by the team (the representative fund) set against a chart that shows the gap between the valuation of value stocks versus growth stocks.

The representative fund outperformed both during and immediately after the financial crisis. Ian and Lance say that they found themselves positioned defensively going into the crisis – ‘boring’, steady earners were out of favour and cheap ahead of the crisis but in demand afterwards. As markets fell out of bed, they repositioned their portfolios, picking up ‘beaten up’ but otherwise robust companies, which then recovered as the panic subsided.

However, the ensuing period of low to no economic growth, very low rates and material technological change was not a good time to be a value investor. Conditions improved in 2018 when firming economic growth was thought to be an indicator of a move to a more normal economy but stalling growth, trade wars, no-deal Brexit fears and – most recently – the pandemic put an end to that.

Asset allocation

The team sees extreme value in sectors such as financials – banks and insurance companies in particular; energy – especially the oil & gas majors; consumer discretionary – retailers, media, support services and telecoms; and selected companies within the materials sector. They say that some target stocks are trading at prospective earnings yields in the 20s (the earnings yield is the inverse of the price-earnings ratio – it is the earnings per share, for the most recent 12-month period, divided by the current market price per share).

By contrast, the team believes that stocks that are perceived to be high quality and have defensive earnings are fully valued (defensive industries have demand that tends to remain stable irrespective of the various phases of the economic cycle, meaning that their earnings and dividend paying capacity should also be stable). This translates into relatively low exposure to consumer staples companies and health care.

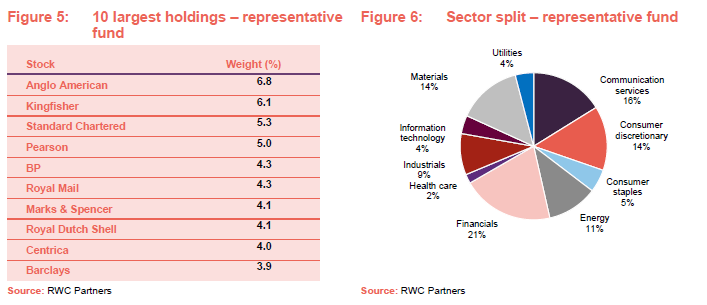

Figures 5 and 6 are for illustrative purposes only, and TMPL’s portfolio may look quite different.

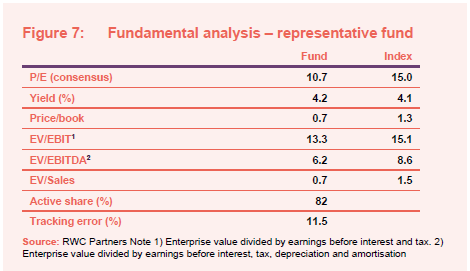

Figure 7 shows how fundamentals of the representative fund compare to its benchmark index.

The managers gave us three examples of stocks that they are considering for inclusion within the portfolio.

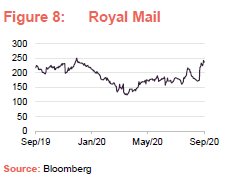

Royal Mail

Royal Mail’s share price has travelled sideways over the past year, after more than halving from its peak in the previous year. The RWC team believes that investors dismiss the stock on the grounds that its core letters business is in terminal decline. However, this ignores the secular growth in its parcels business as it fulfils the shift to online shopping. The team is particularly enthused about the potential for the company’s European parcels business, GLS.

Over the year to the end of March 2020, the group’s operating profit fell by 13.6%, extending a long decline in profitability. Letter volumes (adjusted to exclude the effect of elections) have fallen by about 30% over five years. COVID appeared to reinforce this trend with 553m fewer letters delivered in April and May 2020. However, against that, parcel volumes grew by 37% year-on-year and revenues from the parcels division were 28% higher.

The board did not declare a final dividend. It has stress-tested the impact of COVID and believes the company has the balance sheet strength and the liquidity to get through this and continue to build its parcels business. The RWC team thinks Royal Mail could spin out or sell GLS for an amount close to the market cap of the group as a whole.

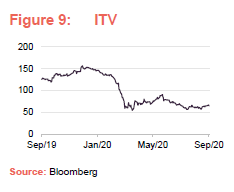

ITV

ITV’s share price has been falling for some time. Figure 5 shows the share price over a year but the stock is trading currently at less than a quarter of its level at the end of 2015. The bear case is falling advertising revenue as viewers switch from watching traditional linear broadcast TV to dipping in and out of shows on services such as Netflix.

Advertising revenue did fall by 21% over the first six months of 2020 relative to the same period in 2019 as companies cut marketing budgets in the face of the uncertainty created by the pandemic, but, actually, ITV’s advertising revenue had been fairly stable for the previous five years. It is attempting to shore up its viewership numbers by switching the audience to ITV hub and BritBox. At the same time, revenue from its studios business, while again impacted by COVID in the first half of 2020, had been compounding at 8% a year.

RWC believes that the long-term prospects for the studios business are good and this will eventually eclipse the stalled advertising revenue from the broadcast business in investors’ minds.

In 2019, the studios business generated about £270m in operating profit and as such in RWC’s view it accounts for the entire valuation of the company. In their view, the broadcast business is therefore in for free.

ITV cancelled its final dividend and is yet to reintroduce dividend payments. The previous 8p per share was absorbing most of its free cash flow, but even if this halved, the stock would still offer a 6.2% yield.

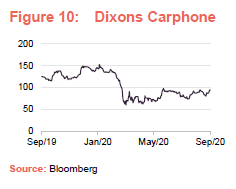

Dixons Carphone

Dixons Carphone’s shares have recovered somewhat from the depths of March 2020 but are a long way off the level of a year ago and a fifth of their 2015 high. The success of businesses such as Amazon in Dixons Carphone’s segment of electrical goods and telecommunications and the ‘death of the High Street’ narrative have weighed on the company.

The group has been trying to grow its online business. It has delivered modest growth in revenue over the past five years, but the revenue mix is changing. Over the year to the end of April 2020, overall revenue growth for its electricals business was 2% but within that, online sales grew by 22%. The shift to online accelerated markedly over the last five weeks of its financial year as COVID lockdowns were put in place. In its AGM statement, the company said that online sales more than tripled year-on-year while stores were closed, and have continued at more than double last year’s sales since stores reopened.

The RWC team believes that investors don’t appreciate that Dixons Carphone is still outselling Amazon in consumer electronics. Furthermore, Dixons Carphone is considering listing a minority stake in its Nordics business, which the RWC team thinks could highlight the undervaluation of the rest of the group.

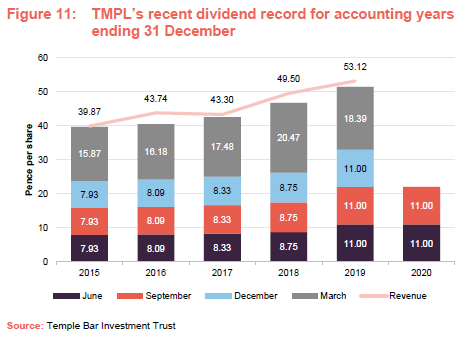

Dividend reset

In the light of the effects of COVID-19 on UK dividend income, the RWC team believes that TMPL’s dividend needs to be reset to a more sustainable level. The intention is that the full-year dividend for the year ending 31 December 2020 will fall to 38.5p (down 25% from 51.39p for 2019). The team believes that this will facilitate steady income growth in subsequent years. The 38.5p dividend represents a yield of 5.9% on TMPL’s share price of 654p as at 22 September 2020.

At the end of December 2019, the trust had revenue reserves of £37.1m (equivalent to 55.5p per share). This has enabled TMPL to maintain its quarterly dividend payments to date. However, the team points out that about 40% of FTSE350 companies have cut, postponed or cancelled their distributions in the wake of the pandemic. While many of these are already starting to reinstate distributions, past experience tells the team that companies will not restore dividends to previous levels immediately, perhaps in some cases not for many years or not at all.

Board

TMPL’s board comprises four non-executive directors, all of whom are independent of both the current and the proposed manager, and who do not sit together on other boards. Each of the directors was re-elected at the AGM on 30 March 2020. There is a good spread of experience and length of service within the board. The longest serving director is the chairman, Arthur Copple, who has been a director for over nine years. All the other directors have been appointed within the last five and a half years.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid by RWC Partners to produce this note on Temple Bar Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained in this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.