Further portfolio diversification

In recent weeks, JLEN Environmental Assets Group (JLEN) has further diversified its portfolio with three new investments, a battery storage project and two investments in the low carbon and sustainable solutions portion of its portfolio; a controlled environment aquaculture facility in Norway; and a UK glasshouse construction project drawing low-carbon heat and power from an existing anaerobic digestion plant owned by JLEN.

In an environment of volatile energy prices and uncertainty over the shape of future electricity market reforms, investors may be reassured by the breadth of JLEN’s portfolio and the managers’ ability to find new ways of adding value. JLEN’s NAV gains this year have been amongst the best in its sector. There are some factors that might support a higher NAV, but share prices are now falling, perhaps because investors are concerned about the prospect of higher discount rates.

Progressive dividend from investment in environmental infrastructure assets

JLEN aims to provide its shareholders with a sustainable, progressive dividend, paid quarterly, and to preserve the capital value of its portfolio. It invests in a diversified portfolio of environmental infrastructure projects generating predictable, wholly or partially index-linked cash flows. Investment in environmental infrastructure projects is supported by a global commitment to support low-carbon electricity targets.

Many NAV drivers appear supportive

Power prices

Our last note on JLEN was published on 29 March 2022, shortly after the outbreak of the war in Ukraine. Since then, UK power prices have soared past previous highs, which is generally accepted to be driven largely by record natural gas prices.

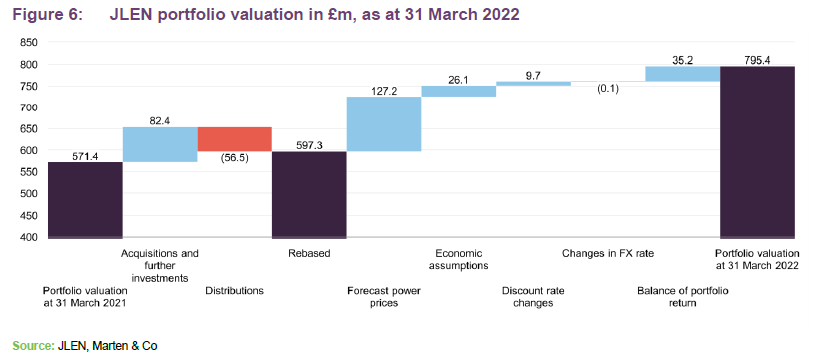

JLEN has fixed prices for the majority of its output. At 31 March 2022, the portfolio had price fixes secured over 77% for the Summer 2022 and 74% for Winter 2022 seasons. In the statement that accompanied the publication of its end-June NAV, JLEN said that new price fixes achieved since 31 March 2022 had contributed 1.2p to its NAV uplift over the quarter. In addition, uplifts in seasonal forward pricing added 1.5p, and revisions to long-term energy price forecasts provided by independent third-party consultants added a further 5.8p.

Since the end of June 2022, based on the data in Figure 1, average power prices have been about 39% higher than the level at 30 June 2022.

Inflation

JLEN benefits from underlying portfolio revenues being linked to inflation. At 31 March 2022, JLEN said that 62% of lifetime revenues were contractually inflation-linked.

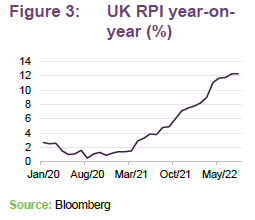

At the end of March 2022, JLEN was assuming 5% RPI inflation for 2022 as a whole, falling to 3% until 2030, and then 2.25% thereafter. This assumption will be revisited when the interim report covering the six months to end September 2022 is published. The figure for this year may be increased, which would feed through into a higher NAV, everything else being equal.

JLEN’s 31 March 2022 accounts said that, for illustrative purposes, were inflation to be higher than JLEN’s valuation assumption by 3% for the next three years, its NAV would be expected to increase by 7.5 pence per share.

Corporation tax

The new UK administration has reversed the planned increase in corporation tax from 19% to 25% that would have taken effect in April 2023. JLEN and its peers had already factored the corporation tax increase into their NAV calculations. In its

31 March 2022 accounts, JLEN said that an increase in the UK corporation tax rates of 2% would result in a downward movement in the portfolio valuation of £11.5m (1.7p per share) compared to an uplift in value of £11.7m (1.8p) if these rates were reduced by the same amount. This suggests that JLEN’s NAV might rise by 5.4p to reflect the tax U-turn.

Intervention in the UK wholesale market under consideration

In the short term, the EU Commission plans to raise about €140bn by the imposition of a windfall tax on power sold at prices over €180MWh. Just 4% of JLEN’s portfolio was based in Europe at 31 March 2022, with the balance of 96% in the UK.

While the UK government has proposed to support UK consumers with an energy price guarantee, which should mean that a typical household will pay no more than £2,500 per year for their energy, it is still weighing up whether to make an intervention in the wholesale electricity market to capture some of the high profits being earned by electricity generators currently.

The collection of green levies within UK power prices will be suspended. However, the ROCs and FiTs that these fund will continue to be paid by the government. In this regard, JLEN’s income will be unaffected.

A number of bodies, including the UK Energy Research Centre and Energy UK, have suggested that the government encourage renewable energy generators to shift existing ROC/FiT-based contracts onto a CfD basis. Previous chancellor Nadhim Zahawi expressed a similar opinion. The big question would be: At what price? The suggestion is that prices would have to reflect the higher build-costs associated with older projects and so they would be set at a premium to the AR4 clearing prices. The net effect for a generator such as JLEN could be that, in the short term, it might not be able to capture the peak of spot prices for energy, but, over the longer term, it might be able to guarantee higher-than-budgeted, inflation-linked prices for the energy it produces.

Energy market reform

The UK government’s Review of Electricity Market Arrangements (REMA) launched on 18 July 2022 and is at the consultation stage until 10 October 2022. It is a far-ranging review intended to deliver an appropriate framework for all non-retail electricity markets to deliver security of supply, cost effectiveness, and decarbonisation. Within this, there is a clear desire to see consumer prices for power produced by renewable generators better reflect the cost of producing that power.

Since 2014, the UK government has sought to support the development of new renewable energy projects through a mechanism of contracts for difference (CfDs). Generators bid for a guaranteed price for the power that they produce.

Earlier this year, in auction round four (AR4), contracts were agreed to support the development of 900MW of onshore wind, 2.2GW of solar and 7GW of offshore wind, plus lesser amounts of other types of generation. These contracts cleared at:

- £42.47MWh for the onshore wind;

- £45.99MWh for the solar; and

- £37.35MWh for the offshore wind.

These are 2012 prices, equivalent to £55.64MWh, £60.25MWh and £48.93MWh in today’s prices, respectively. Successful bidders receive the guaranteed price, adjusted for inflation based on CPI, for 15 years from the date that production commences. Income from power sales below these prices is topped up to the guaranteed level by the government-owned Low Carbon Contracts Company (LCCC), and income from power sales above this level is handed over to the LCCC.

Discount rates – a potential negative

In its annual report covering the 12 months ended 31 March 2022, JLEN noted a risk that discount rates used to calculate the NAV increase in a high inflation environment, impacting valuations. However, it also noted that recent market transactions had supported the view that attractive infrastructure assets remain in high demand with institutional investors.

An independent verification exercise of the methodology and assumptions applied by Foresight in the NAV calculation is performed by a leading accountancy firm and an opinion provided to the directors on a semi-annual basis.

The increase in yields on long-dated UK government bonds that has occurred in recent months and has accelerated since the announcement of the mini budget on 23 September 2022, may have an impact on the discount rates used to value JLEN’s assets as at the end of September 2022. However, other factors will be taken into account, including levels of risk premium applied to projects.

The overall weighted average discount rate of the portfolio was 7.3% at 31 March 2022 (31 March 2021: 7.3%).

Asset allocation

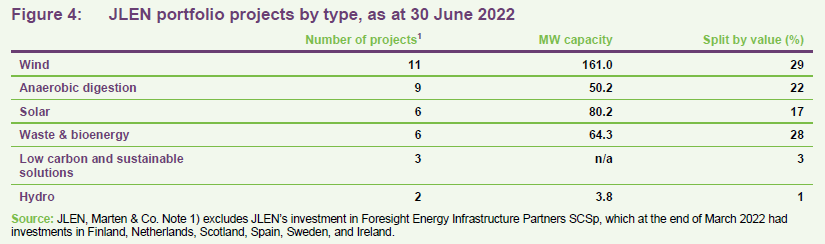

Figure 4 displays JLEN’s portfolio by project type, as at 30 June 2022. In aggregate, at that date there were 37 projects spread across the wind, AD, solar, waste & wastewater, hydro, and low carbon & energy efficiency technologies. It does not take into account the new investments that JLEN has made since 30 June 2022 that we discuss overleaf.

Between 31 December 2021 (the data used in our last note) and 30 June 2022, the company sold two French windfarms (as covered in our last note).

New investments – introducing controlled environments

As JLEN’s managers continue to seek out new opportunities for the trust, it has made two investments in the growing area of controlled environments.

Aquaculture plant in Norway

JLEN is making an equity investment in a farmed trout business in Rjukan in Norway. JLEN is investing alongside other Foresight funds, as well as the developer and operator of the facility, Hima Seafood AS. JLEN’s total investment is expected to be up to about £40m over the next three to four years.

In contrast to sea or loch-based fish farming, this is a land-based aquaculture facility, which allows for a controlled environment. That means that not only can the plant control variables such as water quality (eliminating microplastics) and temperature, there is a much-reduced chance of infection by parasites and diseases. That in turn means healthier fish and lower mortality, with much less need for antibiotics and other chemicals. Fish are raised in 16 independent pens so that, if one does experience an issue, there is much less chance of this affecting the whole facility. In addition, waste can be minimised and could even be used for fertiliser.

The 23,400sqm plant, which will use established recirculating aquaculture system (RAS) technology, is expected to begin operating in 2024 with full operations expected in 2025, following which the facility is forecasted to produce approximately 8,000 tonnes of trout annually, equivalent to 10% of Norway’s total production.

RAS is a closed-loop process. Water is cleaned, reoxygenated, and recycled, to reduce the demand for freshwater. The plant can raise four batches per year.

The trout will be branded as Hima trout, marketed as a premium product, and sold via an offtake agreement with an established Norwegian seafood distribution company with global reach, Villa Seafood.

Industry background

Aquaculture is the farming of aquatic species such as salmon and trout, shrimp, mussels or seaweed. A growing global population and an expanding middle class is increasing global demand for quality protein (expected to double by 2050). Fish and seafood provides a high proportion of that protein.

The global fish and seafood market grew between 4% – 8% annually in the ten-year period to 2019. Fish, including salmonids such as salmon and trout, is considered one of the most efficient sources of high-quality animal protein due to the rate at which it converts feed into edible mass, its high protein retention and high rate of edible meat per kilogram, as well as various nutritional benefits.

In response, and as wild catches have stagnated or declined, farmed fish and seafood has increased in importance. However, the industry has a poor reputation, particularly for fish welfare, the escape of farmed varieties into the wild and the pollution that farms create. This is inefficient too; the annual cost of the damage caused by sea lice to the sea-based aquaculture industry is estimated to be €1.5bn.

Norway has a well-developed aquaculture industry, ranking seventh globally by weight and second highest by value after China. It is a leading producer of Atlantic salmon and ranks third in the production of rainbow trout. Its main market for salmon is the EU, but exports of rainbow trout are global. Experts consulted ahead of JLEN’s commitment to the project believe that oversupply is not a concern as buyers of salmon can be relatively easily converted to trout. The target market for the plant is intended to be the EU, East Asia and North America, and the end-market is growing.

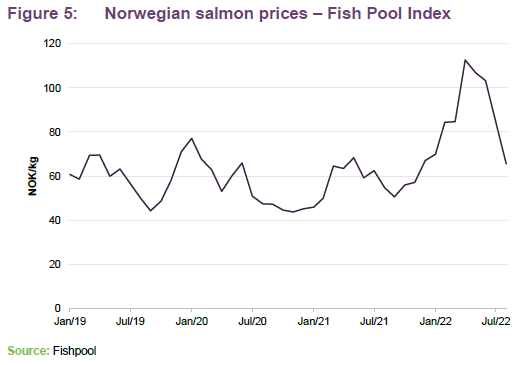

Interestingly, prices for salmon and trout tend to move in tandem. Figure 5 shows an index of salmon prices compiled by Fish Pool.

Land-based aquaculture is not new, but is growing fast. PwC’s 2021 Seafood Survey says that as of January 2021, there were at least 86 global projects, with a total capacity of around 1.7m tonnes, in land-based fish farms under planning or construction. 31 of these (661,000 tonnes) were based in Norway. In 2019, Norway produced about 1,440,000 tonnes of salmon from all sources.

Sustainability

The project maps onto nine of the 17 UN Sustainable Development Goals and aligns well with the EU Taxonomy classification system (despite it not currently including activities specifically related to aquaculture). It has been evaluated using Foresight’s proprietary Sustainability Evaluation Tool.

The project will be powered by electricity from the Norwegian grid that is about 99% from renewable sources. While considerable quantities of fresh water are required, these are abundant in the plant location and up to 99.9% of water used can be recycled. The impact of waste from the plant will be monitored carefully. Sustainability of feed products is an important consideration and Hima’s feed supplier is focused on increasing the proportion of raw materials coming from certified sustainable sources.

UK glasshouse project

JLEN is investing up to £26.7m into an advanced glasshouse. The 2.1-hectare glasshouse, which has already received planning permission, will be built adjacent to an existing anaerobic digestion (AD) plant already owned by JLEN. The AD plant will be upgraded to supply low carbon heat (sourced as waste heat from the existing CHP engines and delivered by pipe and a heat exchanger) and power to the glasshouse via a private wire.

For the glasshouse, the energy comes at a discount to the import market price. For the AD plant, the electricity it sells will fetch a higher price than it would if the power was exported to the grid. The AD plant continues to benefit from the inflation-linked RHI regime, while also utilising surplus heat.

JLEN’s interest in the project will be structured as a combination of a senior secured loan for the construction of the glasshouse and a convertible loan and a minority equity stake in the glasshouse operator to provide for working capital.

The glasshouse is expected to commence production in 2023. It will be capable of growing a wide array of different horticultural products, from consumable produce to cut flowers. However, its initial operator will focus on the lawful cultivation of the heavily regulated tetrahydrocannabinol (THC) flower, conforming to tightly monitored licence requirements for secure supply to established UK-based pharmaceutical manufacturers.

In addition, wastage from the glasshouse produce may also be returned to the digester, creating a circular ecosystem.

The manager continues to explore private wire opportunities across the rest of the portfolio.

New battery project

On 1 August 2022, JLEN announced a £14.1m investment in its third grid-scale battery project. It is buying a 50% stake in Clayfords Energy Storage Limited, which has the right to build a 50MW lithium-ion battery storage plant in Buchan, Aberdeenshire. The deal was done alongside JLEN’s sister fund, Foresight Solar Fund Limited.

The revenue strategy will likely prioritise the capacity market or arbitraging intraday fluctuations in power prices, for example, and is capable of adapting as market opportunities change. All necessary permissions have been secured for the project and it is expected to start commercial operations in the final quarter of 2024.

Performance

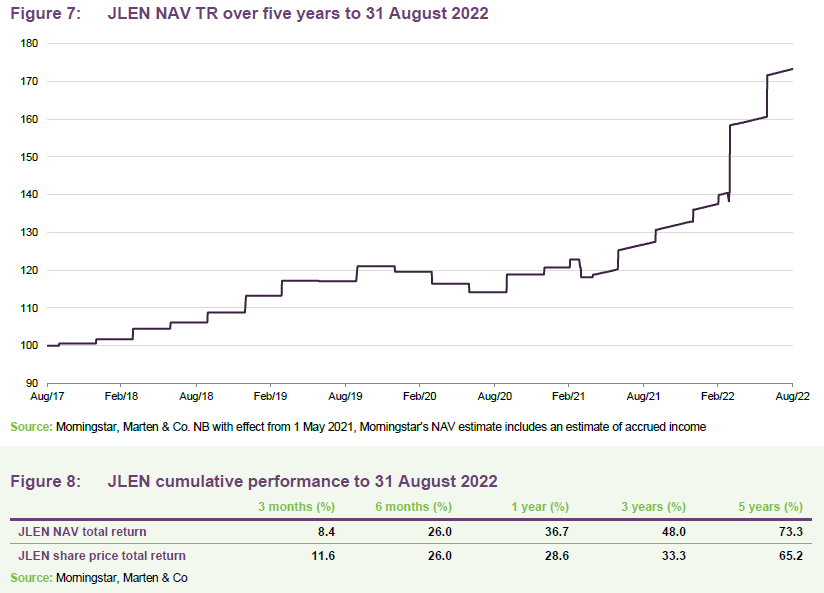

Since we last published, JLEN has announced results for the 12-month period ended 31 March 2022 and updated the market with an unaudited NAV figure as at 30 June 2022.

31 March full-year results

The end March NAV figure was £762.9m or 115.3p per share, well ahead of the unaudited 100.7p estimate as at 31 December 2022 used in our last note. A full-year dividend of 6.8p, up from 6.76p for the prior year, was covered 1.10x. The target for the current financial year was announced as 7.14p.

30 June update

On 4 August 2022, JLEN announced that its unaudited NAV as at 30 June 2022 was £814.3m or 123.p per share. This figure was 7.8p higher than the end March 2022 NAV.

The statement said that the increase was due to a combination of:

- price fix arrangements secured above previous valuation assumptions (+1.2p);

- uplifts in seasonal forward pricing (+1.5p); and

- revisions to long-term forecasts provided by independent third-party consultants (+5.8p).

Financial performance

Peer group comparison

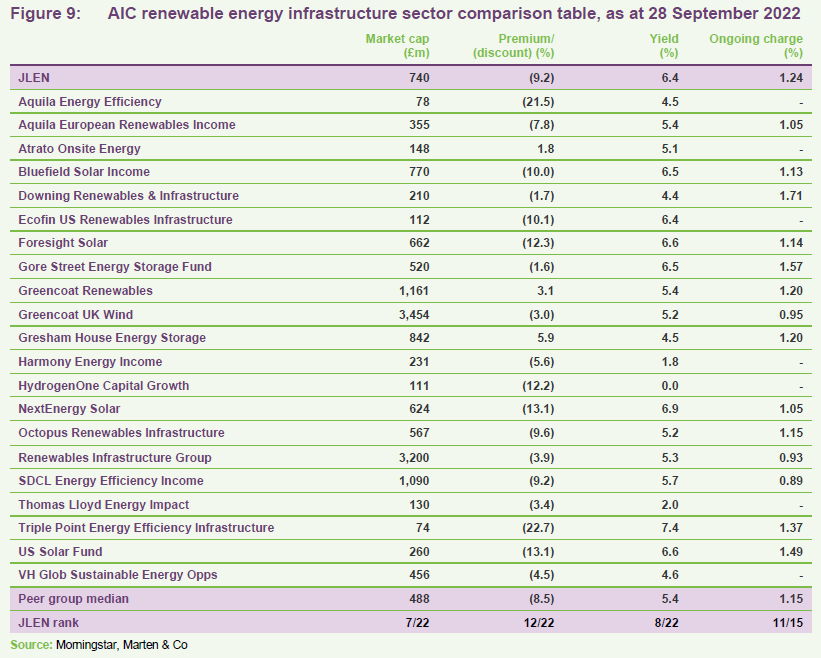

JLEN has one of the broadest remits of the 22 companies that comprise the members of the AIC’s renewable energy sector. Most of these funds are focused on solar or wind or some combination of the two. Three of these funds are focused solely on energy storage.

There is an increasing variation of geographic exposure within the peer group too, with a number of funds that are heavily exposed to the North American market (which has a different risk/reward structure) and one focused on Asia.

JLEN’s diverse portfolio, which includes many asset types not found in competing funds, makes it unique within the sector. The sector continues to attract fresh equity capital from investors, although the pace of that has eased somewhat and no new funds have been added to the sector in recent months. Following JLEN’s oversubscribed issue earlier this year, it now ranks seventh by market cap.

In recent days, the share prices of most funds in the sector have dropped sharply. It may be that investors fear that discount rates are going to rise and that the negative impact of that on NAVs will overwhelm the many other positive developments underway within the sector.

JLEN’s ongoing charges ratio and yield appears competitive in absolute terms compared to similarly sized funds, especially when taking into account the extra diversification provided by its wider remit.

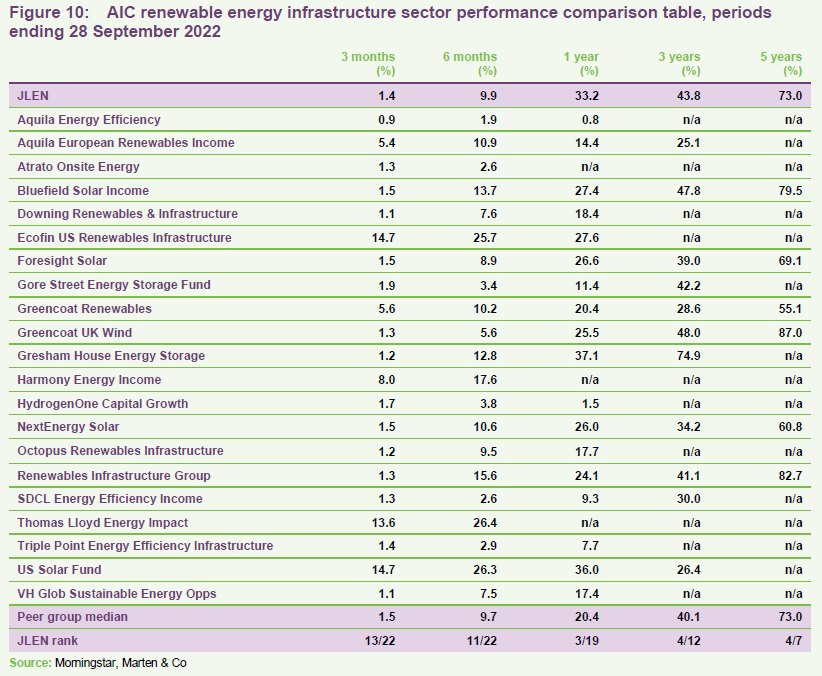

Figure 10 compares the performance of the funds. JLEN is one of only seven funds that were in existence five years ago. Its NAV gains this year have pushed it towards the top of the peer group over 1 and 3-year periods ending 28 September 2022.

Variations in performance across the peer group tend to reflect differences in asset composition. Some of the newer funds are still not fully invested. Given sterling weakness, currency movements have been distorting returns.

JLEN’s unique incorporation of environmental infrastructure assets means it is less vulnerable to a poor year of irradiation or weak wind generation than most of its peers. Technologies in which JLEN is actively expanding, such as AD and hydro, continue to benefit from a high proportion of inflation-linked cash flows that are backed by subsidies. JLEN is also pushing into sectors that are not yet considered as ‘core’ infrastructure, which the manager believes are also set to play an important role in decarbonisation, while also arguably providing more compelling valuation dynamics, in its view.

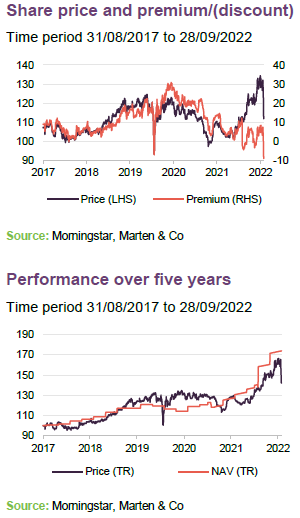

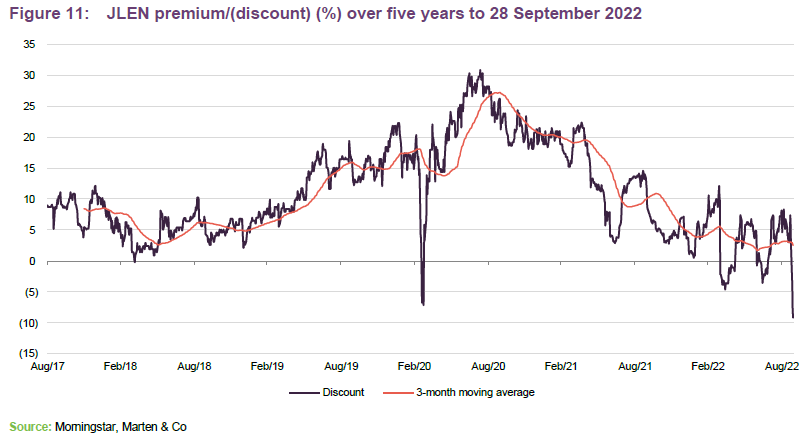

Premium/(discount)

Over the 12 months to 28 September 2022, JLEN’s shares traded between a range of a discount of 9.2% and a premium of 12.1% and averaged a premium of 3.8%. As at 28 September 2022, JLEN was trading on a discount of 9.2%.

JLEN’s brief period of trading at a discount earlier this year coincided with a big (and perhaps unanticipated by the market) jump in the NAV. It took a few weeks for the shares to re-rate. Nevertheless, the premium trended downwards from August 2020.

As yields on long-dated UK government bonds have risen recently, most funds valued on a discounted cash flow basis, including those in the renewable energy sector, have experienced share price weakness. It seems likely that fears of higher discount rates driving down NAVs are weighing on the share prices of JLEN and its peers. However, as was discussed above, it would appear that this is not the only factor that is likely to have an influence on the direction of the NAV.

Previous publications

JLEN Environmental Assets – Increasingly diversified as green-led recovery looms

John Laing Environmental Assets Group – Life extensions to boost NAV?

John Laing Environmental Assets – Diversification benefits shine through

John Laing Environmental Assets Group – Anaerobic diversification

John Laing Environmental Assets Group – Diverse renewables exposure

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on JLEN Environmental Assets Group Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.