Compelling three-year track record

Compelling three-year track record

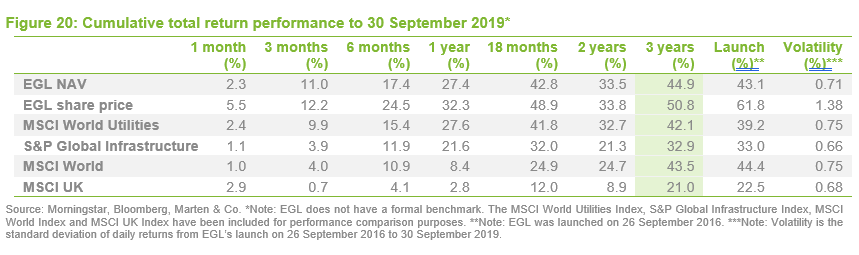

Ecofin Global Utilities and Infrastructure Trust (EGL) has just had its third birthday, and it has much to celebrate. Since launch, the trust has built a compelling track record (NAV and share price total returns of 44.9% and 50.8% respectively) while outperforming a range of comparable indices, including MSCI World Utilities, S&P Global Infrastructure, MSCI World and MSCI UK.

EGL has achieved this while providing an attractive dividend yield and less volatile returns than the MSCI World Index, and against a backdrop that has been challenging for the sectors it focuses on.

EGL has recently benefitted from increased investor awareness, following some high-profile press coverage, and its discount has moved in. However, for a number of reasons (see page 12), there is the potential that this could narrow further, to the point where the trust could start to expand, particularly if the manager continues to provide sector-beating returns.

Developed markets utilities and other economic infrastructure exposure

EGL seeks to provide a high, secure dividend yield and to realise long‐term growth, while taking care to preserve shareholders’ capital. It invests principally in the equity of utility and infrastructure companies which are listed on recognised stock exchanges in Europe, North America and other developed OECD countries. It targets a dividend yield of at least 4% per annum on its net assets, paid quarterly, and can use gearing and distributable reserves to achieve this.

Market outlook and valuations update

Recent history and valuations

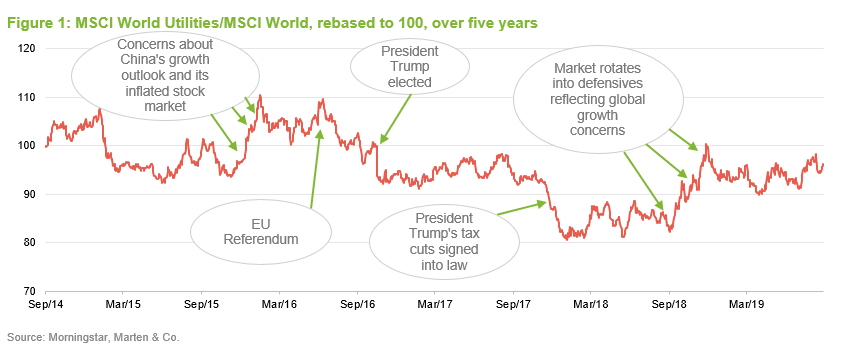

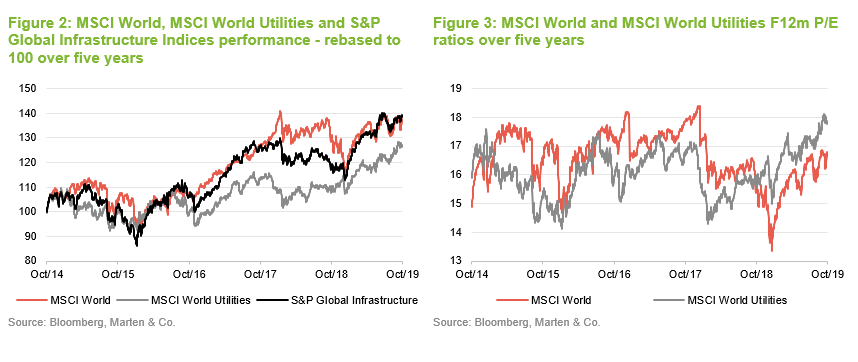

As illustrated in Figures 1 and 2, global utilities have experienced distinct periods of volatility but have broadly underperformed global equity markets during the last five years, even after staging a strong recovery during the last 18 months. These periods of under- and outperformance have been largely driven by economic and political factors, outweighing company fundamentals (a subject QuotedData has discussed in its previous notes – see page 15 of this note).

Aided by improved power prices, new investment in renewables and, in some cases, years of cost-cutting, earnings growth for utilities has generally been strong. Consequently, over the last 18 months, the increase in global utilities valuations (alongside stronger markets) has been driven by a combination of better earnings and higher valuation multiples. As illustrated in Figure 2, listed infrastructure shares have kept pace with the MSCI World Index on a five-year view, but have lagged over the last three years.

As is illustrated in Figure 3, valuations have increased and are now close to five-year highs, although in reality, valuations have held within the 14x – 18x Price/Earnings ratio (P/E) range and are not excessively above long-term averages. As at 1 October 2019, the MSCI World Utilities Index was trading at a F12m P/E (a P/E based on 12 months’ forward earnings) of 18.0x, versus its five-year average of 16.1x. As discussed in the manager’s view section overleaf, EGL’s manager, Jean-Hugues de Lamaze, believes that the earnings growth profiles for EGL’s sectors are good, particularly against the backdrop of a low growth world, and that earnings quality has also improved significantly. If so, this would suggest that a higher rating for utilities is justified and that they are well positioned to grow into this.

With signs of weakness in the global economy and, with an improving earnings outlook, utilities may become increasingly sought-after should the global economy continue to soften. Reflecting this economic weakness, interest rates have declined and sentiment towards utilities appears to have improved. (Note: interest rate rises are generally considered to be negative for equities but more so for utilities and infrastructure that tend to have higher levels of debt. Also, the relationship between changing interest rates and the impact on utilities is more complex than this. Readers interested in more detail on this topic should see pages 6 and 7 of QuotedData’s October 2018 note.)

Manager’s view – strong underlying fundamentals

Accelerating infrastructure spend

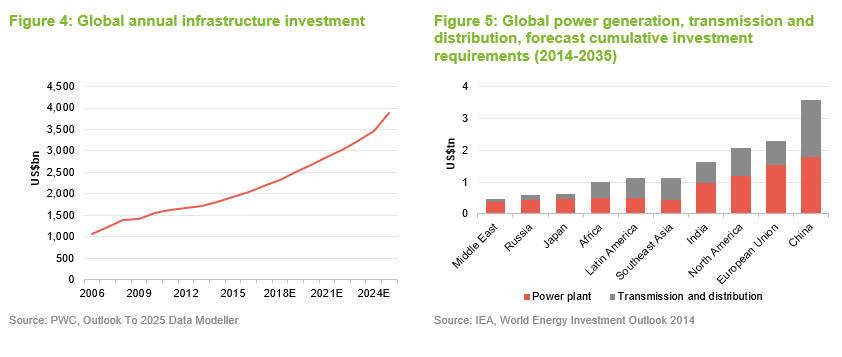

Global infrastructure spending, in both developed and emerging markets, is forecast to grow strongly over the next decade or more. The manager expects that this high demand will allow providers of capital for infrastructure investments to earn attractive returns.

In the developed world, the average age of infrastructure assets has been rising steeply in recent years, made worse by a period of austerity in the post financial crisis period. Increasingly there are calls to upgrade large swathes of transport, power, water and telecommunications infrastructure; to replace ageing kit; to adapt it to a changing technological environment, notably the expansion of renewable energy, and to support economic growth. Emerging markets, in comparison, already dedicate a large proportion of their GDP to developing infrastructure, but clearly further investment is required, as they are still unable to meet the needs of large proportions of their populations.

As discussed below, climate change and population growth are also creating their own challenges for society. Despite ever-increasing efficiency, the world needs to produce more energy in a cleaner way. This is driving spending to alter the energy mix (a reduction in dirtier fossil fuels with an increase in renewables and other ‘greener’ technologies, such as batteries, hydrogen and biogas).

Data from PwC’s ‘Outlook To 2025 Data Modeller’ suggests a marked acceleration in annual investment in utilities and transportation (power, water, roads, rail, airports and ports) infrastructure during the next few years (see Figure 4 overleaf). Data from the International Energy Agency’s World Energy Investment Outlook 2014 (see Figure 5) suggests that a significant portion of investment in power generation, transmission and distribution will occur in developed markets and China. As noted below, the manager generally favours the return/risk profile of opportunities available in developed markets over emerging. As is also explored in further detail below, he also considers that this growth in capex is a very positive trend. This is because capex is largely regulated and therefore guarantees a return on assets in his view.

The utilities sector is not a collection of bond proxies

QuotedData previous notes have discussed the view that investors have a tendency to treat utilities as a collection of proxies for bonds, given that they are both defensive and perceived as interest-rate sensitive. However, the sector is not uniform. It is actually a very diverse space comprising different businesses, with different strategies, including large integrated companies and companies with a more niche focus. Some companies can exhibit high levels of growth, while others are mature (Jean-Hugues comments that the dispersion of returns tends to be high). There is also considerable variation in the extent to which these businesses are regulated. In summary, Jean-Hugues thinks that it is far too simple to treat the space as a uniform collection of bond proxies. He cites the high growth available in the renewables space is a fitting example.

Energy transition is creating positive disruption

Within the portfolio, there is a strong focus on renewable energy generation. Jean-Hugues believes that utilities and infrastructure will be major drivers, investors and benefactors of the industry transformation as we move to a low carbon world. In terms of new capacity additions, renewables installation rates have overtaken that of fossil and nuclear. Wind and solar are expected to account for 48% of installed capacity and 34% of electricity generation globally by 2040 (these account for 12% and 5% respectively today). Given the global efforts to slow climate change, including the reform of the EU’s emission trading scheme, the manager expects fossil fuel power generation to trend lower in perpetuity. Renewables, in contrast, will trend higher and gain market share. The manager believes that this represents a major growth opportunity for EGL’s sectors.

Strength in regulated business models

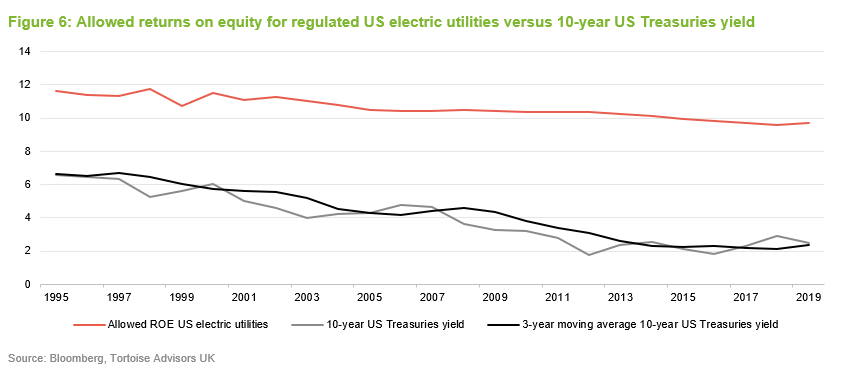

Jean-Hugues believes that regulated business models offer stable and above average growth in a deflationary environment. Figure 6 shows the allowed return on equity for regulated US electric utilities against the yield on 10-year US Treasuries and its three-year moving average.

Reflecting low interest rates and the deflationary environment, companies have seen allowed returns trend down over time. However, as illustrated in Figure 6, the permitted return on equity has been relatively stable and significantly above the yield available on US Treasuries (utilities have benefitted both from cost efficiencies and a falling cost of debt).

Earnings growth momentum

Periodically, the manager analyses the dividend growth profile of EGL’s portfolio (forecasts are prepared on a stock-by-stock basis). The portfolio yield is currently in the region of 4.1% (unadjusted for the effects of gearing returns with borrowings) and dividends from companies in the portfolio are expected to grow at a compound rate of over 5% per annum over the next 2-3 years. Jean-Hugues believes that underlying earnings momentum is solid and that this will continue to drive improvements in cash flows and dividends.

The manager says that deleveraging (paying down debt) within the utilities space, over the last 10 years, has helped to put its free cash flows in positive territory, while credit ratings have improved as the sector has focused on less volatile activities. He reiterates that this profile helps him to feel confident about reaching the trust’s long-term total return target of 6-12% per annum.

Higher power prices in Europe

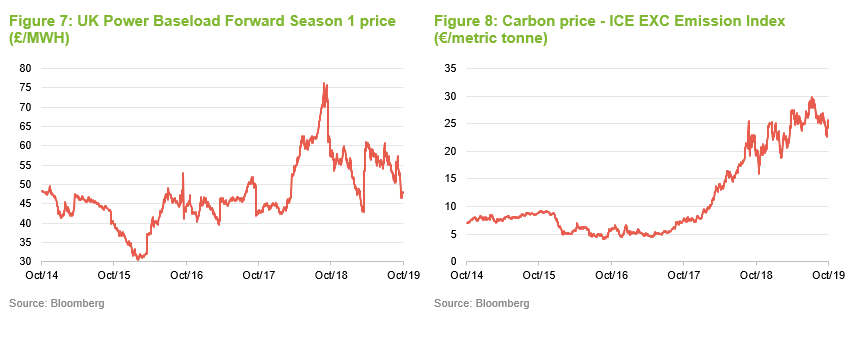

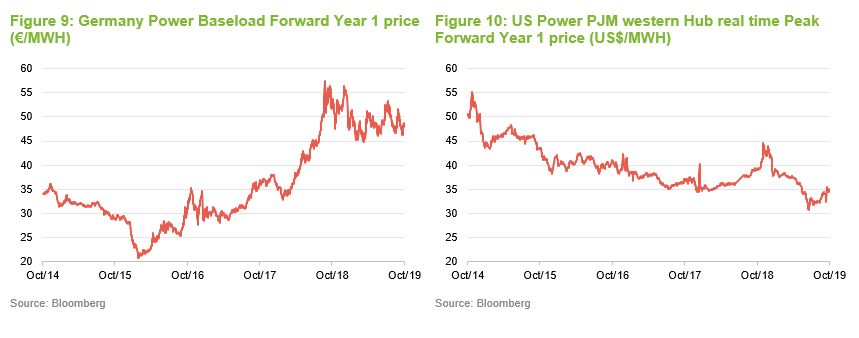

As discussed in some detail in QuotedData’s October 2018 annual overview note (see pages 8 and 9 of that note), power prices increased meaningfully during 2018 and, whilst they are below their September 2018 peak, the trend of higher power prices has continued in Continental Europe (see Figure 9) and to a lesser extent the UK (see Figure 7). The primary drivers were rising commodity prices and a reform of the EU’s emission trading system (EU ETS), which has led to a higher carbon price (see Figure 8). Higher power prices benefit all power producers, but it is highly beneficial to the fixed-cost producers (for example, renewables and nuclear generators) who see the full benefit drop through to their bottom lines. As Figure 10 illustrates, US power prices also rose in the second half of 2018 but have since retreated.

Mergers and acquisitions

In QuotedData’s March 2018 note, it was noted that Jean-Hugues believed that E.ON’s acquisition of the controlling stake in Innogy from RWE could trigger a phase of merger and acquisition activity across Europe, having seen a decade with hardly any such transactions in the space (the larger players’ balance sheets were previously too indebted to finance these deals). 2018 saw a record number of transactions and Jean-Hugues thinks this trend could continue. While this is not a driver in stock selection, he nonetheless thinks that some of EGL’s holdings are potential takeover candidates and that, if the path of increasing merger and acquisition activity continues, this could be very beneficial for the trust.

Cautious on emerging markets

Jean-Hugues remains cautious on emerging markets. He says that there are lots of names in China, with good growth outlooks, but these are nonetheless challenging in a number of respects; the trade war with the US poses a significant risk, for example. There are obviously exceptions and EGL’s participation in the IPO of Neoenergia (see page 10) is one of them. However, given the opportunities currently available in developed markets, Jean-Hugues does not consider that EGL needs to focus heavily on emerging markets to get access to good growth.

Asset allocation

Portfolio activity

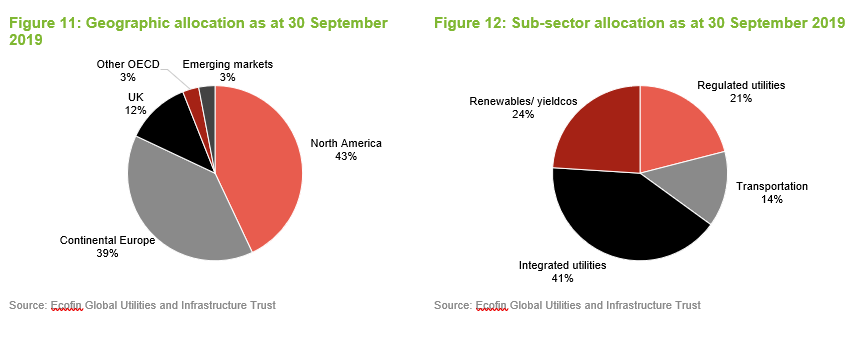

Since QuotedData last published on EGL in April 2019, the changes to EGL’s geographical allocations have been modest: Comparing EGL’s exposures at the end of September 2019 and the end of March 2019 (the most recently available data when QuotedData last published), EGL’s exposures to North America and emerging markets have increased slightly at the expense of Continental Europe and the UK. The allocation to renewables has increased with integrated utilities and transportation falling at the margin. The number of holdings as at the end of September 2019 was 43, an increase of three relative to the end of March 2019.

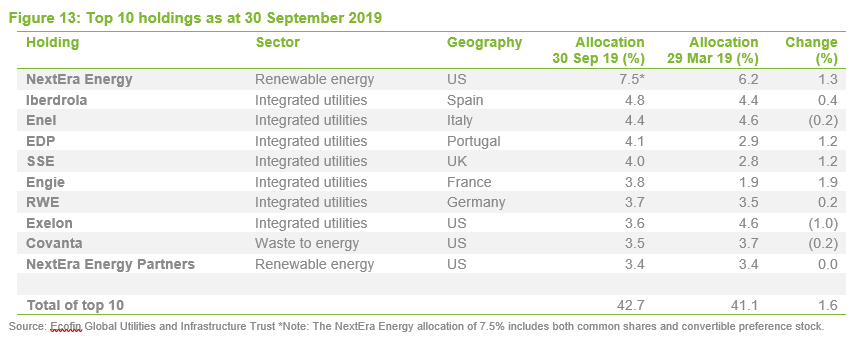

Figure 13 shows EGL’s top 10 holdings as at 30 September 2019 and how these have changed since 29 March 2019 (the most recently available data when QuotedData last published). New entrants to the top 10 are EDP, SSE and Engie. Names that have slipped out of the top 10 are EDF, Terraform Power (the manager has been selling Terraform down following a strong price performance) and National Grid. Some of the more interesting changes are discussed in the following pages. Readers interested in other names in the top 10 should see QuotedData’s previous notes, where many of these have been previously discussed (see page 15 of this note). Jean-Hugues has also initiated positions in Neoenergia and Atlas. He highlights that, while a significant proportion of the top 10 holdings come under the banner of integrated utilities, most are highly orientated towards renewable generation and are very large investors in the infrastructure required to modernise grid networks to accommodate renewables.

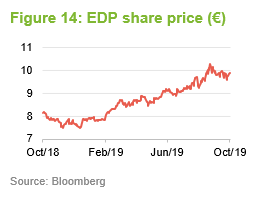

EDP (3.9%) – shareholders scuppered CTG bid

EDP (http://www.edp.com) is a Portuguese electric utilities company headquartered in Lisbon. It is Portugal’s dominant power company and a global leader in renewables generation. On 11 May 2018, China Three Gorges Group (CTG – a Chinese state-owned power company and a significant shareholder in EDP) made an offer for EDP of €3.26 per share for the 76.7% share of EDP that CTG did not already own, which valued EDP at €9bn. The offer was rejected as being low (the bid was a 4.8% premium to the closing price on the day of the offer).

Jean-Hugues believes that EDP has more value than the market ascribes to it. He felt, in common with the company’s board and other shareholders, that the Chinese bid was opportunistic and undervalued the company (EDP said that the premium was “significantly below what is customary for cash transactions in the European utilities sector”). Overall, Jean-Hugues felt that the offer was not attractive and voted against the resolution to remove the 25% voting right limit proposed at a company meeting in April 2019, which was required for the offer to proceed (it is worth noting that the manager is not an activist, but will make its views very clear to companies).

The resolution failed, scuppering the takeover, and CTG withdrew from the process. Jean-Hugues says that, because of the failure of the Chinese bid, EDP is now one of the cheapest utilities in Europe.

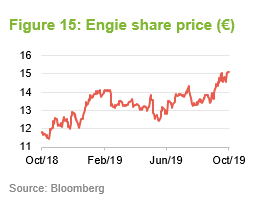

Engie (3.8%) – Q2 2019 saw a significant recovery

Formerly known as GDF Suez, Engie (http://www.engie.com) is a French multinational utility company that has three core businesses: power (electricity generation and distribution), gas and energy services. Its electricity business has both thermal (fossil fuel powered) and renewable power-generation plants. These include solar, hydropower, offshore wind power, biomass, onshore geothermal, traditional thermal and nuclear, and benefit from low CO2 emissions.

Engie’s gas business is Europe’s largest. It has invested €800m in developing green gases during the last five years and aims to have at least 10% of its gas derived from green sources by 2030. This includes biogas; it has 48 biogas projects in France and another 80 projects globally. Its energy services business provides a range of services; energy efficiency, urban heating and cooling networks as well as energy solutions for cities.

Jean-Hugues considers that Engie is well-positioned to take advantage of the move to a low carbon economy. The company’s results for the first quarter of 2019 disappointed the market (Engie suffered from above-average winter temperatures in France, lower nuclear power production in Belgium and, in its client solutions business, a slower start than in the previous year) and its share price struggled as a result. Jean-Hugues, convinced that both the quality of the company and that the issues were temporary, topped up the holding and EGL benefitted as the stock recovered. Engie had a much better second quarter driven by strong energy management, a recovery in its Belgium nuclear operations and an improvement in client solutions. Its share price responded, pushing the stock back up EGL’s rankings.

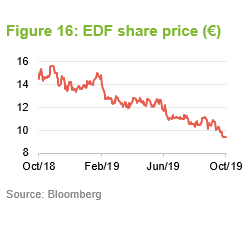

EDF Group – suffered from negative news flow

EDF (http://www.edf.fr) is a French multinational electricity utility company that, like Engie, has a focus on low-carbon electricity generation. However, the bulk of this is nuclear (78% for 2018) with hydropower (9%), other renewables (3%), combined cycle gas and cogeneration (8%), coal (4%) and oil-fired (1%) making up the balance.

QuotedData last discussed EDF in its November 2017 note. At that time, Jean-Hugues had used a share price setback to initiate a significant position. Having previously been cautious on EDF, he believed that significant bad news had been discounted into the share price (for example, unfavourable pricing context in France, issues at Framatome, risk of nuclear closures and uncertainties on EPR (pressurised water nuclear reactor) developments including Hinkley Point). Jean-Hugues also considered that, of all of the major utilities, EDF had the highest sensitivity to power prices and carbon prices, (it benefits as these rise), and felt that these could rise if the EU was able to reform its Emission Trading Scheme. As discussed in QuotedData’s October 2018 note (see pages 8 and 9 of that note), this reform passed with carbon and power prices moving up significantly as a result.

However, as illustrated in Figure 16, EDF’s share price has faced continued downward pressure during the last 12 months, which has ultimately served to push it out of EGL’s top 10 holdings. EDF’s UK profits were weak in the first half of 2019; the European Parliament decided to exclude nuclear from the list of investments that can benefit from the EU’s green investment label in June 2019, and reports emerged in September 2019 that six of its reactors contained components that failed to meet manufacturing standards (this includes a new-generation reactor that is being constructed at Flamanville in Normandy and is of the same design as the reactor at Hinkley Point in Somerset).

Jean-Hugues acknowledges the challenges that EDF is facing but considers that the company will work through the difficulties it is experiencing with its new nuclear reactors (three, including Hinkley Point, are overdue and overbudget). The company has also announced that it does not expect to have to halt production to replace components in those plants with the components that did not meet manufacturing standards. Overall, Jean-Hugues thinks EDF’s formal restructuring plan, including a potential nuclear regulatory reform, could add value to the company.

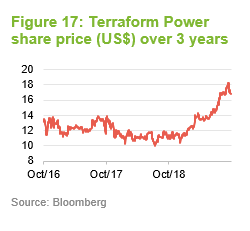

Terraform Power – position reduced into strength

Terraform Power (http://www.terraform.com) is a renewable power generation company that owns a portfolio of solar and wind assets in North America (including Mexico) and Western Europe (there is a bias towards the US, which accounts for 2.4GW or 65.5% of Terraform’s installed capacity). Its portfolio totals some 3.7GW of renewable generation capacity, which is split 64% wind/36% solar. It has ambitions to grow further, both through the development of new plants and the acquisition of new facilities. It aims to grow its dividend per share by 5-8% per annum.

Since Brookfield Asset Management took over the management of the company’s portfolio in 2017, significant progress has been made in both increasing its scale, generating improved economies of scale, and enhancing existing asset value. Jean-Hugues thinks that Terraform is a high-quality company with good assets that is very well positioned to benefit from growth in wind and solar as the world moves towards a low-carbon economy. It has strengthened its balance sheet, increasing debt maturities and lowering its interest costs, and has achieved credit rating upgrades. Despite this, Jean-Hugues has reduced EGL’s position into this strength and has used the cash to fund a holding in Pattern Energy.

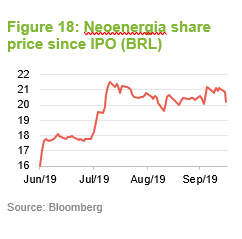

Neoenergia – Brazilian power has lots of growth potential

Neoenergia (http://www.neoenergia.com/en-us) is a Brazilian power company. In terms of electricity distribution, it is the second-largest in Brazil and, in terms of number of customers (it serves 34m people), the largest in Brazil and one of the largest in Latin America. Its operations cover distribution, transportation, generation (both conventional and renewable) and energy commercialisation. It operates in 18 Brazilian states and manages 13.9m supply points in a concession area covering 840,000 square kilometres. Spain’s Iberdrola is Neonergia’s largest shareholder; it has control of the company.

Neoenergia listed on the São Paulo Stock Exchange on 1 July 2019. EGL participated in the IPO, securing a small position that accounts for about 1% of its portfolio.

Whilst Jean-Hugues was pleased to receive an allocation for EGL, he would have liked more. He knows the management of the parent company, Iberdrola, well and believes that the company has lots of growth potential (Brazil needs lots more power distribution). He says that Brazil also has a relatively stable and generous regulator that allows companies to earn good rates of return (the regulator appears to accept that private capital is needed and must be appropriately incentivised). The new government in Brazil is pro-economic development and pro-business, and Brazil is also cutting interest rates. Jean-Hugues comments that EGL’s exposure to emerging markets is very low (Neoenergia is one of three holdings that, collectively, account for less than 5% of EGL’s portfolio).

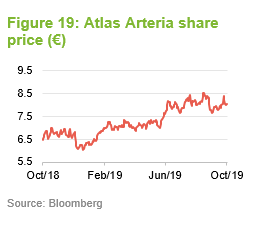

Atlas Arteria – scarce assets and well positioned for growth

Atlas Arteria (http://www.atlasarteria.com), formerly known as Macquarie Atlas Roads, is a large developer and operator of private toll roads globally. It has a portfolio of toll roads in France, Germany and the US. These are:

• A 25% indirect interest in the ARRR, a 2,318km motorway network located in Eastern France. It comprises three concessions: the APRR Concession (1,891km), the AREA Concession (408km) and a minority interest in the ADELAC Concession (20km), which expire 30 November 2035, 30 November 2036 and 31 December 2060 respectively. Tolls for the ARRR and APRR concessions escalate annually in February by 70% of the French inflation rate as measured by CPI. The ADELAC Concession benefits from February toll increases at French CPI plus a fixed (undisclosed) percentage. The ARRR may also benefit from supplemental toll increases as agreed with the French state (click here to see Atlas Arteria’s APRR factsheet) (click here to see Atlas Arteria’s ADELAC factsheet).

• A 100% interest in the Dulles Greenway, a 22km toll road in north Virginia, with three lanes in each direction, connecting Leesburg to Washington D.C. through Loudoun County. Atlas says that the Dulles Greenway is part of a key route in one of the fastest growing and most affluent counties in the US, connecting Dulles International Airport through Loudoun County to Leesburg, Virginia. It anticipates that, as Loudoun County continues to grow, the Greenway will be well positioned to provide capacity, a quality service and attract a greater share of future corridor growth, with the ability to expand to meet future demand. The concession expires on 15 February 2056. Through to 2020, the tolls escalate annually at the higher of CPI + 1%, real GDP growth or 2.8%. Post 2020, the tolls are set by the Virginia State Corporation Commission (click here to see Atlas Arteria’s Dulles Greenway factsheet).

• A 100% interest in the Warnow Tunnel, Rostock, Germany. The Warnow Tunnel is a 2.1km toll road, including a 0.8km tunnel under the Warnow River with two lanes in each direction. The tunnel, which opened to traffic in September 2003, allows road traffic to cross under the Warnow River which divides Rostock. The concession expires on 12 September 2053. It permits toll increases that are linked to the internal rate of return on the project’s pre-tax equity. At the time of investment, Rostock was the largest of seven Baltic ports and the fourth-largest German port. It has a roll-on roll-off freight and passenger ferry port for Baltic shipping, a bulk port, cruise ship terminal (which can accommodate up to five ships a day in the summer peak) as well as a growing bulk retail centre (click here to see Atlas Arteria’s Warnow Tunnel factsheet).

Atlas is a new addition to EGL’s portfolio. Jean-Hugues considers that it has very valuable assets, that are difficult to gain exposure to; it has benefitted from a major cost cutting programme, has a good dividend yield (approximately 5%) and is well positioned for growth (the plan is to bid on new assets, with significant growth expected in its US portfolio). Jean-Hugues believes it can provide double-digit growth over the next five years and that the company could be of strategic value to a private equity buyer. He says that over 90% of infrastructure assets are held privately, hence their scarcity in listed markets. There can be a significant premium when such assets are taken private.

Performance

Now with compelling three-year track record

As discussed on the front page of this note, EGL had its third birthday on 26 September 2019, and so it now has a three-year performance track record. As discussed in the discount section (see page 12), this is a valuable milestone for any investment fund to pass; for some investors the lack of a three-year performance track record can be an impediment to investment, and so reaching this stage with a strong record of performance opens the door to a wider pool of investors.

EGL’s NAV and share price total returns have outperformed all of the indices provided over the three-year period. That is, it has outperformed the MSCI World Utilities Index, the S&P Global Infrastructure Index, the MSCI World Index and the MSCI UK Index. Outperformance of the S&P Global Infrastructure Index and the MSCI UK Index are particularly strong. In the case of the former, infrastructure assets decoupled from utilities, which continued to perform well (especially in the US) following the Morandi Bridge disaster in August 2018 (a topic QuotedData has discussed in its previous notes – see page 15 of this note). In the case of the latter, the UK market has been impacted by the Brexit process.

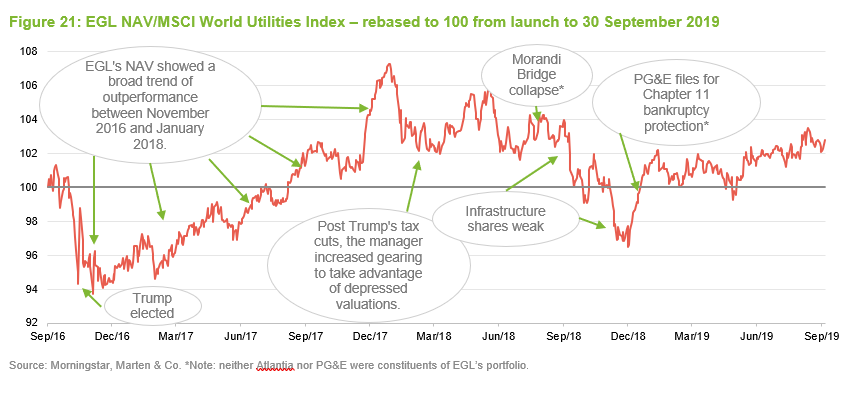

It should be noted that this outperformance has been achieved during a period in which the sector has faced various headwinds. For example, the utilities and infrastructure sectors suffered as investors rotated towards growth stocks in the aftermath of President Trump’s election. These sectors subsequently recovered but suffered heavily at the beginning of 2018 as investors once again rotated towards growth stocks, following President Trump’s tax reforms. As noted above, infrastructure de-rated following the Morandi Bridge disaster in August 2018, as investors became concerned about the risk of rare but extreme events within infrastructure assets given their long lives. The sector also suffered in the aftermath of the bankruptcy of the Californian utility PG&E in January 2019 (it should be noted that Jean-Hugues had avoided investment in both Atlantia S.p.A., which held the concession that included the Morandi Bridge – see pages 3 and 4 of QuotedData’s April 2019 update note, and PG&E). A further point of note, when inspecting Figure 20, is the consistent way in which the NAV has grown.

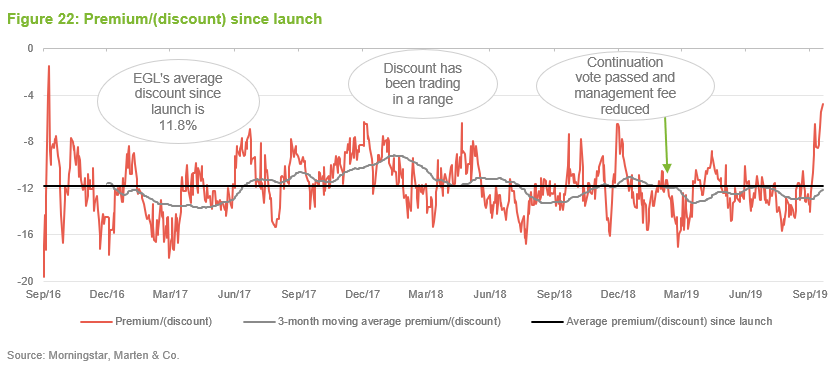

Discount/premium

Since launch, the manager and board have been frustrated by the stubbornness of EGL’s discount. As QuotedData has commented in its previous notes, the discount level has been somewhat out of step with the strong NAV performance, efforts by the manager and board to raise the profile of the trust, the continuation vote passing and the implementation of a 25 basis point (0.25%) reduction in the management fee (this took effect from 5 March 2019 – see page 11 of QuotedData’s April 2019 update note).

As illustrated in Figure 22, EGL’s discount has tended to trade in a distinct range and has demonstrated a tendency to move back towards its long-term average level. The discount has tended to narrow and widen as the trust’s sectors have moved in and out of favour. It is possible that, given the advanced stage of the economic cycle, the trust could find itself the beneficiary of increased investor interest as investors look towards more defensive exposures. There is evidence that the market might be starting to appreciate this.

The manager also considers that the growth elements inherent in infrastructure, including utilities, at this juncture, may become a key attraction that serves to stimulate interest in EGL’s shares and ultimately narrow the discount.

The trust has recently benefitted from some high-profile coverage that has helped raised awareness amongst investors, stimulating demand for EGL’s shares and narrowing its discount. As a consequence, EGL’s discount stood at 4.8% on 14 October 2019, having been 12.5% a month earlier. This lower discount is still wider than the board would like or expect it to be but, for the reasons outlined above, there is the potential that this could narrow further, particularly if the manager provides attractive sector beating returns.

EGL’s discount reached a 12-month high of 17.4% on 21 March 2019. The current discount of 4.8% is markedly below this and close to an all-time low.

As noted in the performance section of this note (see page 12), EGL now has a three-year track record of compelling performance. For some investors, a three-year track record is a prerequisite for making an investment and passing this milestone expands the pool of potential buyers for EGL’s shares. This too could lead to further narrowing of the discount.

Fund profile

Developed markets utilities and infrastructure exposure with an income and capital preservation focus

Ecofin Global Utilities and Infrastructure Trust Plc is a UK investment trust listed on the main market of the London Stock Exchange (LSE). The trust invests globally in the equity and equity-related securities of companies operating in the utility and other economic infrastructure sectors. EGL is designed for investors who are looking for a high level of income, would like to see that income grow, and wish to preserve their capital and have the prospect of some capital growth as well.

EGL has a strong focus on capital preservation.

Reflecting its capital preservation objective, EGL does not invest in start-ups, small businesses or illiquid securities, as these may involve significant technological or business risk. Instead, it invests primarily in businesses in developed markets, which have ‘defensive growth’ characteristics: a beta less than the market average (beta is a

measure of the volatility of a security or a portfolio in comparison to the market as a whole); dividend yield greater than the market average; forward-looking earnings per share growth; and strong cash flow generation.

It also operates with a strict definition of utilities and infrastructure as follows:

• Electric and gas utilities and renewable operators and developers – companies engaged in the generation, transmission and distribution of electricity, gas, liquid fuels and renewable energy;

• Transportation – companies that own and/or operate roads, railways, ports and airports;

• Water and environment – companies operating in the water supply, wastewater, water treatment and environmental services industries.

EGL does not invest in telecommunications companies or companies that own or operate social infrastructure assets funded by the public sector (for example, schools, hospitals or prisons).

No formal benchmark

EGL does not have a formal benchmark and its portfolio is not constructed with reference to an index. However, for the purposes of comparison, EGL compares itself to the MSCI World Utilities Index, the S&P Global Infrastructure Index, the MSCI World Index and the All-Share Index in its own literature. QuotedData is using a similar approach here, but are using the MSCI UK Index to represent the UK market. Of the three indices, the MSCI World Utilities is arguably the most relevant – although it should be noted that this index has a strong bias towards US companies.

Strategy has room to grow

EGL had a market capitalisation of £148.8m as at 15 October 2019. The manager believes that its strategy could easily be applied to a much larger fund and its defensive growth characteristics should prove attractive to investors. Expanding the size of the trust should, all things being equal, have the dual benefits of further reducing the ongoing charges and improving liquidity in EGL’s shares.

Previous publications

Readers interested in further information about EGL may wish to read QuotedData‘s previous notes by clicking the links. Structural growth, low volatility and high income (published in May 2017); Delivering the goods (published in November 2017); On the contrary (published in March 2018); Staying nimble (published in October 2018); and Unrecognised outperformance (published in April 2019).

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Ecofin Global Utilities and Infrastructure Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.