Selloff provides opportunities

Shares in the good-quality growing businesses favoured by Montanaro UK Smaller Companies (MTU) have experienced a sharp selloff since the beginning of 2022, when interest rates began to rise in response to rampant inflation.

Manager Charles Montanaro is focused on picking stocks for the long term rather than trying to second-guess macroeconomic trends. He and his extensive team have a strong dialogue with the management of these companies. He observes that high-quality, well-managed small businesses with strong market positions and pricing power have been able to pass on additional costs and are better able to cope with supply chain disruptions. Charles believes that following the selloff, valuations are now the most attractive that they have been in many years. This could be a great opportunity for long-term investors.

UK small cap with a bias to quality

MTU aims to achieve capital appreciation through investing in small quoted companies listed on the London Stock Exchange or traded on AIM, and to outperform its benchmark, the Numis Smaller Companies Index (excluding investment companies).

At a glance

Share price and discount

Over the year ended 30 June 2022, MTU’s shares traded in a range from a discount of 15.2% to a premium of 1.1% with an average of a 4.7% discount (and a median discount of 3.8%). The company has worked hard to make MTU more attractive to private clients, including a five-for-one share split in 2018, the enhanced dividend policy, reducing costs and an increased focus on marketing which the board hopes will reduce discount volatility over time.

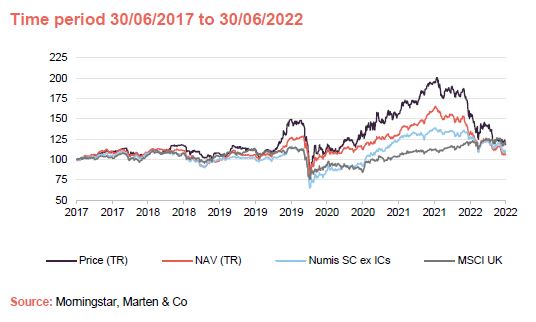

Performance over five years

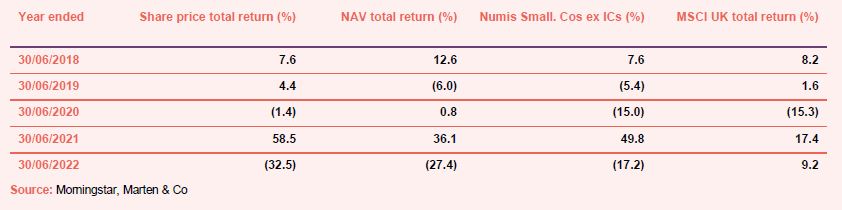

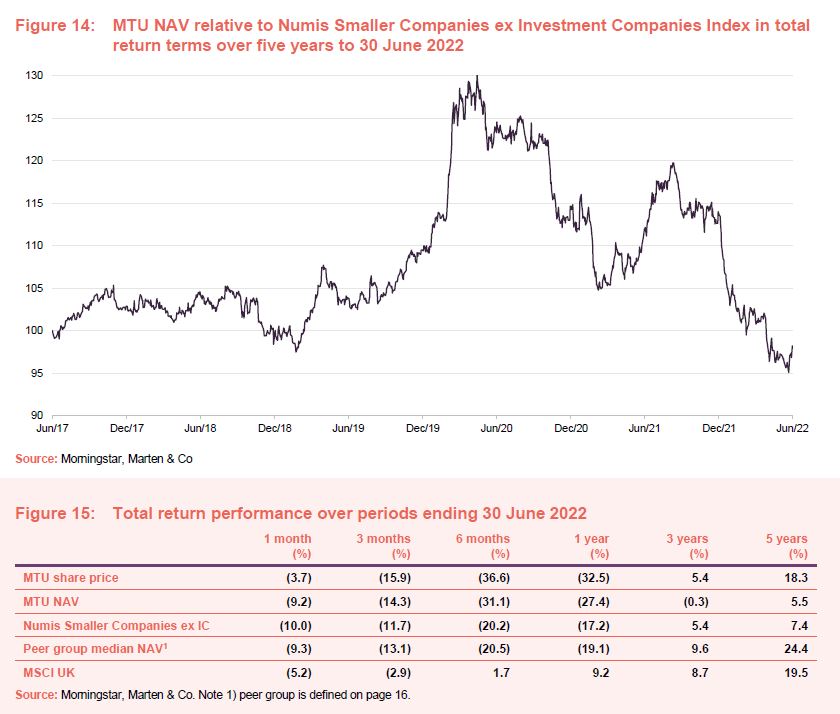

MTU’s outperformance of the Numis Smaller Companies ex ICs index accelerated in the spring of 2020, as investors became more unnerved about the likely effects of COVID and sought safety in the high-quality and growth stocks that are the focus of MTU’s portfolio. However, the good news on vaccines in 2020 triggered a sharp rotation into value stocks. Against that backdrop, MTU lagged the benchmark index.

Fund profile

MTU is a UK smaller companies trust with a focus on capital growth. Montanaro Asset Management Limited (MAML) is the trust’s Alternative Investment Fund Manager (AIFM). Charles Montanaro established MAML in 1991, and MTU was launched in March 1995 with Charles as its lead manager. He has been the trust’s named manager for about three-quarters of its life, most recently returning in 2016. This year, Guido Dacie-Lombardo was appointed as back-up manager to MTU. However, Charles has assured the board that he is happy to remain as MTU’s named manager until at least 2026.

The trust raised £25m at launch and topped that up with a £30m C share issue the following year. Today, the trust has a market cap of £174m.

MAML has one of the largest teams in Europe (and the largest in the UK) focused on researching and investing in quoted small- and mid-cap companies. It boasts 37 team members, including 16 analysts and portfolio managers. The team is experienced, multi-lingual, multi-national (10 different nationalities), and there is relatively little turnover of staff. At the end of March 2022, MAML had assets under management of more than £4.3bn (this was over £5bn at the end of 2021). Charles Montanaro and his family together own 95% of the business, and head of investments Mark Rogers owns 5%. However, the wider team has options over about half of the equity.

The trust is benchmarked against the Numis Smaller Companies Index (excluding investment companies), and we have also used the MSCI UK Index as a performance comparator in this report. The benchmark plays no part in determining which stocks are selected for the portfolio, or how large positions are as a percentage of net assets.

MAML owns around 5% of the trust, which helps align its interests with those of other shareholders.

A turbulent couple of years

A lot has happened to markets across the globe since our last note, Long COVID effect requires a focus on corporate health, was published on 16 April 2021.

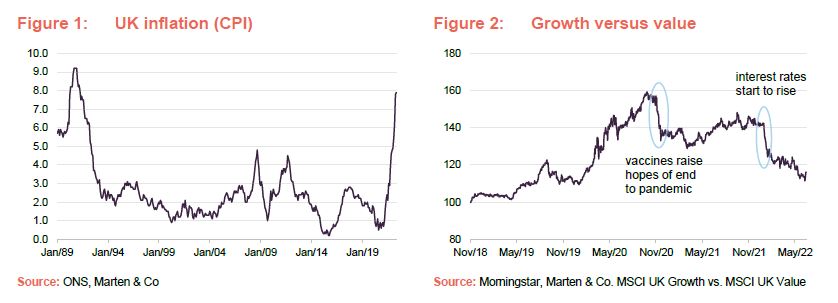

As we approached the end of 2021, investors grew increasingly concerned about inflation and began to anticipate interest rate rises. Following a significant increase in energy costs and household expenses more generally, the Bank of England’s monetary policy committee (MPC) has now raised its key rate to 1.25% with 0.25% jumps in February, March, May and June. The February move was followed soon after by an announcement from the European Central Bank (ECB) of a sharp turnaround in its interest rate policy; a 0.25% hike in its interest rate is expected in July.

Meanwhile, the Russian invasion of Ukraine, which started at the end of February of this year, has made investors more risk-averse and exacerbated the inflation problem. While both countries are small in terms of their contribution to the global economy, the ramifications of Russia’s shocking actions and the sanctions applied have already been felt in commodity markets and could weaken the outlook for the global economy and sentiment more generally.

Charles Montanaro, manager of MTU, says that it has been the most volatile two-year period that he can recall, in a career in investing spanning more than four decades. Charles feels that just when the world appeared to be finally emerging from two exhausting years of a pandemic and lockdowns, we find ourselves wrestling with extraordinary macroeconomic and geopolitical uncertainty once again.

Fears of persistent and significant price and wage increases have resurfaced globally, including in the UK where inflation has recently climbed to a 40-year high. The war in Ukraine is further amplifying the pressure on food, commodity and energy prices, while consumers are faced with the prospect of a significant increase in the cost of living. Meanwhile, businesses are doing their best to manage the pressure on margins from rising input costs and supply chain challenges.

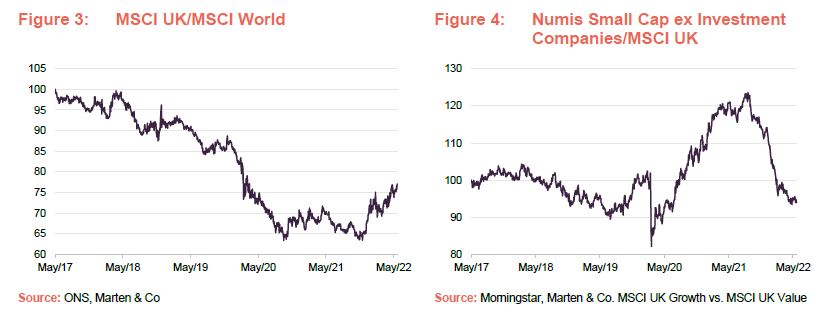

The direction of inflation and interest rates triggered a sharp rotation from growth-style investing – the second-biggest rotation into value globally in 50 years. Over 2022, UK large cap indices have fared well relative to global indices, reflecting a low exposure to technology and high exposure to resources and staples. However, UK small and mid-cap stocks have lost ground relative to large caps. Year-to-date, the MSCI United Kingdom index is up 1.67% while the Numis Smaller Companies ex Investment Companies index is down 20.24%. The first quarter (Q1) of 2022 tied with Q1 2020 as the worst quarter for UK small cap in a decade, and quality growth small cap had its worst quarter since the Brexit referendum. UK small cap is now trading below its historical average price/earnings ratio.

However, quoted smaller companies in the UK have generally delivered higher returns than large companies over the long term, and over the past 67 years (to end March 2022), this has amounted to an average outperformance of 3.6% per annum. £1 invested in UK large companies in 1954 would now be worth £1,210, whereas the same £1 invested in UK smaller companies would now be worth £10,139 – almost nine times more (Source: Numis).

Notwithstanding the macroeconomic backdrop, the manager feels that it can be more productive by focusing on the fundamentals of its investee companies. MAML notes that high-quality companies with pricing power ought to be best placed to face inflationary pressures in the coming months.

Previous periods of significant underperformance from such companies have presented good buying opportunities for those with a long-term investment horizon and the team feels that the current macroenvironment will eventually prove no different.

Increased activity in ESG investing

MAML has a long track record of sustainable investing and engagement which is integral to the way the portfolio is managed.

During the last financial year, the investment team continued to develop its approach to environmental, social and governance (ESG) analysis by redeveloping its bespoke ESG checklist, incorporating further data points provided by MSCI. The analysts were able to conduct a site visit to a Cranswick facility in Suffolk to discuss progress of the company’s ‘Second Nature’ sustainability programme initiated in 2018. Pleasingly, Cranswick has announced targets for net zero, carbon neutrality, food waste, regenerative farming and waste.

Other engagements included Ideagen, with whom the team discussed carbon reduction plans and the composition of their audit committee; and Treatt, in relation to the company’s ESG footprint and its research into natural sugar substitutes.

MTU also engaged extensively with Marshalls about its carbon emission reduction plan during the year. The company has made impressive progress on that front: They are now using carbon dioxide from carbon capture projects to cure concrete bricks and have also issued a solar reflectivity index (SRI) score for all their materials. This is intended to help combat urban heating which is exacerbated by the building materials used. In addition, Marshalls has implemented a new goal to achieve net zero by 2030 in line with a 1.5 degree scenario. This has been developed in line with the new guidance from the Science Based Targets initiative.

Investment process

MAML’s purpose is to deliver strong and sustainable investment returns to investors by investing responsibly in quoted, high-quality growth smaller companies. It invests conservatively and for the long-term and does not invest in derivatives or lend the stock in its portfolios. It avoids loss-making companies, highly leveraged companies and unquoted/illiquid stocks. MAML’s staff are encouraged to invest in its funds, to better align their interests with those of the underlying investors.

The company has a strong emphasis on proprietary research, while actively avoiding that from brokers. It also encourages some theoretical research and lateral creative thought. The size of the team makes that achievable and gives MAML a competitive edge.

MAML is an entrepreneurial boutique with a flat structure that allows for quick decision-making and avoids the politics that bog down more bureaucratic large asset managers. MAML cites research from Andrew Clare produced in January 2020 which finds that European boutiques generate 0.52% p.a. of alpha on average, and a premium of 1.86% p.a. for European Small & Mid-Cap boutique managers.

Turnover and transaction costs are kept low and the team follows its companies closely over many years. The manager says he would rather pay more for a higher-quality, more predictable company that can be valued with greater certainty than a more speculative business.

MAML does not encourage the development of ‘star’ fund managers, but is focused on staff retention, including the granting of staff options over MAML equity. MAML’s ‘back office’ functions are carried out in-house rather than being outsourced (as they are in many smaller investment management boutiques).

The underlying philosophy

MAML’s core values underpin its business and its approach to investing. They are:

- “My word is my bond.”

- “Look after your clients and they will look after you.”

- “Share the same investment risks that your clients do.”

- “You cannot be good at everything – stick to what you are good at.”

- “Stay humble.”

- “Treat your team as you would your family.”

MAML invests in:

- Simple businesses that it can understand;

- Niche businesses in growth markets (non-cyclical companies, growing organically);

- Market leaders (strong, defensible market positions and pricing power);

- Companies with high operating margins and high returns on capital (barriers to entry/a sustainable competitive advantage);

- Profitable companies trading at sensible valuations;

- Good management that it trusts (aligned to shareholders and demonstrating sound ESG practices); and

- Companies that can deliver self-funded organic growth and remain focused on their core areas of expertise, rather than businesses that spend a lot of time on acquisitions.

This could be summed up as investing in high-quality businesses at sensible prices.

In addition, MAML believes that it is easier to add value through stock selection for a small and mid-cap portfolio, especially given the relative paucity of research available on these companies.

Selecting the underlying companies

An internal investment committee, chaired by Charles, reviews the portfolio every quarter, which reduces the dependence on any one individual – including Charles – for performance.

MAML follows a two-staged investment process, designed to identify stocks that are both good businesses and good investments. MTU’s portfolio is drawn from a universe of about 2,000 companies, with a focus on those with a market cap between £100m to £1.5bn. Microcap companies (<£100m) are avoided based on the liquidity risk they can pose.

The trust, by virtue of its structure, can have exposure to less liquid stocks and they have permission to hold up to 40% in AIM stocks. This is less than some of their competitors. In practice, though, it is unlikely that they would hold much more than 35%.

MAML has always generated its own investment ideas rather than relying on brokers. A team of analysts, each with their own sector expertise, continually screens the investable universe for new ideas. Research responsibilities are distributed amongst the team on a sector basis (although analysts may also compare and contrast UK companies to global peers). Emphasis is placed on being well-prepared for meetings with potential investee companies, which is possible as the research team is well-resourced. MAML’s analysts can then set the agenda, challenge management and get the information that they need. Site visits are encouraged (another perk of having a large team is that it is not desk-bound).

Both management and the board of potential investee companies are closely examined, as MAML looks to predict where a company might be in five to 10 years.

- Management’s track record is analysed to understand their goals and aspirations;

- The board structure is considered, as are the corporate governance and remuneration policies; and

- The level of insider ownership is considered.

On site visits, the team will meet employees who have not met investors before, believing that doing so allows them to gain a better insight into the products and services provided and observe the culture of the company in a way that is hard to decode from reading an annual report.

The size of the team allows for some theoretical research and lateral creative thought is encouraged. On average, each analyst will seek to identify around 20 stocks within their sector coverage worthy of closer scrutiny. These will form the pool from which portfolio constituents are drawn. The first part of the process is to eliminate poor-quality companies. These stocks are identified by applying a quantitative screen to the wider universe. Loss-making companies, those with poor cash-flow, and highly indebted businesses are rejected. Stocks that fit structural growth themes that the team has identified may be prioritised. Each company within the universe is assigned a quality rating (D to AAA).

Then the detailed work starts. The analysts build a financial model and conduct a ‘SWOT’ – strengths, opportunities, weaknesses, strengths – analysis on each stock. They also check whether a stock meets MAML’s ESG criteria. Then the idea is put before MAML’s investment committee, who challenge assumptions and ask for more information if they feel this is warranted. Stocks that pass these quality thresholds may then go on to an approved list of over 250 companies. No fund manager can buy a company that is not on the approved list.

Now, attention turns to valuation. Various valuation tools are considered (primarily discounted cash flows but also including P/E, free cash flow yields and dividend yields relative to peers) and the team operates with a time horizon of five to 10 years. The ideal investment should provide a margin of safety in excess of 25% over its intrinsic value.

Analysts will also look at risk factors. Analysts will then assign a recommendation to each stock. These will be presented to the whole team at weekly meetings and the fund managers will then decide which stocks make it into portfolios. Once a stock makes it into a portfolio, it will usually remain there for many years.

Portfolio construction

MTU’s investment policy is more fully described in its annual report. It only invests in listed or quoted securities and unquoted companies are not eligible for consideration.

Some other rules apply:

- MTU does not hedge its currency exposure;

- At the time of initial investment, a potential investee company must be profitable and no bigger than the largest constituent of the Numis Smaller Companies (ex IC index);

- For risk management purposes, the manager limits any one holding to a maximum of 4% of MTU’s investments at the time of initial investment; and

- MAML will hold no more than 10% of the voting rights in any company (across all funds managed by MAML).

Typically, the target weighting for a new position will be between 1% and 3.5%, depending on both the strength of conviction that the manager has in the stock, and its liquidity. The total number of holdings is typically around 40 to 50 (currently 44). There is no obligation to sell a company if its market cap exceeds €5bn, but these will be gradually recycled into lower market cap companies. The manager will ensure that a single position does not exceed 7.5% of the portfolio, while he also cannot increase the size of a position once its weight exceeds 4%.

The manager adds that when entering into a new position, he typically buys 50% of the target weight initially. If the investment grows to the target weight organically, it is left alone. If it declines following the investment, the manager will add to the investment to take it to its target, if it still meets the criteria.

ESG analysis

ESG analysis has been part of MAML’s investment process for well over 20 years, and sustainability is embedded within the culture of the firm. MAML has been a certified B Corporation since June 2019. Certified B Corporations are legally required to consider the impact of their decisions on their workers, customers, suppliers, community, and the environment. MAML has committed to achieving net zero emissions by 2030, offsets its business travel in conjunction with ClimateCare, supports a number of charities and promotes diversity, equality and wellness within the team.

Having become a signatory to the Net Zero Asset Managers initiative, MAML was the only UK investment boutique to be invited to join the Glasgow Financial Alliance for Net Zero (GFANZ) taskforce. It was also invited to co-chair the B Corporation Investment & Working Group and led a group of investment boutiques to the UN Climate Change Summit COP26 in Glasgow to discuss the benefits of being a B Corporation in the financial sector.

Within its portfolios, including MTU’s, MAML will not invest in tobacco companies; companies manufacturing weapons; those facilitating gambling or manufacturing alcohol; companies engaged in oil and coal-related exploration and production; companies involved with pornography; and those making high-interest-rate loans. MAML’s corporate governance checks include an assessment of a company’s remuneration policy.

MAML has an eight-member internal sustainability committee, chaired by Christian Albuisson, that meets quarterly and oversees MAML’s efforts in this area. MAML also has its own handbook, policies and checklists. It votes the shares it controls, and engages with companies. MAML expects the companies that it invests in to improve their ESG awareness and it monitors their progress.

MTU has been awarded an ‘AA’ rating – the second-best rating out of a possible seven – for its ESG credentials by MSCI. At end March 2022, MSCI had ascribed MTU’s portfolio a carbon intensity score of 40.5, which is impressively low when compared against a score of 289 for the wider benchmark.

Sell discipline

Stocks exit the portfolio for a variety of reasons – for example, when they become significantly overvalued, if they become too big, or due to takeovers.

Furthermore, stocks may leave the portfolio if the analysts identify unfavourable changes in the fundamentals of the business, or an unfavourable management change.

Stocks will also be sold if they no longer pass MAML’s quality threshold, or if a new opportunity comes along that offers better prospects.

Asset allocation

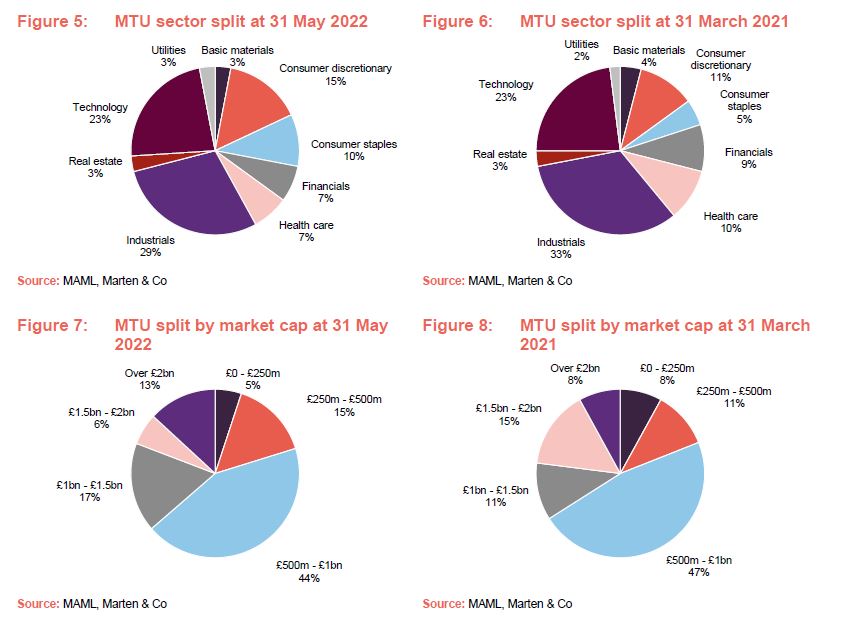

At the end of May 2022, MTU had 44 holdings, down from 53 in March 2021 (the last time we published a note), and the median market cap of the companies it was invested in was £721m. Reflecting the investment style, on average, MTU’s stocks tend to be higher-rated but faster-growing than typical UK smaller companies. Balance sheets are also strong.

Looking at consensus estimates for the next financial year, the price/earnings ratio on the portfolio was 18.5x at end May 2022, EV/EBITDA 13.6x, and average earnings per share (EPS) growth was estimated at 9.0%. Net debt/equity was forecast at -7.8%.

The sector split is driven by MAML’s stock selection decisions. There is no allocation towards energy or telecoms stocks. There has been little change to MTU’s sector allocation since our last note was published. Industrials and technology remain the portfolio’s biggest exposures, while the health care, financials and consumer discretionary weightings have been trimmed slightly. The most significant change is to MTU’s consumer staples exposure, which has doubled over the past year. Meanwhile, MTU’s market cap breakdown is broadly unchanged.

Top 10 holdings

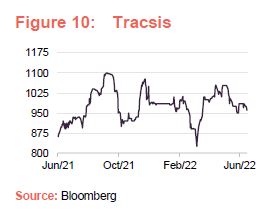

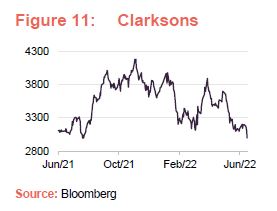

The list of MTU’s 10-largest holdings has changed a little since our last note, although portfolio turnover for the year to 31 March 2022 stood at 23.3%, lower than the previous year’s 27.8% figure, and most of these moves just reflect relative share price performance of these companies. Since 31 March 2021, XP Power, Dechra Pharmaceuticals and Liontrust Asset Management have fallen out of the top holdings, while Tracsis, Clarkson, and Big Yellow have moved up to replace them.

Tracsis

Tracsis (tracsis.com) offers technologies to manage business-critical resources, planning, asset and safety/risk management problems, across the transportation sector, but primarily to the railways and the event traffic management sectors. It has been one of MTU’s best performers, having enjoyed a strong recovery in events and announced an attractive acquisition in America of RailComm LLC.

For the six months ended 31 January 2021, its revenue rose by 31% year on year, in part reflecting a recovery from the effect of COVID on its events business. On the back of these results, the company reinstated its progressive dividend policy.

Clarksons

Clarksons (clarksons.com) is the world’s leading provider of integrated services and investment banking capabilities to the shipping markets. Recovery from the effects of COVID, port congestion, and the effects of the Ukrainian war are helping to drive up rates. For the year ended 31 December 2021, Clarkson reported record underlying profits, a 56% hike in underlying earnings per share and a 42% increase in the size of its forward order book.

At its AGM in May, the chairman said that the company was benefitting from improved conditions across many of the shipping sectors in which it operates.

Big Yellow

Big Yellow (bigyellow.co.uk) is the market leader in the UK self-storage sector. It is a constituent of the FTSE 250 and has the highest brand-awareness in the sector. The company enjoyed a 35% share price increase during MTU’s last full-year reporting period. This reflected significant occupancy growth since the first lockdown in May 2020, and increased rental growth. The position boosted MTU’s NAV by 1.2% over the 12 months to 31 March 2022.

Big Yellow’s financial year also runs to 31 March. Its latest full-year results show a 27% increase in revenue, 24% uplift in EPRA earnings per share and 40% jump in free cash flow. The results statement says that, as the economic outlook becomes more uncertain, the company will be looking to find new opportunities, helped by the strength of its capital structure and business model.

Ideagen

Ideagen (investors.ideagen.com) targets the global audit, risk and compliance software market. It has been growing well; organic revenue growth was running at 13% per annum as at the end of January 2022. In April 2022, Cinven said that it was considering making an offer for the company. It decided against it in May, but both Hg and Astorg said that they were interested in acquiring the business. Later that month, Ideagen said it would recommend a bid from a vehicle controlled by Hg.

We think that the bid is illustrative of the value within MTU’s portfolio. Private equity funds are cash-rich and more approaches may be forthcoming.

Performance

MTU’s outperformance of the Numis Smaller Companies Index accelerated in the spring of 2020, as investors became more unnerved about the likely effects of COVID and sought safety in the high-quality and growth stocks that are the focus of MTU’s portfolio. However, the good news on vaccines in 2020 triggered a sharp rotation into value stocks. Against that backdrop, MTU lagged the benchmark index. This has continued going into 2022, as growth stocks have sold off further on the back of rampant inflation and rising interest rates, as discussed in the market overview section of this note.

Charles described the year to 31 March 2022 (the period which MTU’s last released annual report covered) as a year of two halves. Between 31 March and 30 September 2021, the trust saw strong outperformance of 9%, but this was fully reversed due to the war in Ukraine and the rotation away from quality growth companies in the first calendar quarter of 2022.

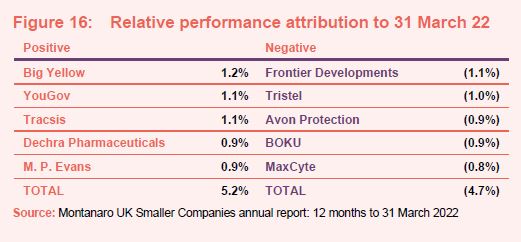

Attribution

There were a number of standout performers as well as key detractors over the 12 months to 31 March 2022. The top and bottom five performers are listed in the table below and more information about some of them is detailed in the following pages.

Positive contributors

Tracsis and Big Yellow were discussed in the asset allocation section above.

YouGov

YouGov (www.yougov.co.uk) is an international on-line market research and data analytics company which conducts and produces surveys. It is headquartered in the UK, but has operations in Europe, North America, the Middle East and Asia Pacific. The company confirmed strong growth well ahead of expectations over MTU’s last financial year, leading to a 37% gain in the share price. However, since then the share price has fallen back to a new one-year low.

The company’s half-year figures, covering the six months ended 31 January 2022 were robust, with underlying revenue up 25% and adjusted underlying EPS up 11%. The company is currently targeting annualised EPS growth of 30% per annum.

Negative contributors

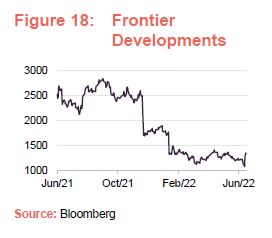

Frontier Developments

Cambridge-based Frontier Developments (www.frontier.co.uk) is a developer of software games using Cobra, a proprietary cross-platform technology. It publishes a number of its own game franchises such as Elite Dangerous, Planet Coaster, Jurassic World and Planet Zoo. The manager says that the company suffered from delays and disappointing reviews of new releases (chiefly Elite Dangerous: Odyssey), margins fell and the shares more than halved.

The manager says it continues to have confidence in the founder of the business, David Braben, (who has a 32% stake in the company) and his belief in the potential for recent release F1 Manager 2022 and upcoming releases for Warhammer.

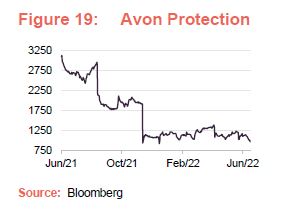

Avon Protection

Avon Protection (www.avon-protection-plc.com) is one of the world’s largest producers of military grade helmets. As we reported in our last note, the company announced at the end of 2020 that there were problems with the approval process for certain US defence contracts, and a protest had been lodged against its US Army Next Generation Integrated Head Protection System sole source contract.

The manager says that the company went on to have a torrid year after a failure in bullet-proof body armour led to it closing that part of its business and it experienced delays in orders and supply chain issues. The holding has now been sold.

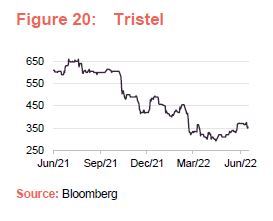

Tristel

Tristel (www.tristel.com) is an infection prevention business. It supplies disinfectant products based on chlorine dioxide to healthcare providers in medical, pharmaceutical, veterinary and laboratory settings. Its medical device disinfectants product range is branded Tristel and its surface disinfectants product range is branded Cache.

The company says that COVID-19 impacted on its sale growth. It announced the write-down of discontinued parts of the business (lower-margin animal health and pharma/life sciences products) and delays in the Food and Drug Administration (FDA) approval of their products in the United States, which led to the share price halving over MTU’s last annual reporting period. Following a site visit in November 2021, the manager continues to have high hopes for the company.

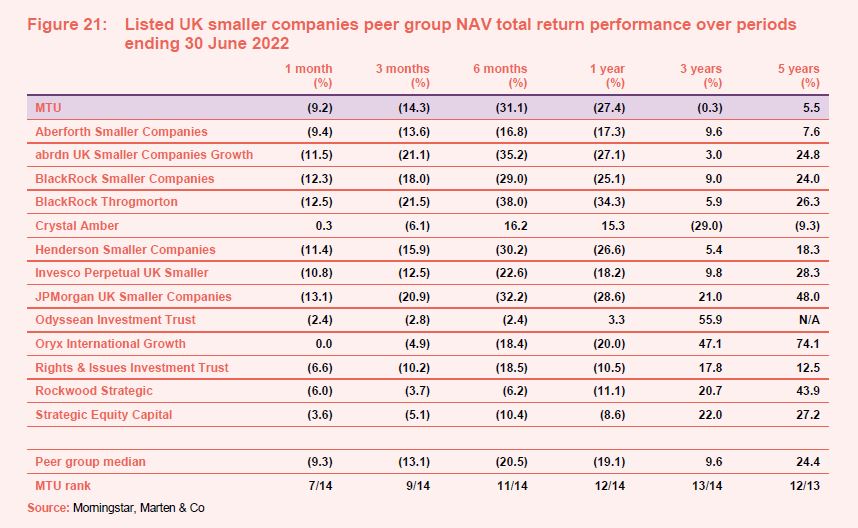

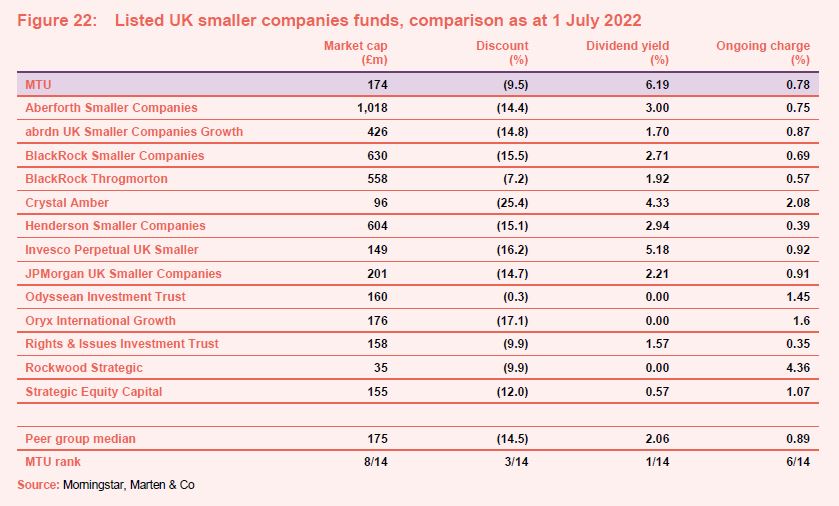

Peer group comparison

The peer group that we have used in this note is a subset of funds within the AIC’s UK smaller companies sector. We have omitted split-capital companies, trusts with a small market capitalisation, and those with an exclusive focus on micro-cap companies.

MTU’s portfolio held up well in the falling markets when the pandemic first hit in 2020, which can be seen in its three-year numbers in Figure 21. However, the impact of the attitude towards growth stocks since the start of 2022 has hit more recent figures.

The sharp deterioration of MTU’s relative returns since the vaccine announcements of early November 2020 has pushed it towards the bottom-end of the peer group performance tables over most short/medium-term time periods. If Charles is right, and quality starts to come back into favour, MTU could move swiftly back up the rankings.

Comparing MTU on other measures as shown in Figure 22, it is a reasonable size – about middle of the pack for this peer group. Meanwhile, MTU’s supportive shareholder base has helped keep its discount under control. Although it remains wider than in recent history, it is not as wide as the majority of its peers. This perhaps suggests that investors agree with Charles that the relative underperformance will prove temporary.

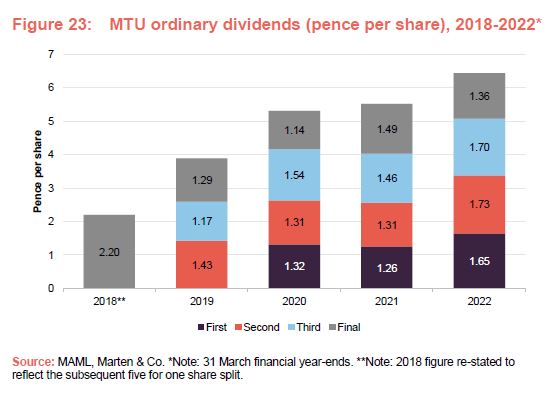

MTU’s dividend, which we discuss overleaf, is another source of comfort for investors. It currently has the highest yield in the peer group at 6.2% and the dividend continues to grow.

Lastly, we would highlight MTU’s ongoing charges ratio, which is towards the lower end of those in the peer group, especially given its size. MTU’s ongoing charges ratio is comparable to – and in some cases smaller than – those of much bigger funds in the peer group.

Dividend

In accordance with a policy introduced in July 2018, MTU pays out 1% of its NAV each quarter as a dividend – a level it considers to be meaningful for investors. Dividends are paid each quarter equivalent to 1% of the company’s NAV on the last business day of the preceding financial quarter, being the end of March, June, September and December.

The enhanced dividend policy has had no impact on the way in which the fund is managed or the yield on the underlying portfolio. To the extent that MTU’s revenues are insufficient to cover the dividend the balance is met from reserves. MTU’s primary objective is to generate capital growth with the income generation of the underlying portfolio considered to be a by-product of the stock selection process.

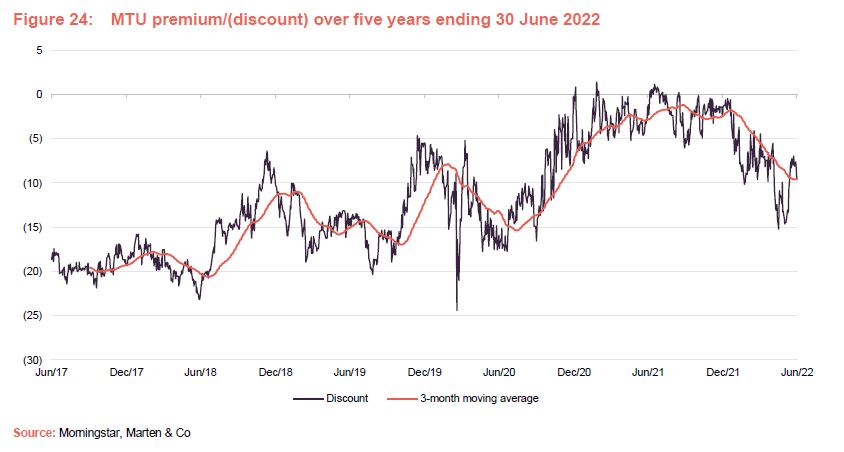

Premium/(discount)

Over the year ended 30 June 2022, MTU’s shares traded in a range from a discount of 15.2% to a premium of 1.1% with an average of a 4.7% discount (and a median discount of 3.8%).

Over the five-year period shown in Figure 24, MTU shares traded between a 24.4% discount and a 1.4% premium. The average discount was 11.6% while the median discount was 13%. At 1 July 2022, MTU’s shares were trading at a discount of 9.5%.

The company has worked hard to make MTU more attractive to private clients, including a five-for-one share split in 2018, the enhanced dividend policy, reducing costs and an increased focus on marketing. These initiatives continue to bear fruit as more and more retail investors join the share register. The board and the manager hope that, over time, this will reduce discount volatility in the shares.

Fees and costs

As MTU’s investment manager, MAML is entitled to receive a management fee of 0.50% of the trust’s gross assets. There is no performance fee. The AIFMD receives an annual fee of £50,000.

For accounting purposes, the management fee is allocated 75:25 between capital and revenue account split. The same allocation is applied to interest accrued on MTU’s borrowings.

MAML may terminate the management agreement on giving 12 months’ notice in writing. The trust may terminate the agreement by notice in writing forthwith or at a specified date. In the event that the trust is the party terminating, the manager will be entitled to a termination fee of 1% of the gross assets of MTU at the end of business on the last day of the calendar month immediately preceding the effective date of termination of the contract.

The company’s ongoing charges ratio for the year ended 31 March 2022 was 0.78% down from 0.82% for the prior year.

Capital structure and life

MTU has 167,379,790 ordinary shares in issue and no other classes of share capital. The shares were subdivided in July 2018 on a five-for-one basis. The objective of this exercise was to increase the liquidity of the shares and make it easier to make relatively small investments into the trust (making it better suited to monthly savings plans and the like).

At the AGM held on 12 August 2021, over 99% of shareholders voted in favour of the continuation of MTU for a further five years. The next continuation vote is scheduled to be held in 2027.

MTU’s financial year ends on 31 March. It tends to announce annual results in June and hold its AGMs in July, with this year’s due to be held on 27 July 2022.

Gearing

The AIFM, in consultation with the board, is responsible for determining the net gearing level of the company and approves the arrangement of any gearing facility.

On 17 December 2021, the borrowing facilities with ING Bank were renewed for a period of three years. The interest rate on the £20m fixed rate term loan was reduced by approximately 0.2% per year, which represents a saving for shareholders. Similarly, the £10m revolving credit facility (RCF) was renewed with a lower commitment fee.

At 30 June 2022, MTU was not geared.

Major shareholders

Board

MTU is managed with a tight board of just four non-executive directors, all of whom are independent of the manager and do not sit together on other boards. Arthur Copple, the chairman, was elevated to that position in July 2019 following the retirement of Roger Cuming. The trust believes a smaller board to be appropriate for its size, allowing it to keep costs down – ongoing charges have been falling.

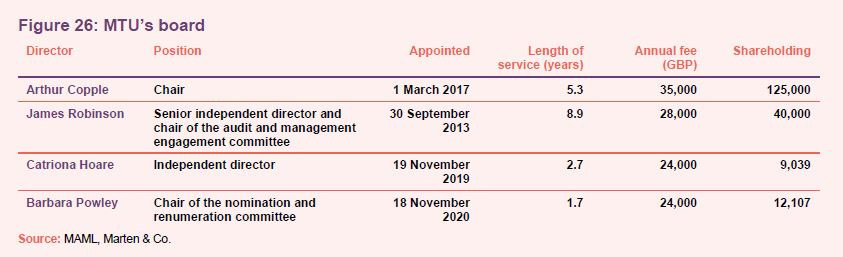

Arthur Copple (chair)

Arthur has specialised in the investment company sector for over 30 years. He was a partner at Kitcat & Aitken, an executive director of Smith New Court Plc, and a managing director of Merrill Lynch. Arthur is also non-executive chairman of Temple Bar Investment Trust Plc and vice-chair of the University of Brighton Academies Trust.

James Robinson (senior independent director and chair of the audit and management engagement committee)

James was chief investment officer (investment trusts) and director of hedge funds at Henderson Global Investors prior to his retirement in 2005. A chartered accountant, he has over 35 years’ investment experience and is a director of JP Morgan Elect Plc. James is also chairman of Polar Capital Global Healthcare Trust Plc, a governor of Lord Wandsworth College and a former chairman of the investment committee of the British Heart Foundation.

Catriona Hoare (independent director)

Catriona’s experience includes having been an investment partner at Veritas Investment Management in London since 2013. Before joining Veritas, Catriona held the position of fund manager at Newton Investment Management.

Barbara Powley (chair of the nomination and renumeration committee)

Barbara was appointed to the board as an independent director in November 2020 before being made chair of the nomination and renumeration committee in April 2021. She has more than 30 years of experience in the investment trust industry, combined with a strong corporate governance and accountancy background.

Previous publications

Readers interested in further information about MTU may wish to read our previous notes listed below.

| Title | Note type | Date |

| Reputation restored | Initiation | 5 March 2020 |

| Long COVID effect requires a focus on corporate health | Update | 16 April 2021 |

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note Montanaro UK Smaller Companies Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.