June 2024

Winners and losers in May 2024

| Best performing funds in price terms | (%) |

|---|---|

| Capital & Regional | 22.0 |

| Safestore | 16.4 |

| Big Yellow Group | 15.6 |

| Derwent London | 13.2 |

| British Land | 12.8 |

| Helical | 9.8 |

| Phoenix Spree Deutschland | 9.2 |

| Shaftesbury Capital | 8.2 |

| Workspace | 7.5 |

| SEGRO | 7.5 |

| Worst performing funds in price terms | (%) |

|---|---|

| Life Science REIT | (15.4) |

| Residential Secure Income | (8.4) |

| Triple Point Social Housing REIT | (6.3) |

| Alpha Real Trust | (6.1) |

| Tritax EuroBox | (3.1) |

| Schroder REIT | (2.9) |

| NewRiver REIT | (2.8) |

| PRS REIT | (2.8) |

| Custodian Property Income REIT | (2.7) |

| Grainger | (2.5) |

Best performing funds

A more positive tone on market sentiment and continued corporate activity helped boost the real estate sector in May, with the mean average share price across the peer group up 2.4% and the median average up 1.4%. One such company on the receiving end of merger and acquisition (M&A) attention was small-cap shopping centre landlord Capital & Regional. Its share price bounced 22.0% after revealing that it had received interest from two parties including NewRiver REIT (see page 3). April’s news that self-storage specialist Lok’n Store had received a bid (see last month’s round up) may have been behind the share price uplift of the two other listed self-storage companies – Safestore and Big Yellow Group. London office developers Derwent London and Helical both rallied in May, although the latter gave up a considerable gains when it reported a sizable drop in NAV in annual results. In contrast,

British Land reported limited valuation falls in a decent set of annual results and was rewarded with a double-digit share price uplift. Meanwhile, the publication of a more favourable rent index for Berlin was a much-needed tonic for residential landlord Phoenix Spree Deutschland.

Worst performing funds

Share price pressure on Life Science REIT continued with another double-digit monthly drop. The company shares are now down 47.2% in the year-to-date, reaching an all-time low in its short existence of 33.4p at the end of May. Another company whose share price has come under unrelenting pressure is Residential Secure Income. It is down 22.4% in 2024 and is in need of a positive catalyst for a turnaround in fortunes. Triple Point Social Housing REIT was down despite reporting a marginal uplift in NAV for the first quarter (see page 2 for details). European logistics landlord Tritax EuroBox fell back 3.1% in May, but jumped in early June when it was announced that private equity giant Brookfield was mulling an offer for the company. As mentioned earlier, NewRiver REIT revealed it was considering making an offer for fellow retail landlord Capital & Regional. As is often the case in potential mergers, the target company’s share price rises and the bidding company’s falls with arbitrage strategies at play. Still reeling from its own merger activity, or lack thereof, Custodian Property Income REIT’s share price was down again in May, and it has now lost 17.6% in value this year.

Valuation moves

| Company | Sector | NAV move (%) | Period | Comments |

|---|---|---|---|---|

| Target Healthcare REIT | Healthcare | 2.2 | Quarter to 31 Mar 24 | Portfolio value uplift of 1.4% on like-for-like basis to £934.8m |

| Impact Healthcare REIT | Healthcare | 1.7 | Quarter to 31 Mar 24 | 1.5% like-for-like increase in portfolio valuation to £660.8m |

| Triple Point Social Housing REIT | Residential | 0.3 | Quarter to 31 Mar 24 | Marginal increase in portfolio value due to inflation-linked rental uplifts |

| AEW UK REIT | Diversified | (0.8) | Quarter to 31 Mar 24 | Reported a 0.4% like-for-like portfolio valuation increase to £210.7m |

| Alternative Income REIT | Diversified | (1.2) | Quarter to 31 Mar 24 | Value of portfolio fell 0.7% to £102.6m |

| abrdn European Logistics Income | Europe | (1.7) | Quarter to 31 Mar 24 | Portfolio value declined 1.6% on a like-for-like basis to €606.29m |

| abrdn Property Income Trust | Diversified | (2.3) | Quarter to 31 Mar 24 | Like-for-like fall in the value of the portfolio of 0.9% to £420.6m |

| Balanced Commercial Property Trust | Diversified | (2.3) | Quarter to 31 Mar 24 | Portfolio fell 1.6% in value to £957.0m |

| Grainger | Residential | (3.6) | Half-year to 31 Mar 24 | Portfolio value fell 1.9% to £3,674m, mainly due to removal of multiple dwellings tax relief |

| Tritax EuroBox | Europe | (5.9) | Half-year to 31 Mar 24 | Like-for-like portfolio valuation decline of 2.9% to €1,464.8m |

| Picton Property | Diversified | (4.0) | Full year to 31 Mar 24 | Portfolio valuation reduced 2.8% to £745m |

| British Land | Diversified | (4.4) | Full year to 31 Mar 24 | Portfolio valuation fell 2.6% in the year to £8,684m |

| Assura | Healthcare | (8.0) | Full year to 31 Mar 24 | Portfolio value drop of 1.1% to £2,708m |

| Land Securities | Diversified | (8.2) | Full year to 31 Mar 24 | Value of portfolio down 6.0% in the year to £9,963m |

| Great Portland Estates | Offices | (17.6) | Full year to 31 Mar 24 | Portfolio valuation of £2.3bn, down 12.1% on a like-for-like basis |

| Helical | Offices | (32.9) | Full year to 31 Mar 24 | 22.4% valuation decrease, on a like-for-like basis, to £660.6m |

Corporate activity in May

Special Opportunities REIT – a new internally-managed REIT seeking to capitalise on the recent dislocation in UK real estate capital markets – is targeting a fundraise of £500m via an initial public offering (IPO). If successful, the shares would be admitted to trading on the standard segment of the London Stock Exchange’s main market. Commitments have been received from three cornerstone investors, GoldenTree Asset Management, TR Property Investment Trust and other Columbia Threadneedle investments funds, and the Bhavnani family office, to subscribe for between 104m and 119m shares (£104m to £119m) in total.

NewRiver REIT announced it was weighing up a bid for listed shopping centre landlord Capital & Regional. NewRiver REIT approached Capital & Regional’s majority shareholder Growthpoint Properties (which owns 68.13% of the company) regarding a possible offer in cash and shares. No formal proposal has been made at this stage. NewRiver REIT said that it believed that a combination would substantially accelerate its growth ambitions, whilst delivering significant value for both sets of shareholders and also maintaining its core operational expertise in retail real estate. Capital & Regional had also received an indicative proposal from Vukile Property Fund (a retail-focused REIT operating in South Africa and Spain) regarding a possible offer for the company, but Vukile has since pulled out.

London office developer Great Portland Estates launched a fully underwritten 3-for-5 rights issue to raise £350m (£336m net of expenses) through the issue of 152m new shares at a price of 230 pence. The issue price represents a 44.5% discount to its share price and a 33.4% discount to the theoretical ex-rights price. The company said the rights issue would allow it to take advantage of “attractive new acquisition and development opportunities emerging in central London” and deliver attractive and accretive shareholder returns. The company has a near-term acquisition pipeline worth £1.4bn within central London, and an additional watchlist worth another £1.4bn.

abrdn European Logistics Income announced that it will undergo a managed wind down. Ahead of a continuation vote this year, the board launched the strategic review into the future of the company in November 2023, with the fund suffering from a wide discount to NAV and a materially uncovered dividend. The company received 11 indicative proposals and a smaller number of offers, while the company’s investment manager provided a proposal involving a managed disposal of the portfolio over a period of 12-24 months, with capital being returned to shareholders. The board concluded that it would be in the best interests of shareholders to put forward a proposal for a managed wind down of the company, with the potential value from the managed wind down materially in excess of the net value achievable from the indicative cash offers received. As part of the proposed managed wind down, it is expected that the majority of assets will be disposed of by the end of the second quarter of 2025. The board recommends that shareholders vote against the continuation vote resolution at the forthcoming Annual General Meeting (AGM) on 24 June 2024.

The merger of Tritax Big Box REIT and UK Commercial Property REIT became effective on 16 May after shareholders voted overwhelmingly in favour of the merger.

abrdn Property Income shareholders approved the managed wind down of the company.

May’s major news stories – from our website

- LondonMetric swaps unwanted LXi retail assets for urban warehouses

LondonMetric sold seven properties for £31.3m (including £18.3m of non-core LXi REIT assets at a 5% premium to book values), reflecting a net initial yield of 7.0% and a 3% profit over book values. Separately, it acquired six reversionary urban warehouse assets for £45.0m, reflecting a net initial yield of 6.1%.

- Assura enters £250m JV to invest in NHS infrastructure

Assura Group entered a £250m joint venture with Universities Superannuation Scheme (USS) to invest in NHS infrastructure. The JV (which is split 80:20 in favour of USS) will be seeded with an initial portfolio of seven assets (£107m) transferred from Assura’s existing portfolio at a small discount to the March 2024 valuation. The £85m net cash proceeds received by Assura will be recycled into its pipeline of acquisition and development opportunities.

- British Land sells Meadowhall stake for £360m

British Land exchanged contracts to sell its 50% stake in the Meadowhall Shopping Centre to its joint venture partner Norges Bank Investment Management for £360m. The sales price was 3% above the September 2023 book value.

- Land Securities checks out of £400m hotel portfolio

Land Securities completed the sale of its entire hotel portfolio to real estate funds managed by Ares Management for £400m. This compares to a September 2023 book value of the assets of £404m.

- Unite sells £184m student digs portfolio

Unite Students sold six properties to PGIM Real Estate for £184m, as it continues to focus on student accommodation close to highly ranked universities. The properties, comprising 2,948 beds, are located in Birmingham, Cardiff, Leicester, Liverpool, Nottingham and Sheffield and have an average age of 18 years.

- Helical enters JV on 100 New Bridge Street development

Helical entered into a joint venture arrangement for the redevelopment of 100 New Bridge Street, London, selling a 50% interest for £55m on a preferred equity basis to a vehicle led by Orion Capital Managers. Simultaneous to the joint venture being signed, the parties entered into a development financing arrangement with NatWest and an institutional lender.

- Tritax EuroBox announces lettings success in Belgium

Tritax EuroBox agreed a lease re-gear, a new lease and associated solar PV Power Purchase Agreement (PPA) at Logistics Park Bornem, Belgium. The re-gear and new lease are both eight-year, inflation-linked leases and have been signed, together with the PPA, with the existing global pharmaceutical and medtech tenant.

- Tritax EuroBox sells Gothenburg warehouse bringing disposal programme to €173m

Tritax EuroBox exchanged contracts to sell its warehouse asset in Gothenburg, Sweden for SEK 385m (€34m) to a pan-European real estate investment manager. The sale price is broadly in line with book value and is part of the company’s disposal programme aimed at reducing leverage. Since launching the disposal programme in May 2023, the company has sold four properties for €173m.

- Impact Healthcare REIT brings in new tenant at struggling care homes

Impact Healthcare REIT completed the transfer of three care homes located in Bradford to a new tenant, We Care Group on long-term leases. The homes had been operated by Silverline Group, which went bust last year.

- Home REIT sells off more properties at auction room

Home REIT sold a further 76 properties at a public auction for a total of £14.6m (12.4% below the draft August 2023 valuation – which was already heavily marked down from the price the company bought them for).

Visit https://www.QuotedData.com for more on these and other stories plus analysis, comparison tools and basic information, key documents and regulatory announcements on every real estate company quoted in London

Managers views

A collation of recent insights on real estate sectors taken from the comments made by chairmen and investment managers of real estate companies – have a read and make your own minds up. Please remember that nothing in this note is designed to encourage you to buy or sell any of the companies mentioned.

Diversified

Land Securities – Mark Allan, chief executive:

For much of the decade leading up to 2022, creating value in real estate was often about leveraging up a spread between rental yields and ultra-low borrowing costs or picking high-level sector themes. The significant rise in cost of capital across the globe has not only changed the former but also the latter, as shown by the challenges faced by low-margin online retail models and the shift back to physical retail. As such, irrespective of sector, quality has become a much more important driver of future performance, which means it can be misleading to look at market averages. Indeed, even though market-wide vacancy is elevated, with London offices at 8.8%, retail at 12% and even logistics at 7.8% now, the best assets in each of these sectors have little vacancy and so continue to show good rental growth.

This provides a critical underpin for capital values. The outlook for interest rates is more balanced now than it has been for a couple of years, but we remain of the view that it is unlikely that rates will come down sharply from current levels. In what will therefore likely remain a higher nominal rate environment, we think yields for assets which have inherent income growth and therefore provide a real income stream look attractive, yet for most assets which lack this growth, we think the risk to values remains down.

British Land – Simon Carter, chief executive:

In the past 12 months macroeconomic and geopolitical uncertainty has remained high. However, inflation has declined, and markets are now anticipating interest rate cuts. Consequently, yield expansion in the portfolio slowed significantly in the second half and strong rental growth meant values were broadly flat.

Our base case is that we will be operating in a more supportive economic environment over the next 12 months than we have seen in the last two years. With inflation lower, the next move in the base rate is likely to be down rather than up and although UK GDP growth is expected to be modest at best, most forecasts are for it to be positive. Unemployment is expected to remain low which should be supportive of demand for best-in-class workspace at our campuses as businesses continue to focus on attracting and retaining talent in a competitive jobs market. The return of real wage growth should provide valuable breathing space for consumers, supporting our retail parks business.

Picton Property – Michael Morris, chief executive:

During the year there has been lacklustre transactional activity, due to the increased cost of debt and falling capital values. MSCI recorded £40.1bn of investment transactions for the year to March 2024, which is 27% down on the £55.4bn recorded for the year to March 2023 and 51% lower than the £82.1bn transacted in the year to March 2022. Transactions in the industrial sector had the highest weighting, comprising 24% of the total.

With interest rates anticipated to reduce from the second half of 2024 and increased liquidity in the lending market, it is expected that trading activity will begin to pick up as we head towards the end of the year.

The UK economy appears to be improving, with inflation falling and the Bank of England widely anticipated to commence base rate cuts in the second half of 2024. This expected reduction in interest rates should continue the positive momentum in terms of improving business, investor and consumer confidence, as the cost of debt and cost of living pressures continue to ease.

Despite increases in long-term UK Government bond yields over the year, paralleled by similar rises in property yields, there are signs of stabilisation emerging. The short to medium-term economic outlook offers signs of cautious optimism. Downside risks remain, particularly in relation to geopolitical instability in the Middle East and eastern Europe, which could potentially fuel inflationary pressures. The timing of and scale of the Bank of England’s interest rate cuts are highly dependent on the trajectory of inflation and strength of the labour market in the coming months.

Healthcare

Assura – Jonathan Murphy, chief executive:

The UK is facing a healthcare crisis, and the nation’s ageing population combined with unrelenting hospital waiting lists continues to drive significant demand for investment in healthcare infrastructure.

This demand for investment in improved and more diverse health facilities has received cross-party political support, with countless reports highlighting the need to move services out of hospital and tackle health inequalities within communities in a cost-effective way. 2024 is set to be an election year and the NHS will undoubtedly be a key election topic, already having been granted considerable air time by all the major political parties in recent months. Whichever party is in Government post-election, our expectation is that there will continue be a desire to demonstrate improvements in health services during the next parliamentary term. Investment in community healthcare is an obvious way to achieve this – easing pressure on the NHS, benefiting patients, focusing on prevention rather than treatment, and ultimately making the health system more efficient over the long-term.

The primary care market remains a challenging environment in which to achieve external growth, with delays in agreeing the rents required for new build developments to be commercially viable. The underlying demand for new buildings remains high, so we are confident that this position will unlock in due course, and pockets of opportunity have started to emerge in some regions.

Offices

Great Portland Estates – Toby Courtauld, chief executive:

Whilst macro-economic volatility persists, our confidence and belief in London remains. Unrivalled as one of the world’s most attractive and diverse mixed-use locations, London is a true global city. Central London is busy and office workers have returned, with hybrid working now the norm. 74% of our portfolio is in the West End and 93% located close to Elizabeth line stations. Looking forward, we anticipate supportive rental conditions for the best spaces and are optimistic for further rental growth.

With customers increasingly demanding the very best, sustainable spaces, they are competing in a market increasingly starved of new, Grade A supply, putting further upward pressure on prime rents.

Despite a weak macro-economic backdrop, we anticipate that current occupational trends will continue. We expect that the demand for the best spaces will outstrip supply and the trend for smaller spaces to be provided on a flexible basis to increasingly become the norm. Buildings that are unable to meet this evolving demand, particularly in the face of competition from elevated secondary supply, will underperform. The gap between the best and the rest is likely to widen further.

Europe

Tritax EuroBox – Phil Redding, chief executive:

Market sentiment has continued to be influenced by macro-economic factors, with the continuation of restrictive monetary conditions and uncertainty on the timing of interest rate cuts, leading many investors to adopt a “wait-and-see” approach. This environment has led to valuations across some of our markets to drift lower during the period. However, with inflation in Continental Europe on a downward trajectory and expectations that interest rates will also turn lower, this should provide a more supportive backdrop for our markets over the remainder of the year.

While investment volumes have remained subdued, more recently we have seen evidence of activity picking up, particularly from those investors with high conviction on the sector’s long-term structural drivers and strong market fundamentals. The reported up-tick in investment volumes during the period reflects this trend and is also an encouraging sign that activity should gain momentum through the year and into 2025. However, stability and valuation improvement will likely remain dependent on the extent and timing of Central Bank actions in the near term.

Occupier markets in Continental Europe have also not been immune to the more challenging economic outlook, with take-up declining, albeit off the back of three very strong years through the pandemic. Demand remains broad-based but some occupiers are becoming more cautious, and decision-making is taking longer.

The significant decline in development pipelines towards the end of last year has mitigated to a degree this fall in demand, with average vacancy levels only increasing moderately in most markets. Increases in country averages also mask a divergence between core markets, that remain very tight, and peripheral markets, where speculative development is taking longer to lease up. Overall, occupier market fundamentals remain robust and continue to support positive rental growth.

Real estate research notes

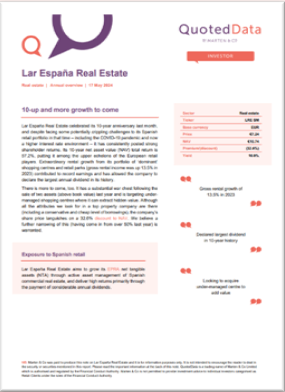

An annual overview note on Lar España Real Estate (LRE SM). Impressive rental growth allowed the company to declared the largest dividend in its 10-year history.

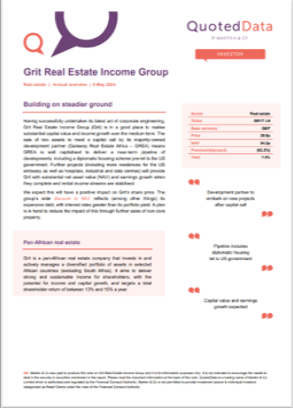

An annual overview note on Grit Real Estate Income Group (GR1T). Its latest act of corporate engineering has opened the door for new NAV and earnings accretive developments.

An update note on Tritax EuroBox (EBOX), which is sailing in calmer waters as demonstrated by a portfolio valuation that has changed little and a 30% uplift in earnings that now fully covers its 8.6%-yielding dividend.

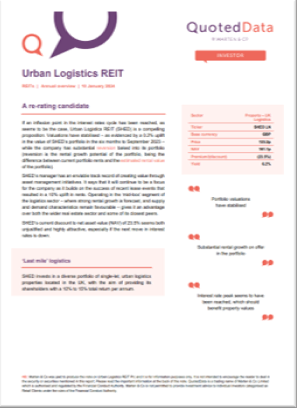

An annual overview note on Urban Logistics REIT (SHED). The company appears to be a re-rating candidate as values stabilise and management extracts the rental reversion in the portfolio.

IMPORTANT INFORMATION

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.