New policy bearing fruit

There are many investors looking for a high and growing income and a modest level of capital growth. JPMorgan Multi-Asset Growth & Income (MATE), with a portfolio diversified across a range of different asset classes, was designed with this in mind.

MATE was established about three and a half years ago. As the trust approached its third anniversary, the board took stock. The long-term performance objective of 6% per annum total returns on average over five years seemed to be on track. However, the board was concerned that a requirement to cover the dividend was too restraining for the managers. MATE’s returns were lagging its peer group. The board felt that, by removing this constraint, MATE would no longer be fighting with one hand tied behind its back.

Equally importantly, MATE would be able to commit to growing its dividend at least in-line with inflation (as measured by UK CPI).

Income and capital growth from multi-asset portfolio

MATE aims to generate income and capital growth, while seeking to maintain lower levels of portfolio volatility than a traditional equity portfolio. It operates a multi-asset strategy, maintaining a high degree of flexibility with respect to asset class, geography and sector of the investments selected for the portfolio.

Why MATE?

MATE is targeting total returns in excess of 6% per year over rolling five-year periods.

In its new guise, MATE is designed for those investors who are looking for relatively predictable, income that grows at least in line with inflation and a diversified portfolio of investments designed to be less volatile than that of a typical equity portfolio (the managers target volatility two-thirds of that of a global equity index).

MATE’s board feels that the income ought not to come at the expense of investors’ total returns.

Why multi-asset?

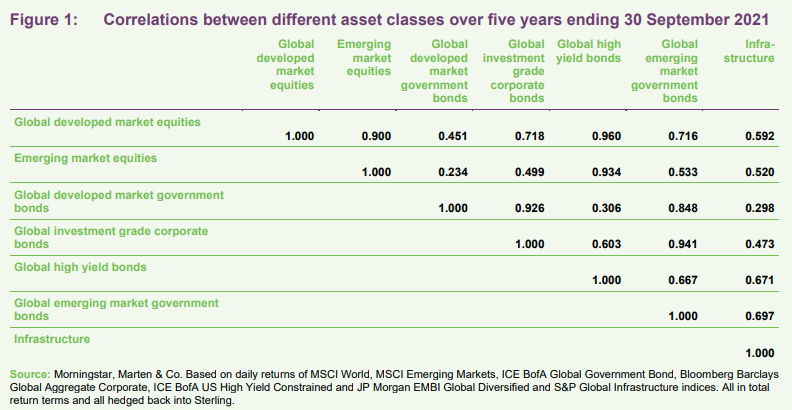

Multi-asset investing allows portfolios to be created that contain assets whose returns are not correlated with each other. The implication is that a fall in value in one asset class might not be accompanied by a fall in value in other asset classes. By building a portfolio that includes a range of less-correlated assets, a manager should, in theory, be able to achieve lower return volatility for a given expected return.

Figure 1 shows the correlations between the different asset classes that make up about 90% of MATE’s portfolio.

At the outset, MATE’s managers devised a strategic asset allocation (SAA) for the fund that was designed to optimise the combination of risk and returns. This was informed by JPMorgan’s long-term capital market assumptions (looking 10–15 years ahead) and the correlations between these different asset classes. There is no requirement for the portfolio to have exposure to all of the core asset classes that make up the SAA.

The managers also have the freedom to make opportunistic investments. For example, whilst the portfolio currently includes some convertible bonds (which are not in the SAA), it holds no investment-grade bonds. MATE may also invest in alternative assets and currently holds exposure to infrastructure, for example. An important constraint on exposure to alternative assets is liquidity.

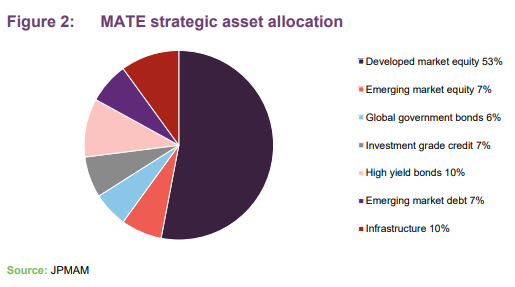

The SAA has not changed since launch and the asset class split is shown in Figure 2.

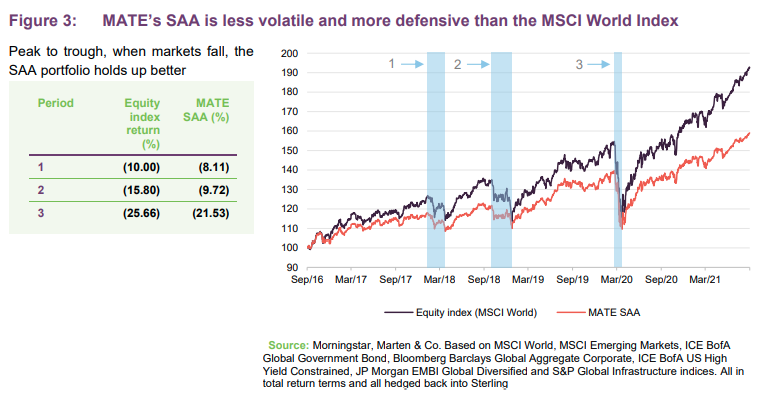

Figure 3 charts the returns from a portfolio of 100% developed market equities versus the return on a portfolio constructed in line with the SAA. Over this five-year period, the equity index outperforms. However, as the figures in the table show, in times of equity market stress, the SAA portfolio is more resilient.

Fund profile

MATE aims to provide a cost-effective investment vehicle for investors who seek income generation and capital growth from a multi-asset strategy, maintaining a high degree of flexibility, taking account of wider issues including environmental, social and governance.

Its managers seek to achieve the best risk-adjusted returns (with lower levels of volatility than a traditional equity portfolio) by investing in a globally diversified portfolio that includes company shares, bonds and other assets. Their aim is to construct a well-balanced portfolio which is flexible with respect to asset class and geography. The managers feel that this flexibility allows them to take advantage of the best opportunities to deliver an attractive total return to shareholders.

Management arrangements

JPMorgan Funds Limited (JPMF) acts as MATE’s Alternative Investment Fund Manager and company secretary. JPMF delegates the management of the portfolio to JPMorgan Asset Management (UK) Limited (JPMAM).

The lead investment managers responsible for MATE’s portfolio are Katy Thorneycroft and Gareth Witcomb, who have a combined experience of over 35 years in the asset management industry (see page 20). They are members of JPMorgan Asset Management’s Multi-Assets Solutions Team, which consists of over 80 investment professionals located across the globe, managing assets of over $304bn as at 30 June 2021. They can draw on the resources of over 1,200 investment professionals and access a platform of over 500 managers.

The wider JPMorgan Asset Management business is one of the world’s largest, managing over $2.5trn on that date. JPMorgan Asset Management also manages 21 investment trusts across a diverse range of geographies and asset classes.

A refined objective

As we described on page 3, when MATE was launched, the managers were tasked with constructing a portfolio capable of generating sufficient net income to pay a covered dividend equivalent to 4% of the IPO price that would grow over time. The managers felt that, based on the SAA that they had derived, the portfolio would be capable of generating average total returns of 6% per annum over the long term.

In time, the board came to believe that the requirement to pay a covered dividend was too constraining and, by restricting the managers’ flexibility, the company’s total returns were being compromised.

In March 2021, the company announced a refined objective and policy. The main points of this were:

- the removal of the target that dividends be covered by net revenue, with a portion of future dividends likely to be met from distributable reserves;

- a total dividend for the financial year ended 28 February 2021 of 4p (unchanged from previous years). This was paid in 1p quarterly instalments and dividends will continue to be paid quarterly (see page 17);

- an intention to grow the dividend, as a minimum, in-line with inflation, as measured by the UK’s annual Consumer Price Index (CPI), with an initial target for the financial year ended 28 February 2022 of 4.1p (1.025p per quarter);

- a change in the reference index used to benchmark the company’s returns from LIBOR one-month Sterling +4.50% each year to a total return of 6% per year, measured over a rolling five-year period (see below); and

- a change of name to JPMorgan Multi-Asset Growth & Income Plc (from JPMorgan Multi-Asset Plc).

The greater investment flexibility afforded by the refined objective has allowed the managers to invest in a number of lower-yielding but potentially attractive total return strategies.

MATE changed its name effective from 31st March 2021.

Benchmark

The previous benchmark was based on LIBOR. Following the LIBOR-fixing scandal, the FCA plans to phase out LIBOR by 31st December 2021. A new interest rate benchmark has been created, but the board felt that a clear and simple reference index would be of more use to MATE’s shareholders. The new 6% compound total return objective (measured over rolling five-year periods) is in line with the total return objective set out at MATE’s IPO. The managers believe that the return is achievable based on JPMorgan’s long-term return assumptions which inform the company’s strategic asset allocation (see page 4) and the additional alpha achievable from active positioning both bottom up and top down.

Managers’ macroeconomic views

COVID-19 and the measures taken to tackle both it and the economic fallout from lockdowns have had a profound effect on markets over the last 18 months. The managers believe that, in short-order, the global economy moved from being late cycle to a sharp slump and now a synchronised, if occasionally faltering, recovery. They say that vaccination rates and the impact of new COVID variants are still important factors in the pace of economic growth. There are also concerns over problems with supply-chains.

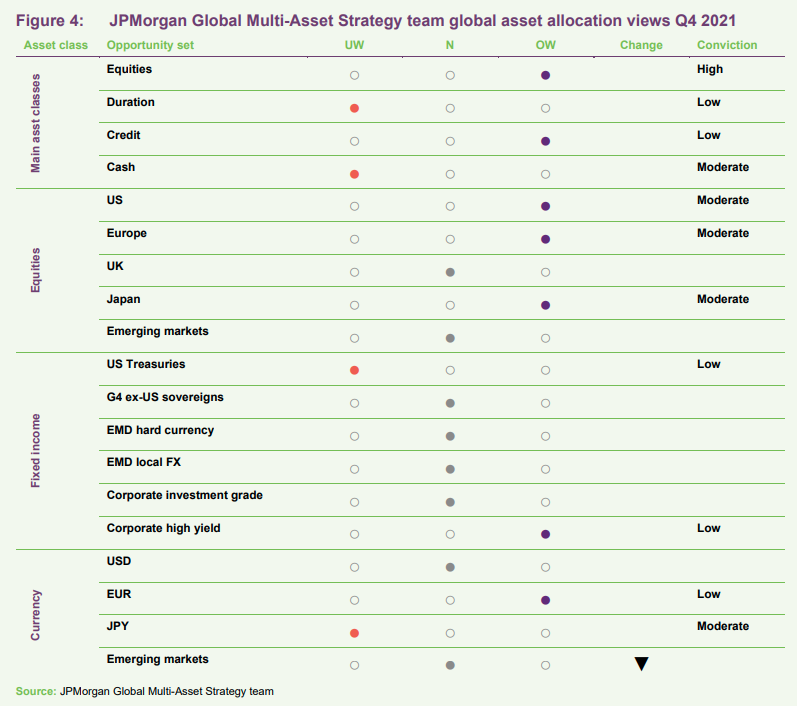

JPMorgan’s Global Multi Asset Team includes economists, market strategists, and quantitative research analysts. It is cautiously optimistic, believing that while the pace of growth is slowing, there is scope for further earnings growth. The team recognises that fiscal and monetary policy is still accommodative but thinks that investors’ focus is increasingly on the prospect of tapering.

Figure 4 shows the team’s views on various asset classes at the start of Q4 2021.

The team believes that the US economy is already mid-cycle, while other more developed economies are in the earlier stages of recovery. They favour developed markets over emerging markets and equities over bonds.

Equities are supported by growing/recovering earnings and the team’s preference is for quality, value and cyclical sectors. Bond yields are expected to rise slowly. The team’s expectation is that real yields will remain profoundly negative throughout 2022. The team has a mild underweight to duration, but thinks bonds and equities are now negatively correlated. Therefore, it makes sense to hold both in a diversified multi-asset portfolio, in the team’s view.

The team expects to see a modest increase in US interest rates, which they feel should be supportive of the US dollar in the near term, but they think the long-term trend is for a weaker dollar. Inflation has been a concern for some investors, but the team feels that while inflation is elevated now, it should normalise in 2022.

Investment process

MATE’s investment team can add value by getting their asset allocation right relative to the SAA and selecting well-managed funds. The top-down quantitative and qualitative research produced by the Global Multi-Asset Strategy Team therefore forms a key part of the investment process.

No changes have been made to the SAA since MATE was launched, but it is revisited annually. The removal of the requirement to cover the dividend has given the managers greater flexibility and increased the range of strategies available to MATE.

Typically, asset classes are accessed through funds, except for global equities, which are managed as a directly-invested portfolio. Within those funds/ or the equity portfolio, the underlying managers have full responsibility for their bottom-up investment selection, and that includes decisions relating to industrial sector and geographic exposures.

The portfolio is monitored and managed within the framework of a formal cycle of meetings.

- Macroeconomic strategy is revisited quarterly. A formal, quarterly strategy summit helps to set the broad research agenda and determine MATE’s asset allocation.

- Monthly portfolio construction meetings will typically trigger changes to the portfolio. Changes to the portfolio are usually made gradually.

- However, the portfolio managers also attend daily meetings which capture significant developments and facilitate a discussion of event risks.

The next element of the investment process is evaluating and selecting investment teams, within JPMorgan Asset Management, to oversee individual asset class allocations in the portfolio. The managers may feel that an external manager may provide better access to a particular asset. MATE may invest in other investment companies in this context. For example, currently the portfolio has some of its infrastructure exposure through 3i Infrastructure. The managers say that they would not use externally-managed open-ended funds.

The managers adjust MATE’s overall market exposure and regional asset allocation by using equity index futures and bond futures.

Risk management is an integral, ongoing and critical part of the managers’ investment process. They believe that risk is a necessary component of active investment management, and that it can be estimated, measured and managed.

The lead managers monitor a range of aspects such as performance, portfolio diversification and the potential impact of proposed portfolio changes.

A risk team, embedded within the Multi-Asset Solutions Team, monitors a broad range of ex-ante risks and market sensitivities; stress tests against market scenarios and asset price shocks; and monitors risk concentrations both within MATE’s portfolio and across all portfolios.

An independent risk management team monitors trading and portfolios across the manager’s business, looking at aspects such as Value at Risk (VaR).

Examples of quantitative factors that the managers take into consideration include the correlations between strategies, downside risk and consistency of performance. In addition, face-to-face meetings with the managers and investment teams responsible for the different parts of the portfolio allow the lead managers to clarify more qualitative factors such as the stability of investment process, stability of investment team and risk measurement.

ESG

In the belief that consideration of ESG factors can help deliver enhanced risk-adjusted returns over the long run, ESG is integrated into the investment process across all asset classes.

The investment process includes a quantitative element which draws on MSCI data, but also integrates JPMorgan Asset Management’s proprietary research. The over-150 analysts covering stocks complete a globally consistent checklist of 40 ESG questions on every company they follow.

In addition, JPMorgan Asset Management is developing its own ESG framework and carries out detailed research into specific ESG topics.

A central Stewardship team sets priorities for corporate engagement both in terms of issues and in terms of significant individual investments held in portfolios. They have ongoing dialogues directly with companies’ top management.

Investment restrictions

The company has the following investment restrictions at the time of investment, calculated on the company’s total assets:

- no individual investment may exceed 15%, with the exception of developed countries government bonds and funds;

- no single developed country government bond or fund will exceed 30%;

- for investment in funds, on a look-through basis, no individual investment may exceed 15%; and

- listed equities and fixed income securities will represent not less than 50%.

Derivatives and hedging

Whilst MATE has the ability to borrow money, in practice it has not done so. Instead, when they feel it is appropriate, the managers achieve leverage through the use of futures.

MATE’s managers use derivatives to seek to enhance portfolio returns and for efficient portfolio management, to reduce, transfer or eliminate risk in its investments, and to offset exposure to a specific market. For example, the current underweight duration in the bond element of the portfolio has been achieved by shorting long-dated government bonds.

MATE usually hedges developed market currency risk back to Sterling. However, they may, as part of the overall asset allocation process, decide to retain currency exposure as part of their investment strategy.

Asset allocation

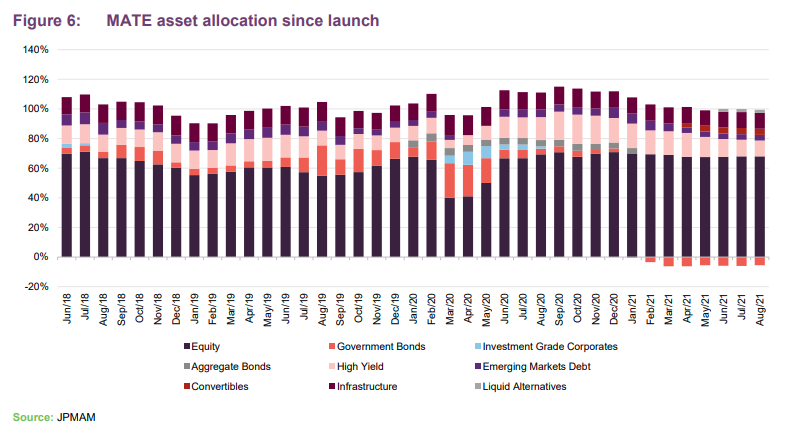

Figure 6 shows how MATE’s actual asset allocation has changed since launch.

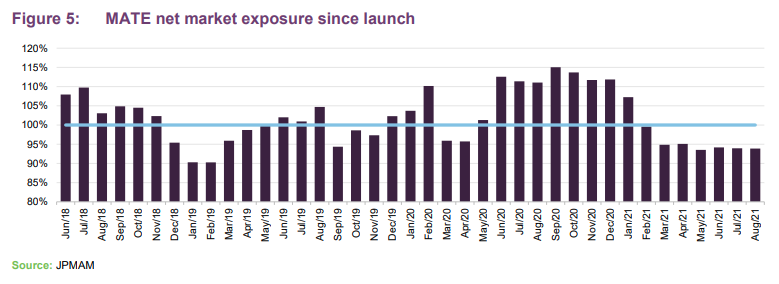

In February 2020, MATE’s portfolio was 110.2% invested, with an overweight allocation to equities relative to the SAA. When markets crumbled in March 2020, the managers cut the equity exposure savagely and this was not reversed for a couple of months.

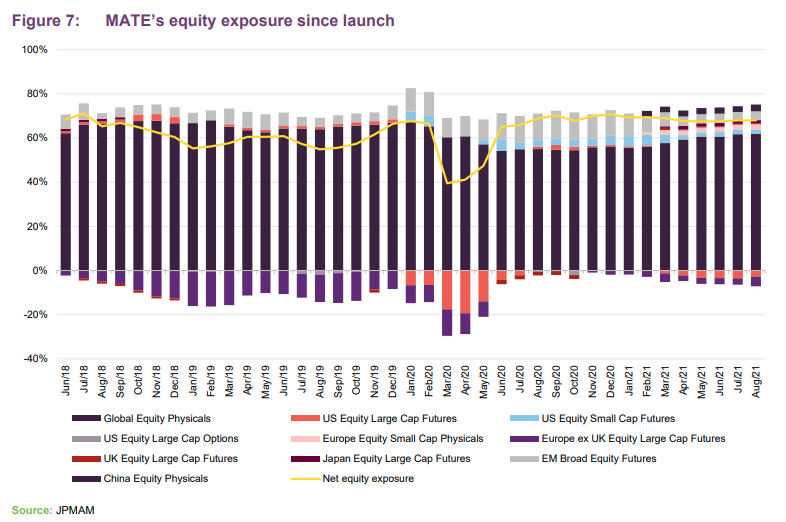

Figure 7 shows how the composition of the equity portfolio and the net equity exposure has changed over time. In the wake of the pandemic panic, MATE’s net equity exposure fell to 39.5%, but by September it was in excess of 70%.

Unfortunately, MATE missed out on the equity market rally that occurred in April and May. This had a significant influence on MATE’s returns last year as we discuss on pages 14 and 15. The managers say that, at the time, they felt that there was no clear catalyst for a change in their risk perception.

However, the managers did add to MATE’s investment grade bond exposure and rode the rally in that. Those positions were liquidated over Q4 2020, but MATE’s high yield exposure was maintained until quite recently when they have trimmed it a little. MATE benefited from its leverage over the second half of 2020.

The position at end August

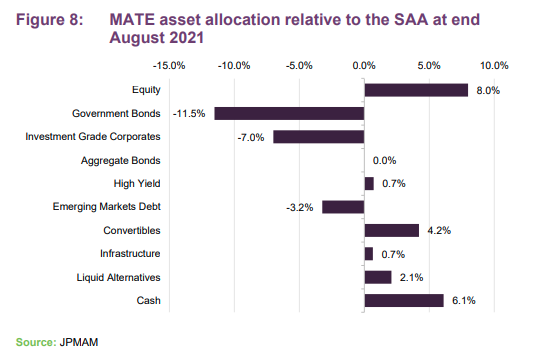

The managers say that they are still pro-risk today. An 8% overweight exposure to equities is complemented by 4.2% in convertible bonds, which equates to about a 10% overweight exposure to equities in total. The portfolio is underweight duration by about half a year, reflecting an expectation that long-term yields will rise. However, they do not believe that the modest increase in yields that they foresee will have much of an impact on the trust’s infrastructure exposure. Whilst the portfolio does have a net market exposure of 93.9%, overall, the managers are positive on markets.

The rationale for this is an ongoing earnings recovery. The managers feel that the tick up in inflation that we have experienced in 2021 is transitory.

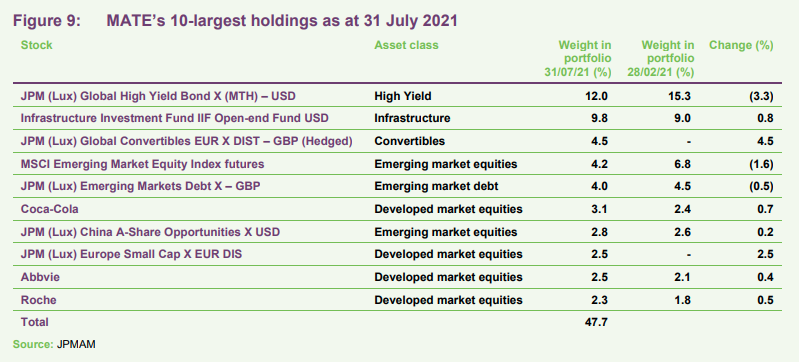

The 10 largest holdings

With the freedoms granted by the revised objective, the managers added exposure to European small cap, China A share and convertibles to the portfolio. The managers say that the China A share exposure (incorporated into the emerging market allocation in Figure 10) has been increased over a period when political concerns have been weighing on Chinese stock prices.

Equity portfolio

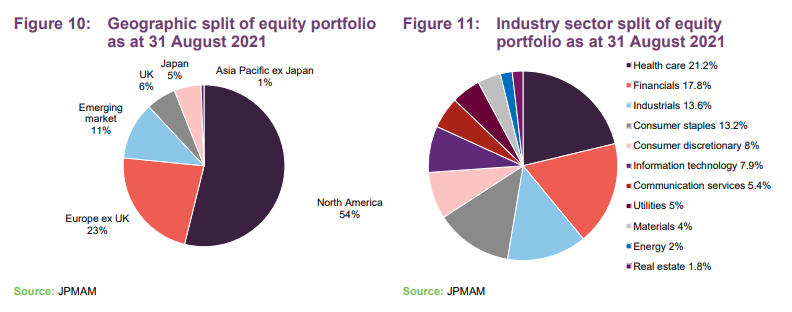

Relative to the MSCI AC World Index, the equity portfolio has a significant underweight exposure to the information technology and consumer discretionary sectors and an overweight exposure to health care – notably, large pharmaceutical companies.

The revised objective also facilitated a change to the composition of the directly invested global equity portfolio. MATE now has a higher proportion of lower-yielding stocks.

Top 10 equity positions

MATE’s leading equity positions were not much changed over the six-month period ending 31 August 2021. The overall allocation to equities was increased. A few stocks slipped down the ranks, falling outside the list – Iberdrola, Zurich Insurance and Texas Instruments all dropped out to be replaced by Procter & Gamble, Nestle, and Yum Brands (operator of brands such as Taco Bell, KFC and Pizza Hut).

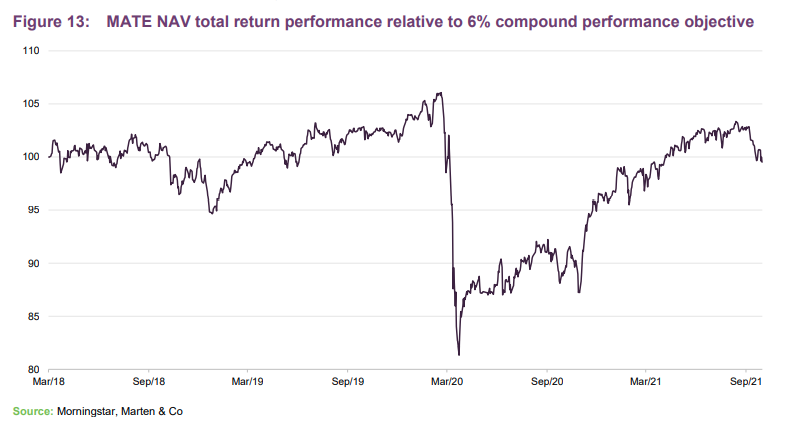

Performance

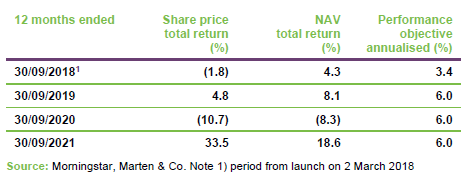

As Figure 13 demonstrates, after an almost two-year period of where MATE met and even exceeded its 6% per annum total return objective, the dislocation in markets caused by COVID-19 hit it hard. The managers were caught off-guard by the outbreak of the virus. They had been positioning the portfolio for a period of good returns from equities.

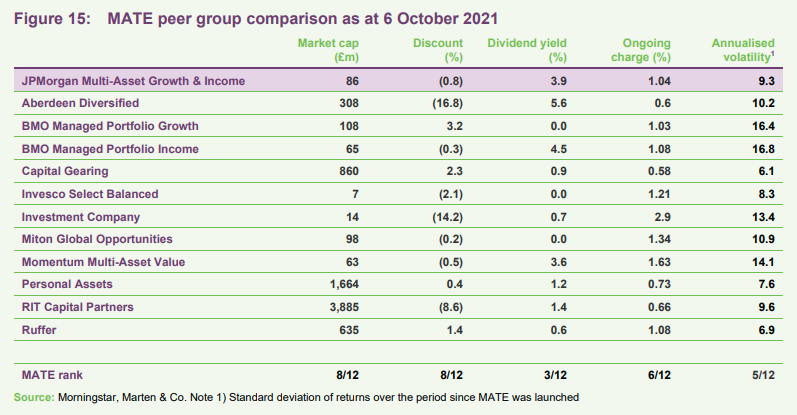

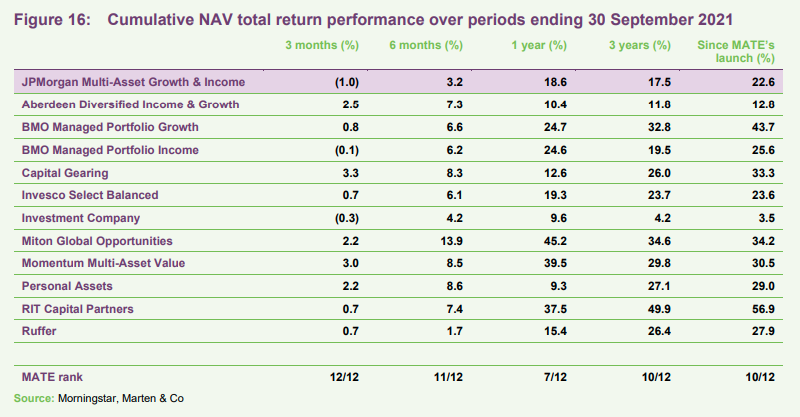

Peer group

MATE is a constituent of the AIC’s Flexible Investment sector. These funds have investment objectives and/or policies that allow them to invest in a range of different asset types – multi-asset funds, therefore. However, this encompasses a wide variety of funds with very different performance objectives.

The list of funds that we have selected for Figures 15 and 16 exclude Caledonia Investments (a trust managed on behalf of a family), CIP Merchant Capital (which has a very concentrated portfolio of influential stakes in small companies), Hansa Investment Company (a family-controlled trust with a strong bias to Brazil and which recently moved its domicile to Bermuda), JPMorgan Core Real Assets (which has no equity exposure), JZ Capital Partners (a private equity fund that strayed into real estate with disastrous results), Livermore Investments (which has a strong bias to structured finance), New Star Investment Trust (which is run largely for the benefit of ex-employees of New Star), RiverFort Global Opportunities (which provides financing to very small companies), Schroder BSC Social Impact (which aims to make investments that have a positive social impact), Tetragon Financial Group (which invests in a wide variety of alternative investments including an asset management business), and UIL (a split capital company with an eclectic portfolio).

Even this pared-down list encompasses quite a wide variety of investment styles and risk appetites. The closest comparator to MATE may be Aberdeen Diversified Income & Growth.

MATE’s managers may have previously been constrained by the requirement to cover the dividend, potentially to the detriment of its performance historically, but this restriction has now been removed. As can be seen from Figure 15, few of these funds offer high yields, and those that do tend to have lower long-term total returns. Going forward, our intention is to highlight MATE’s returns since the strategy change.

Nevertheless, we note that MATE has been meeting its volatility objective. Its annualised standard deviation of returns since launch is 9.3, almost half that of the MSCI World Index, which was 18.0.

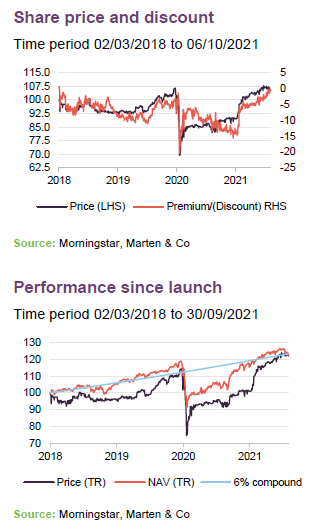

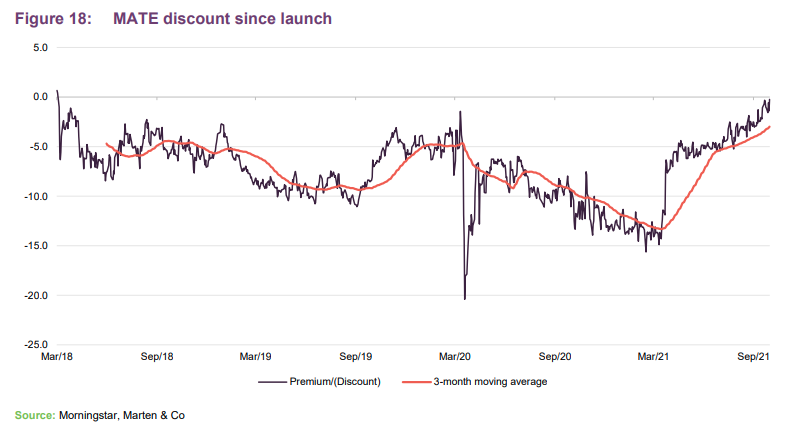

MATE is on the small side. However, we note that the discount has almost been eliminated.

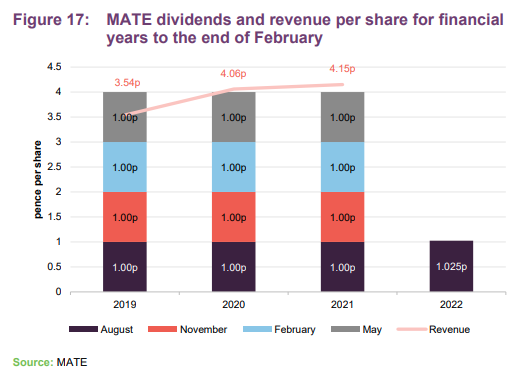

Predictable, inflation-linked dividend

MATE met its initial 4p dividend target, but under the previous strategy did not manage to achieve dividend growth. The new strategy should have changed this, however.

The board’s objective is to grow the dividend at least in-line with inflation, as measured by the UK CPI, funding part of the dividend from distributable capital reserves, if needed.

The dividend target for the current financial year is 4.1p, 2.5% ahead of FY 2021.

At 28 February 2021, MATE had revenue reserves of £681,000. It also had a distributable special reserve of £84.8m. Together, these accounted for almost 97% of shareholders’ funds.

Premium/(discount)

Over the year ended 30 September 2021, MATE’s shares moved between trading at a 15.6% discount and a 0.2% discount and, on average, traded at a discount of 8.2%. On 6 October 2021, MATE was trading at a discount of 0.7%.

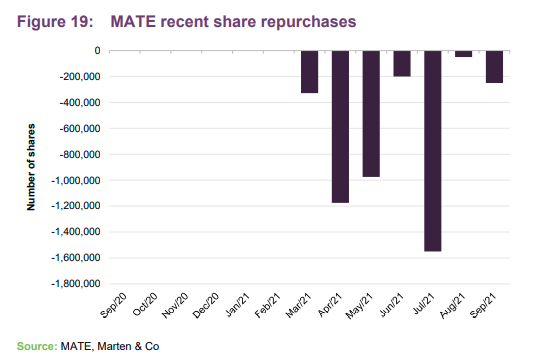

The board believes that it is in the interests of shareholders to maintain a share price as close as possible to the NAV. It considers using buybacks to address imbalances in supply of and demand for MATE’s shares in the market, when it believes it is in the interests of all shareholders and subject to normal market conditions.

Shareholders have granted the board the authority to repurchase shares in the market either for cancellation or into treasury. Such repurchases are carried out at a price below NAV, thereby enhancing the NAV for ongoing shareholders. As is typical, the limit on the amount of shares that can be repurchased is 14.99% of the shares in circulation on the date of the last AGM.

The directors may also sell treasury shares or issue new ordinary shares at a premium to NAV. Here the authorised limit is 10% of the shares in circulation on the date of the last AGM.

As Figure 19 shows, since March 2021 (immediately following the announcement of the changes to the objective), MATE has been repurchasing its shares on a fairly regular basis, to the benefit of a narrower discount.

The managers believe that the programme of share repurchasers has helped to remove those large investors on the share register who were motivated by the prospect of a narrowing discount.

Patrick Edwardson, a non-executive director of MATE since October 2020, acquired 5m shares at 100.9p on 13 May 2021 and now holds 6.6% of the company. Patrick had a long career as a manager of similar vehicles.

Fees and costs

MATE’s investment management fee is charged at the rate of 0.65% per year on the first £250m of NAV and 0.60% on the balance. No performance fee is payable at the company level, but the portfolio may be invested in funds that charge performance fees and these are not rebated. The management fee is calculated and paid monthly in arrears.

Where they are available, investments made through funds managed by J.P. Morgan Asset Management are in non-management-fee-bearing share classes. Where a non-management-fee-bearing share class is not available, the investment will be made through the lowest institutional-fee-bearing share class available and MATE’s investment management fee is reduced to offset these charges.

The investment management agreement is terminable by either party on six months’ notice or on shorter notice in certain circumstances.

All secretarial and administrative services are also provided by JPMF and the costs of these services are included in the management fee.

For the year ended 28 February 2021, administration expenses of £212,000 (FY20: £182,000) and directors’ fees of £120,000 (FY20: £137,000) made up the bulk of MATE’s other expenses.

MATE’s ongoing charges ratio, calculated for the year ended 28 February 2021, was 1.04% (FY20: 1.01%).

Capital structure and life

MATE has ordinary shares and no other classes of share capital. At 6 October 2021, there were 93,115,643 ordinary shares in issue. 11,547,235 ordinary shares were held in treasury and therefore the number of shares in circulation and with voting rights was 81,568,408.

The company’s accounting year end is the end of February, and it usually holds its AGMs in June/July.

Gearing

MATE may use gearing, in the form of borrowings and derivatives, to seek to enhance returns over the long term. At present, the company has no bank loans/facilities or structured debt.

Borrowings may be in sterling or other currencies. Total borrowings will not exceed 20% of net asset value at the time of drawdown. Total net investment exposure, including derivative exposure, would not normally be expected to exceed 120% of NAV.

Continuation vote

Whilst MATE is designed to have an unlimited life, the directors will ask shareholders to vote on the continuation of the company at MATE’s fifth AGM, expected to be held in 2023. Assuming that this is passed, subsequent continuation votes will be held at five-yearly intervals thereafter.

Managers

Katy Thorneycroft, managing director, leads Multi-Asset Solutions’ International Portfolio Management team, focusing on multi-strategy investing, including benchmark oriented, flexible and total return strategies, as well as funds of investment trusts. Katy has worked for what is now JPMAM since 1999, having previously been a portfolio manager in the convertible bonds team and a member of the Multi-Asset Solutions team in New York. Prior to this, Katy was a portfolio manager in the European Equity group in London focusing on small and mid-cap strategies. Katy has an M.Chem. from the University of Oxford and is a CFA charterholder.

Gareth Witcomb, executive director, is a portfolio manager in the Multi-Asset Solutions team, based in London. He manages global balanced portfolios and flexible mandates, and participates in the asset allocation framework, where he specialises in providing fixed income insight. Gareth has previously worked on JPMAM’s macro strategies and alternative beta products as a portfolio manager. An employee since 1998, Gareth joined the Multi-Asset Solutions team in 2005. Gareth has a B.A. in History and Politics from University College Wales.

Board

MATE’s board is comprised of four directors, all of whom are non-executive, independent of the manager and who do not sit together on other boards. Whilst three of the directors were appointed when the company was incorporated in December 2017, ahead of its March 2018 listing, the board has been refreshed since launch as two directors, Richard Hills and Sir Laurence Magnus, have stepped down (in July 2020 and October 2020, respectively).

Each of the directors stands for re-appointment at each AGM.

Sarah MacAulay

Sarah is chairman of Schroder Asian Total Return Investment Company Plc and a director of Aberdeen New Thai Investment Trust Plc and Fidelity Japan Trust Plc, as well as a trustee of Glendower School Trust, an educational charitable trust.

She has 20 years of Asian fund management experience in London and Hong Kong managing significant institutional assets and unit trusts. Sarah was formerly a director of Baring Asset Management (Asia) Ltd, head of Asian equities at Kleinwort Benson Investment Management and Eagle Star Investment Management.

James West FCA

James is a former chief executive of Lazard Asset Management and a managing director of Lazard Brothers, prior to which he was managing director of Globe Investment Trust Plc. He is currently chairman of Associated British Foods Pension Fund Ltd.

Patrick Edwardson

Patrick is a non-executive director of The Edinburgh Trust Plc. He has substantial experience as a fund manager with Baillie Gifford, where he was a partner and head of the multi-asset team.

Sian Hansen

Sian is currently global chief operating officer with CT Group and a non-executive director of Pacific Assets Trust Plc. From 2013 to 2016 she was executive director of the Legatum Institute, a global public policy think tank, and previously she spent seven years as managing director of UK think tank Policy Exchange. She is currently a trustee of The Almeida Theatre. Formerly, Sian was a director and co-head of sales for Asian Equities at Société Générale, and prior to that, she was an equity analyst with Enskilda Securities in Europe.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on JPMorgan Multi-Asset Growth & Income Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.