On the front foot

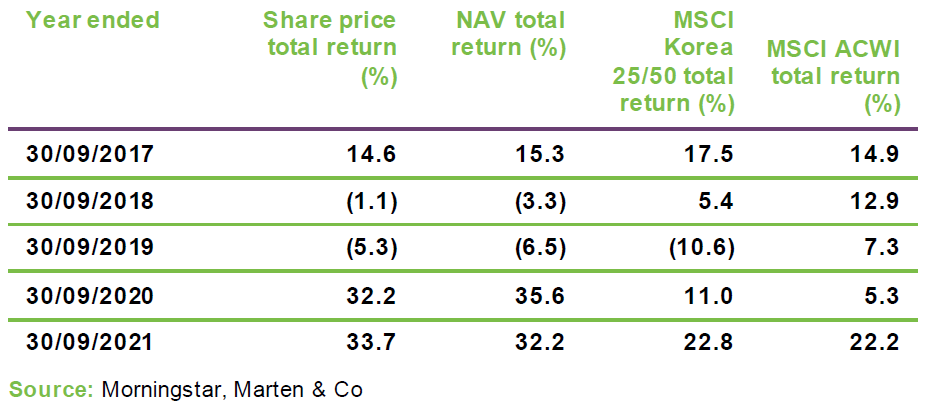

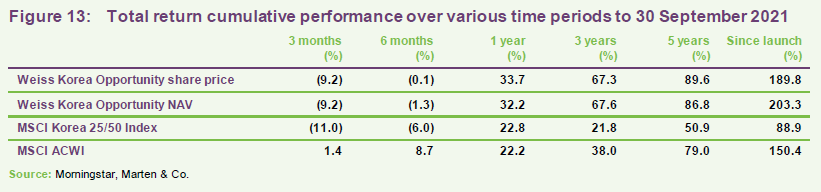

Weiss Korea Opportunities (WKOF)’s returns continue to be well-ahead of those of comparable indices. From its launch in May 2013 to the end of September 2021, shareholders saw returns of almost 190%, more than double those of the MSCI Korea 25/50 Index. Nevertheless, the board and the manager feel that the discount opportunity that WKOF was designed to exploit remains highly attractive.

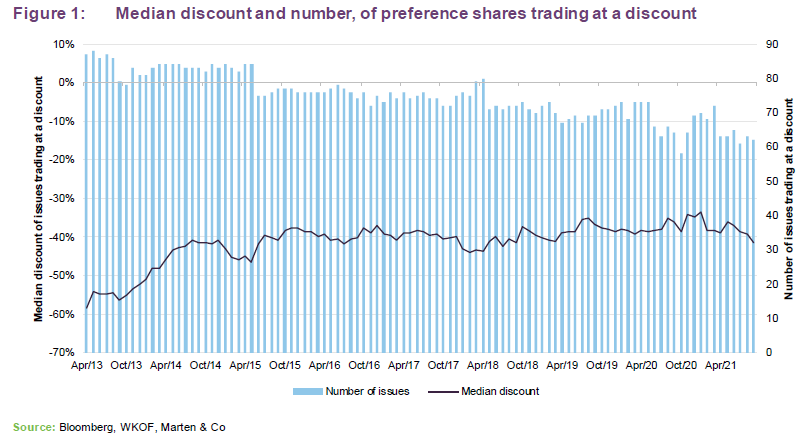

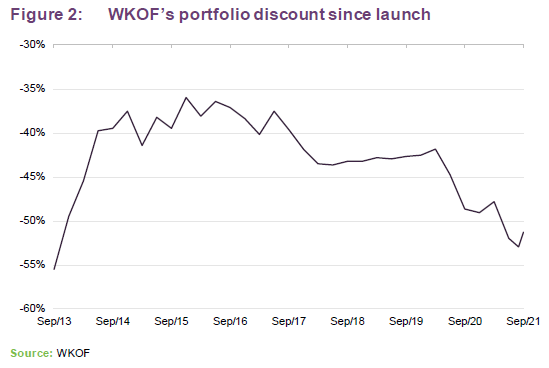

The average discount at which the company’s portfolio of Korean preference shares trades relative to the prices of equivalent common shares is as wide as it has been since the launch of the fund in 2013. In recognition of this, the board feels that it makes sense to try to expand the company.

South Korean preference shares

WKOF aims to earn an attractive return through long-term capital appreciation by investing primarily in South Korean preference shares. Most Korean preference shares are effectively non-voting common shares and are generally entitled to the common per share dividend plus an additional fixed amount. Relative to their corresponding common shares, many Korean preference shares trade at a discount resulting in higher dividend yields and lower price-to-earnings ratios.

Time for growth?

As described in QuotedData’s initiation note, WKOF was established to profit from the valuation gap between the preference shares that make up substantially its entire portfolio and the equivalent common shares issued by the same companies. At launch, the median discount on all of Korea’s preference shares was in the 50s.

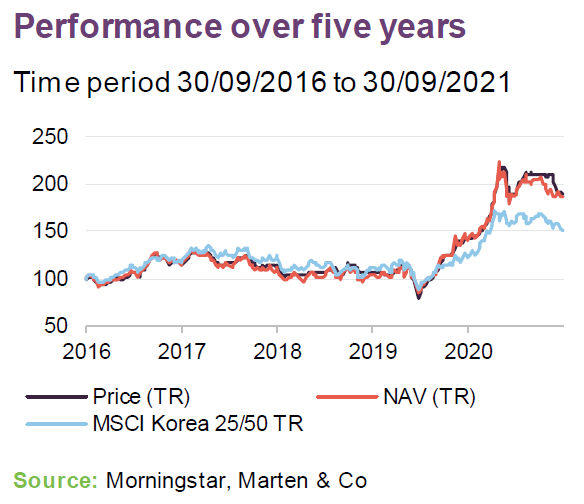

As we show in Figure 13 on page 9, since WKOF was admitted to AIM on 14 May 2013, its NAV has increased by 203.3% as compared to 88.9% for the MSCI Korea 25/50 Index.

WKOF’s manager has added value by capturing narrowing discounts on many preference shares, some of which have contracted significantly. Notably, the discount on the largest preference share issue – that of Samsung Electronics – which was over 40% in 2013 and is now in single digits. Nevertheless, the board and manager believe that a substantial opportunity still remains with 62 of 122 Korean preference shares trading at a discount at 30 September 2021.

As we describe from page 6 onwards, the managers have been taking profits on some positions and reinvesting the proceeds into preference shares on wider discounts. The result is that, as Figure 2 shows, WKOF’s portfolio discount was 51.3% at the end of September 2021, comparable with the discount on the portfolio in 2013. The portfolio discount represents the discount of WKOF’s actual NAV to the value of what the NAV would be if WKOF held the respective common shares of issuers rather than preferred shares on a one-to-one basis.

The board and the investment manager feel that the opportunity set is such that it would be appropriate to seek to grow the company. It initiated a series of measures designed to attract new investors to the fund, eliminate the discount and facilitate WKOF’s expansion.

Chief of these was registering the company under the Alternative Investment Fund Managers Directive (AIFMD). The combination of a Guernsey domicile and a manager based in Boston, USA was hampering attempts to market the trust to UK investors. AIFMD registration alleviates this problem.

AIFMD registration also allows the company to issue new shares at a premium to NAV as well as redesignating realisation shares (created in relation to the periodic realisation opportunities provided by the company – see page 10) as ordinary shares. These may then be held in treasury and reissued subsequently, without the costs typically associated with a new share issue.

WKOF is now a member of the Association of Investment Companies. This means that it features on the statistics pages on the AIC’s website as well as benefitting from the wider services provided by the association.

Korean market background

COVID-19 and social distancing measures continue to affect the Korean economy. South Korea has kept its number of cases and deaths relatively low, although both have been rising rapidly recently as the Delta variant affects the country. 79% of the population have had at least one dose of a vaccine and 67% are fully vaccinated (having just overtaken the UK on that score).

Exports have been strong since the global economy started to reopen and this has helped drive economic growth. At the end of June 2021, GDP growth was running at 5.9% (note this number is flattered by a low base effect). In August, in response to high levels of household debt and soaring property prices, the Bank of Korea raised its benchmark rate by 25bps to 0.75%. The rising debt has perhaps been driven in part by the COVID-related hit to household incomes, especially for the self-employed. This may constrain future consumer spending.

The government is responding to growing income inequality by upping spending on welfare and job creation. That is expected to push government debt past 50% of GDP.

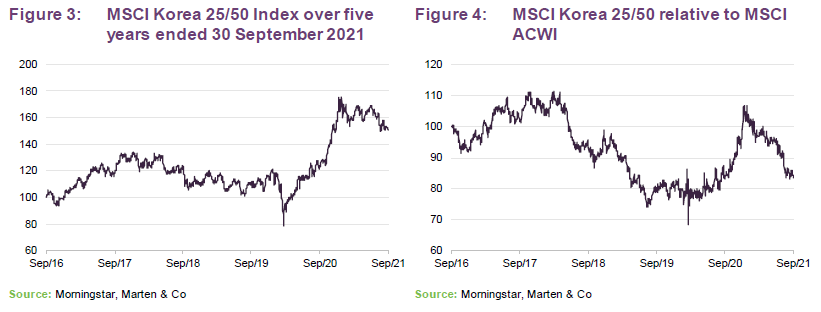

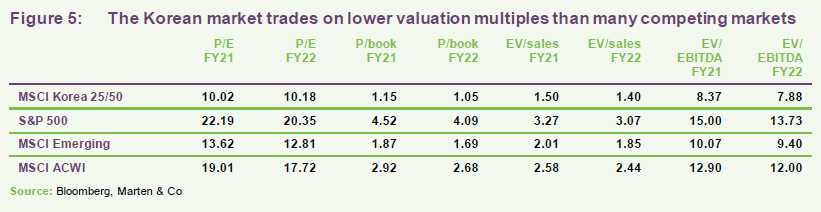

The MSCI Korea 25/50 Index has lagged the recovery in world markets and, on average, Korean stocks are considerably cheaper than those of many other markets.

Asset allocation

At 30 September 2021, there were 37 positions in the portfolio, down from 45 as at end February 2021. The portfolio discount of the preference shares had risen to 51.3% from 46.2% as the manager traded out of positions on relatively narrow discounts in accordance with its efforts to rebalance the portfolio towards preference shares trading at larger discounts.

At the end of September 2021, the average historic p/e ratio of the portfolio was 6.4x and the portfolio yield was 1.9%.

The portfolio also had some exposure to credit default swaps on the sovereign debt of South Korea and put options on iShares MSCI South Korea as general market and portfolio hedges.

10 largest holdings

The most substantial change to WKOF’s portfolio since the end of February 2021 (the data we used in our initiation note) has been the sale of the position in Samsung preferred and the reinvestment of the proceeds into other preference shares trading at wider discounts.

Kumho Petro Chemical

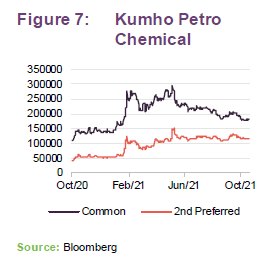

SK Chemicals (see below) recently replaced Kumho Petro Chemical (kkpc.com) in the list of the 10-largest holdings. The discount on synthetic rubber company Kumho Petro Chemicals was 61.5% back in February, but by the end of September 2021, it had narrowed to 37.6%. Park Chul-whan, the largest shareholder in Kumho Petro Chemicals and nephew of chairman Park Chan-koo, put forward a proposal to shake up the board, hike the dividend 10-fold and boost the company’s ESG credentials. The board also had a plan to buy Kumho Resort, a hotel and golf course business. Park Chul-whan was defeated and the acquisition went ahead. However, in May 2021 Park Chan-koo resigned along with an executive director Shin Woo-sung in a move aimed at “facilitating the company’s transition toward professional management”.

Looking at some of the other holdings in more detail:

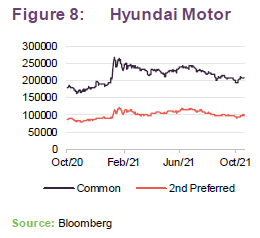

Hyundai Motor

Hyundai Motor (hyundaimotorgroup.com) is a leading global automotive manufacturer. It also owns around a third of Kia Motors. Hyundai sells electric vehicles under its Ioniq brand. Hyundai Motor aims to quadruple its EV sales from 258k in 2020 to over 1m in 2025 and is aiming for 8–10% market share in EVs by 2040. It also has a hydrogen fuel cell vehicle – the Nexo – in production and its subsidiary Hyundai Mobis is building two fuel cell plants in Korea. In 2020, in common with other automakers, Hyundai Motor’s business was impacted by COVID-19. Despite weaker sales in its home market and in China, globally sales are recovering – 2.926m vehicles were sold over the first nine months of 2021, up 12.3% on the prior year.

WKOF holds the 2nd preferred stock currently, which traded on a discount of 52.2% at the end of September (each of the three Hyundai Motor preference stocks is trading at a discount wider than 50%).

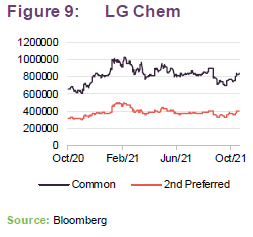

LG Chem

LG Chem (lgchem.com) is part of the wider LG Group which encompasses 68 affiliate companies operating across a broad range of sectors. LG Chem is one of the world’s largest chemical companies, manufacturing a wide range of products across three divisions: petrochemicals, advanced materials and life sciences.

In December 2020, the company spun out its battery business (the world’s leading manufacturer of automotive batteries) into a separate, but still wholly-owned company, LG Energy Solution. It also controls an agrochemical business, Farm Hannong.

LG Chem had sales of $26.4bn in 2020, almost half of which (48%) was accounted for by the petrochemicals division. Sales and profits are recovering from 2020’s COVID-related disruption. However, LG Energy Solution appears to have been impacted by the global semiconductor shortage.

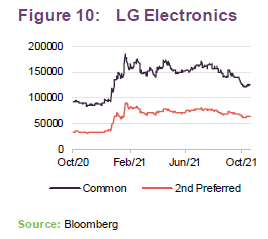

LG Electronics

LG Electronics (lg.com/global) produces a wide range of domestic appliances, home entertainment equipment, mobile communications, automotive components and business solutions (which includes displays and solar power modules).

Sales and profits are running well-ahead of comparable levels in 2020 as the business recovers from the effects of COVID-19. The recovery is strongest within its vehicle solutions division. However, the company says that rising raw material/component costs and semiconductor shortages are restricting profit growth.

The preference share dividend was increased substantially in 2020 over 2019 (KRW1250 versus KRW800). The company says that it will seek to maximise shareholder value by making dividends to the extent that they do not undermine the investment resources and financial soundness for the future.

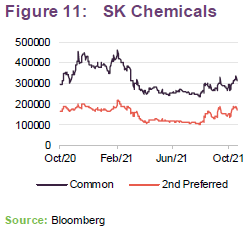

SK Chemicals

SK Chemicals (skchemicals.com/en/) describes itself as a green chemicals and life sciences company. Helped by the economic recovery and its vaccines business, sales and profits are growing significantly (up 51% and 388% year-on-year, respectively in Q2 2021).

The company’s copolyester business has been affected by rising raw materials prices. However, the SK Biosciences vaccine business (which already had a strong presence in areas such as influenza vaccines) has also been benefiting from its COVID-19 vaccine operations.

In March 2021, SK Chemicals adopted a new Governance Charter and IPOd SK Bioscience, retaining a 68.4% stake in that business. Strong share price performance by SK Bioscience since its IPO (it is trading at 3.4x the IPO price) has led to calls for SK Chemical to monetise more of its stake.

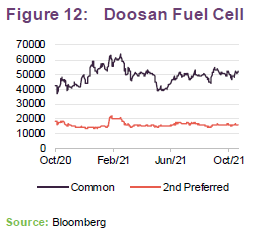

Doosan Fuel Corp

Doosan Fuel Cell (doosanfuelcell.com/en) is building stationary hydrogen fuel cells, mainly in Korea and the US. Development work is underway on producing fuel cells for the shipping industry (licensing solid oxide fuel cell technology from the UK’s Ceres Power) and commercial vehicles. 2020 sales were down on the previous year, impacted by a temporary hiatus in Korean orders over the past year. The company expects to see rebounding sales in H2 2021. The Korean government is prioritising the development of the hydrogen industry within the country. Since 2012, it has also implemented its Renewable Portfolio Standard (RPS) policy, under which large power producers must meet a minimum portion of their power generation from new and renewable technologies, including fuel cell power generation.

Performance

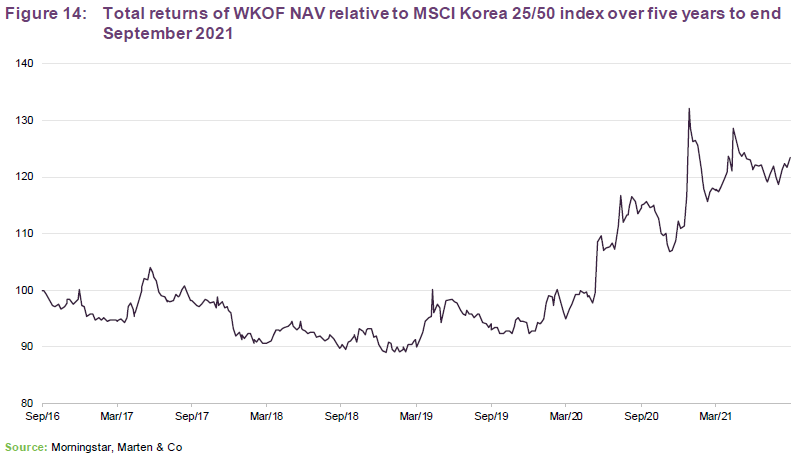

Since launch, WKOF has delivered material outperformance of the Korean market. Relative to its benchmark, the MSCI Korea 25/50 Index, its performance has been particularly strong since the start of 2020.

As Figure 13 shows, the Korean market has lagged the MSCI All Countries World Index by a considerable margin.

The manager believes that the attraction of the upside potential of the Korean market is compounded by the discount opportunity within WKOF’s portfolio.

WKOF sits within the AIC’s country specialist sector and is the only fund focused on the Korean market.

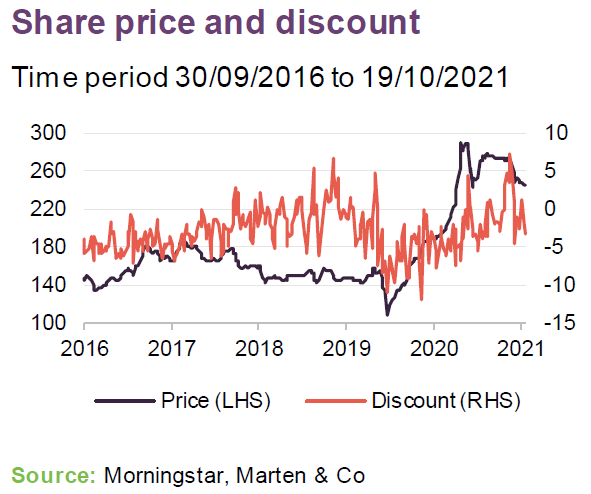

Discount

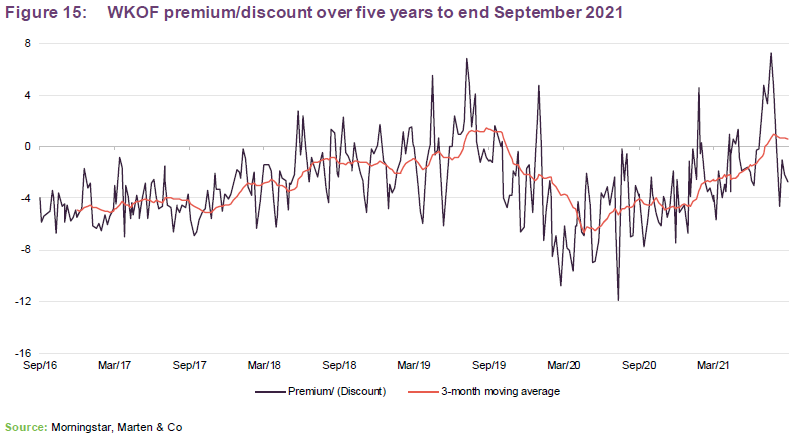

WKOF’s shares have traded fairly close to NAV over its life. The uncertainty created by the pandemic in March 2020 caused many discounts to widen across the whole investment companies market. WKOF appears to have brought its discount back under control, however.

Over the 12 months ended 30 September 2021, WKOF’s discount moved within a range of a 7.8% discount to a premium of 7.3% and averaged a discount of 2.1%. At 19 October 2021, based on Marten & Co’s estimate of WKOF’s NAV, WKOF’s discount was 3.3%.

Shareholders have granted the directors the authority to purchase in the market up to 40% of WKOF’s ordinary shares in issue from time to time. The directors seek annual renewal of this authority from shareholders at each AGM. Since inception WKOF has bought back 13,190,250 shares at an average discount of 6%.

In addition, as described below, WKOF offers its shareholders a realisation opportunity on a biennial basis.

The realisation opportunity

WKOF provides it investors with an opportunity to redeem all or some of their investment in the company at biennial intervals. Shareholders may elect to take advantage of the realisation opportunity. The portfolio is then split into continuation and realisation pools and the realisation pool is liquidated with the net proceeds returned to exiting investors.

The opportunity is presented every two years, with the last being in May 2021. Elections were received in respect of 11,710,750 ordinary shares (about 14.5% of the issued share capital). To date, 90% of shares designated as realisation shares in May 2021 have been redeemed.

In addition to the shares being bought back to satisfy the realisation opportunity, 600,000 shares were bought back at 286p on 27 January 2021.

Fund profile

Weiss Korea Opportunity Fund (WKOF) is the only UK-listed fund offering investors dedicated access to the South Korean stock market. It seeks to add value relative to that market by exploiting the valuation gap between the preference shares that make up substantially its entire portfolio and the common shares issued by the same companies.

Preference shares form part of the equity capital of many South Korean companies. They are generally entitled to receive the same dividends as the common shares but tend to have no voting rights. Generally, they rank alongside common equity in seniority (as opposed to a UK preference stock, which usually rank ahead of ordinary/common shares in their claim to dividends and capital). Korean preference shares often trade at a substantial discount to equivalent common shares. Consequently, an investment in WKOF offers access to South Korean companies at price-to-earnings ratios that are typically lower and dividend yields that are typically higher than an investment in their common shares.

The manager

Weiss Asset Management LP (Weiss), a Delaware limited partnership formed on 10 June 2003, is the company’s investment manager. Weiss is registered as an investment adviser with the SEC.

At the end of September 2021, Weiss had combined assets under management of approximately $2.7bn, including private investment funds with diversified strategies. Dr. Andrew Weiss, who founded the investment manager, has been managing private investment funds for over 29 years and the senior management team has been with the firm for an average of 15 years. The investment manager has a 32-strong investment team including seven people working in its Asian strategies team.

Weiss invests using proprietary value-based strategies, identifying opportunities from deep fundamental research and statistical analysis. The investment team works collaboratively and rigorous debate of investment decisions is encouraged.

Weiss has been successfully investing in emerging markets for more than 28 years, with 20 years of experience investing in Korea. Weiss has accumulated substantial expertise in Korea over that period, with regard to registration in Korea, relationships with local brokers, in depth trading and research analysis, and understanding of regulatory requirements. The investment team includes two Korean speakers.

Jack Hsiao is managing director and head of Asian strategies at Weiss. He joined the firm in 2008. Jack holds a BA in Economics from Harvard University. Ethan Lim is a portfolio manager within the Asian strategies team. He joined the team in 2015. Ethan holds an MS in Financial Engineering from Columbia University, and a BS in Mechanical & Aerospace Engineering and BA in Economics from Seoul National University.

The performance benchmark

WKOF compares its performance to the MSCI Korea 25/50 net total return index and iShares MSCI Korea UCITS ETF (both in sterling terms). The two comparators tend to move in tandem and therefore we have just used the MSCI index in this note. We have also added a comparison to the MSCI All Countries World net total return index (abbreviated throughout to MSCI ACWI). All returns are in sterling unless otherwise indicated.

At the end of February 2021, the MSCI Korea 25/50 Index had 106 constituents and covered approximately 85% of the free float-adjusted market capitalisation in Korea. It caps the exposure to the largest single issuer at 25% and the sum of the exposure to issuers accounting for more than 5% of total unadjusted market capitalisation of the index is capped at 50%.

Previous publications

Readers may wish to refer to our initiation note – A remarkable success story – which was published on 9 March 2021.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Weiss Korea Opportunity Fund.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.