Has logistics been oversold?

The sell-off of real estate investment trusts (REITs) has been breathtaking, with industrial and logistics-focused funds taking their fair share of pain. The major concern is that borrowing costs are now higher than the initial yields on their portfolios, implying an upward re-basing of property yields and a decline in portfolio values.

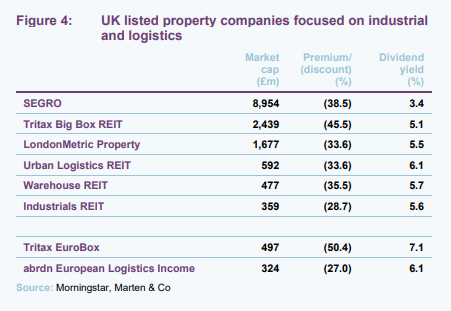

The average discount among the eight London-listed, industrial and logistics-focused companies has widened to 37.5%. Most were on hefty premiums just six months ago. But what these discount ratings seem to have failed to take into consideration is the off-setting effects of rental growth on valuations and the continued strong occupier market. While demand remains robust, the vacancy rate is the key metric for rental growth and lies at around 3% in the UK and Europe. This suggests substantial rental growth will continue.

As industrial and logistics yields move out, rental growth in the sector will play an important role in cushioning the impact on values. We have run a number of scenarios to assess the impact of higher property yields and rental growth on valuations and even using our most aggressive assumptions suggests valuation declines that are less than are implied by current discounts (see page 5).

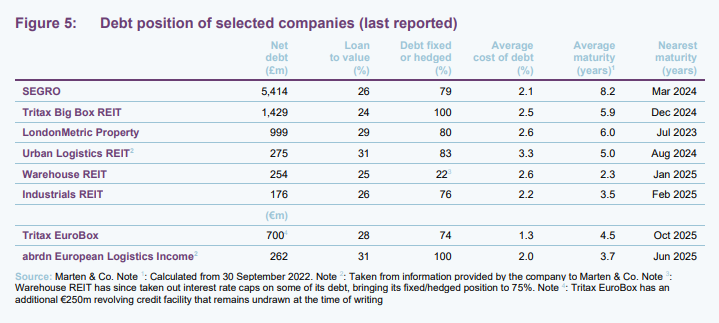

When you take into account the strong balance sheets within the sector – with an average LTV ratio of 27%, current average debt cost of 2.3% with a five-year average duration and more than 80% of total debt costs fixed – then the discounts do seem unjustified.

As we look forward, if inflation can be brought under control and the cost of debt falls then real estate valuations falls should be reversed.

Valuations under pressure from rising rates

The higher interest rate environment has brought into sharp focus the valuation of commercial real estate. After the Bank of England increased the base rate to by 0.5% to 2.25% in September, the catastrophic impact of the ‘mini’ budget at the end of September sent bond markets into turmoil and raised interest rate expectations further. Meanwhile, in Europe the European Central Bank announced in September a record rise in eurozone interest rates to 1.25% to help fight inflation.

Rising rates are putting pressure on investment yields across the commercial real estate sector. The five-year SONIA swap rate (the typical floating rate on which banks add their margin for lending to real estate) increased from 0.97% in October 2021 to 4.65% in October 2022. The five-year Euribor swap rate (the European equivalent) increased from -0.099% to 2.985% in the same period. This pushed the total cost of debt close to or higher than the prime real estate yield for many segments of the property market, where yields had compressed to sub-3% in some prime markets.

Without the availability of low-cost finance, which had pushed yields to new record low levels, many leveraged investors have been taken out of the market and the pressures that underpinned pricing have been taken away. Lower-yielding commercial real estate sectors, such as industrial and logistics, find themselves one of the most susceptible among the real estate sectors to softening investment yields and falling capital values.

On top of this, rising interest rates are putting pressure on loan covenants, which could precipitate forced sales. As values fall, loan to value (LTV) covenants could also start to feel the heat. Refinancing loans at the end of their term could also become impossible for some highly leveraged real estate companies, forcing a fire sale of assets and driving a further decline in values in the market. This is more likely to be the case in retail and some office sectors, where values have fallen over the past five years (the typical loan term) and lending conditions have tightened meaning many assets now have a lower LTV ratio than they did five years ago. This is less of an issue in the industrial and logistics sector where values have risen sharply in the same period.

By how much values fall in the industrial and logistics sector (which has seen values rise furthest over the past decade), it is too early to say and depends on a number of factors including how long it takes to bring inflation under control – something inherently linked with the war in Ukraine and energy prices. Goldman Sachs has predicted commercial property values in the UK to fall by between 15% and 20%, while Oxford Economics and Bayes Business School forecast values to fall by up to 35% – mainly in the retail sector.

Understandably, there has been a hiatus in industrial and logistics investment over the past few months as investors assess the market. However, the first signs of tangible valuation declines are starting to come through. UK real estate fell by 2.6% on average in September and 5.1% in the quarter to the end of September, according to the MSCI/IPD UK Monthly Property Index, which tracks the value of more than £50bn of UK real estate. The industrial sector was the hardest hit, with a 4% decline in London and the South East of England, a 3.7% fall in distribution warehouses and a 3% drop in the rest of the UK. Industrial is still up over the long term, however, having risen by 15.6% in the UK over the past 12 months.

Has logistics been oversold?

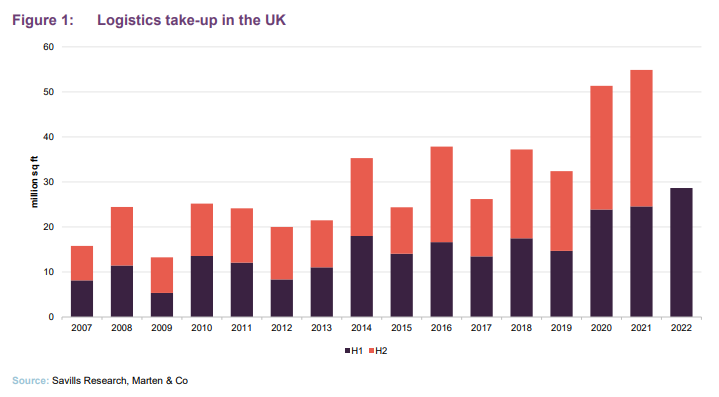

The importance of rental growth during this period of capital value falls cannot be overstated. On the occupier front, the logistics sector is still displaying strong characteristics, with both supply and demand metrics favourable and continued rental growth likely. Take up of logistics space in the UK hit a new record in the first half of 2022, with 28.6m sq ft of deals signed (surpassing last year’s half-year total of 24.5m sq ft), according to Savills. The effect of e-commerce is still playing out, but there has also been a resurgence in demand from the manufacturing and automotive sectors, where concerns over supply chain resilience and the need to hold more inventory have become more important and are leading to more space requirements. Looking forward, there was 19.4m sq ft of space under offer (including pre-let developments) at the end of June, according to CBRE and 200m sq ft of longer-term occupier requirements logged by Savills.

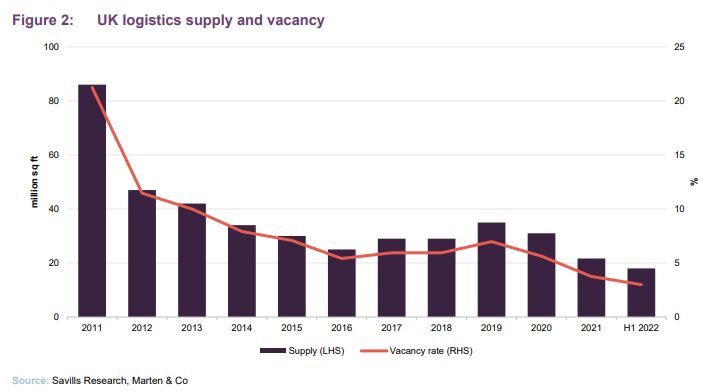

On the supply side, there is currently just 18.4m sq ft of available space, according to Savills, and CBRE estimates that ‘ready-to-occupy’ space remains at historically low levels of 1.2%. Figure 2 shows the supply and vacancy rate since 2011, with the current vacancy rate at 3.0%.

Development of new buildings is unlikely to keep pace with demand. Savills is tracking 16.5m sq ft of speculative development due for delivery in 2022 and 2023 and given the wider economic context, new announcements are expected to tail off.

It is a similar picture in Europe, where vacancy rates are 2.9% on average and less than 2% in many prime locations. Take-up of space in the first half of the year was 12% up on the same period in 2021, according to Savills. This supply and demand tension saw rents across the UK increase 16% from February 2022, according to the MSCI monthly index. In Europe rents increased by 8.2% in the year to June 2022. JLL’s European logistics rental index, which includes the UK, rose to 14.2% in the second quarter of this year.

Most real estate portfolios have some form of inflation protection baked into them through index-linked leases. Typically, these have caps and collars in place (usually capped at 4%). Indexation is more prominent in Europe, where a majority of inflation-linked leases are uncapped (meaning they will rise on an annual basis in line with inflation, which in September was 10.9% in the European Union).

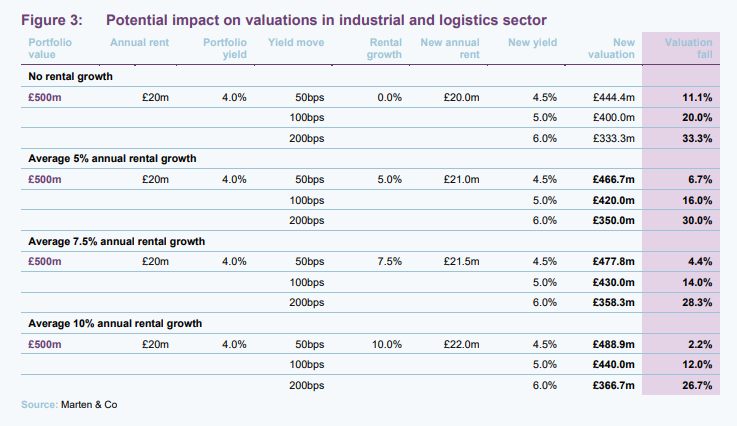

As industrial and logistics yields move out, rental growth in the sector will play an important role in curtailing the impact on values. Figure 3 details the impact on valuations in certain scenarios of yield movement and rental growth. It shows the impact of a 50bps, 100bps (equivalent to a 20% fall in valuations as predicted by Goldman Sachs) and a 200bps move in yields, coupled with the effect of different rental growth scenarios. Although a rate rise greater than 200bps is not out of the question, it is our assumption that a further 200bps would be more than enough to bring inflation under control.

Figure 3 shows the importance of capturing rental growth during this period. In this scenario, a 50bps move out in yields could see a £500m portfolio fall in value by 11.1%. However, this fall is offset by rental growth over the period, with a 5% increase in the portfolio rental income cushioning the blow to a 6.7% valuation fall. The same is true for a 100bps and 200bps move in yields. The greater the average annual rental growth, the greater the cushioning effect on valuations.

In a worst-case scenario of no rental growth and 200bps move in yields, valuations would fall by 33.3%. Many of the listed, industrial and logistics-focused property companies are trading on discounts to NAV beyond this figure, as shown in Figure 4. The market may also be pricing in a recession into the rating, but with such strong supply and demand dynamics (as mentioned above), the industrial and logistics sector should be able to weather any storm.

Most of the industrial and logistics property companies have a focus on asset management initiatives to capture rental increases borne out by the supply and demand dynamics in the sector. Asset management initiatives by Urban Logistics REIT, for instance, has contributed to 71% of the uplift in valuations across its portfolio since it launched in 2016 – a significant number considering the yield compression witnessed over the period.

Another example is Industrials REIT, which owns a portfolio of multi-let industrial estates, which has developed a technology-enabled operating and leasing platform that has improved performance and reduced cost across the business. It hopes that platform will transform the way in which the multi-let industrial sector is managed in the future, in line with other customer-focused property sectors such as self-storage, student accommodation and hotels.

Debt positions

For those companies that are particularly highly leveraged and exposed to variable rates, the impact of rising interest rates on earnings will be significant. Following the financial crisis of 2007/8, where many property companies got their fingers burnt with highly leveraged portfolios, the sector seems to have learnt their lesson and is in a much better place this time around.

Figure 5 is a snapshot of the debt position of the listed, industrial and logistics-focused companies and shows that LTV ratios are pretty conservative across the board and the majority of debt is either fixed or hedged against interest rate rises.

The majority of the companies are in a strong position with debt fixed or hedged, protecting it from further increases in interest rates. Sector leader SEGRO, for example, has stated that a further 100bps rise in benchmark rates from current levels would increase its cost of debt by 24bps. The same rise in benchmark rates would increase LondonMetric’s cost of debt by 20bps and reduce earnings per share by 0.2p on an annualised basis. Rental growth and its high level of inflation-linked rent reviews would mitigate against this potential rising interest costs.

While refinancing debt will be painful, none of the companies have a material refinancing event until 2024 (LondonMetric’s nearest maturity in 2023 is for £83m). Unlike other sectors, especially retail, loan covenants are unlikely to come under pressure despite valuation falls. The value of the property or portfolio with which LTV covenants are imposed are set at the start of the loan term and the substantial valuation uplifts witnessed since then should negate/offset recent and future valuation declines. For SEGRO, property valuations would need to fall by around 62% from their 30 June 2022 levels to reach the covenant threshold, while a 50% drop would put both LondonMetric and Tritax Big Box REIT at risk.

Interest coverage ratio (ICR) covenants (net interest covered by net property rental income) are typically set at 1.5x and would require a material drop in rental income to come under pressure, which as mentioned earlier seems improbable.

Attractive buying opportunity?

Predicting where interest rates and real estate prices will go from here is impossible. But if one looks through the current interest rate cycle and trusts that inflation will be brought under control at some point within an investable timescale, then the hope is that as the cost of capital reduces real estate values will rise again. Our worst-case scenario of a 200bps move in yields and no rental growth, as displayed in Figure 3, would see valuations fall 33.3%. Many of the discounts that industrial and logistics property companies are trading on are currently wider than this. Couple this with the strong occupier market fundamentals and the relatively strong balance sheets (conservative LTVs, a high percentage of fixed/hedged debt and long maturities) leads us to believe that logistics has been oversold.

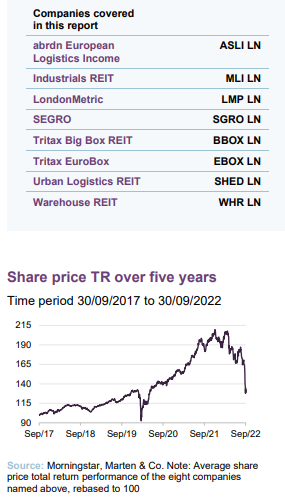

Appendix: Performance

Legal

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority). This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access. No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.