Just getting started

RWC Partners took on responsibility for Temple Bar Investment Trust (TMPL) on 1 November 2020, and its appointment has coincided with a remarkable improvement in the fortunes of this UK equity income trust. Dramatic outperformance, a narrowing of the discount and a buzz around the resurgence of value-style investing mean that RWC has got off to a great start.

However, the managers think that this is just the beginning of TMPL’s turnaround. They note that value-style investing often outperforms for an extended period following a shock to markets such as the one inflicted by COVID-19. Although the news is better, the easing of lockdowns has only just begun. The considerable economic stimulus being injected by governments offers the prospect of a synchronised global economic recovery. TMPL could be set fair.

UK equity income and capital growth

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities, with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

Fund profile

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

For 18 years, TMPL was managed by Alastair Mundy, who was head of the Value Team at Ninety One UK. He stepped down as manager in April 2020. On 23 September 2020, the board announced that it had selected RWC Partners as TMPL’s new investment manager. RWC took on responsibility for the portfolio with effect from 1 November 2020.

RWC Partners

TMPL’s AIFM is RWC Partners. RWC was established in 2000 and employs around 155 people, including 57 investment professionals. RWC manages around $18bn of assets for clients across a range of strategies, from offices in London, Miami and Singapore.

Within RWC Partners, responsibility for managing TMPL’s portfolio rests with Nick Purves and Ian Lance (the managers). Nick and Ian each have over 30 years’ experience and have worked together for 13 years. The two co-manage over £3bn of assets across a number of income funds.

Nick Purves joined RWC in August 2010 from Schroders where he was a senior portfolio manager with responsibility for both Institutional Specialist Value Funds and the Schroder Income Fund and Income Maximiser Fund, together with Ian Lance. He worked at Schroders for 16 years, having moved from KMPG where he qualified as a chartered accountant.

Ian has 30 years of experience in fund management and started working with Nick at Schroders in 2007 before joining RWC in August 2010. While at Schroders, he was a senior portfolio manager managing the Institutional Specialist Value Funds, the Schroder Income Fund and Income Maximiser Fund, together with Nick. Previously, Ian was the head of European equities and director of research at Citigroup Asset Management and head of global research at Gartmore.

Manager’s views

When we published our initiation note last September, whilst the managers were optimistic about the future of the trust, market sentiment was still very much in favour of growth stocks and against the manager’s value approach.

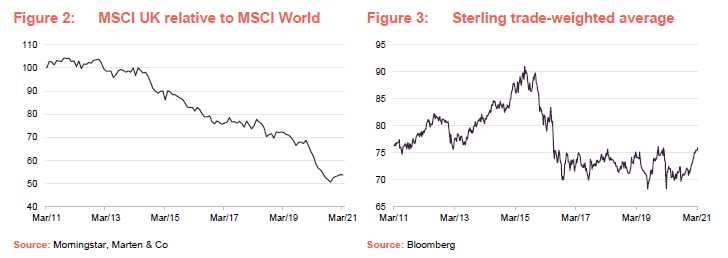

The reorganisation of TMPL’s portfolio had been completed by the end of the first week in November, just after RWC’s formal appointment. The timing could hardly have been more perfect for RWC. Just a few days later, good news began to roll in about the efficacy of a number of COVID-19 vaccines. The effect was to trigger what felt like a dramatic rotation from growth to value. However, as Figure 1 shows, there is much ground for the value style to make up just to get back to its relative position ahead of the global financial crisis. RWC feels that the rotation in markets could be only just getting started. The managers note that there is still considerable dispersion in valuations and we have not yet reached a point where a significant proportion of investors are switching exposure towards value stocks.

Likewise, although the UK stock market has had a better few months, relative to other leading markets, it is still well behind where it was ahead of the decision to hold the Brexit referendum in 2016. The same is true of sterling.

The prospect of a synchronised global economic recovery over 2021 appears increasingly likely. Earnings revisions will look all the more impressive for coming off last year’s lows. Value sectors should see the strongest upward earnings revisions.

The managers’ experience with other funds that they manage is that it can take a while for markets to reset themselves after a shock such as the bursting of the tech or financial bubbles. Value tends to outperform for some time after these events. They feel that the pattern will repeat for COVID-19. The managers suggest that, as the value rally continues, not participating in it will become increasingly painful and this should help extend the rally.

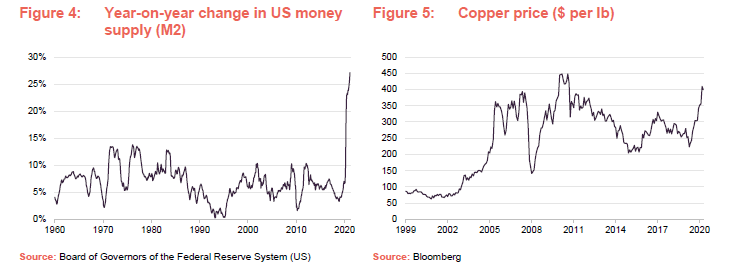

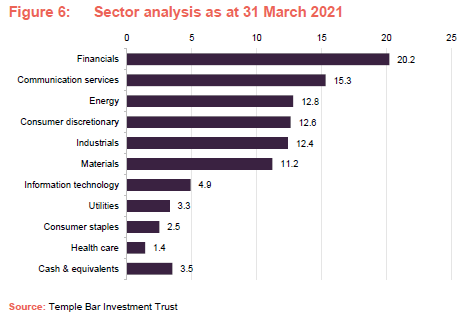

Further impetus could be provided by reflation/inflation. In areas such as employment the immediate outlook is deflationary, but as the recovery gathers pace, various bottlenecks in the economy could force prices higher. The managers note that US money supply figures (see Figure 4) are supportive of inflation. In addition, oil prices are recovering, as are many other commodity prices such as copper (see Figure 5). At the same time, central banks will likely want to keep short-term interest rates down for fear of choking off the post-COVID economic recovery.

Reflective, perhaps, of rising inflation expectations, yield curves have been steepening (in other words, the gap between long-term interest rates and short-term interest rates has been widening). This has been supportive of the financial sector and banks in particular, where higher interest rates should result in higher margins.

Banks also seem to have come through 2020 without seeing a big spike in defaults. If anything, it looks as though loan loss provisions have been too pessimistic. When this is coupled with restrictions on dividends and other forms of capital distribution, many banks’ balance sheets now look over-capitalised. This raises the prospect of strong dividend growth in future.

By contrast, the managers note that many so-called defensive stocks actually look quite expensive (defensive stocks are those whose performance is relatively independent of the performance of the economy and therefore tend to do better in a downturn). They cite the example of the drinks company Diageo, which is often perceived as defensive and a place to hide in periods of economic uncertainty. However, the managers stress that it is hard to argue that the stock is good value on a price/earnings ratio of 25x. Anaemic revenue and profit growth (around 2% per annum), vulnerability to competition from craft drinks and start-ups, and stronger sterling reduce the attraction of the stock in RWC’s eyes.

Asset allocation

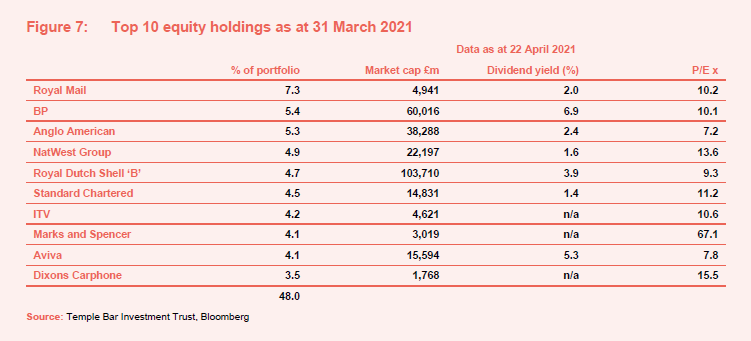

TMPL’s portfolio is weighted towards energy, materials and financials and has very little exposure to so-called ‘defensive’ sectors. That is a stance that has not changed much for RWC’s funds over the past year.

The figure for cash and equivalents may include some exposure to gilts. The figure at the end of February was high in advance of the repayment of TMPL’s £38m 5.5% debenture stock on 8 March 2021 but by the end of March was down to 3.5%.

10-largest equity positions

The list of the 10-largest equity positions as at the end of March is fairly close to the list of the 10-largest holdings provided in Figure 5 of our initiation note using data from six months earlier for a similar fund managed by the team. While the ranking of stocks may have changed and some positions may have been added to on weakness or trimmed on profit-taking, RWC’s UK’s equity income portfolios have been fairly stable.

Looking at a few of these:

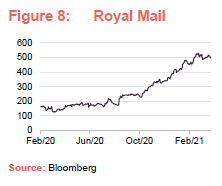

Royal Mail

18 months ago, there was perhaps a perception that Royal Mail was a poor-quality stock in a declining industry. However, the RWC team is enthused about the prospect for the company’s parcel business, which includes GLS, its European parcel delivery division, which handles around 6m parcels per day. What was largely a business-to-business (B2B) operation saw sharp growth in its business-to-consumer (B2C) business as home deliveries boomed. The company responded by expanding its sorting capacity by more than 50%. The business’s sensitivity to this is such that much of its sales growth fell through to bottom line as profit. Royal Mail thinks GLS’s profits could more than double over the next four-to-five years.

Royal Mail’s share price more than doubled over the course of 2020, but the managers feel that the stock was very oversold previously and is still attractively valued.

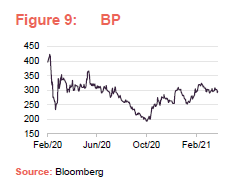

BP & Shell

The oil majors were hit last year by a slump in the oil price and growing adverse sentiment towards fossil fuels. The managers believe that the penny has dropped for the oil industry and, for the most part, it is now working towards 2050 net zero emissions targets. The European majors have been setting robust emissions targets and have begun to reposition their businesses for a carbon neutral future. Both operating expenditure and capital expenditure have been cut. They are working around an equilibrium oil price of $50 – $60 per barrel.

The managers say that BP is generating about 50 cents per share or 35p of cash flow and is trading on a 12% free cash flow yield. They think demand will decline more slowly than share prices suggest. TMPL also holds Total and Shell, which have similar stories.

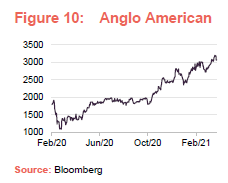

Miners

In terms of mining stocks, TMPL has positions in Anglo American (copper, iron ore and diamonds) and two gold miners – Newmont and Barrick. A combination of supply-side constraints (after years of cutting back on capital expenditure), a resurgent global economy and an increased emphasis on infrastructure investment has created a supportive environment for commodities prices. The industry’s capital discipline is much improved, management having learned from the commodities price falls of 2012.

The managers also feel that the ingredients are in place for a higher gold price. We discussed the possibility of higher inflation on page 6. There is also the chance of increased demand for jewellery as consumer confidence returns.

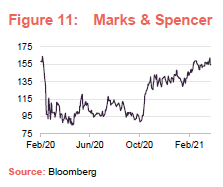

Retail

The arguments against high street retail have been well-rehearsed. COVID lockdown measures accelerated the pace of the shift to online sales. This was true of Marks and Spencer, for example, where the managers reckon three-to-four years’ change happened in a few months. The managers highlight that M&S’s profits are increasingly derived from its food division. The acquisition of a 50% stake in home food delivery business Ocado was announced in February 2019. M&S replaced Waitrose as the supplier of groceries to Ocado with effect from 1 September 2020.

Other holdings in the sector include Dixons Carphone and Kingfisher. Kingfisher is beneficiary of an uptick in DIY projects during the pandemic, and Dixons did reasonably well as people kitted out home offices.

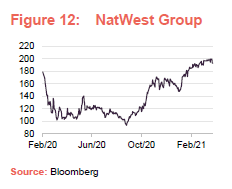

Banks

In the banking sector, TMPL holds NatWest and Standard Chartered in the top 10 as well as Barclays and Citigroup. The managers note that even though these stocks have been rising (for the reasons outlined on page 6), they still do not look expensive. NatWest is on 0.63x book value and Barclays on 0.60x book value, according to Bloomberg, for example.

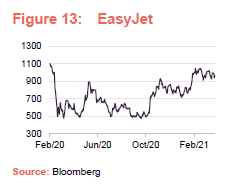

EasyJet

EasyJet was a holding that RWC opted to retain when the managers took on the portfolio, and it has done well since, but lies just outside the list of 10-largest holdings. The company is highly operationally geared and clearly hard-hit by COVID-related travel restrictions. The managers acknowledge that the stock is facing an uncertain future. They feel that the re-rating that has occurred since November may be premature. It is not clear to the team when the company could get back to 2019 levels of profitability. Some of the decline in corporate travel may prove permanent, but if foreign leisure travel recovers, the stock should do well.

Performance

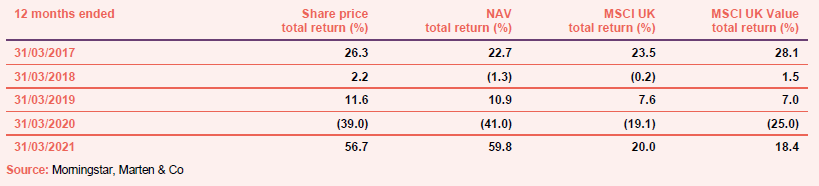

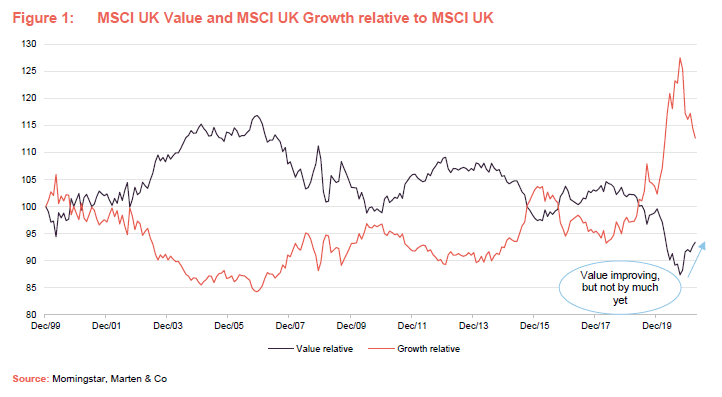

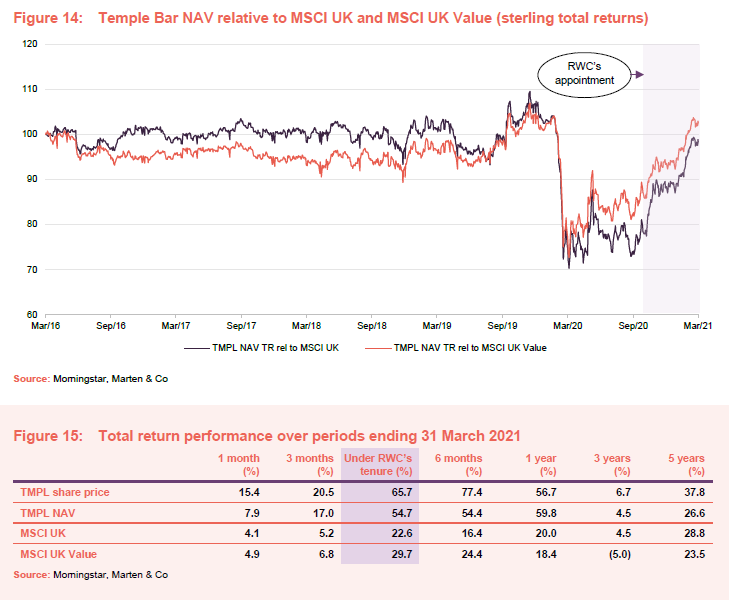

To some extent, RWC’s appointment with effect from 1 November 2020 renders an analysis of TMPL’s performance prior to that date redundant. However, for completeness, we have included our standard five-year chart in this note. Our initiation note contained some data on the performance of RWC prior to its appointment (see Figure 1 of that note).

TMPL was hit hard when investors’ concerns about the likely effects of COVID-19 were reaching their fever pitch last spring. A rush to growth and quality and away from value was one factor, but the trust even underperformed the MSCI UK Value Index. Nevertheless, as confidence began to recover, things improved for the trust. The portfolio was repositioned over October and the beginning of November 2020 ahead of the good news on vaccines in November. This was the catalyst for a sharp rotation into value stocks, to TMPL’s benefit. The momentum appears to have been sustained into 2021 and TMPL has now made up almost all of the ground it lost in March 2020.

The managers note that there have been some very big share price moves within the portfolio. Royal Mail, which we discussed on page 8, was a notable contributor to TMPL’s returns, for example.

Royal Sun Alliance was taken over – Canadian group Intact and Denmark’s Tryg made a joint bid at 685p per share, a 49% premium to the share price ahead of the offer. Intact took control of the group’s UK and Canadian business and Tryg took the Swedish and Norwegian operations.

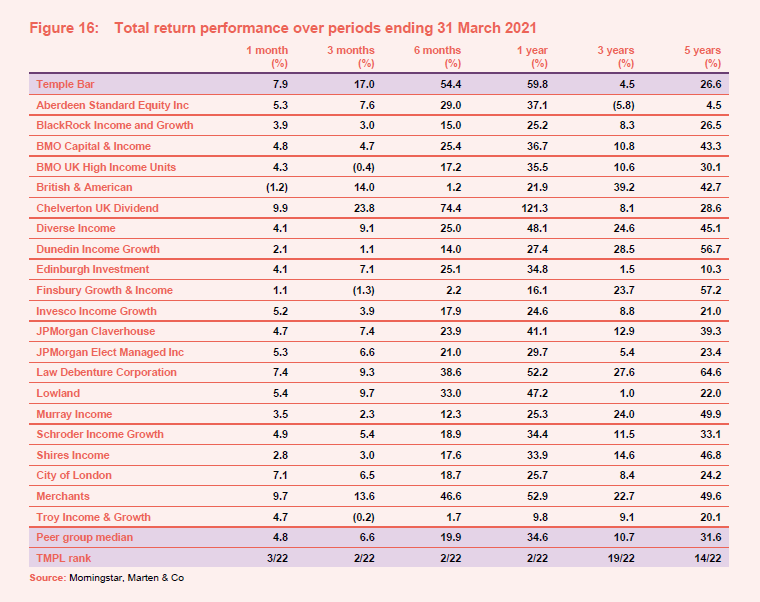

Peer group

We have compared TMPL to the constituents of the AIC’s UK equity income sector. The two funds that vie with TMPL for best-performing fund in recent times are both quite highly geared; in Chelverton UK Dividend’s case by a zero dividend preference share and in Merchants Trust’s case with debt. By contrast, TMPL is not much geared (TMPL’s borrowings were around 7% of its net assets at the end of March 2021), suggesting that returns from its underlying portfolio have been sector-leading over the past year.

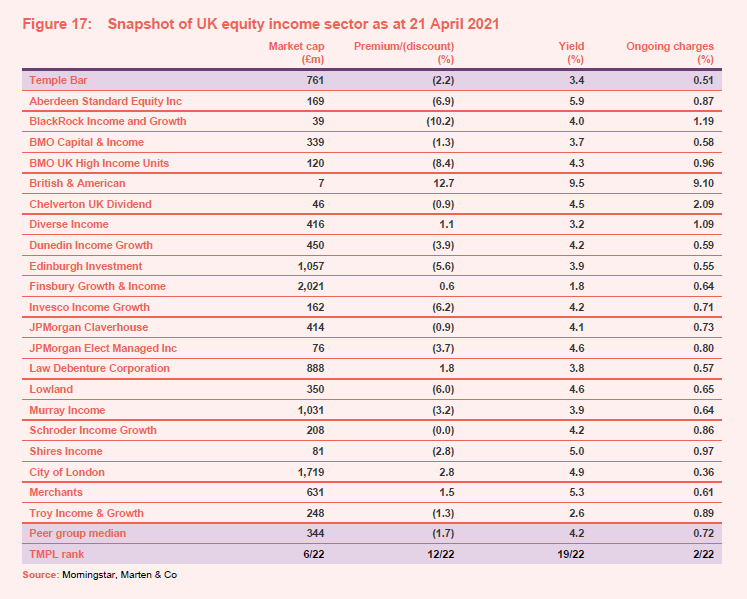

TMPL is a decent size (over the twice the sector median), sufficient in March 2021 for it to re-enter the FTSE250 Index, and this is a factor in its extremely competitive ongoing charges ratio, which is one of the lowest in the sector. While TMPL’s shares are trading close to asset value, the sector contains a number of investment companies that are trading at a premium. As confidence builds in the new manager, it might be reasonable to expect that TMPL does the same.

One factor that might hold it back a little, however, is its dividend yield, which is now towards the lower end of the peer group ranking. Strong total returns will likely override that, however, as has been the case with both Troy Income & Growth and Finsbury Growth & Income.

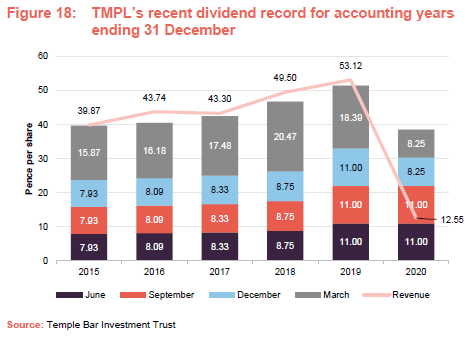

Dividend

The effect of COVID-19-related dividend cuts, omissions and postponements, and to a lesser extent a rebalancing of the portfolio following the appointment of the new manager, was to reduce TMPL’s net revenue per share for 2020 to 12.55p, from 53.12p for 2019.

As we discussed in our initiation note, the board and RWC felt that TMPL’s dividend needed to be reset to a more sustainable level. Accordingly, the December and March dividends were set at 8.25p, bringing total dividends for 2020 to 38.5p.

The intention is that this is a base from which the dividend can grow in future years. The managers say that TMPL’s revenue for this year is looking better. They felt that it makes sense to sacrifice some income in the current environment to try to achieve higher total returns. This is an approach that the team used in the wake of 2008’s financial crisis, and the managers say that it worked out well.

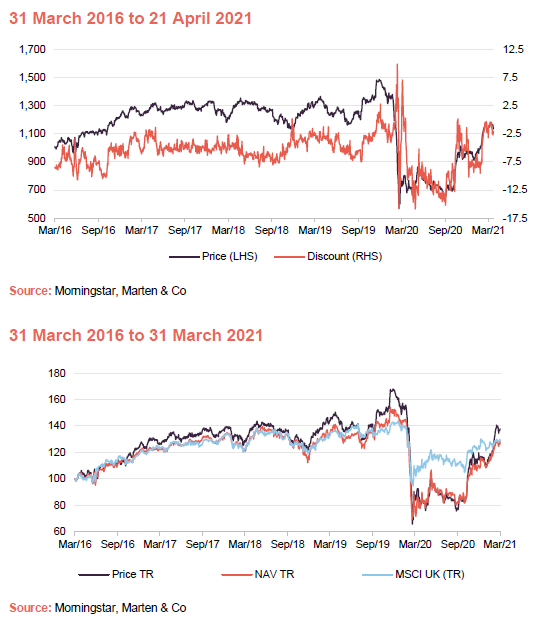

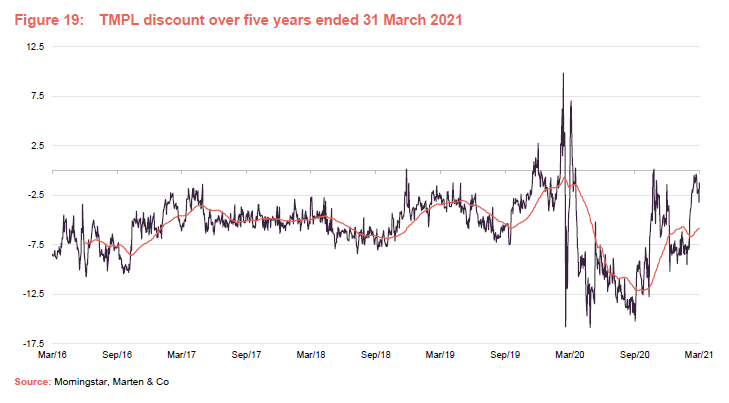

Discount

TMPL’s discount has been more volatile in recent quarters, reflecting the turmoil in markets. It narrowed in the wake of November’s vaccine announcements, briefly trading at a premium, and the general trend now seems to be positive.

Over the year ended 31 March 2021, TMPL traded between a 15.9% discount and a 7.1% premium, hitting those extremes in the volatility of last Spring. The average discount over that period was 8.2%. At 21 April 2021, TMPL was trading at a discount of 2.2%.

Previous publications

Our initiation note – Keeping faith – was published on 23 September 2020. Readers can access the note by clicking the link or visiting our website, QuotedData.com.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Temple Bar Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.