Much more than just oil & gas

Gulf Investment Fund (GIF) has built up an attractive track record of both absolute performance and outperformance of its benchmark. Recent higher energy prices appear to have bolstered sentiment toward the region. Governments are using the revenue windfall to fund vast infrastructure projects aimed at diversifying their economies.

GIF is unique within the London-listed investment company universe and offers exposure to an arguably increasingly important region. Notwithstanding GIF’s track record, institutional investors have taken advantage of stringent discount control mechanisms and have shrunk the company. The board would like to see it re-expand.

Exposure to growth within the GCC economies

GIF aims to capture the opportunities for growth offered by the GCC economies of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates by investing in listed or soon-to-be-listed companies on one of the GCC exchanges.

Fund profile

GIF aims to capture the opportunities for growth offered by the GCC economies of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. It is permitted to invest in listed or soon-to-be-listed companies on one of the GCC exchanges. In practice, the company does not make pre-IPO investments.

GIF makes its investments through its wholly-owned, BVI domiciled subsidiary Epicure Qatar Opportunities Holdings Limited.

GIF was admitted to trading on AIM on 31 July 2007 and moved across to the Main Market on 13 May 2011. Following a growing concentration of the share register (see page 18), on 19 May 2021 the company moved to the Specialist Fund Segment. A more diversified share register might allow it to switch back to the Main Market again.

GIF’s initial focus was on the Qatari market. In 2017, the remit was broadened to encompass the whole of the GCC region.

The investment adviser

GIF’s investment adviser is Qatar Insurance Company SAQ (QIC) and GIF’s investment manager is Epicure Managers Qatar Limited, a wholly-owned subsidiary of QIC. QIC’s investment team has a total AUM of approximately $8bn. The core management team (see page 20) is based in Doha and manages about $800m in discretionary mandates for local institutions. Having a local presence makes it easier to access companies’ management and makes them less reliant on third-party sell-side research. The team aims to meet holdings at least twice each year.

The management team is not invested in the fund, but QIC is.

The backdrop – soaring energy prices

Countries within the GCC region are amongst the richest, in terms of per capita incomes, globally. Demographically, they are relatively young, and inbound migration is swelling the local population. Youth unemployment is relatively high, and the need to address this is high on governments’ agendas.

The wealth of the region is rooted in its oil and gas reserves (the adviser quotes figures of 489bn barrels of oil and 41.9trn m3 of gas). The prices of both commodities have a significant influence on governments’ revenues; local rates of taxation are relatively low, but oil and gas extraction businesses tend to be State-owned.

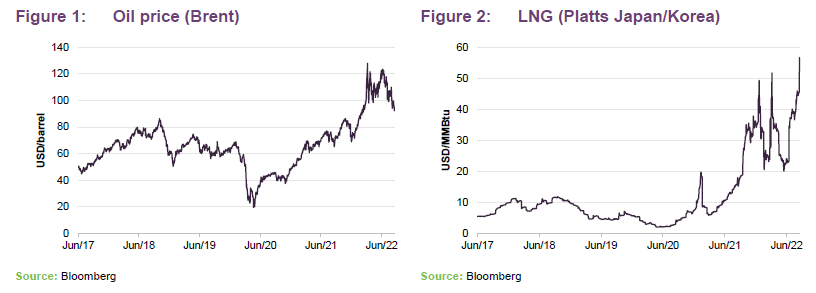

Gas prices continue to hit new highs, which is extremely positive for Qatar. Elsewhere in the region, with the oil price above $90bbl, and the threshold for balanced budgets ranging between $44bbl and $76bbl, governments’ finances are healthy. It may be that, where possible, governments will have been trying to lock in recent high prices for both oil and gas.

The economic recovery from COVID and growing demand for gas in Asia (as a less carbon-intensive alternative to coal) may have contributed to a steady rise in energy prices through 2021, but the war in Ukraine supercharged these. The sanctions that have been imposed on Russia since the invasion have led to a sharp increase in demand for oil and gas from the Gulf states. Russia’s threats to turn off the taps are seemingly maintaining the upward pressure, and OPEC’s refusal to up production could also help keep oil prices high, although economic weakness in the US and China appears to be affecting sentiment currently.

The advisers think that the higher oil prices will persist for a while yet. However, a hard landing is possible in time.

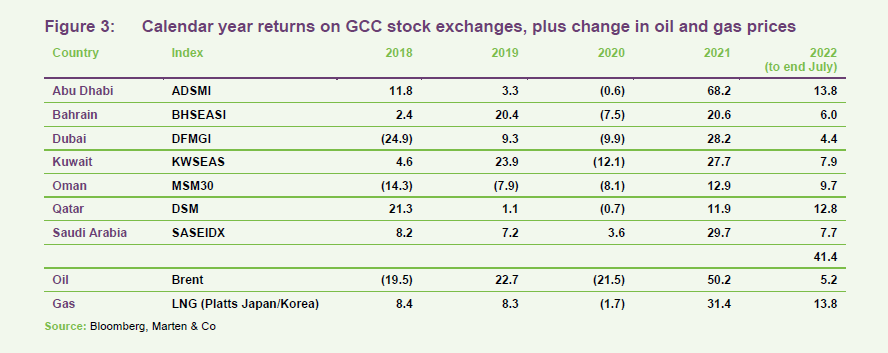

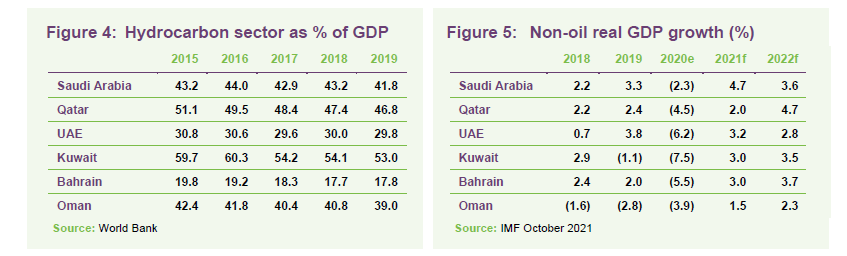

The rise in energy prices seems to have driven positive sentiment toward GCC exchanges, but there is much more to the region’s economy than just oil and gas extraction as is evident in Figure 4.

The period between 2014-2018 was one of low oil prices and this was part of the impetus behind efforts to diversify these economies away from sales of hydrocarbons and reduce the local population’s dependence on State largesse. The adviser says that subsidies for things like food, utilities and petrol have been slashed.

COVID had a significant impact on the region’s economies in 2020. However, the adviser feels that this was managed fairly well, and vaccination rates are now high in most GCC countries, although Oman appears to be lagging, with just 60% of the population fully vaccinated. Areas that were heavily affected by travel restrictions are now recovering.

Local currencies are tied to the US dollar, which could make these markets more attractive to US investors.

The high inflation plaguing many global economies seems to be much less of an issue amongst the GCC. Across the region, inflation is running below 2%. HSBC is forecasting that GCC inflation will hit 3.8% by the end of the year, falling back to around 3% in 2023.

As most oil and gas producing businesses are State-owned, the sector’s weight within local stock markets is relatively low. GIF is, therefore, primarily a play on the growth of the non-oil sector.

The correlation between oil prices and GIF’s NAV may be low, but it does affect sentiment toward the region. Recently, the sanctions imposed on Russia appear to have triggered a redirection of funds from that market to the GCC region. Qatar has seen more than $3bn of inflows since January, for example. Nevertheless, global investors generally have an underweight exposure to Qatar, Kuwait and Saudi Arabia.

An expanding universe

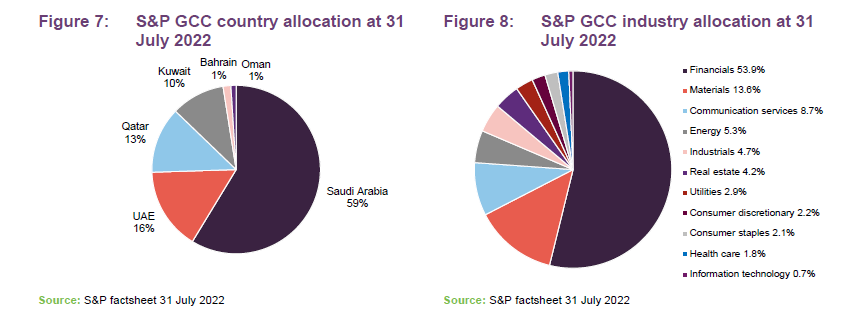

There were 333 companies within the GCC Index at end July 2022 and the universe is projected to grow relatively quickly. Earlier this year, the advisers were suggesting that 78 IPOs were anticipated. Capital market reforms have encouraged these, increasing the breadth and depth of local markets. Most IPOs are of good quality, the advisers think, and some have found their way into GIF’s portfolio. For example, GIF bought a stake in the holding company for the Saudi exchange – see page 15. The increasing breadth and depth of Gulf markets means that they now account for about 7.8% of the MSCI Emerging markets Index.

Investment adviser’s view

The investment adviser believes that investing in the region is not just all about oil. It is about diversification, infrastructure spending, expansion of the non-oil and gas sector, privatisation, and economic, social and capital market reforms.

The ongoing socio-economic/structural reforms in Saudi Arabia continue to open up opportunities for long term investors. Its Shareek Program (www.shareek.gov.sa), which is a part of the Kingdom’s SAR27trn investment plan, is expected to boost economic growth and strengthen the private sector.

The adviser believes that events such as FIFA World Cup 2022 (where over 1.5m people could visit Qatar during the tournament for what could be the world’s first post-COVID mass audience sporting event) and large-scale infrastructure projects such as NEOM City, the Red Sea project, and the North Field Gas expansion project, could propel economic prosperity in the region.

In Saudi Arabia, the government is pressing ahead with its reform agenda to deliver economic growth, following a slow start in recent years. Higher oil prices have refilled the Kingdom’s coffers and are likely to provide additional resources for its Public Investment Fund (PIF) and state funds to press ahead with investment plans.

Sector views

Financials

QIC is positive on the financial sector currently. US interest rate rises are positive for banks as they should increase the scope for higher margins. The adviser suggests that a 50bp increase in SIBOR translates into a 10bp increase in net interest margins and a 5% increase in earnings, on average.

The adviser expects to see continued credit growth within the banking sector, helped by areas such as project financing and a growing mortgage market (figures from QIC and the Saudi central bank – SAMA – suggest that the latter could grow at a compound rate of 13–14% between 2020 and 2030). There is scope for further M&A activity within the sector. Bad debts are not expected to be a problem, given the health of local economies. However, the adviser is being selective; some banks look expensive.

Infrastructure

Enormous sums are being invested in infrastructure. The construction and building materials industries are obvious beneficiaries of this, but it is also pulling in people from outside the region. The adviser feels that these mega projects and population growth are key drivers for continued economic success.

Tourism and leisure

COVID hit the sector hard, but it has bounced back. Governments are investing significant sums in the sector, as we describe elsewhere in this note. Tourism growth is helping local airlines such as Air Arabia (held by GIF), which the adviser says is the local equivalent of Ryanair. It has ambitious expansion plans, having placed orders with Airbus for 120 aircraft to complement its existing fleet of 58.

The adviser notes that visitors are taking longer holidays in the region, which feeds through into increased room demand.

Technology

Prospects for the information technology sector should be good given the local commitment to upgrading and digitalising infrastructure. However, the adviser notes that IT companies have sold off, in common with global peers.

Consumer

Many consumer – especially food and beverage – stocks have been impacted by cost input inflation. Much depends on their pricing power, but the adviser is cautious on the sector.

Energy and petrochemicals

Considerable sums are being spent on developing and upgrading hydrocarbon infrastructure, including Qatar’s North Field expansion (see below), in excess of $120bn of planned investment by Abu Dhabi National Oil Company (ADNOC) by 2026, and $4.2bn on the modernisation of Bahrain’s BAPCO refinery.

The adviser is uneasy about valuations within the petrochemical sector as rising feedstock prices are hitting margins.

Country views

Qatar

The adviser’s most favoured market within the GCC region is Qatar. In part, that reflects the relative valuations of stocks between the various exchanges. However, the adviser is also optimistic about the macroeconomic prospects for the country.

Increased demand for LNG, initially across Asia and then as a replacement for Russian supplies, has propelled the gas price to new highs. Qatar is fortunate to have abundant reserves (the third-largest globally) and a capacity expansion is underway – the QAR200bn North Field expansion – which could allow a 64% increase in Qatar’s LNG production by 2027. Qatar is already one of the lowest-cost LNG producers globally. The adviser thinks that the LNG expansion will contribute to a doubling of Qatar’s GDP.

In addition, it is hoped that the upcoming FIFA World Cup will provide a permanent boost to tourism in the country. The adviser says that Qatar’s Hamad International and Doha International airports should handle 34–36m passengers this year, nearly double 2021’s passenger numbers.

The adviser also highlights Qatar’s March 2021 lifting of restrictions on foreign ownership of Qatari stocks. It thinks this could translate into QAR5.4bn of inflows of foreign investment. Qatar’s GDP growth is expected to be 3.4% over 2022.

Saudi Arabia

Saudi Arabia’s GDP is forecast to grow by 7.6% over 2022.

The fund’s benchmark is dominated by Saudi Arabian stocks, which account for around 60% of the index by market capitalisation. Ever since its mandate was broadened to include the GCC, GIF has tended to have a significant underweight exposure to the country, and this applies currently. The main reason is that stock valuations in the country are higher than the investment adviser is comfortable with. They moved up sharply when Saudi Arabia was included within emerging market indices, and have not normalised since. That move did help to increase the importance of the GCC region within EM indices.

Privatisations in areas such as healthcare, wastewater management and education are helping to grow the listed sector.

The largest of its mega projects (about $500bn) is NEOM (neom.com), the new Saudi city being built on the Red Sea. The project is proceeding in phases, the first of which are The Line (a linear city of 1m people) and OXAGON (a clean industrial and technology hub with strong logistics infrastructure). There is an emphasis on sustainability and the use of renewable power. By providing amenities locally, cars will be de-emphasised in favour of pedestrians and high-speed mass transit.

Saudi Arabia is investing to boost its tourism sector, and not just to accommodate increased numbers of pilgrims. Annual Umrah visitors are projected to hit 30m by 2030 and that means additional investment in Makkah, Madinah and Jeddah.

Saudi Arabia plans other developments on its Red Sea coast, including a tourism project on the Amaala island, with completion of its first phase planned for 2024. There is also a separate Red Sea Project aiming for 22 islands, 48 hotels, 6 inland sites and 8,000 rooms to be developed by 2030.

Other leisure investments include Al Qiddiya, a 320,000sqm entertainment project that includes a Six Flags theme park. The adviser notes that these developments could, in time, have an impact on the UAE’s tourism and leisure sector.

In the mining and metals sector, Saudi Arabia hopes to attract $32bn of investment into nine projects.

Kuwait

GIF has no exposure to Kuwait at the moment. Again, the issue is one of excessive valuations.

Kuwait has ambitious plans to spend around $160bn on its five islands project and a further $86bn on its Silk City project. However, progress has been slow, not helped by COVID. The Sheikh Jaber al-Ahmad Al-Sabah causeway now links Kuwait with the Silk City site, and work is underway on Mubarak Al Kabeer port, but construction work on the city is yet to begin.

UAE

The UAE is working hard to diversify its economy. Progress on that front was held back by a real estate bubble and then the pandemic, but its economy is now recovering. The UAE plans to spend $163bn on renewable energy projects, including the 3GW Mohammed bin Rashid Solar Park, and considerable sums on tourism-related projects, including SeaWorld Abu Dhabi. A nuclear power station – Barakah nuclear power plant – is also under construction.

Tourism is an important contributor to the economy, and Emirates and Etihad are the region’s first and fourth-largest airlines, respectively.

Remarkably, perhaps, given cultural sensitivities, Dubai is considering a casino project in conjunction with Wynn Resorts.

Oman

The adviser says that Oman is a small market and low liquidity constrains GIF’s allocation to that country.

Investment process

The investment adviser is a stock picker; while GIF’s returns are compared to the S&P GCC Index, the investment approach is index agnostic and index weightings do not influence portfolio construction.

The investment universe encompasses all listed stocks in GCC markets. Whilst the fund is permitted to make pre-IPO investments, in practice these will not feature within the portfolio.

The adviser applies a liquidity screen to the universe; in theory the adviser would like to construct a portfolio that could be liquidated within five trading days. The remaining stocks will be modelled by the team, and the team will seek to meet management and may also source research from external analysts.

From this, a watch list of stocks that the advisers feel are attractive is constructed. To progress to inclusion within the portfolio, stocks will have to be attractively valued relative to the wider market and to peers. Valuations are assessed based on the adviser’s DCF models and using recognised metrics such as EV/EBITDA.

The size of an individual position depends on the adviser’s view of the balance of risk and reward offered by a stock. GIF operates with a focused portfolio of between 20 and 25 stocks. The adviser is comfortable with a single stock accounting for about 10% of the portfolio, but would not seek to have more than 15% in an individual position. The portfolio will typically include at least eight to 10 core holdings, and at least four to six lower-conviction positions.

Turnover has been high in recent years, reflecting market volatility – a number of stocks kept hitting target prices. In more normal conditions, the adviser would expect to hold a position for about two to three years on average.

The high market volatility means that the adviser is not comfortable with using leverage. GIF does not have a borrowing facility currently.

GIF does not seek to hedge its market or currency exposures.

ESG

A consideration of ESG aspects forms part of the adviser’s investment research process. The adviser acknowledges that there is room for improvement in all these areas and the additional risk associated with any failings in these areas is factored into investment decisions. Things are said to be improving; independent non-executive directors are more commonplace but not mandated, for example. Attitudes towards greater female participation in the economy are changing too.

With respect to the environment, the region’s hydrocarbon extraction is clearly a significant contributor to climate change. These countries are well aware of this and, ahead of COP 26, net zero commitments were made by countries such as the UAE (2050), Saudi Arabia (2060), and Bahrain (2060). Qatar is aiming for a 25% reduction in greenhouse gas emissions by 2030.

Asset allocation

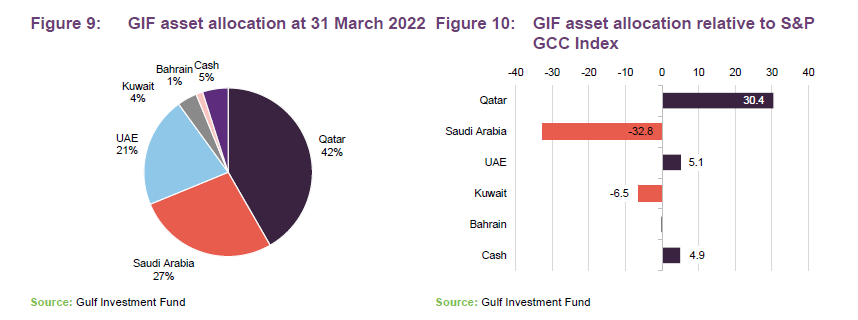

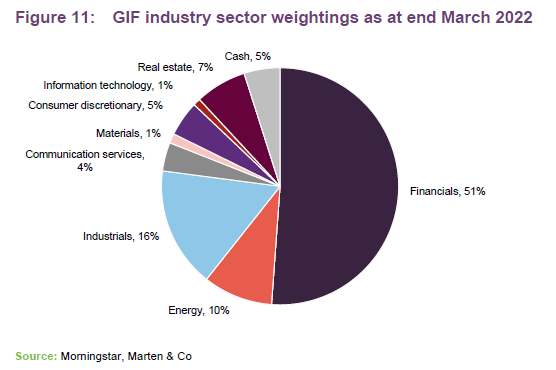

At the end of March 2022, GIF had 23 holdings.

The adviser says that the fund’s overweight exposure to Qatar reflects that country’s macroeconomic resilience, growth prospects and attractive valuations. By contrast, the significant underweight exposures to Saudi Arabia and Kuwait reflect relatively expensive valuations. At the end of June, the allocation to Qatar was 37.0% (24.5 percentage points higher than its weight within the benchmark), UAE (19.7% versus 15.9%), Saudi Arabia (30.6% versus 58.6%), and Kuwait (2.9% versus 10.6%). GIF has not disclosed the respective allocations to Bahrain and cash at end June 2022.

The portfolio’s relative high exposure to financials reflects the adviser’s view on the prospects for that sector in an environment of rising US interest rates. Over Q2, the exposure to financials was reduced from 51% to 33%, while exposure to industrials and healthcare was increased.

Top 10 holdings

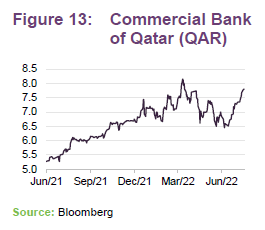

Commercial Bank of Qatar

Commercial Bank of Qatar (cbq.qa) is the second-largest bank in Qatar. The adviser notes that the bank is aiming to strengthen its balance sheet by cautiously managing its risk exposure, and is expanding its geographic footprint through strategic partnerships with other banks in the region.

Latest (Q2) results show improving profits (up 7.9%), a capital adequacy ratio of 17.5%, 8.8% growth in assets to QAR176.4bn, and an interest margin of 2.8%, up from 2.7% for Q2 2021. The bank’s Turkish subsidiary – Alternatif Bank – was profitable over the first half of 2022 (lossmaking in H1 2021).

The statement noted the 3.4% forecast expansion of Qatar’s GDP over 2022, and the tailwind to growth coming from the North Field expansion.

Qatar Islamic Bank

Qatar Islamic Bank (qib.com.qa) is the country’s largest Islamic bank by assets and the second-largest bank in Qatar. The adviser says that the bank has one of the highest ROEs of its peers, is cost-efficient, well-capitalised, and has a superior asset quality profile.

QIB’s first half figures for 2022 show a small deterioration in total assets (down 0.7%) and its capital adequacy ratio (down 0.4% to 18.5%). However, EPS rose by 13.8% as the cost to income ratio and provisions both fell over the period.

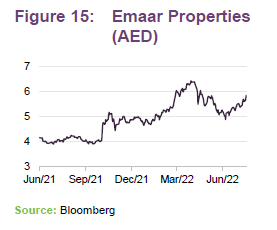

Emaar Properties

Emaar Properties (properties.emaar.com) is the leading property developer in the UAE, with a land bank in excess of 1.7bn sq ft. It offers exposure to the recovery of the real estate market in Dubai through Emaar Malls, Emaar Hospitality, entertainment, leasing, and a retail asset portfolio (including Burj Khalifa, Dubai Mall, and Dubai Fountain). In addition, it has activities in markets outside the GCC such as Egypt and India. The adviser notes that it has a strong balance sheet, a strong credit profile, and brand loyalty.

Emaar’s Q2 2022 figures were very strong, supported by strong sales of properties and the February 2022 launch of Dubai Hills Mall. The hospitality segment reported revenue growth of 93% over H1 2021, helped by average occupancy levels of 71%, which it attributes to a robust recovery in the region’s tourism sector.

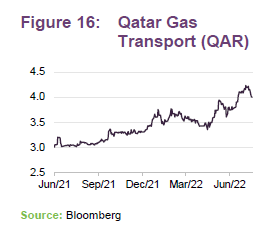

Qatar Gas Transport

Qatar Gas Transport aka Nakilat (nakilat.com) is the largest LNG transportation company globally with interests in 74 vessels and significant expansion plans to cater for the increased production associated with the North Field expansion. Globally, the LNG market is forecast to grow at a compound rate of 4.6% up to 2026.

Q2 2022 results showed a 6.3% increase in revenue accompanied by a lower increase in expenses (up 2.4% mainly on higher finance charges) which fed through into a 14.9% increase in net profit.

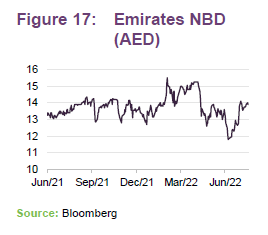

Emirates National Bank of Dubai

Emirates National Bank of Dubai (emiratesnbd.com) is the fourth-largest bank in the GCC region. It is a global bank operating in 13 countries with over 900 branches. The adviser believes that the bank is well-capitalised (a common equity Tier 1 ratio of 15.0% at the end of June 2022) with a stable asset quality outlook and has strong management, and commends its track record. It says that it is a leader in digital banking and thinks that this will translate into improved margins in time.

The bank’s Q2 2022 results showed net profit up 11% and earnings per share up 14% year-on-year as income rose and impairments fell. The net interest margin expanded to 2.86% from 2.45% for H1 2021.

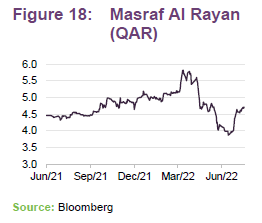

Masraf Al Rayan

Masraf Al Rayan (alrayan.com) is a Qatar-based Sharia-compliant bank, offering corporate and personal banking, asset management, treasury and trade finance. The bank also has operations in the UAE, UK and France. The adviser says that Masraf’s Q4 2021 merger with Al Khalij Commercial Bank will help strengthen its revenue streams and will be associated with cost savings.

The bank’s Q2 2022 figures showed strong growth of income (up 21% year-on-year) and a capital adequacy ratio of 20%. Excluding one-off merger expenses, the bank has a cost-to-income ratio of 20.4%, one of the lowest in Qatar.

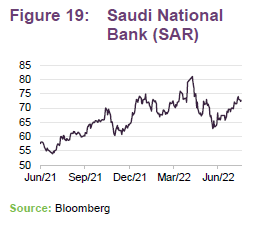

Saudi National Bank

Saudi National Bank, aka Alahli (alahli.com), was the product of a merger of NCB and Samba Financial Group that was agreed in October 2020. The bank has made significant progress in digitalising its business, with over 99% of retail and 98% of wholesale transactions processed digitally. A new Incubator Bank is planned for Q1 2023 to drive market innovation and introduce digital financial services to niche segments.

The merger brought a number of cost synergies; at 31 March 2022 the company said it had achieved SAR700m of a targeted SAR1.2bn of cost savings.

At the end of June 2022, the bank had a tier 1 capital ratio of 17.6%, down from 18.4% at end December 2021. It is targeting a 28% cost-to-income ratio for 2022 (28.5% at 30 June 2022), down from 33.5% for 2021, and a return on total equity of between 15% and 16%, up from 12.6% (16.3% at 30 June 2022).

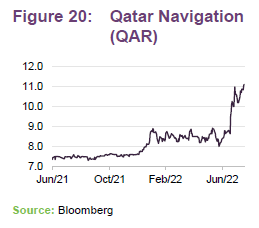

Qatar Navigation

Qatar Navigation, aka Milaha (milaha.com), is maritime transport, logistics, port management, and marine offshore services business. It also owns a 36.3% stake in Nakilat (see above) and a 49% stake in QTerminals, which provides container, general cargo, RORO, livestock and offshore supply services in Phase 1 of Hamad Port in Qatar. Milaha has its own extensive fleet of vessels including container ships, LNG carriers, and offshore support vessels.

Nakilat’s success helped drive a 46% year-on-year increase in net profits for H1 2022. Milaha says that it expects that shipping rates will remain relatively stable over the rest of 2022. It expects to benefit from an uplift in warehousing & freight forwarding from new global network partnerships. It is also a beneficiary of the work on the North Field expansion.

Saudi Tadawul Group

Saudi Tadawul Group (tadawulgroup.sa), which IPO’d on 8 December 2021, is the parent company of the operator of the Saudi stock exchange. The exchange has over 200 listed companies and a market capitalisation in excess of SAR10trn. The upgrading of Saudi Arabia to emerging market status in 2018 and the subsequent end 2019 listing of Saudi Aramco provided a significant boost to its business.

Q2 2022 results were down on the equivalent period for the prior year as trading volumes ‘normalised’ (total comprehensive income contracting by 24% year-on-year). This was offset to some extent by higher data and technology services, and listing fee revenue, and lower overheads.

Dubai Islamic Bank

Dubai Islamic Bank (dib.ae) is the largest Islamic bank in the UAE by assets (over $75bn) and the second-largest globally. It serves around 5m customers from about 500 branches distributed across the Middle East, Asia and Africa.

Q2 2022 figures showed a 45% jump in net profit year-on-year as the business grew, loan impairments fell, and the cost-to-income ratio improved. At the end of June 2022, the bank had a capital adequacy ratio of 17.9%.

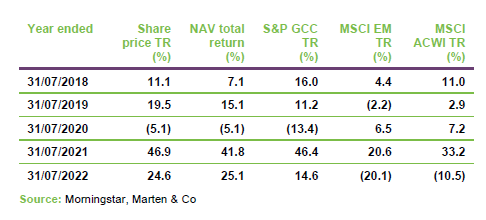

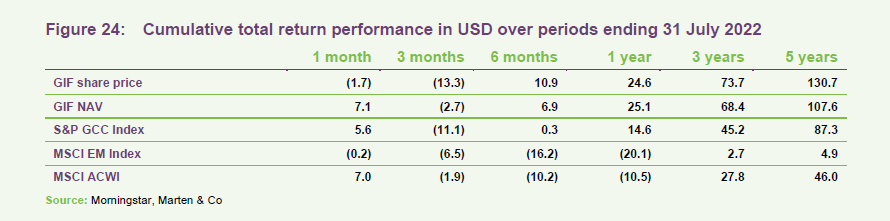

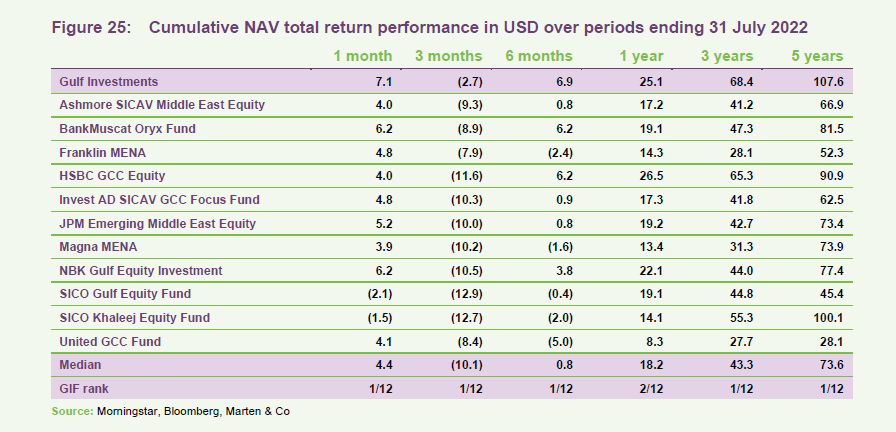

Performance

A broadly-based rally in GCC markets, driven in part by strong oil and gas prices, has helped generate decent absolute returns for GIF in recent quarters. However, in Q2, GCC markets fell back in line with other global markets.

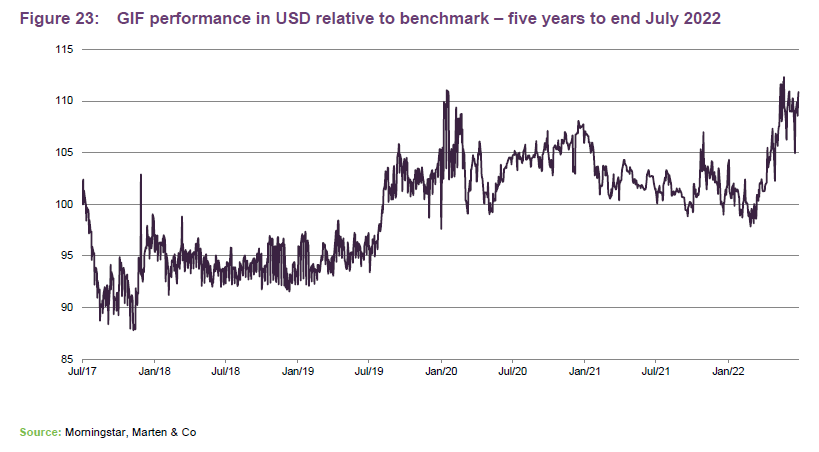

As we show in Figure 23, GIF has delivered considerable outperformance of its benchmark, the wider emerging markets universe, and global indices over the past five years in NAV terms, and a narrowing discount has generated even higher returns for shareholders.

Al Rajhi Bank, which is a significant constituent of the benchmark index but is not held within GIF, was a strong performer over 2021 and that held back GIF’s performance relative to the S&P GCC Index for a period.

GIF’s Q1 report said that positions in Saudi Tadawul Group (up 51.8%), Alinma Bank (up 62.1%), Qatar Islamic Bank (up 30.1%), and Emaar Properties (up 22.7%) were all significant contributors to returns.

In its Q2 report, GIF said that its underweight exposure to Saudi Arabia provided a positive contribution to relative returns. A higher cash weighting and stock selection were also positives. Looking at individual stocks, good performance came from Air Arabia (up 29.2%), Gulf International Services (up 6.0%) and Qatar Gas Transport (up 4.5%). In the case of Air Arabia, the shares were helped by recovering passenger demand. Gulf International Services reported stronger revenues. Elsewhere, Qatar’s North Field Expansion project remains a catalyst for Qatar Gas Transport.

Large holdings that contributed negatively to GIF’s Q2 2022 returns were Commercial Bank of Qatar (down 8.4%), Emirates National Bank of Dubai (down 12.0%) and Emaar Properties Company (down 13.3%).

Looking at the longer term, GIF published some figures as at end January 2022 that showed that it outperformed its benchmark in eight of the 10 previous years. Looking at its quarterly returns over that period, GIF outperformed a rising market 65% of the time and outperformed a falling market 71% of the time.

The five-year numbers in Figure 24 include a few months when the fund had a narrower focus on the Qatari market.

Peer group

GIF sits within the AIC’s global emerging markets sector. However, with no direct closed-end comparators, GIF tends to compare its returns to an open-ended peer group. The peer group that we have assembled comprises GIF’s five chosen comparators plus other funds investing in GCC equities. Many of these funds may not be easily accessible by UK-based investors – SICO Khaleej Equity Fund is only registered for sale in Bahrain, for example.

GIF ranks at or close to the top of the performance tables over all time periods.

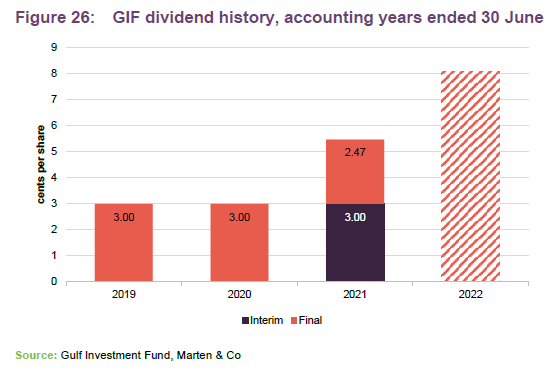

Dividend

The portfolio is not managed to produce a target level of income. GIF tended to pay one dividend per year historically. However, in 2021, the board introduced an enhanced dividend policy targeting semi-annual payments of a total annual dividend equivalent to 4% of NAV at the end of the preceding year. The unaudited NAV at 30 June 2022 was $2.0261, which implies a total dividend of 8.1 cents for the accounting year ended 30 June 2022.

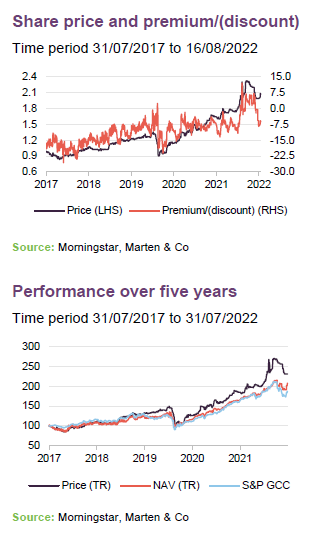

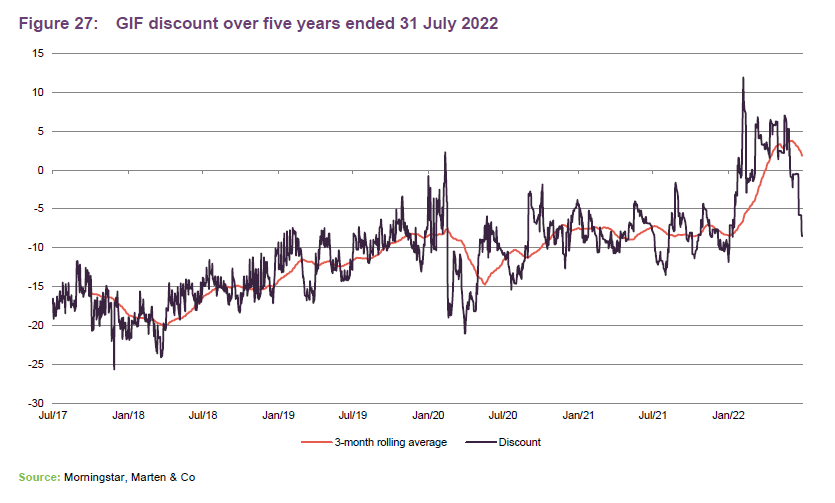

Premium/(discount)

Over the 12-month period ending 31 July 2022, GIF’s shares traded between a 13.5% discount and an 11.9% premium. Over this period the average discount was 3.8%. At 16 August 2022, the discount was 6.3%.

GIF’s aggressive discount control efforts and track record may have contributed towards the shares trading above or close to NAV in recent months. However, despite GIF’s recent outperformance of its benchmark, the discount has widened in recent weeks.

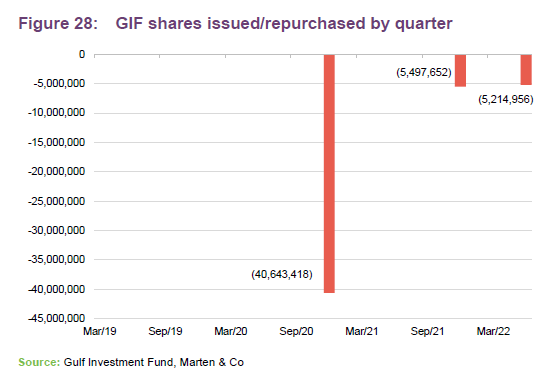

GIF offered shareholders a 100% tender offer in 2020 and that led to significant shrinkage of the fund. Following this, GIF adopted a policy of biannual tender offers. Two subsequent tender offers reduced the size of the fund further, but the board’s hope is that the renewed interest in GIF, on the back of strong investment performance, will lead to a re-expansion of the fund in time. Should the number of shares in issue fall below 38m, the directors will put forward a continuation vote.

Assuming that the shares trade at a premium, GIF is able to re-expand by issuing shares (which enhances the NAV for existing shareholders and improves liquidity). On 9 May 2022, GIF announced that it had made an application to the London Stock Exchange for a block listing of 2,700,000 ordinary shares to be admitted to trading on the Specialist Fund Segment. The shares may be issued on a non pre-emptive basis, to satisfy continuing market demand for the shares and to manage the premium to NAV at which the shares trade.

Fees and costs

The investment manager is entitled to a fee of 0.8% of NAV, calculated monthly and payable quarterly in arrears. This fee arrangement has been in place since 1 January 2021, when the fee was reduced from 0.9% of NAV.

The other significant expenses incurred by the fund over the year to end June 2021 were $189,000 for the administrator and registrar (FY20 $199,000) and $178,000 (FY20 $278,000) for the directors (see page 21).

GIF’s ongoing charges ratio for the accounting year ended 30 June 2021 was 1.55%, but this was running at 1.71% at end December 2021, reflecting the shrinkage of the fund (as fixed costs are spread over a smaller base).

Capital structure

GIF has 41,105,216 ordinary shares in issue and no other classes of share capital. None of these shares are held in treasury and therefore the number of shares with voting rights is 41,105,216.

GIF does not have a fixed life but the board considers it desirable that shareholders should have the opportunity to review the future of the company at appropriate intervals. Shareholders are able to participate in bi-annual tender offers for up to 100% of the share capital.

GIF’s next continuation vote is scheduled to be held at the AGM in 2023.

Managers

Jubin Jose (portfolio manager)

Jubin Jose has over 16 years of extensive experience in Investment management and research. Jubin joined QIC in 2007. At QIC, Jubin is responsible for the management of the Gulf Investment fund portfolio and QIC’s Qatar equity portfolios. He follows a deep research investment approach to build portfolios with long-term return potential, after rigorous quantitative and qualitative analysis. Jubin has over 14 years’ experience of working in the Middle Eastern Markets.

Bijoy Joy (assistant portfolio manager)

Bijoy is involved in the day-to-day management of the fund. He has over 11 years of investment experience, of which, more than nine years have been in the GCC region stock markets. Bijoy joined QIC in 2014 and is responsible for generating new ideas and expanding the capacity and capabilities of the investment research division. Prior to QIC, Bijoy worked for nearly four years with a leading financial research firm in India focusing on industry and equity research. He holds an MBA in Finance from Bharathidasan University, India and is a CFA level 3 candidate.

Wei Nien Chow (analyst)

Chow joined QIC as an investment analyst in 2021 and is involved in equity analysis and research of most major sectors across the GCC market. Prior to QIC, he was a sell-side equity analyst with a leading local investment bank, based in Kuala Lumpur, Malaysia. He has over three years of extensive experience in equity and industry research, mainly covering the consumer and automobile sectors. Chow holds a Bachelor’s degree in Actuarial Science from Heriot-Watt University, UK and is a CFA Level 3 candidate.

In addition to the managers, there is a team of five analysts covering both equities and macroeconomics, based in India.

The team is growing; the plan is to add two more analysts in Doha and one more in India.

Board

GIF has three non-executive directors, all of whom are independent of the manager and do not sit together on other boards.

GIF’s board has shrunk as the size of the company has reduced. At the end of June 2021, GIF had three non-executive directors (down from four a year earlier). Since then, Nicholas Wilson resigned (as planned) as a director and as chairman with effect from 31 December 2021. Anderson Whamond, who joined the board in August 2021, replaced Nicholas as chairman.

It is the board’s policy that non-independent directors stand for re-election every year and independent directors stand for re-election every three years.

The maximum annual remuneration payable to the directors permitted under the Articles of Association is £200,000, but the current figure is well within that.

Anderson Whamond

has over 30 years’ experience in the banking and financial services sector. He is a non-executive director of The International Stock Exchange Group Limited, and a non-executive director of the Irish domiciled Magna Umbrella Fund and the OAKS Emerging & Frontier Umbrella Fund. Previously, he was a non-executive director of Cayman Islands-domiciled OCCO Eastern European Fund.

Neil Benedict

Neil is based in the USA and has over 30 years’ experience of financial markets. He was formerly a managing director at Salomon Brothers, where he was head of international capital markets, and, prior to that, the founder and head of the worldwide currency swaps group. Neil was also a managing director at Dillon Read and helped establish their Tokyo office. He is currently a senior managing director at Sonenshine Partners, a New York private investment bank. Neil is a fellow member of the Institute of Chartered Accountants in England and Wales.

David Humbles

David worked in the downstream oil industry for 25 years and relocated to the Isle of Man in 1998 as a director of Total. In 2003, he purchased Abbey Properties Ltd which owns and manages a property complex in the north of the island. David also owns Westminster Properties Ltd which manages a large portfolio of residential and commercial properties on the island. David was managing director of Oakmayne, a residential developer in London. He has previously served on the board of two AIM-listed companies.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Gulf Investment Fund Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.