Bright long-term future

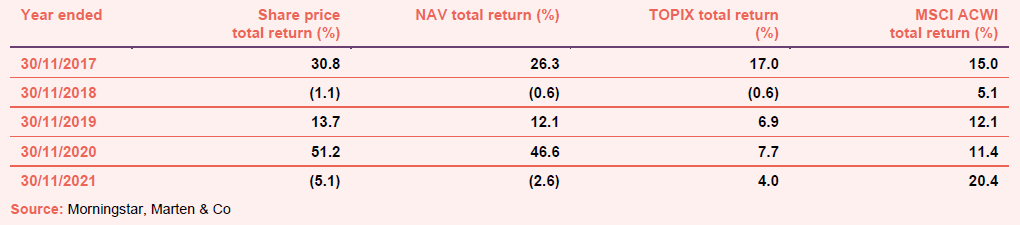

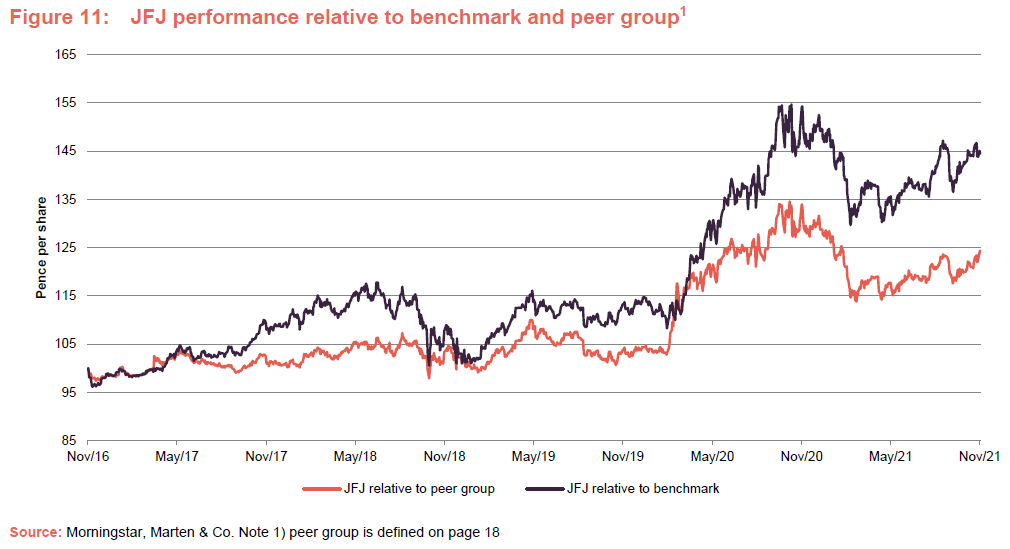

JPMorgan Japanese Investment Trust (JFJ) had an impressive run of both absolute and relative (to its benchmark index and to competing trusts) performance going into and during the worst of the pandemic. However, once vaccines became a reality, the share prices of businesses that had struggled during lockdowns surged. These were often the types of company that the managers would not consider for JFJ’s growth- and quality-focused portfolio. Consequently, over the past 12 months, JFJ has produced decent returns, surpassing £1bn in assets, but has given up a little of its outperformance of its benchmark.

The management team of Nicholas Weindling and Miyako Urabe is unfazed by this. They make the compelling argument that an investor in JFJ is backing the companies that are set to disrupt and revitalise Japan’s sclerotic economy, which are also capable of compounding their earnings sustainably over the long term. The long-term future is bright.

Capital growth from Japanese equities

JFJ aims to produce capital growth from a portfolio of Japanese equities and can use borrowing to gear the portfolio within the range of 5% net cash to 20% geared in normal market conditions.

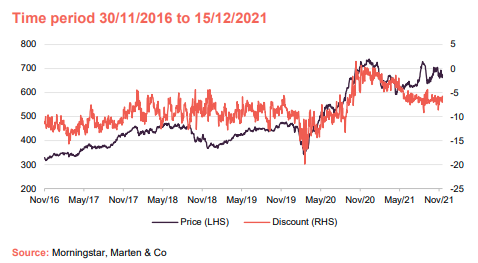

Share price and discount

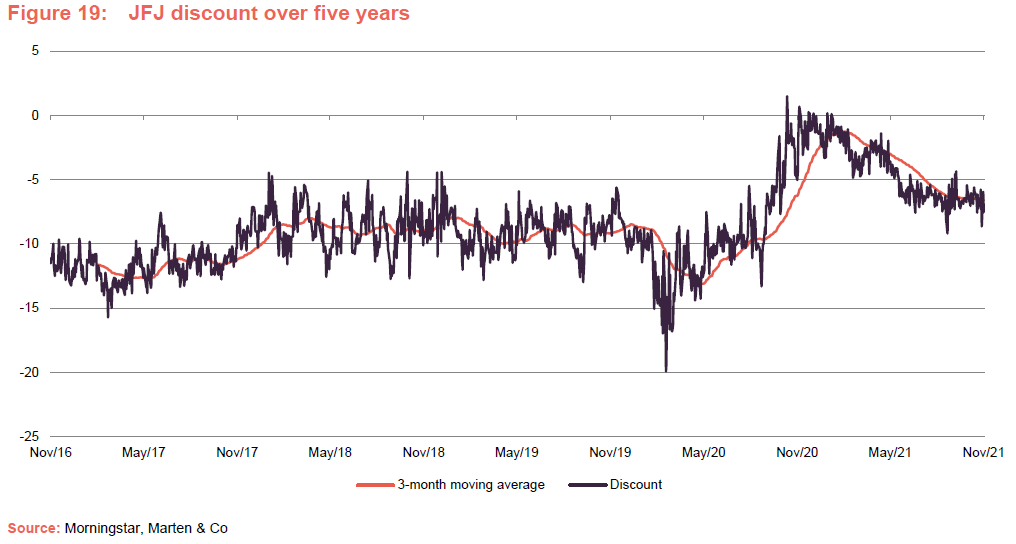

Over the 12 months to the end of November 2021, JFJ’s discount to net asset value (NAV) moved within a range of 9.2% discount to a premium of 0.7% and averaged 4.2%. At 15 December 2021, the discount was 5.9%.

The board monitors the discount closely and has both stepped up efforts to market the trust and authorised share buy backs.

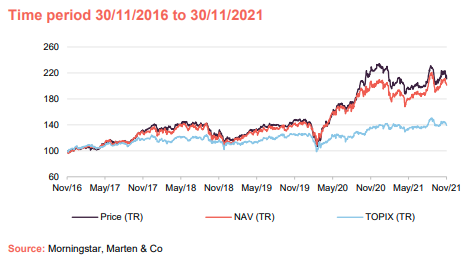

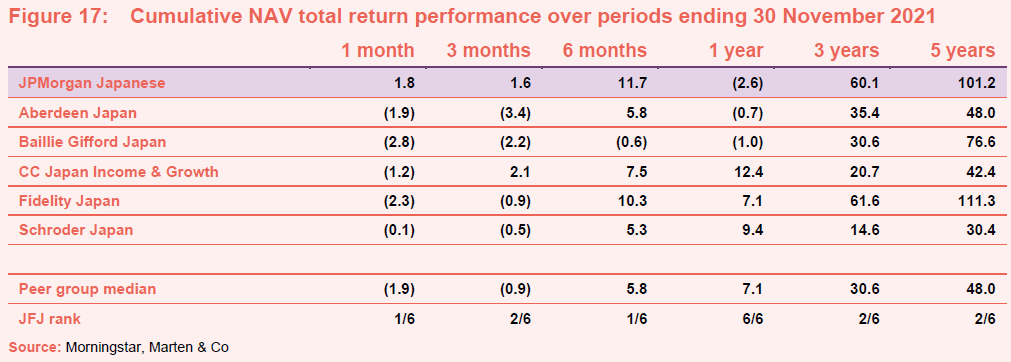

Performance over five years

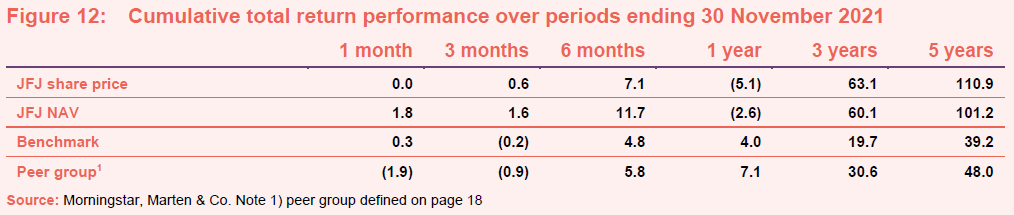

Even though JFJ gave back some of its relative outperformance of its benchmark and its peer group between November 2020 and March 2021, performance is on an improving trend once again.

Fund profile

JPMorgan Japanese Investment Trust (JFJ or the trust) aims to achieve capital growth from investments in Japanese companies. For performance monitoring purposes, the trust is benchmarked against the returns of the Tokyo Stock Exchange First Section Index (commonly known as TOPIX) in sterling.

The trust makes use of both long- and short-term borrowings with the aim of increasing returns.

Day-to-day investment management activity is the responsibility of JPMorgan Asset Management (Japan) Limited in Tokyo. The co-investment managers are Nicholas Weindling, who has had responsibility for JFJ’s portfolio for more than a decade, and Miyako Urabe, who was appointed co-manager in May 2019. They are supported by a well-resourced team of 30 investment professionals in Japan.

The investment emphasis is on identifying high-quality companies that are capable of compounding their earnings sustainably over the long term. That means investing in companies in growing industries that have strong balance sheets and are resilient in the face of macro-economic issues.

The managers recognise that JFJ’s performance may lag its benchmark in periods of market exuberance, triggered by an uptick in growth prospects – as was the case following the vaccine announcements last November, for example. However, the managers prefer to focus on identifying attractive stocks rather than attempting to time markets. Similarly, the trust’s gearing (borrowing) level is driven by availability of attractively priced stocks, not by macroeconomic considerations.

Benefitting from local knowledge

The investment team is based in Tokyo, where JPMorgan has had an office since 1969. Nicholas says that it is now relatively unusual for non-domestic asset managers to have a physical presence in Japan. Visiting companies is an integral part of the team’s investment process, but the pandemic has made it hard for anyone based outside the country to do likewise.

The team is 25-strong and is a mix of fund managers and analysts – roughly half and half. In addition, one of the strengths of the business is that the managers can also draw on the expertise of JPMorgan’s analytical teams around the world. This helps with competitive analysis, for example – it can also help identify trends on which Japan is behind the curve.

Results for the year ended 30 September 2021

JFJ recently published results covering the 12-month period ended 30 September 2021.

Over the trust’s financial year, JFJ generated a return on NAV of 10.7% and a return to shareholders of 11.0%. This contrasts with a return of 15.3% for the trust’s benchmark – the Tokyo Stock Exchange First Section Index (TOPIX) (all in total return terms). The good news on vaccines in November 2020 triggered a recovery in stocks that had been hit hard by restrictions imposed to tackle the pandemic. These were often not the sorts of stocks – department stores and railways, for example – that would be found in JFJ’s portfolio.

The discount narrowed from 7.0% at the end of September 2020 to 6.8% at the end of September 2021. The trust bought back around 2.9m shares at a cost of £18.6m. The board says that it recognises that a widening of, and volatility in, the company’s discount is seen by some investors as a disadvantage of investments trusts. It has restated its commitment over the long run to seek a stable discount or premium commensurate with investors’ appetite for Japanese equities and the company’s various attractions.

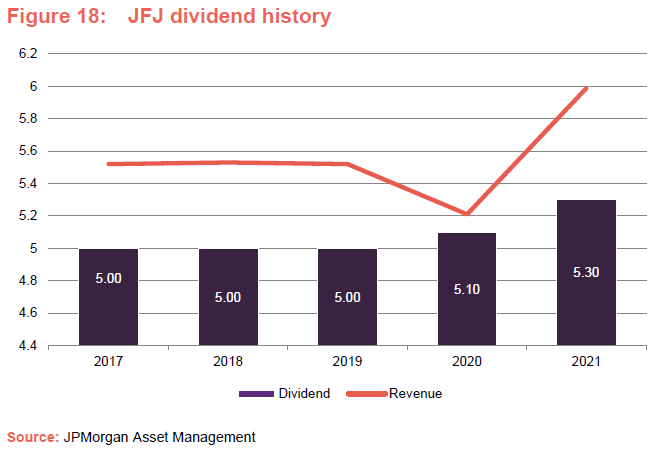

The trust’s annual dividend was increased from 5.1p to 5.3p and this was covered by earnings of 6.0p. Income is a by-product of the investment approach and stocks are not held for the dividend yield. The board aims to pay out the majority of the revenue available each year.

The ongoing charges ratio fell to 0.61% from 0.65%, aided by rising net assets. We look at JFJ’s charging structure on page 20.

JFJ’s relative performance has been on an improving trend since about March 2021. Since the period end, the trust has proven resilient in a weaker market and the NAV and share price have both held up much better than the benchmark. We look into performance in more detail on page 16.

Manager’s view

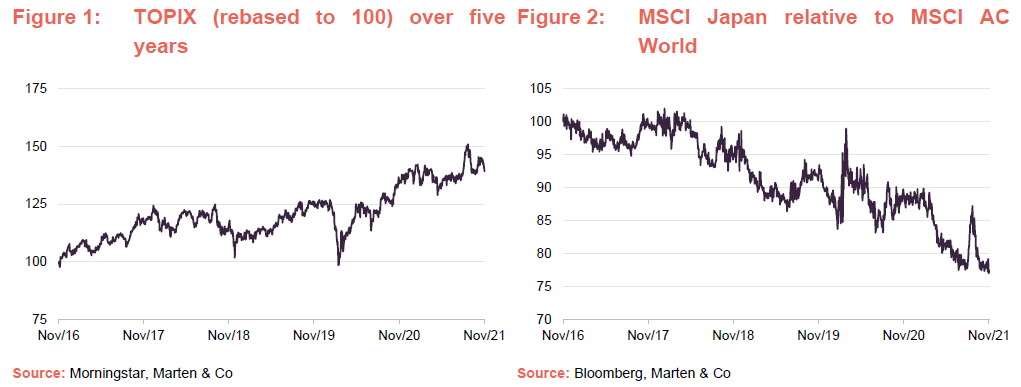

Figure 1 shows the performance of TOPIX – JFJ’s benchmark index over the past five years. Figure 2 shows the degree to which Japanese stocks have been underperforming relative to global peers.

The dominant factor affecting markets is COVID. In Japan, cases are running at about 150 per day, far fewer than in the US and Europe. Nicholas says that everyone is complying with mask-wearing everywhere, which may be a factor in this. The borders are not shut, but after a brief period where entry was open to non-nationals (on the basis of strict quarantine restrictions), they are now only open to nationals and foreign residents. In previous reports we noted the criticism that Japan attracted for the slow rollout of its vaccination programme. After a determined effort, the full vaccination rate is now the highest in the G8 – a great improvement.

While he would obviously have liked JFJ to do better, Nicholas is sanguine about this year’s relative performance. 2019 was a good year because, in an environment of low growth, JFJ owned businesses in structural growth sectors. 2020 started off very well when COVID hit, because their companies had strong balance sheets and were of good quality. They also had very little exposure to companies impacted by lockdowns such as travel and high street retail, for example. Things got even better because they were able to pick up some attractively priced stocks close to the bottom, such as Tokyo Electron and Nomura Research Institute, and then COVID accelerated the process of structural change in areas such as ecommerce which benefited a number of companies in the portfolio.

When the vaccines were approved, there was a bounce in sectors that had been hit by COVID – railways, department stores, banks and beverages, for example – but the managers stuck to their approach. From the second quarter of the year (Q2) onwards, JFJ’s relative performance has been better. The managers say that corporate earnings are visibly recovering. Resurgent global cases of COVID-19 – on the back of Omicron – may have an impact. However, in the managers’ view the petering out of the ‘value’ rally relates more to concerns about inflation in the US and higher rates than to COVID.

Japanese inflation remains low. Raw material – hard and soft commodities – and energy price increases are squeezing margins for some companies, but the economy is accustomed to working with labour in short supply and there has been little to no wage inflation. Companies that have tried to pass input cost inflation through to customers have been hit hard as Japanese consumers are very price-sensitive.

In some cases, stocks in JFJ’s portfolio have been able to take advantage of the situation. For example, SMC which is a top 10 position in the fund (see page 13) and a global leader in pneumatic equipment is facing higher input costs, but it has elected to absorb these within its margins and grow its market share – illustrating the strength of the business.

Japan may be characterised by an ageing population, low economic growth and low inflation, but the managers stress that the earnings growth of its listed companies is outpacing economic growth by some distance and is not that far off that of companies listed on the S&P500.

Faltering Chinese growth may have some impact on Japan because it is a big export market for Japanese companies. Some computer games companies were caught by China’s clampdown on gaming. However, the more worrying development for some companies is China’s ‘Buy China’ policy. This is hitting Japanese (and European/US) companies as Chinese buyers switch to domestic producers. The managers have taken some stocks out of the portfolio to reflect this trend. For example, Kao – a cosmetics company – and Pigeon – in baby goods – were both struggling to compete with Chinese competitors. The managers feel that consumer goods companies appear most exposed, whereas Japanese industrial companies still tend to have dominant and defensible market positions.

The third change of Prime Minister (from Abe, to Suga to Kishida) in the space of a few months has had next to no impact on the economy. The Liberal Democratic Party (LDP) retains its stranglehold on Japanese politics. Policies, including Suga’s emphasis on the digitalisation of the Japanese economy (which is an important theme within the portfolio) are unchanged.

The managers believe that the standard of corporate governance is continuing to improve in Japan. After a period of caution (related to COVID-19) the quantum of buybacks and dividends is forecast to hit new highs for the 12 months ended March 2022. This is supported by balance sheets that are, on average, much more solid than those of companies in the US and Europe.

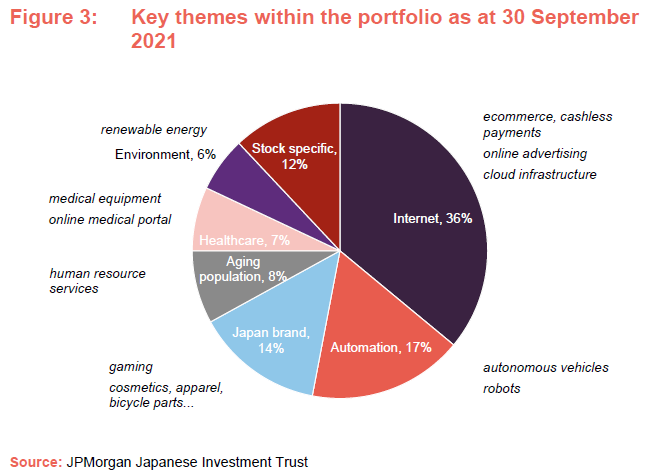

Key themes within the portfolio

The managers break the portfolio down across a number of key themes – internet, automation, Japan brand, ageing population, healthcare, environment and stock specific. Each of these areas represents a structural growth opportunity that the fund can benefit from.

We have discussed many of these themes in previous notes. In the areas of cashless payments and online advertising, for example, Japan lags a long way behind the US and many European countries but also China and South Korea. Japan’s lead in robotics is, in part, reflective of its shrinking workforce, which has also encouraged the development of strong recruitment and employment benefits businesses as companies compete for and fight to retain staff. As the population ages, more business founders are nearing retirement age, which could encourage mergers and acquisitions (M&A) activity. There is also a growing need for medical care.

Tackling climate change

We looked at JFJ’s exposure to companies addressing climate change in our last note. Many of the companies they’d like to own in this area are small parts of larger less-interesting businesses. However, as discussed in the last note, the managers have invested in stocks such as Canadian Solar, Renova and Hitachi.

One other stock that is benefitting from this theme is Shimano. This is the only stock that the fund owns in the transportation equipment sector. Shimano makes gears for bicycles, including electric bicycles, which to date have proved far more popular in Japan than electric vehicles. The managers say that Shimano has no real competition in this area.

Investment process

The emphasis is on long-term sustainability of returns, and there is a clear bias in favour of quality businesses and growth. The approach is unconstrained – they look at the whole market, including a number of smaller companies. The closed-end structure helps in that regard.

Stock selection drives sector exposure and those sectors that do not fit well within their quality and growth style are not included in the portfolio. Typically, the portfolio’s active share will be in excess of 80% and may approach 100% (93.7% at end September 2021).

The Japanese market is highly inefficient and therefore conducive to a stock picking approach. The universe comprises around 4,000 stocks. Based on data from December 2020, over 71% of companies with a market cap in excess of $10m are covered by three or fewer analysts (as compared to 43% in Europe and 38% in the US), and about half the market is covered by one analyst or none.

The team meets as many companies as possible, with around 4,000 meetings in a typical year, including quite a few with pre-IPO companies (although the managers will not invest in unlisted companies).

Japan’s structural transformation

In the managers’ view, the benchmark index is dominated by ‘old Japan’, companies operating in stagnant or declining industries. These are not just obviously outdated industries such as steel, but also companies like the automakers who are facing big challenges in adapting to the shift to electric vehicles and self-driving cars. The managers note that many formerly-successful consumer electronics companies are being displaced by other Asian competitors.

Japan is also well-behind the curve when it comes to the displacement of bricks-and-mortar retailers by online competitors, which implies much pain to come but also highlights opportunities in logistics and online payment processing.

Given all of this, it is easy to see why a stock picking fund such as JFJ offers considerable advantages over an investment in an index-tracking ETF.

Practical approach

For each stock, the managers want to assess:

- does the business create value for shareholders? (Economics);

- can this value creation be sustained? (Duration); and

- how will governance impact shareholder value (Governance).

When assessing stocks for inclusion in the portfolio, the first questions are: is this a business that they want to own? Does it have competitive strengths that will allow it to thrive? And is it operating in an attractive industry demonstrating secular growth? Valuation considerations are secondary to this.

Indications of quality include returns on equity, free cash flow generation and balance sheet strength. The company should have competitive strengths that give it pricing power. Management should be of good quality, accessible and aligned with the interests of shareholders.

Governance and other aspects of ESG

One long-running theme within Japan has been improvements to corporate governance. Assessing governance aspects is therefore a key part of the investment process. Social and environmental factors are evaluated as well.

JPMAM is a signatory to both the UN PRI and the Net Zero Asset Managers Initiative. JPMAM is a signatory to the Japanese Stewardship Code and endeavours to vote at all meetings called by companies within JFJ’s portfolio.

Companies being considered for inclusion within the portfolio are judged on the basis of a 98-question analysis that covers a wide range of environmental, social and governance (ESG) aspects, with simple yes/no answers. This analysis should pick up anomalies such as a substantial divergence between accounting profits and cash generation.

The worst companies – often those in the utilities, energy and real estate sectors – have scores in the high 20s. Within JFJ’s portfolio, on average premium companies score 7, quality companies score 9 and trading companies score 14.

Informed by this analysis, the managers divide JFJ’s universe between ‘premium’, ‘quality’ and ‘trading’ companies. Very few companies qualify for inclusion within the premium category, but these are the companies in which the manager has the highest conviction. About 80% of stocks in the index fall into the trading category.

JFJ is not an activist fund. However, the investment approach emphasises contact with companies, and the managers will engage in dialogue with management where they feel that ESG improvements are needed. They will also ensure that JFJ exercises its voting rights at company meetings.

Assessing value

Valuations are assessed on the basis of five-year forecasts of sustainable earnings growth, dividends and the multiple that the managers think a stock should be trading on in five years’ time. Cash on the balance sheet is reflected later in the process.

Position sizes will reflect the conviction that the manager has in a stock and whether it has been assigned to the premium, quality or trading buckets. Premium stocks may have a 3%–5% weighting in the portfolio, quality stocks a 2%–4% weighting and trading stocks a 0.5%–2% weighting.

On average, the portfolio will contain between 40 and 80 positions. The portfolio is regularly assessed to ensure that overall risk factors are within acceptable levels.

Investment restrictions

The board seeks to manage risk by imposing various investment limits and restrictions:

- JFJ must maintain 97.5% of investments in Japanese securities or securities providing an indirect investment in Japan.

- No investment to be more than 5.0% in excess of benchmark weighting at time of purchase and 7.5% at any time.

- The company does not normally invest in unquoted investments and to do so requires prior board approval.

- The company does not normally enter into derivative transactions, and to do so requires prior board approval.

- The company will not invest more than 15% of its gross assets in other UK-listed investment companies and will not invest more than 10% of its gross assets in companies that themselves may invest more than 15% of gross assets in UK-listed investment companies. In practice, the managers say that they never have and do not ever envisage investing in other investment companies.

- The managers do not hedge the portfolio against foreign currency risk.

These limits and restrictions may be varied by the board at any time at its discretion.

Sell discipline

Generally, JFJ’s is a low-turnover portfolio, reflecting the managers’ long-term investment horizon. However, stocks may be sold if the investment case deteriorates or on an adverse corporate governance change. Stocks may be replaced if the managers identify a similar investment opportunity with a better risk/reward profile.

The managers like to run their winners, but will take profits if valuations exceed their long-run targets.

Asset allocation

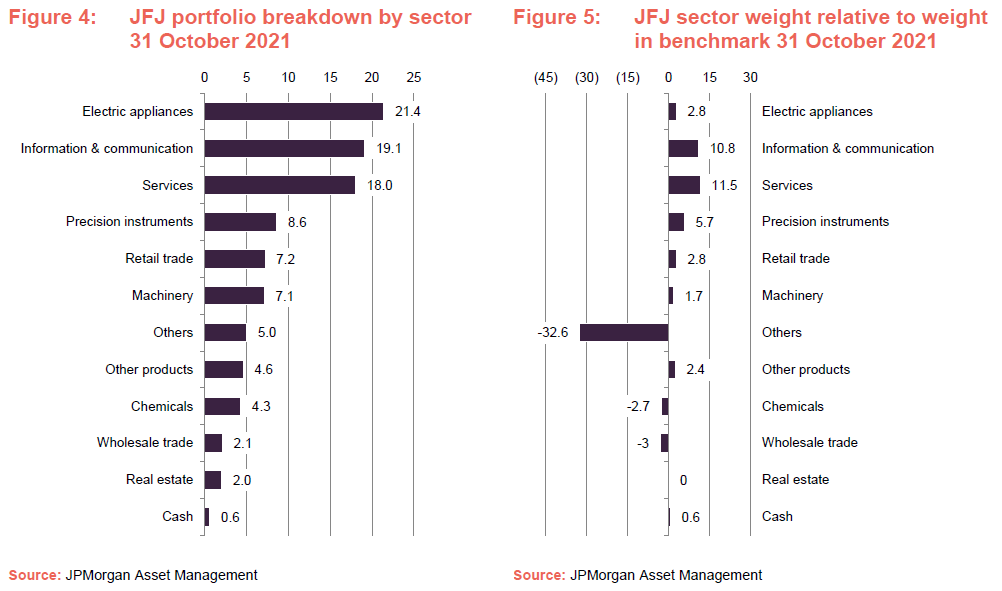

Nicholas says that, to date, 2021 has been the lowest year for portfolio turnover since he has been running the trust (around 10 years). There were 63 holdings in the portfolio at 31 October 2021. The number of holdings has come down as the portfolio has become a little more concentrated.

Sector weights are driven by stock selection, but they reflect the portfolio’s bias to the ‘new’ Japan and the absence of exposure to sectors such as pharmaceuticals, transportation equipment and banks. The distribution of the portfolio by sector is much as it was six months ago, except that the exposure to information & communication has reduced by about five percentage points in favour of electric appliances.

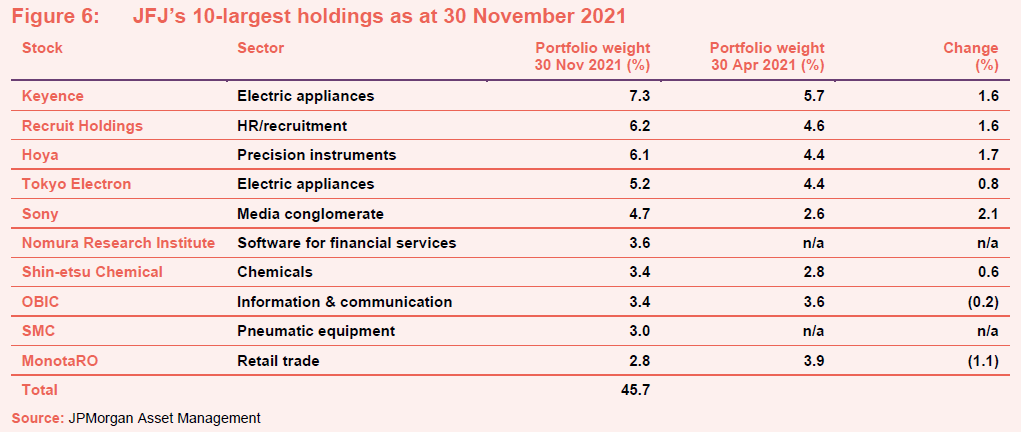

Top 10 holdings

Since we last published (using data as at 30 April 2021) Nintendo and Fast Retailing have fallen out of the top 10 holdings and have been replaced by Nomura Research Institute and SMC.

Looking at a few of these in more detail:

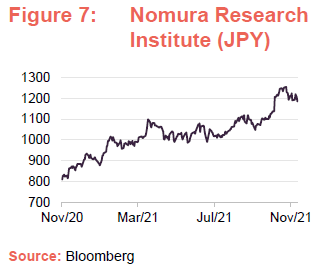

Nomura Research Institute

Nomura Research Institute (ir.nri.com/en) is a software and consultancy company focused on the financial services sector. Its largest client (10.6% of revenue for the quarter ended 30 September 2021) is Nomura Holdings. Overseas income is a relatively small part of the total but growing fast. At the half-year stage (30 September), sales were running at 89.7% ahead of the equivalent period in 2020 and its pre-tax profit was 43% higher. The company says that demand for digital transformation is exceeding its initial expectations (helped by COVID-19) and its business in Australia is doing well.

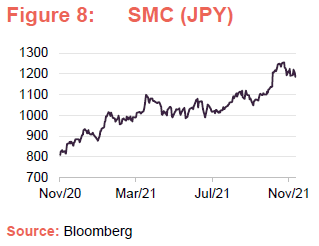

SMC

SMC (smcworld.com/ir/en/) makes a wide range of pneumatic equipment and is a global leader in this field. For the first half of 2021, year-on-year growth in sales was 42% higher than the equivalent period in 2020. Margins improved dramatically (from 25.8% to 32.9%) and this drove an 85% uplift in operating profits. Its market share has been growing in all regions and, as mentioned above, its decision to absorb input cost increases rather than seek to pass these on to customers may accelerate this. At the end of October, its order book was up 32% on 2020 levels.

Other portfolio activity – new holdings/additions

Recent purchases include Healios, Benefit One, Sony and Zozo.

Sony (sony.com/en) – the leading player in gaming (PlayStation), music, film, consumer electronics, and imaging and sensing solutions – was mentioned in the last note. The stock was upgraded by the analyst team from ‘trading’ to ‘quality’. The company is forecasting a 10% uplift in its revenue for the 2021 financial year (FY21) over FY20.

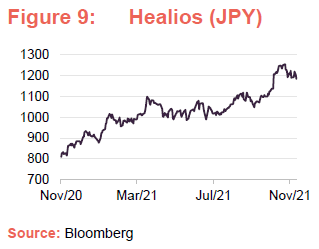

Healios

Healios (healios.co.jp) is a Japanese biotech company with therapies in Phase 2/3 for strokes and ARDS (acute respiratory distress syndrome – a factor in COVID-19 deaths/hospitalisations) and preclinical R&D in immuno-oncology, gene therapies (to treat Wet and Dry AMD and metabolic liver disease) and stem cell therapies. Given the binary risks associated with biotech businesses, this is a small (about 0.3%) position within the portfolio. It is also a stock that is held by JFJ but not by the managers’ equivalent open-ended fund. The managers like the CEO, who has a large personal stake in the company.

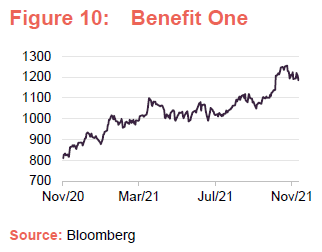

Benefit One

Benefit One (benefit-one.co.jp/en) is an employee benefits company. The managers like the business, which they believe experiences a virtuous circle as it expands. Benefits offered include things like nurseries and baby-sitting, which are highly sought-after. The company recently acquired the benefit service division of travel business JTB for what the managers think was an opportunistic price. Nicholas thinks that this gives the company an unassailable position in this market

Zozo

Zozo (zozo.com) is an online fashion business. 2020 was a year of significant growth for the company and some of this momentum has been carried forward through 2021. The company is delivering a steady uplift in customer numbers, double-digit growth in sales and operating profits. The company’s forecast is for a 7.7% growth in net profits for its 2021 financial year. Zozo is looking to get its software integrated into physical stores – to be used to manage inventory across hybrid online/offline retail businesses, take on more of the planning/production process, and use technology licensing to access overseas markets.

The managers have also bought positions in Mercari, an online marketplace that allows consumer-to-consumer sales of second-hand goods, and WealthNavi, a robo-adviser (which IPO’d in December 2020 and is seeking to benefit from increase retail investor interest in stocks.

Outright sales/reductions

Three stocks that the managers have sold out of recently are Pan Pacific, Hikari Tsushin and Relo Group. For each of these, the sale was driven by a change in the investment case. The managers have also reduced positions in Bengo4 and Rakuten.

Pan Pacific (ppih.co.jp/en) is a retail business operating across a number of brands including Don Quijote. The stock should have been a beneficiary of increased tourism, but COVID-19 had an impact on the business. The managers felt that new management (about two years ago) was taking the company in a strategic direction that they were unhappy with.

Similarly, while Hikari Tsushin (hikari.co.jp/en/) has a good track record in selling a diverse range of products and services, the managers felt that the business was expanding into areas that they felt uncomfortable with.

Relo Group (relo.jp/english) has businesses that support corporate relocations and manage employee benefits. The company ranks behind Benefit One in terms of employee benefits, and the managers sold the Relo stake after Benefit One announced its JTB purchase.

Performance

Even though JFJ gave back some of its relative outperformance of its benchmark and its peer group between November 2020 and March 2021, performance is on an improving trend once again.

The shift in market sentiment that occurred following the good news on vaccines in November 2020 allowed a resurgence in sectors that had been hit hard by the pandemic, such as department stores and railway companies. These were not the types of business that are included within JFJ’s portfolio. The managers held onto good-quality growth stocks, even as other investors were taking profits.

Performance drivers

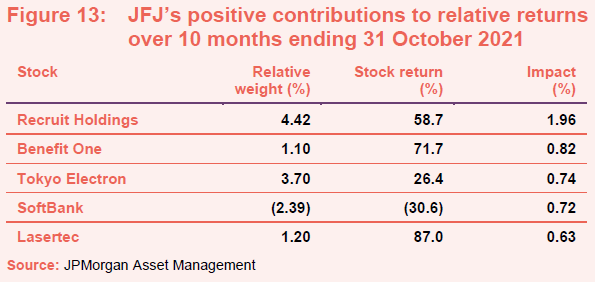

The managers kindly supplied us with some performance attribution data which covers the 10-month period to end October 2021.

Recruit Holdings

Recruit Holdings (recruit-holdings.com/en) did particularly well as the global economy recovered from the pandemic recovery. For the six months ended 30 September 2021, operating income almost tripled from 2020 levels. Its Indeed hiring business took market share and the managers say that this business is getting stronger. The managers like the CEO, who – unusually for a Japanese business – is based overseas (in Austin, Texas). The managers think that Recruit has the potential to be a significant global business.

Benefit One was discussed above. Tokyo Electron is one of the stocks that the managers were able to acquire at an attractive valuation during last year’s pandemic-related sell off. Softbank, a stock that is not owned by JFJ, has been hit hard because of its exposure to Alibaba.

Lasertec is a testing business exposed to the semiconductor manufacturing process. Its order book is expanding. Nicholas says that this has been a ‘slow burner’ but has made JFJ multiples of its initial investment.

Many of these stocks are companies that did particularly well in 2020 and have since been exposed to profit-taking. Nicholas feels that some investors are too fixated on short-term changes in sales/profit growth rather than the big picture.

Nintendo didn’t really have much of a Chinese business – that was not the issue. Nicholas thinks that some investors are worried about the age of the Switch console, but are missing the big picture of the shift to streamed/downloaded, rather than cartridge, games and that Nintendo, with its extensive catalogue of titles, is well placed to exploit this shift.

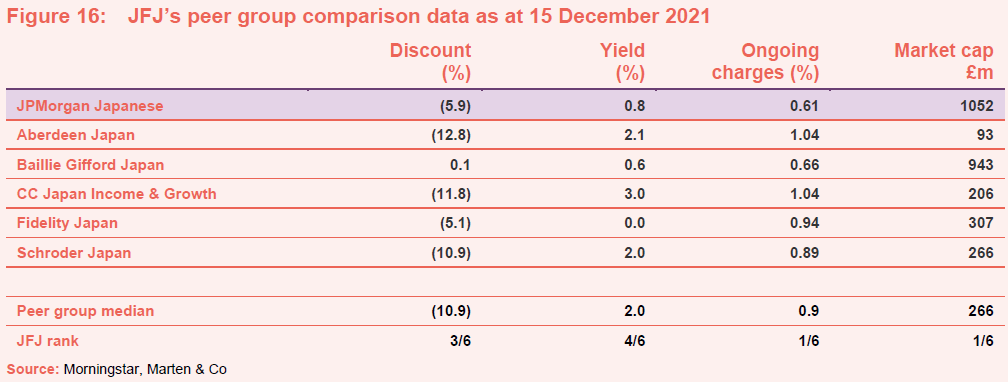

Peer group

For the purposes of this note we have used the constituents of the AIC Japan sector as a peer group. The trusts listed here have roughly similar objectives except for CC Japan Income & Growth, which – as its name implies – places more emphasis on income generation and consequently has the highest yield. By contrast, JFJ’s growth focus puts its yield towards the bottom end of the peer group.

JFJ remains the largest and most liquid trust in its peer group. Its one-year performance may be at the bottom end of this group, but longer-term numbers are much more impressive, and as the short-term time frames suggest, performance is on an improving trend. JFJ can boast the lowest ongoing charges ratio of this peer group and we feel that the combination of the above is reflected in its better-than average discount, although we feel that it deserves to trade at asset value given its track record.

Dividends

The board’s dividend policy is to pay out the majority of the revenue available each year. The investment objective’s emphasis on capital growth means that income generation is not a focus for the managers. A revenue reserve has built up over the years and this stood at £15.1m at the end of September 2021 (equivalent to about 9.7p per share).

Discount

Over the 12 months to the end of November 2021, JFJ’s discount moved within a range of 9.2% discount to a premium of 0.7% and averaged 4.2%. At 15 December 2021, the discount was 5.9%.

The board monitors the discount closely and has both stepped up efforts to market the trust and authorised share buy backs. We feel that the discount is wide given the strong track record, the liquidity of the shares and the low ongoing charges ratio.

Each year at the AGM, the board puts forward resolutions that permit the company to issue new shares, reissue shares from treasury and repurchase shares for cancellation or to be held in treasury. The board has stated that shares held in treasury would only be reissued at a premium to NAV.

Fees and costs

The trust employs JPMorgan Funds Limited as its Alternative Investment Fund Manager (AIFM) and company secretary. Management of the portfolio is delegated to JPMorgan Asset Management (UK) Limited, which in turn delegates day-to-day investment management activity to JPMorgan Asset Management (Japan) Limited in Tokyo. The manager is a wholly-owned subsidiary of JPMorgan Chase Bank which, through other subsidiaries, also provides marketing, banking, dealing and custodian services to the company.

JPMorgan Funds Limited is entitled to an annual management fee calculated as 0.65% of the first £465m of net assets, 0.485% on the next £465m and 0.40% on amounts above £930m. There is no performance fee. The contract can be terminated on six months’ notice. For accounting purposes, in the last financial year the management fee was charged 20% against the revenue account and 80% against the capital account.

Other administrative expenses for the year ended 30 September 2021 amounted to £846,000 (FY20 £790,000).

For the year ended 30 September 2021, the trust’s ongoing charges ratio was 0.61%. The ratio has been falling steadily for the last few years, aided by the increase in the size of the trust.

Capital structure

JFJ is a UK-domiciled investment trust with a premium listing on the main market of the London Stock Exchange. The company has 156,500,739 ordinary shares with voting rights. A further 4,747,339 ordinary shares are held in treasury.

The company’s accounting year end is 30 September and AGMs are usually held in the following January. The next is scheduled for 13 January 2022.

Gearing

The company has the ability to use borrowing to gear the portfolio within the range of 5% net cash to 20% geared in normal market conditions.

The company’s gearing is facilitated by a ¥13bn three-year floating rate revolving credit facility provided by Scotiabank which matures in December 2022 and a series of senior secured loan notes:

- ¥2bn fixed rate 10-year series A senior secured loan notes at an annual coupon of 0.76% which will expire on 2nd August 2028.

- ¥2.5bn fixed rate 15-year series B senior secured loan notes at an annual coupon of 0.95% which will expire on 2nd August 2033.

- ¥2.5bn fixed rate 20-year series C senior secured loan notes at an annual coupon of 1.11% which will expire on 2nd August 2038.

- ¥2.5bn fixed rate 25-year series D senior secured loan notes at an annual coupon of 1.21% which will expire on 2nd August 2043.

- ¥3.5bn fixed rate 30-year series E senior secured loan notes at an annual coupon of 1.33% which will expire on 2nd August 2048.

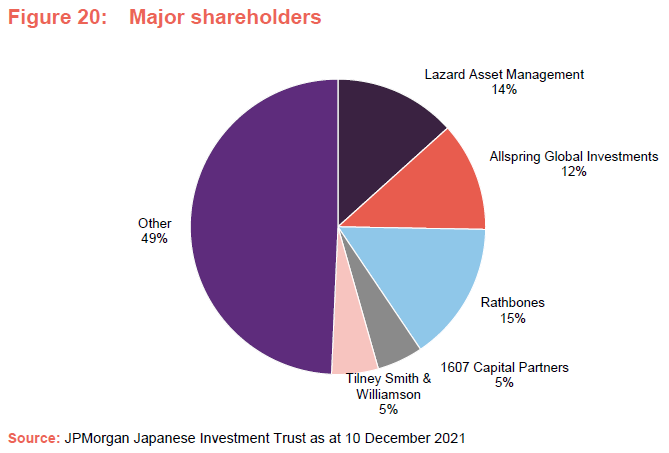

Major shareholders

Core management team

Nicholas Weindling is a country specialist for Japan equities and a member of the Japan team within the Emerging Markets and Asia Pacific (EMAP) Equities team based in Tokyo. Nicholas joined JPMorgan Asset Management in 2006 from Baillie Gifford in Edinburgh, where he worked initially as a UK large-cap analyst and latterly as a Japanese equities investment manager. Nicholas obtained a B.A. (Hons) in History from Cambridge University. He was made manager of JFJ in August 2010.

Miyako Urabe is a country specialist for Japan equities, and a member of the Japan team within the Emerging Markets and Asia Pacific (EMAP) Equities team based in Tokyo. Miyako joined JPMorgan Asset Management Firm in 2013 from Credit Suisse Securities Equity Sales desk in Tokyo as an Asia ex-Japan specialist. She began her career at Morgan Stanley MUFG Securities covering Japan and Asia ex-Japan. Miyako obtained a Bachelors degree in Economics from Keio University, Japan.

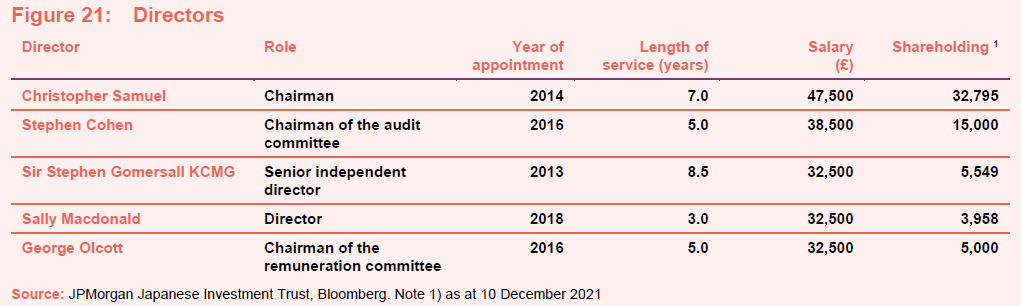

Board

Each of the directors is independent of the manager and they do not sit together on other boards.

Longstanding director Sir Stephen Gomersall was appointed as the senior independent director with effect from July 2021. Yoko Dochi resigned as a director with effect from 1 October 2021 for personal reasons. A replacement director is being recruited.

Christopher Samuel

(Chairman)

Christopher became chairman in December 2018. He is currently chairman of BlackRock Throgmorton Trust Plc and Quilter Financial Planning, and a non-executive director of Alliance Trust Plc, Quilter Plc and UIL. Christopher was previously chief executive officer of Ignis Asset Management. He has considerable experience of financial services, including the investment management industry, over some 35 years and was based in Japan earlier in his career. He is a Chartered Accountant.

Stephen Cohen

(Chairman of the audit committee)

Stephen has had over 34 years in executive roles in asset management, including setting up two businesses in Japan and living there for seven years.

He managed Japanese equity portfolios for 10 years. He also latterly ran a Japanese equity activist business. Currently, he is a non-executive director of Schroder UK Public Private Trust Plc, a commissioner at the Gambling Commission and a council member on the Health and Care Professions Council.

Sir Stephen Gomersall, KCMG

(Senior independent director)

Sir Stephen entered the Foreign & Commonwealth Office in 1970 and held a number of appointments overseas including being Ambassador to Japan from 1999 to 2004. Until 30 November 2021, he was advisor to the CEO of Hitachi Ltd and, during his 17-year tenure, a director of Hitachi Ltd and several Hitachi Group companies in the UK. He has spent over 14 years living and working in Japan.

Sally Macdonald

Sally has 35 years’ experience in asset management, of which seven were in UK markets and 28 in Asian markets, at houses including Sanwa International, Lazard Brothers Asset Management, Canada Life, Morley Fund Managers, Dalton Strategic Partnership and City of London Investment Management. She was until recently head of Asian equities at Marlborough Fund Managers, and will shortly join the board of Fidelity Asian Values Plc. She is also a trustee of Helping the Burmese Delta. Previous board experience includes the Royal College of Nursing Foundation.

Dr. George Olcott

(Chairman of the remuneration committee)

George has 15 years of investment banking and asset management business experience in Japan and Asia with SG Warburg/UBS, and has served on the boards of six listed Japanese corporations as an independent director (currently for Denso Corporation, Dai-ichi Life Holdings and Kirin Holdings). He is a specially appointed professor and vice president of a Japanese university, Shizenkan University, and holds advisory roles at Toyota and JR Central.

Previous publications

Readers may be interested in our previous publications on JFJ, which are listed in the table below. These are available to read on our website or by clicking the links in the table.

| Number one for a good reason | Initiation | 09 September 2020 |

| Strength to strength | Update | 09 December 2020 |

| Medium-term outlook undimmed | Update | 24 May 2021 |

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on JPMorgan Japanese Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.