Navigating a changed landscape

Measures being taken to tackle inflation are weighing on markets. Reflecting this, JPMorgan Multi-Asset Growth & Income (MATE) has also been affected, with falls in its net asset value (NAV) and share price. However, living up to its objective (see below), these falls have not been as severe as those of global equity markets.

In the current environment, MATE’s policy of growing its dividend at least in line with inflation should be attractive to investors. The managers have repositioned the portfolio to reflect the changed circumstances. They are looking for signs that the worst is priced in and markets are braced to recover, and will look to take advantage of this when the time is right.

Income and capital growth from a multi-asset portfolio

MATE aims to generate income and capital growth, while seeking to maintain lower levels of portfolio volatility than a traditional equity portfolio. It operates a multi-asset strategy, maintaining a high degree of flexibility with respect to asset class, geography and sector of the investments selected for the portfolio.

At a glance

Share price and premium/(discount)

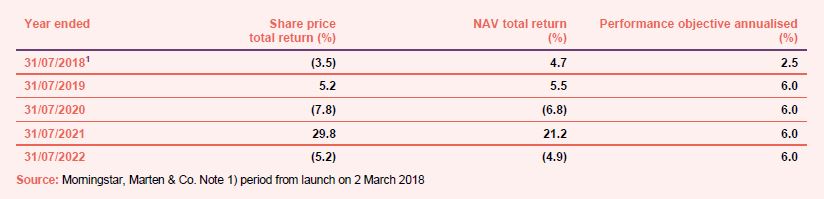

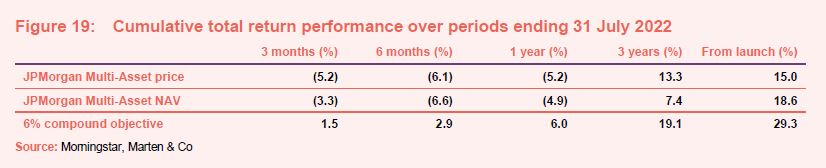

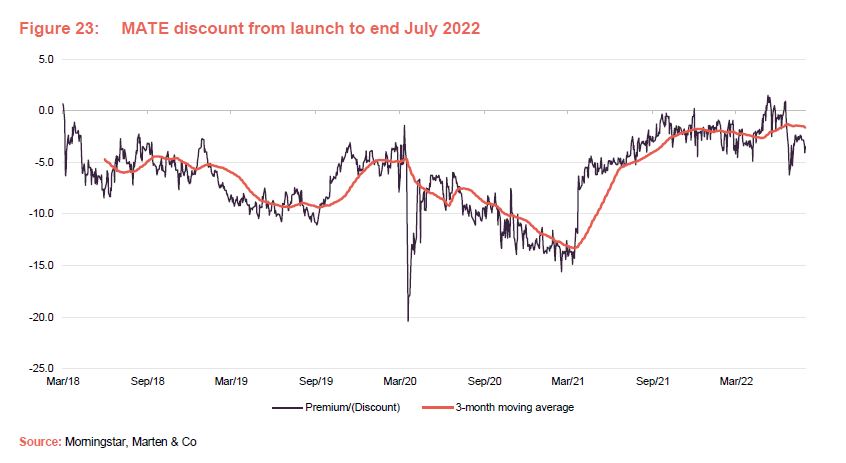

Over the 12 months ended 31 July 2022, MATE’s shares moved between trading at a 6.2% discount and a 1.5% premium and, on average, traded at a discount of 2.1%.

On 18 August 2022, MATE was trading at a discount of 4.4%.

Performance since launch

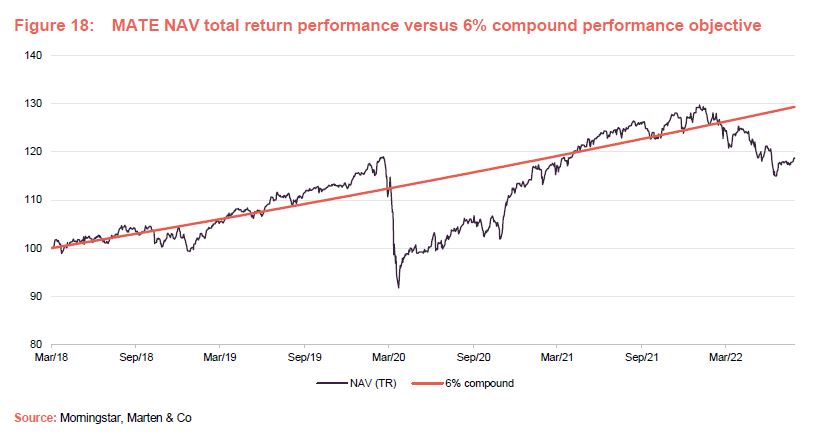

Falling markets have impacted on MATE’s short-term performance relative to its long-term objective of 6% compound returns. Even with the lower risk associated with MATE’s diversification, in the short term, the current environment makes it hard to achieve positive NAV progress.

Why MATE?

MATE is targeting total returns in excess of 6% per year over rolling five-year periods. The trust is designed for those investors who are looking for attractive, relatively predictable, income that grows at least in line with inflation and a diversified portfolio of investments designed to be less volatile than that of a typical equity portfolio (the managers target volatility two-thirds of that of a global equity index).

MATE can commit to growing its income in line with inflation (as measured by UK CPI) because it can top up the amount available to pay dividends from distributable reserves if necessary.

MATE’s board feels that achieving the income objective ought not to come at the expense of investors’ total returns. Consequently, the manager, JPMorgan Asset Management (JPMAM) has the freedom to invest with the aim of maximising total returns rather than chasing revenue.

Multi-asset investing allows portfolios to be created that contain assets whose returns are not correlated with each other. The implication is that a fall in value in one asset class might not be accompanied by a fall in value in other asset classes. By building a portfolio that includes a range of less-correlated assets, a manager should be able to achieve lower return volatility for a given expected return.

MATE’s investment approach was described more comprehensively in our initiation note. Readers may wish to refer to this.

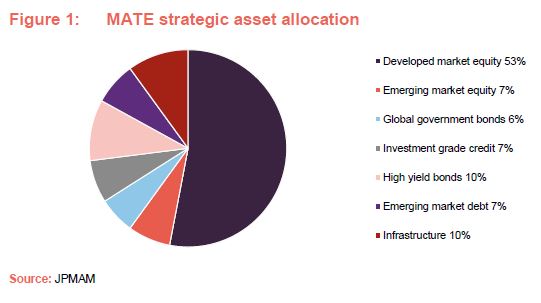

At the outset, MATE’s managers devised a strategic asset allocation (SAA) for the fund that was designed to optimise the combination of risk and returns. This was informed by JPMorgan’s long-term capital market assumptions (looking 10–15 years out) and the correlations between these different asset classes. There is no requirement for the trust to have exposure to all of the core asset classes that make up the SAA. The managers also have the freedom to make opportunistic investments in additional asset classes. An important constraint on exposure to alternative assets is liquidity. A futures overlay allows the managers to adjust the trust’s exposures to different asset classes without elevating turnover within the underlying portfolios.

Much has changed

Much has changed since October 2021, when we published our last note on MATE. Back then, the team was particularly positive on the outlook for equities, expressed through an overweight exposure to the asset class, plus some exposure to convertibles, which are not represented in MATE’s SAA. The team acknowledged investors’ concerns about inflation but felt that these would ease in 2022.

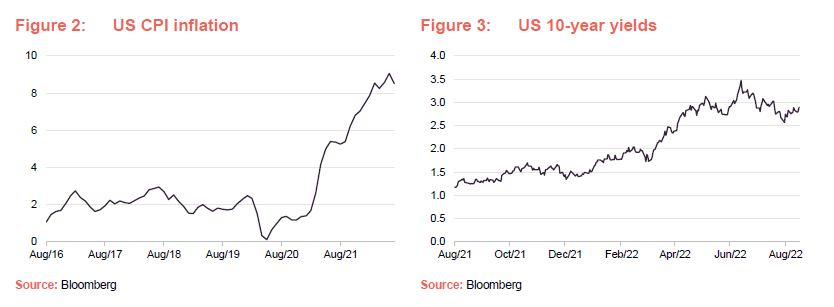

Whilst supply chain disruptions exacerbated inflation, it was Russia’s invasion of Ukraine that entrenched it. Workers are becoming increasingly vocal in demanding pay rises in response to spikes in the prices of energy and food. Figure 2 shows just how far US inflation has climbed; in the UK the inflation rate is even higher.

With inflation stickier and higher than anticipated, central banks needed to take action. Their response has been to hike interest rates and call time on quantitative easing. In the US, the Federal Reserve (Fed) has been criticised for being behind the curve. It began raising interest rates in March 2022 with a 25 basis point (bp) – equivalent to 0.25% – increase, but has become more aggressive in recent months, as inflation has continued to soar. Following two recent 75bp increases (taking the upper bound of the Federal Funds Target Rate to 2.5%), longer dated (10-year plus) bond yields look like they may have peaked for the moment.

Figure 3 shows how the yield on 10-year US Treasury stocks has moved over the past year. The graph peaks on 14 June.

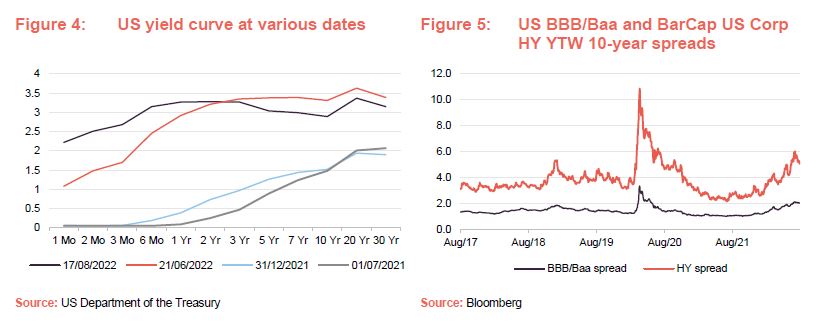

Figure 4 shows a series of yield curves – charts of the yields on US Treasury stocks with different maturity dates. The grey line – representing the curve as it was on 1 July 2021 – shows just how low yields were on short-dated debt at that time. Fast forward to 21 June 2022 (close to when 10-year yields peaked) and rising interest rates have pushed the whole of the curve higher. Right now, the curve is fairly flat, suggesting that markets think that rates are almost at their peak – we shall see.

Looking at Figure 5, which charts spreads (the gap between the yield on a bond and the yield on an equivalent government security) for both investment-grade and high-yield debt, these trended towards historic lows in the summer of 2021, as economies recovered from the effects of COVID-19. Low spreads suggest that investors are not too worried about the amount of risk that they are taking on by buying debt issued by a company rather than the government. However, spreads have widened since, as inflation/recession expectations have increased.

There are two lines on the chart in Figure 5, the US BBB/Baa spread charts the spread between investment grade (relatively low risk) US bonds and US Treasuries, and the BarCap US Corp HY YTW is an index of spreads for high yielding, higher risk bonds (HY – high yield, YTW – yield to worst – the lowest possible yield that can be earned on a bond that might be repaid early).

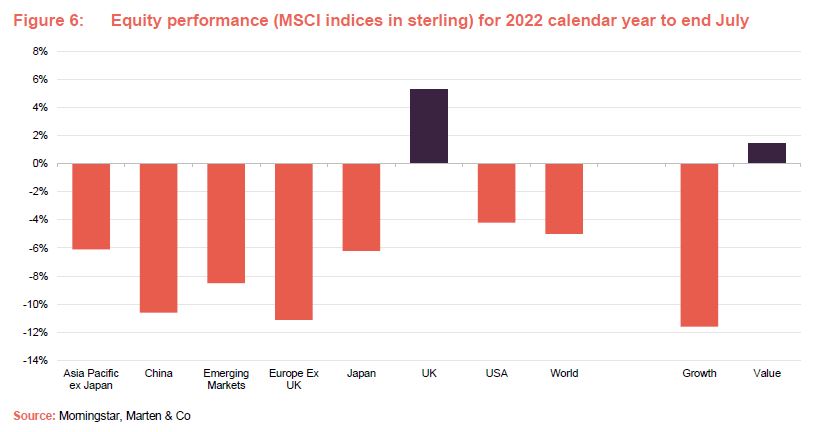

Figure 6 shows the performance of various MSCI indices over the seven months to end July 2022. Europe has been hit hardest, but China is not great either.

Despite a relatively weak pound (down about 9% versus the dollar since the start of the year), the UK is the only major equity market to have made gains (in sterling terms) in 2022.

In addition, against a backdrop of rising interest rates, growth has underperformed value.

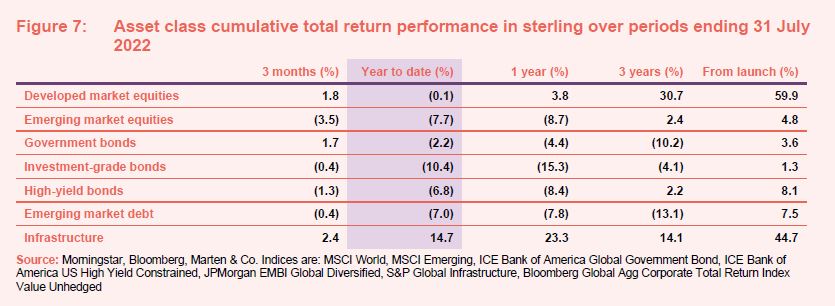

Looking at the components of MATE’s strategic asset allocation, in Figure 7 – where we have used an index to represent each asset class – every element has sold off in 2022 with the notable exception of infrastructure.

Managers’ views

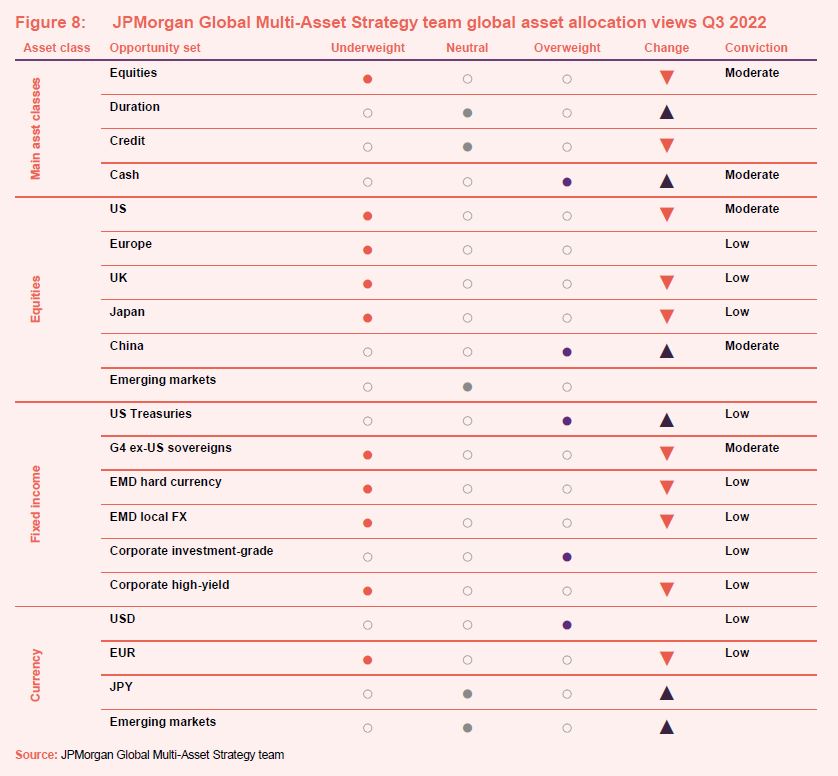

Figure 8 updates a chart that we included in the initiation note. It shows the JPMAM Global Multi Asset Strategy Team’s views on various asset classes at the beginning of the third quarter of 2022 (Q3).

The team thinks that we may narrowly avoid a global recession, but cautions that a prolonged period of sub-trend growth lies ahead.

The managers are cautious, given the macroeconomic backdrop, but are thinking about when it might be right to reintroduce more risk within MATE’s portfolio.

Equities

Equities are under pressure as slowing growth impacts on revenues and input cost inflation depresses profit margins. In recognition that US equity valuations were looking stretched, and margins were high ahead of this downturn, the managers remain cautious towards this area of the market.

In Europe, the obvious problem is the sharp rise in energy prices. These are an issue in the UK as well, but the growing risk of a trade battle with the EU could compound the problem and suggests the outlook is poor.

In Asia, slowing global growth is a problem for export-oriented markets. However, in China there is greater scope for the central bank to be supportive. Emerging markets remain unpopular with investors, and sentiment towards them may not improve until global growth recovers.

In the face of this, the managers decided to reduce MATE’s equity exposure.

Until recently, the underlying equity portfolio had a value-style tilt, which has been helpful given the backdrop. The portfolio had an underweight exposure to technology and an overweight exposure to financials, both of which have been helpful to relative performance.

The fund holds the bulk of its equity exposure in a customised global equity portfolio. Historically, this was managed with a dividend focus as managers looked to capture dividend income for distribution to shareholders. This was retained in the portfolio when the objective pivoted more to total return as this style was favoured by MATE’s portfolio management team. This value tilt proved useful in the first half of this year but in July, the team moved to a more growth-oriented strategy, where they see greater potential for return looking forward.

As the team looked to further reduce risk in the second quarter, they eliminated their allocation to the convertibles strategy which carried high levels of delta.

Running counter to this has been a modest increase in the allocation to China A shares. The managers acknowledge that they had not anticipated the extent of the lockdowns imposed to maintain the Chinese government’s zero COVID policy. However, given that vaccination rates are rising, they think this may now be eased.

The attraction of China is that it is at a different stage in its economic cycle. This makes it one of their favourite regions.

Fixed income

Bonds and equities have been quite well correlated this year. When we last published, the managers did not see any value in government bonds. Consequently, they were short duration at the start of the year. Now, following the selloff in bond markets, this is being increased.

The exposure to government bonds was increased by buying US 10-year futures, on a feeling that the Fed had succeeded in convincing markets of its determination to combat inflation and so US rate rises were priced in. Now the managers are starting to buy cash bonds. Other OECD government bond markets may yet fall further.

In Japan, MATE is short of Japan Government Bond (JGB) 10-year futures. the position is driven by the expectation that there will be increasing pressure on the Bank of Japan to remove the yield cap.

The managers expect that markets will continue to oscillate between worrying about growth and inflation. Nevertheless, we may have seen the top in yields in June (as illustrated in Figures 2 and 3).

The team’s decision to avoid investment grade bonds (a zero weighting despite their importance within the SAA) has paid off. The asset class had a torrid time, experiencing its biggest draw down in years. Spreads have widened to about 200bp now (as evidenced in Figure 4). MATE’s managers think that we are getting closer to the point where this asset class looks more attractive.

The managers say that high yield is also becoming more interesting, and while we are not there yet, at some point spreads may be wide enough to justify increasing the allocation to this area.

The team was not keen on emerging market debt when we last published, and that view has not changed. The managers note that the substantial increases in food and fertiliser prices are a particular problem for many emerging market countries. They feel that it is too early to be bargain-hunting in this area.

The allocation to infrastructure has been useful, given its ability to offer some inflation protection. The managers say that, as yet, there has been no apparent impact from higher yields on discount rates used to value infrastructure assets and the same can be said for many other alternative assets as well.

Currencies

The US dollar has been benefitting from its safe-haven status and a belief that rates would rise, but as investors become more convinced that the Fed has done what it needs to bring inflation under control, their attention may shift elsewhere.

Generally, the policy has been to hedge non-sterling exposure. However, the policy has been eased recently on concerns about the prospect of recession in the UK. The managers note that, given the country’s idiosyncratic risks, sterling could be the release valve. This could require the Bank of England to impose higher UK interest rates.

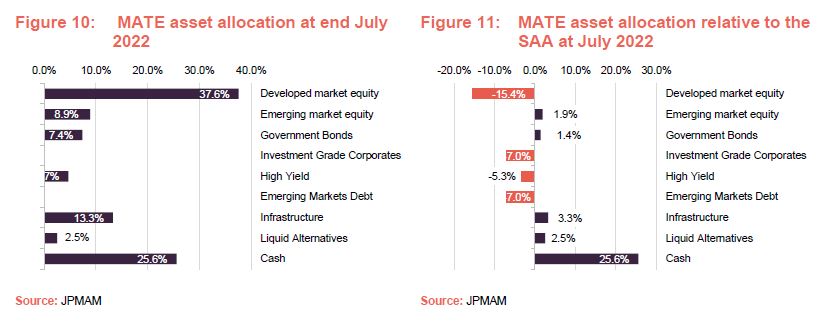

Asset allocation

Relative to the SAA, MATE has large underweight exposures to developed market equities, investment grade and emerging market debt (with zero exposure to the latter two asset classes). MATE’s cash position has increased markedly since we last published (at the end of August 2021, it was just 6.1% of the portfolio). However, part of the cash position reflects an offset against MATE’s futures positions.

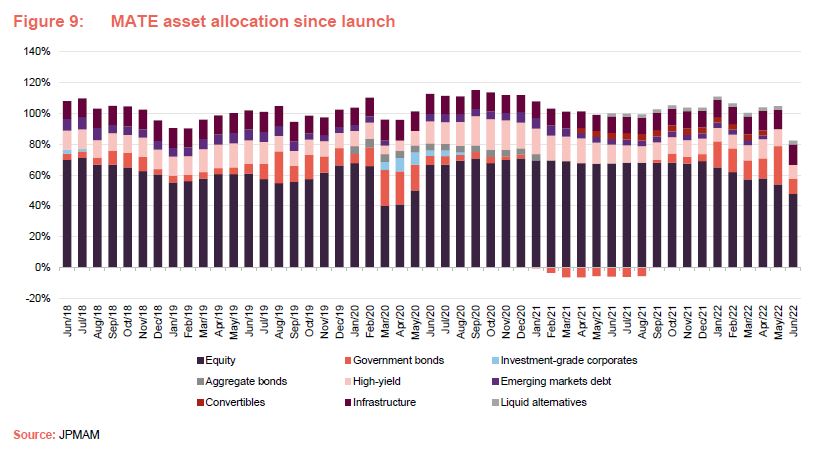

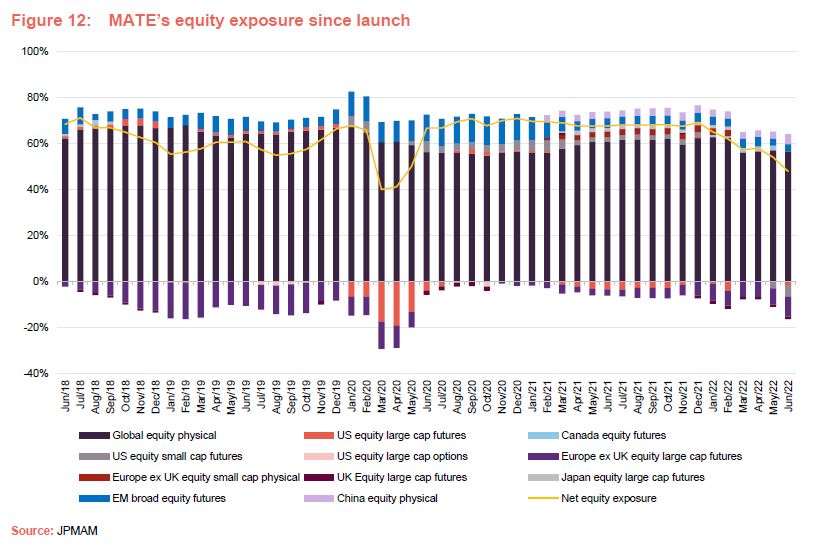

As Figure 12 shows, MATE’s net equity exposure has been falling over 2022. At the end of June 2022. On a regional basis, the team held short positions in US large cap and Europe ex UK equity futures.

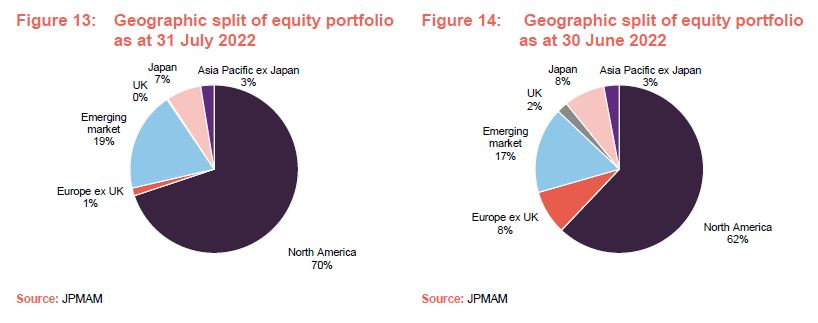

As the following charts illustrate, the equity portfolio was substantially repositioned during July. Most significantly, there was a wholesale shift towards higher growth stocks. The majority of the equity portfolio is in North America, representing an overweight exposure relative to the MSCI All Countries World Index (ACWI). China is included within the emerging market equity exposure.

Within the equity portfolio, the allocation to Europe has been reduced in favour of North America.

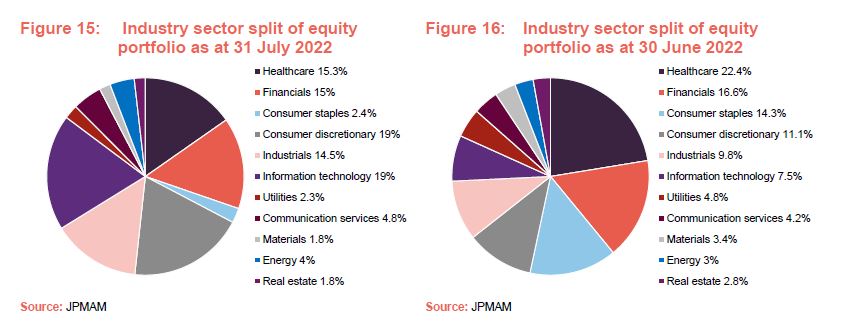

The shift in emphasis within the global equity portfolio is clearly evident when the position at the end of July is set against the position a month earlier. Notably, the allocation to healthcare and consumer staples has been slashed to the benefit of exposure to information technology and consumer discretionary.

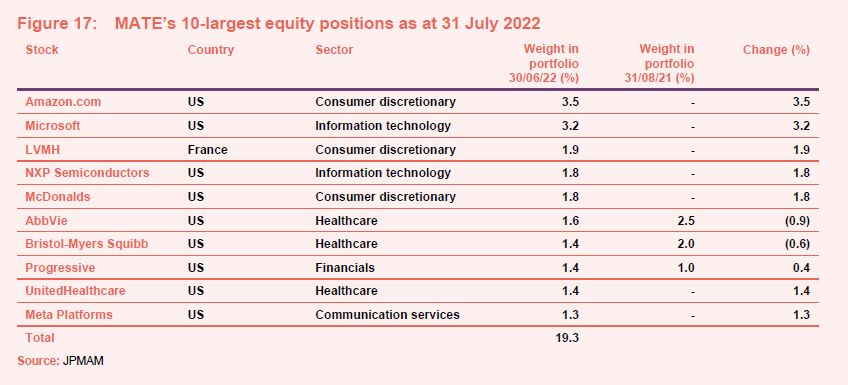

Top 10 equity positions

The portfolio repositioning has had a profound effect on the list of the 10-largest positions. Only one – McDonalds – featured in the list both at the end of June 2022 and the end of July 2022.

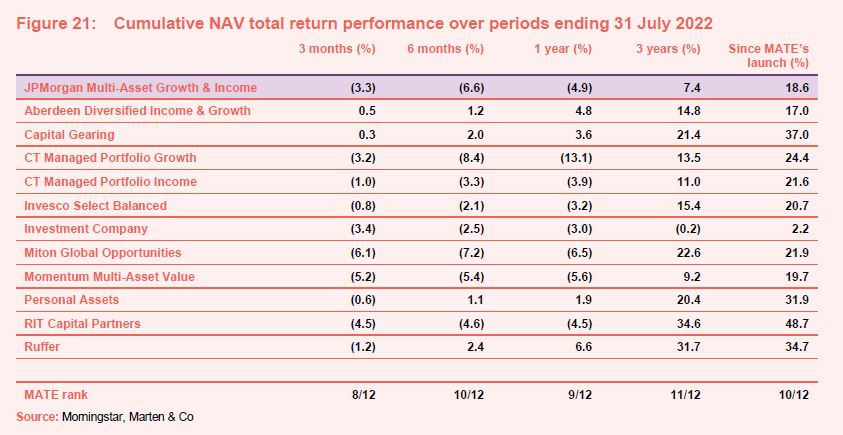

Performance

Falling markets have impacted on MATE’s short-term performance relative to its long-term objective of 6% compound returns. Even with the lower risk associated with MATE’s diversification, in the short term, the current environment makes it hard to achieve positive NAV progress.

Peer group

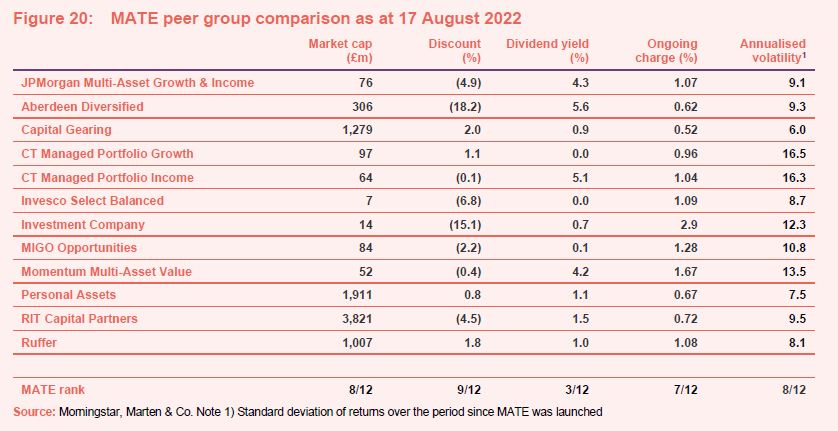

MATE is a constituent of the AIC’s Flexible Investment sector. These funds have investment objectives and/or policies that allow them to invest in a range of different asset types – multi-asset funds, therefore. However, this encompasses a wide variety of funds with very different performance objectives. The full AIC sector would make a poor comparison for MATE.

The list of funds that we have selected excludes Caledonia Investments (a trust managed on behalf of a family), Castlenau (which has a very concentrated portfolio of influential stakes in small companies), Hansa Investment Company (a family-controlled trust with a strong bias to Brazil, and which is domiciled in Bermuda), JPMorgan Core Real Assets (which has no equity exposure), JZ Capital Partners (a private equity fund that strayed into real estate with disastrous results), Livermore Investments (which has a strong bias to structured finance), New Star Investment Trust (which is run largely for the benefit of ex-employees of New Star), RiverFort Global Opportunities (which provides financing to very small companies), Schroder BSC Social Impact (which aims to make investments that have a positive social impact), Tetragon Financial Group (which invests in a wide variety of alternative investments including an asset management business), and UIL (a split capital company with an eclectic portfolio).

Since we last published, BMO Managed Portfolio has changed its name to CT Global Managed Portfolio.

Even this pared-down list encompasses quite a wide variety of investment styles and risk appetites. In the last note, we said that Aberdeen Diversified Income and Growth was perhaps the closest comparator to MATE. However, the Aberdeen fund has significantly increased its exposure to private markets investments, and its portfolio is now very different to MATE’s.

Within this peer group, MATE may be on the small side, but it offers an attractive yield, from a portfolio with below-average volatility and a competitive ongoing charges ratio.

We think that MATE’s longer-term returns were impacted by the earlier requirement to cover the dividend from portfolio revenues. We described the thinking that led up to the change in the investment policy in our last note. MATE’s managers are now free to seek to maximise its total returns.

Nevertheless, we note that MATE has been meeting its volatility objective. Its annualised standard deviation of returns since launch is 9.1%, almost half that of the MSCI World Index, which was 17.9%.

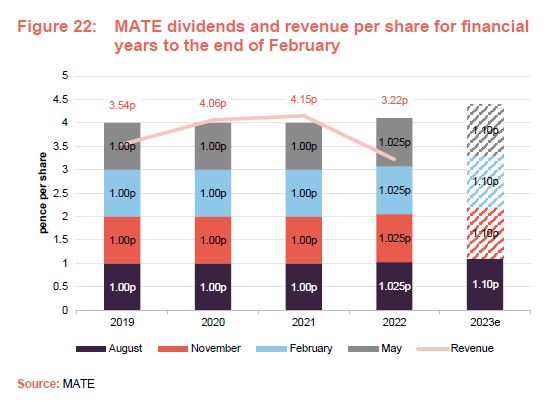

Inflation-linked dividend

We feel that MATE’s commitment to increase its dividend in line with inflation, introduced in March 2021, provides a clear differentiator between it and competing funds.

The target for the current financial year is 4.4p, to be paid in quarterly instalments of 1.1p. This was 7.3% higher than the 4.1p paid for the accounting year ended 28 February 2022. At end February 2022, UK CPI was running at 6.2% year-on-year.

At 28 February 2022, MATE had revenue reserves of £681,000. It also had a distributable special reserve of £84.8m. Together, these accounted for almost 97% of shareholders’ funds.

Premium/(discount)

Over the 12 months ended 31 July 2022, MATE’s shares moved between trading at a 6.2% discount to NAV and a 1.5% premium and, on average, traded at a discount of 2.1%. On 18 August 2022, MATE was trading at a discount of 4.4%.

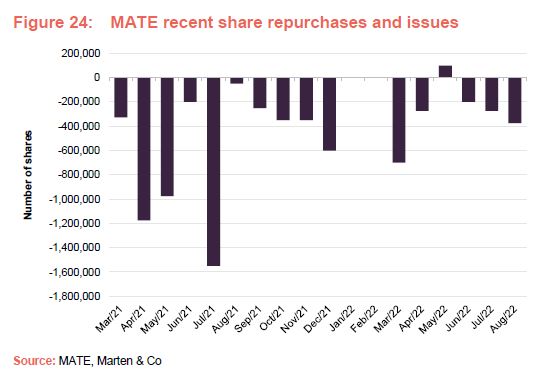

The board recognises that it is in the interests of shareholders to maintain a share price as close as possible to the NAV. It considers using buybacks to address imbalances in supply of and demand for MATE’s shares in the market, when it believes it is in the interests of all shareholders and subject to normal market conditions.

As Figure 24 shows, MATE has been repurchasing its shares on a fairly regular basis (to the benefit of a narrower discount). In May 2022, it was able to reissue some shares from treasury.

Fund profile

MATE is targeting total returns in excess of 6% per year over rolling five-year periods.

In its new guise, MATE is designed for those investors who are looking for attractive, relatively predictable income that grows at least in line with inflation and a diversified portfolio of investments designed to be less volatile than that of a typical equity portfolio (the managers target volatility two-thirds of that of a global equity index).

MATE’s board feels that achieving the income objective ought not to come at the expense of investors’ total returns.

MATE aims to provide a cost-effective investment vehicle for investors who seek income generation and capital growth from a multi-asset strategy, maintaining a high degree of flexibility, taking account of wider issues including environmental, social and governance.

Its managers seek to achieve the best risk-adjusted returns (with lower levels of volatility than a traditional equity portfolio) by investing in a globally diversified portfolio that includes company shares, bonds and other assets. Their aim is to construct a well-balanced portfolio which is flexible with respect to asset class and geography. This flexibility allows them to take advantage of the best opportunities to deliver an attractive total return to shareholders.

Management arrangements

JPMorgan Funds Limited (JPMF) acts as MATE’s alternative investment fund manager (AIFM) and company secretary. JPMF delegates the management of the portfolio to JPMorgan Asset Management (UK) Limited (JPMAM).

The lead investment managers responsible for MATE’s portfolio are Katy Thorneycroft and Gareth Witcomb, who have a combined experience of over 35 years in the asset management industry. They are members of JPMorgan Asset Management’s Multi-Assets Solutions Team.

The wider JPMorgan Asset Management business is one of the world’s largest, and JPMorgan Asset Management also manages 21 investment trusts across a diverse range of geographies and asset classes.

Previous publications

Our initiation note – New policy bearing fruit – was published on 8 October 2021.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on JPMorgan Multi-Asset Growth & Income Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication.

Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.