No compromise

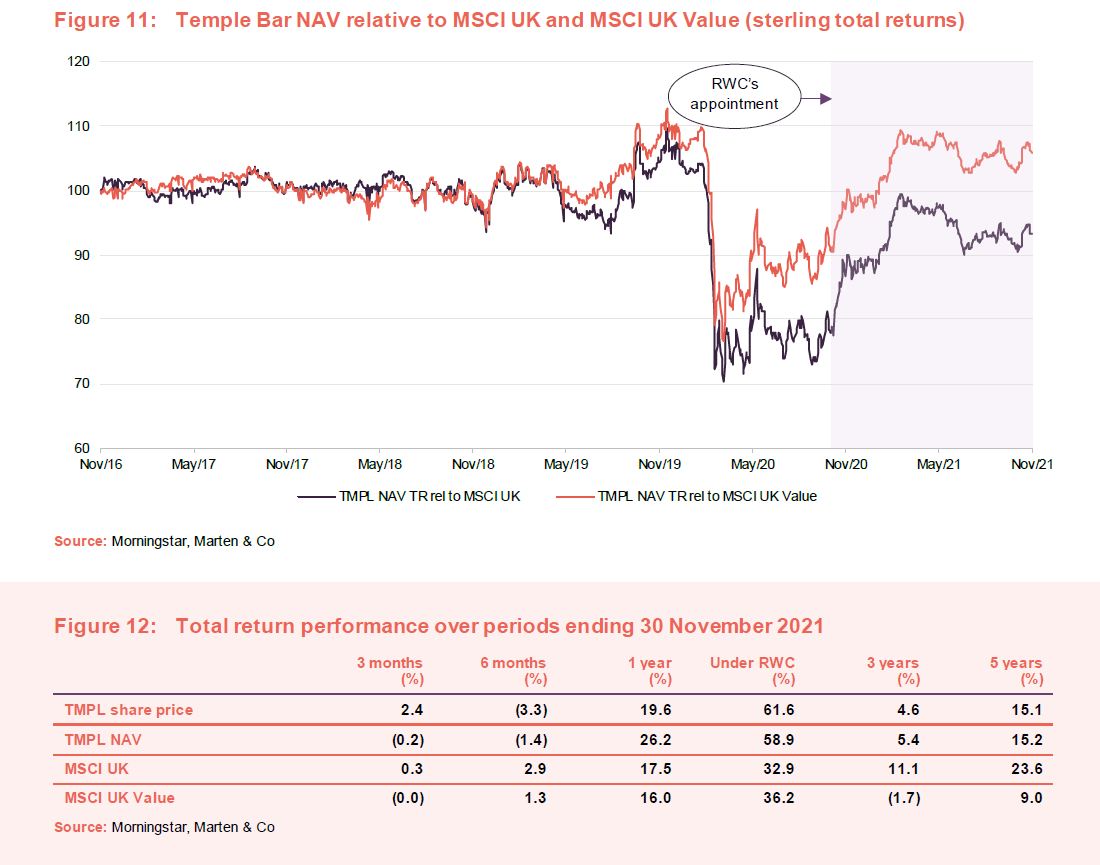

The turnaround in Temple Bar (TMPL)’s fortunes following the appointment of RWC as manager last November and a surge in ‘value’ stocks on hopes of an end to the COVID-19 pandemic has been dramatic. Frustratingly, the discount that the trust’s shares trade on relative to their net asset value widened from the middle of April 2021, as investors fretted about the impact of new variants of the virus and switched back to buying ‘growth’ companies for their perceived ability to thrive even in a lacklustre economy.

As we discuss on page 4 of this note, TMPL’s managers – Ian Lance and Nick Purves – are keen to highlight that value and poor quality do not necessarily go hand-in-hand. They seek to identify good quality and growing business trading on attractive valuations. An investment in a fund run in a value style such as TMPL should not mean compromising on long-term total returns.

UK equity income and capital growth

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities, with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

Fund profile

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

For 18 years, TMPL was managed by Alastair Mundy, who was head of the Value Team at Ninety One UK. He stepped down as manager in April 2020. On 23 September 2020, the board announced that it had selected RWC Partners as TMPL’s new investment manager. RWC took on responsibility for the portfolio with effect from 1 November 2020.

RWC Partners

TMPL’s AIFM is RWC Partners. Within RWC Partners, responsibility for managing TMPL’s portfolio rests with Nick Purves and Ian Lance (the managers). Nick and Ian have over 50 years’ experience between them and have worked together for more than 13 years. The two co-manage over £3bn of assets across a number of income funds.

Value stocks can be growing businesses

Logically, the opposite of ‘value’ is ‘expensive’, not ‘growth’ or ‘quality’. TMPL’s managers bemoan the tendency in some quarters to equate value investments with poor quality companies in terminal decline.

While it is true that some stocks are cheap for good reasons, Ian and Nick see a central part of their job as sifting through the pool of attractively-valued companies to identify those that are capable of growth over the long term. Conversely, they question the wisdom of overpaying for growth and quality.

The investment process, which we discuss in greater detail from page 7 onwards, requires that the managers calculate an intrinsic value for a business, factoring in things like its growth prospects, and the strength and likely persistence of its margins. The value opportunity arises because investors have an irrational dislike of a business, or misunderstand it, or are too focused on short-term problems, for example.

The managers have written an article on this topic – Don’t believe the labels – which is available on TMPL’s website and which we recommend that you read. The article also addresses the question of whether the pace of technological change is accelerating the demise of traditional businesses that fall into the value camp. Their belief is that the world is not polarised into disrupters and the disrupted – indeed, many companies in TMPL’s portfolio are successfully repositioning their businesses to reflect technological change. In addition, many growth companies are threatened by new entrants and, since they are more highly valued, such companies – growth traps – can underperform so-called value traps.

The UK market is still out of favour

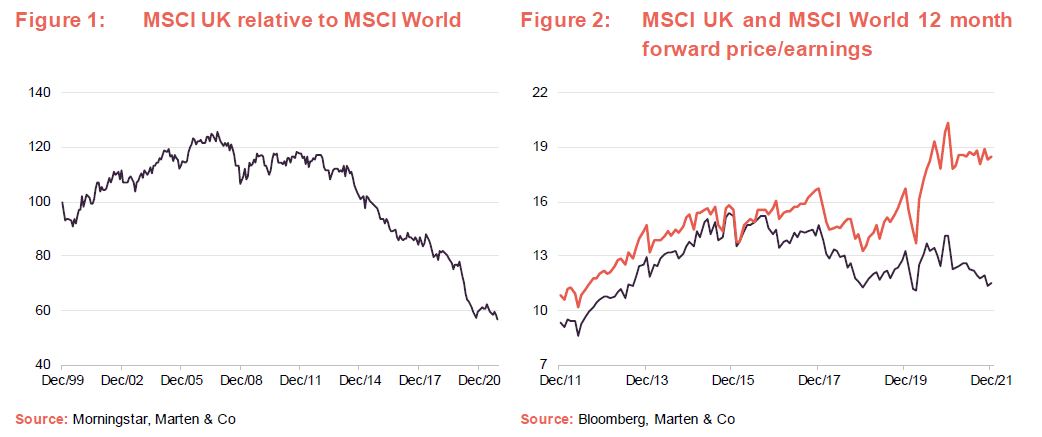

We highlighted the relative underperformance of the UK market relative to global indices in our September 2020 note. The Brexit agreement and the reopening of the UK economy in the wake of the vaccination programme were reckoned by many to be potential catalysts for improved relative performance. However, the chart in Figure 1 (which has 20 years’ worth of data) suggests that this has not happened. Earnings growth is coming through for UK companies, however, and they are heading towards forward price/earnings multiples seen at the trough of the panic last March and, before that, in 2013. UK stocks are still decoupled from global markets.

Value is still out of favour

The managers observe that an uptick in mergers and acquisitions activity in the UK is indicative of a recognition that UK stocks are attractively valued. TMPL benefitted from the acquisition of Wm Morrisons, for example.

The managers say that the larger stocks in the UK are more attractively valued than mid-caps, and this is reflected in the composition of TMPL’s portfolio.

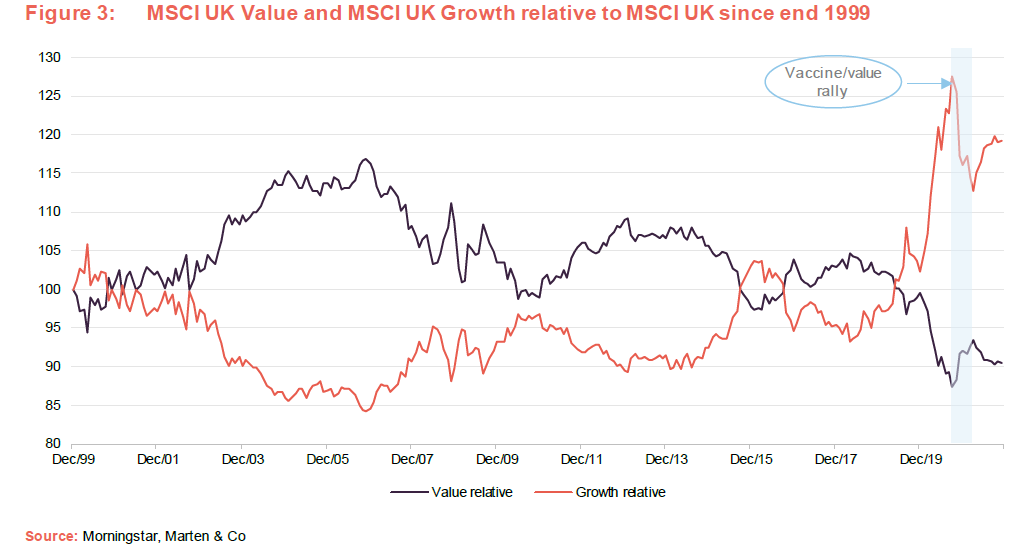

The reversal in the value rally in April has been linked to rising concern over new variants of COVID-19 and the effects of these on the pace of economic recovery. The emergence of the Omicron variant may represent a further setback, especially for the leisure and travel sectors, but it is reasonable to expect that vaccine programmes will adapt in relatively short order. In the UK, the tax increases pushed through in recent budgets could also have an impact on consumer spending.

In some respects, however, the pull-back in value stocks seems at odds with the fundamentals. The managers note sizable earnings upgrades in a range of value sectors.

Shortages of all kinds abound, but many raw materials are in particularly short supply after years of underinvestment. In addition, the commitment to cutting carbon emissions through a shift to renewable energy and the accelerating shift towards electric vehicles amplifies demand for many metals. This is positive for many constituents of the mining sector.

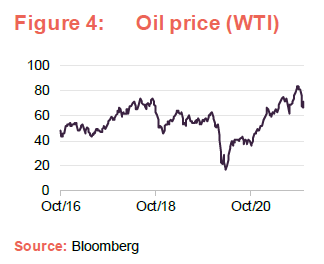

Even with the latest Omicron-related setback, rising oil and gas prices should be lifting the energy sector, which is at the forefront of rising earnings expectations. Again, underinvestment constrains supply. Increasingly, the sector is being shunned by investors on environmental grounds. The managers feel that this will likely mean that capital expenditure is depressed, extending the period of supply deficit and maintaining higher energy prices for longer. This means that the oil majors are highly cash-generative. This gives them the finance that they need to invest in the transition away from fossil fuels and could also support higher dividends.

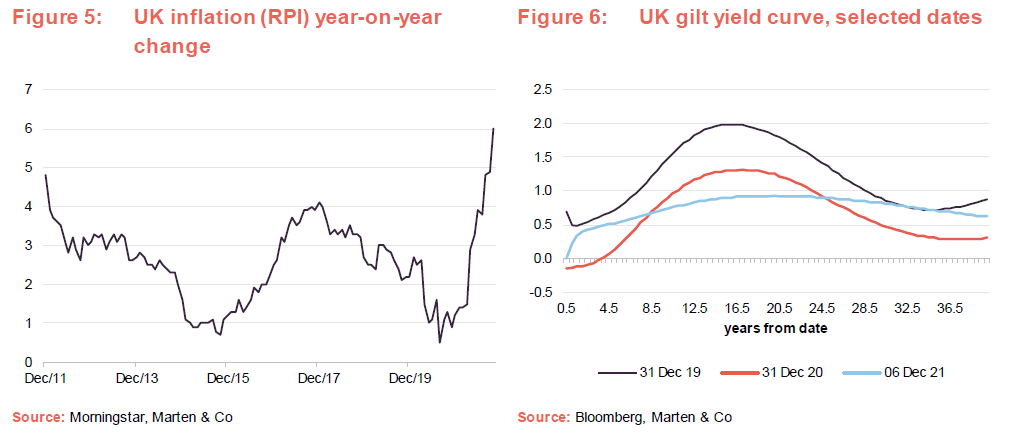

Inflation is not transitory

Governments and central banks have injected huge monetary and fiscal stimulus into the global economy in 2020 and 2021, aiming to combat the effects of the pandemic. A squeeze in input costs has been exacerbated by supply chain bottlenecks. The resultant higher inflation is leading to calls for interest rate rises, which should be good news for banks. The banking sector is in better health than it was when coming out of the global financial crisis. Over a decade of strict capital discipline has left its balance sheets in much better shape and loan delinquencies (late payments) have been kept low by the fiscal largesse.

Figure 6 charts the yield curve in the UK for UK government debt (gilts). Each line represents the yields of gilts for a range of repayment dates. A steeper yield curve (a larger positive gap between the yield at the short end of the curve and the medium-to-long end) would also be beneficial for banks, but for the moment, quantitative easing continues to distort UK gilt yields.

Globally, one dampener on inflation could be slowing growth in China, following a clampdown on various sectors of that economy and the looming failure of some of its largest property developers.

Long-term, value-oriented investment approach

Nick and Ian manage TMPL on a bottom-up basis and the shape of the portfolio is driven by their stock selection decisions. They operate a high-conviction style and TMPL’s portfolio will normally comprise about 30 positions and, at the end of October 2021, the 10 largest positions accounted for 51.3% of the portfolio. Index weights have no influence on portfolio construction and the portfolio has a high active share.

Stock selection is driven by fundamental research. The managers are looking for stocks that are trading at a discount to their intrinsic value. When assessing the potential of the stocks being considered for their portfolios, the team takes a five-year view. The managers then apply a long-term average valuation multiple to their view of normalised, mid-cycle earnings.

The managers say that they are cognisant of the economic environment when making investment decisions, but make no attempt to time markets.

The managers are keen to avoid so-called value traps and so, whilst these companies may have short-term issues, their businesses should be on a medium- to long-term growth trajectory. The company should be managed in line with sustainable or responsible principles. Companies should also be robust enough, in terms of balance sheet strength, to survive whatever short-term problems they are facing.

The underlying ethos behind the approach is that, just as investors become over-exuberant about some stocks, they become overly pessimistic about others. They then extrapolate from short-term setbacks and apply very low valuation multiples to trough earnings.

This presents an opportunity for value managers such as the RWC team, but they have to be patient. This means that turnover on their portfolios is usually quite low. Often, there is no obvious catalyst, but improved fundamentals, an influx of new management, reduced competition or recognition by the market that it has overlooked the company’s growth potential may trigger a re-rating.

TMPL has the flexibility to invest up to 30% of its portfolio overseas and the managers will take advantage of this in areas where the UK market is underrepresented or does not offer sufficient diversification.

Asset allocation

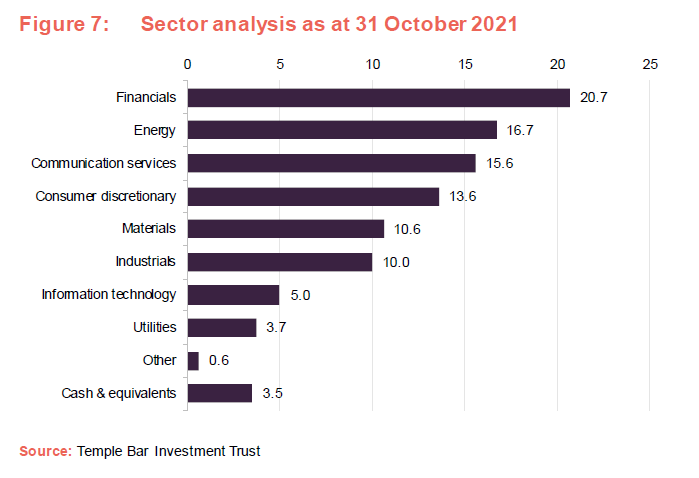

TMPL’s portfolio continues to be weighted towards energy, materials and financials. The biggest change since we last published (using data as at end March 2021) is increased exposure to the energy sector and reduced exposure to consumer staples and healthcare.

10-largest equity positions

Since we last published (using data as at end March 2021) ITV and Dixons Carphone have dropped out of the list of 10-largest holdings to be replaced by TotalEnergies and WPP. Whilst the ranking of stocks may have changed and some positions may have been added to on weakness or trimmed on profit-taking, RWC’s UK’s equity income portfolios tend to be fairly stable.

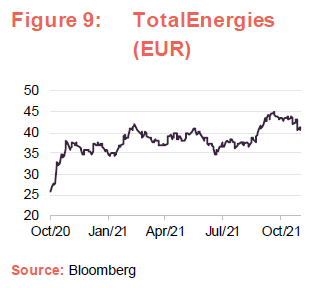

TotalEnergies

TotalEnergies is a leading global producer of liquified natural gas (LNG). Soaring LNG prices, following strong demand from Asia and the Middle East, are helping to drive a significant EBITDA uplift – up 76% year-on-year for the nine months ended 30 September 2021. Its cash flow from operations was 2.1x higher. Dividends are running at €0.66 per quarter and it is also buying back its shares. Cash is also being used to pay down debt and invest in its renewables business.

TotalEnergies has committed itself to net zero carbon emissions by 2050 and has set milestones for the amount of renewable energy generating capacity it hopes to achieve along the way – 25GW in 2025 and 100GW by 2030. Recent renewables projects include wind in Scotland, offshore floating wind in the US and France, a stake in an electric vehicle (EV) battery project (alongside Mercedes Benz and Stellantis) and EV charging stations in Europe and China. TotalEnergies is also investing in green hydrogen projects.

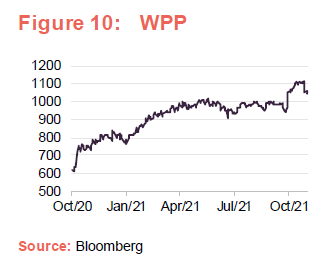

WPP

Communications, advertising and PR conglomerate WPP has seen a fairly steady recovery in its share price since the COVID-related panic in March last year. The business is recovering well from last year and revenue is running 2.6% ahead of 2019 levels. The company is targeting £600m of share buybacks over 2021 while also reducing its debt (down to £1.6bn at end September, £1bn lower than a year earlier).

The other oil majors – BP…

The article that we referred to on page 3 also sets out the managers’ buy case for selected stocks in the energy sector. They highlight BP, where management say an oil price of $70 equates to earnings of 73 cents per share. In addition to annual share buybacks of about $4bn, BP is targeting dividend growth of 4% per year (as is Shell, having increased its dividend by 38% in Q2). The managers point out that BP could return more than 55% of its market cap to investors in buybacks and dividends by 2025.

… and Shell

Shell has been attracting headlines for its plan to relocate its head office to the UK, abandoning its dual share structure. The company has also committed to halve its carbon emissions by 2030. The managers voted against the approval of Shell’s Energy Transition Strategy in May 2021, saying that they do not believe it to be ambitious enough.

The managers have also highlighted activist hedge fund Third Point’s theory that Shell’s energy transition businesses account for the entirety of Shell’s stock market value (based on a 10x multiple for $25bn of attributable EBITDA), leaving its upstream, refining and chemicals businesses, which account for 60% of profits, ‘in for free’. Third Point wants to break the company up to unlock value. Shell dismisses the idea on the basis that the cash flow from the legacy businesses is needed to fund its transition.

Higher gas and oil prices are driving substantial increases in cash flow, which is helping to repay debt.

Vodafone

The managers note that stripping out the attributable value of Vodafone’s listed subsidiaries (Vantage, Vodacom, Safaricom, Vodafone Idea and Indus Towers) leaves the remaining business valued on about 4x EV/EBITDA and a 25% free cash flow yield.

Performance

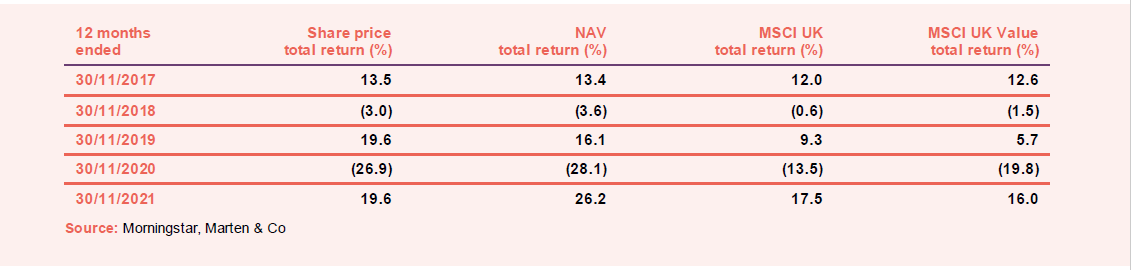

To some extent, RWC’s appointment with effect from 1 November 2020 renders an analysis of TMPL’s performance prior to that date redundant. However, for completeness, we have included our standard five-year chart in this note. Our initiation note contained some data on the performance of RWC prior to its appointment (see Figure 1 of that note).

The positive news about the efficacy of vaccines in November 2020 drove a sharp and significant rotation from growth sectors to value sectors, with mining, energy and banks doing particularly well. The managers say, however, that prior to November 2020 there were many stocks trading on ‘ridiculous’ valuations. They single out NatWest, for example, which, despite significant success in cleaning up its balance sheet, strengthening reserves and taking out costs, was trading at the same level that it had been on in 2008 in the wake of the global financial crisis. The managers think it is capable of achieving earnings per share of 25p, which compares to a current share price of 220p.

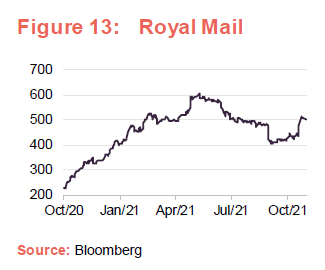

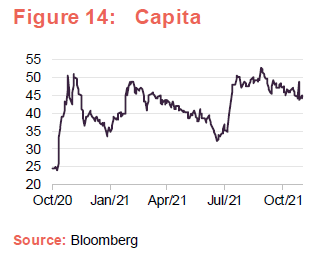

The managers highlight a number of stocks that have contributed to TMPL’s improved performance, including Royal Mail, Capita and Marks & Spencer.

Royal Mail

We have discussed Royal Mail in previous notes. However, the interesting thing is that, despite significant share price appreciation from the stock since RWC took on TMPL, the managers still think that there is more to go for. The managers report that Royal Mail’s European parcels business GLS is expected to make operating profits of €500m in 2023/24. They value that on 10x which works out at about £4.3bn. Royal Mail has a market cap of about £5bn and net debt (at end September 2021) of £540m. That suggests a value for the UK business of about £1.2bn, but the UK parcels business is generating as much cash as the European business.

In its recent half-year results, the company reported a sharp recovery in the profitability of its business. A relaxation of COVID restrictions meant that parcel volumes are lower than last year, but there has still been a 33% uplift in UK parcel volumes versus the first half of its 2019/20 financial year. The board felt confident enough to announce a £200m special dividend payable in January 2022 alongside a £200m share buyback.

Capita

Capita managed to return to profitability over the first half of 2021 on revenues barely changed from the previous year. Stronger free cash flow is supporting a reduction in Capita’s net debt. The group is also shedding non-core businesses and cutting costs. The share price has improved since November 2020 but is still less than a third of its pre-COVID level.

It is some years since Capita paid a dividend, and for the moment, its focus is on reducing and refinancing its debt.

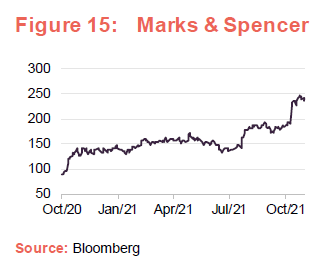

Marks & Spencer

The managers believe that many investors had written off Marks and Spencer’s clothing division as a business in terminal decline and were underestimating the potential of the food division. They say that new management has reinvigorated the business and they highlight the success of the company’s online retail effort, which now accounts for more than 40% of sales. The acquisition of Ocado also transformed its online food/groceries offering.

The share price has risen following strong results. At its half-year stage (covering the 26 weeks ended 2 October 2021), revenue, profits and cash flow were much higher than the equivalent COVID-hit prior year, and up on the previous year too. It is targeting £500m of profit before tax for the full year, ahead of expectations. The ambition is to restore the group’s investment grade credit rating and think about reintroducing dividends, possibly in the next financial year.

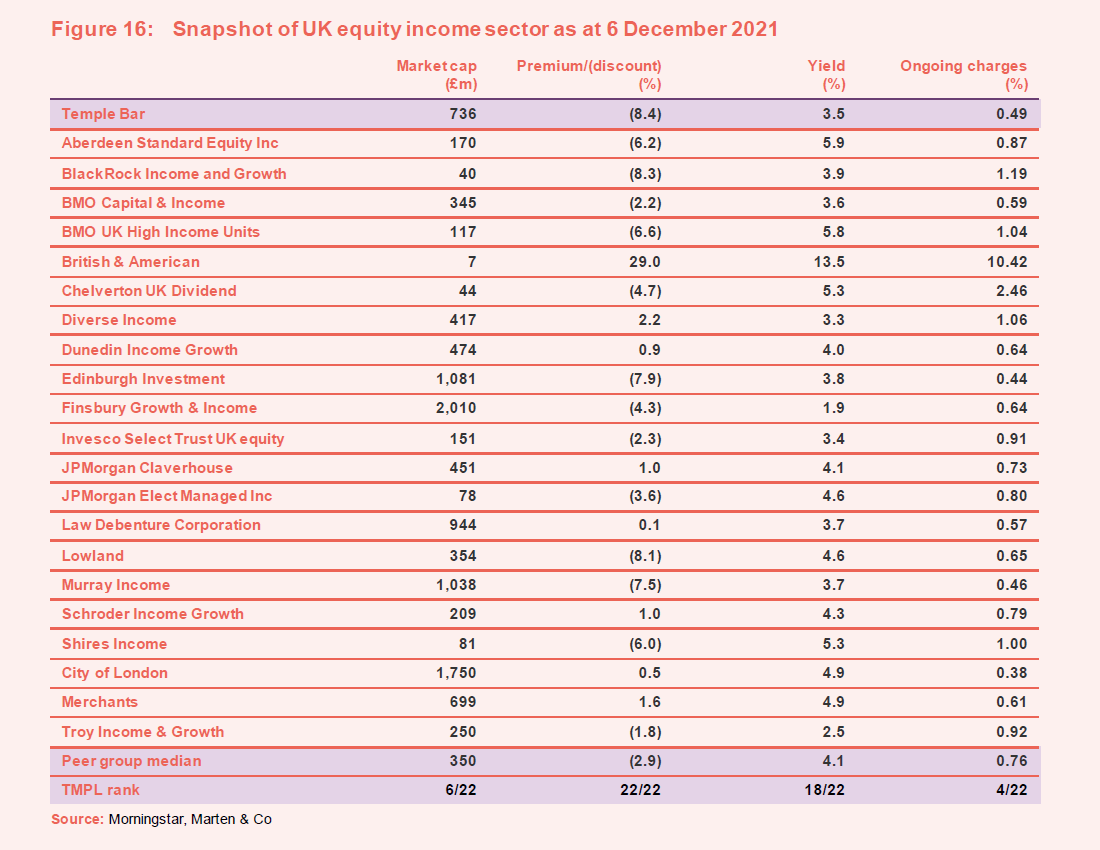

Peer group

TMPL is one of 22 funds in the AIC’s UK equity income sector.

TMPL is one of the larger funds in its peer group and this is a factor in its extremely competitive ongoing charges ratio, which is one of the lowest in the sector. Discounts have widened out across the sector since we last wrote. However, TMPL’s is now the widest in the sector, which seems unjustified to us. It may be though that TMPL’s dividend yield, which is now towards the lower end of the peer group ranking, affects its rating.

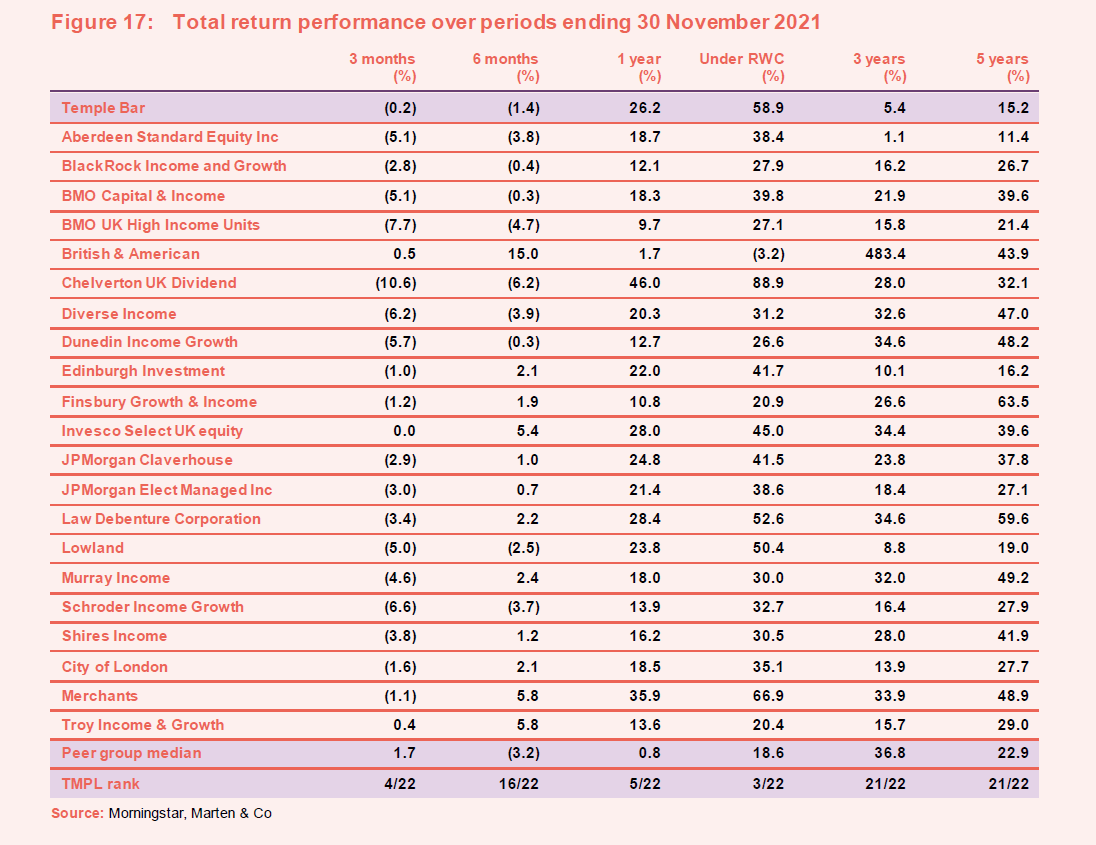

TMPL’s long-term performance numbers are very poor. However, the figures improved dramatically following RWC’s appointment and, while the six-month numbers reflect the pause in the value rally from April onwards, the three-month figures remain encouraging.

Dividend

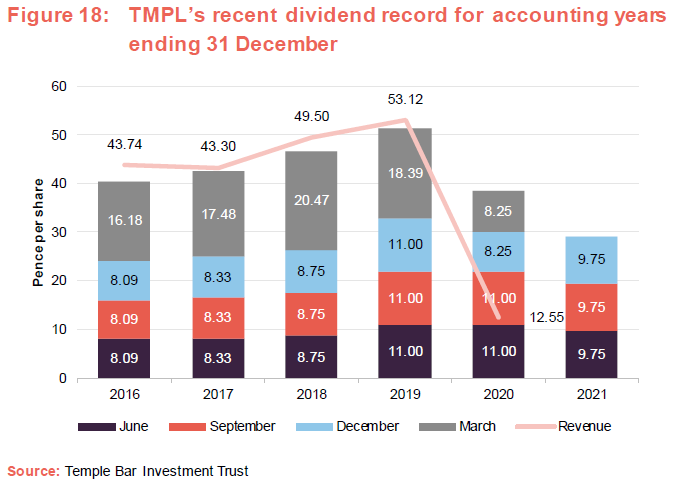

As we discussed in our initiation note, the board and RWC felt that TMPL’s dividend needed to be reset to a more sustainable level. Accordingly, the December and March dividends were set at 8.25p, bringing total dividends for 2020 to 38.5p. For the 2021 accounting year, the dividends have been running at a rate of 9.75p per quarter, implying a total for the year of at least 39p, a modest increase on 2020.

However, we should stress that the amount of the fourth quarter’s dividend has not yet been announced.

As is clear from Figure 18, the revenue per share for the 2020 accounting year fell well short of the dividend paid, and the balance was met from revenue reserves. At 30 June 2021, the trust’s revenue reserve stood at just over £10m, equivalent to 15.1p per share. In addition, the company had distributable realised capital reserves of £547,405,000 at 31 December 2020 (no figure for 30 June 2021 is available).

Prospects for the trust’s revenue account are good

The lifting of curbs on dividends and buybacks by banks, some over-cautious dividend cuts and suspensions when the crisis first hit, and fast-recovering earnings in many stocks in the portfolio are translating into high dividend cover/excess capital in many companies.

The managers think that this presages some decent revenue growth for TMPL’s portfolio. However, they expect that many boards will be cautious about raising dividends too quickly.

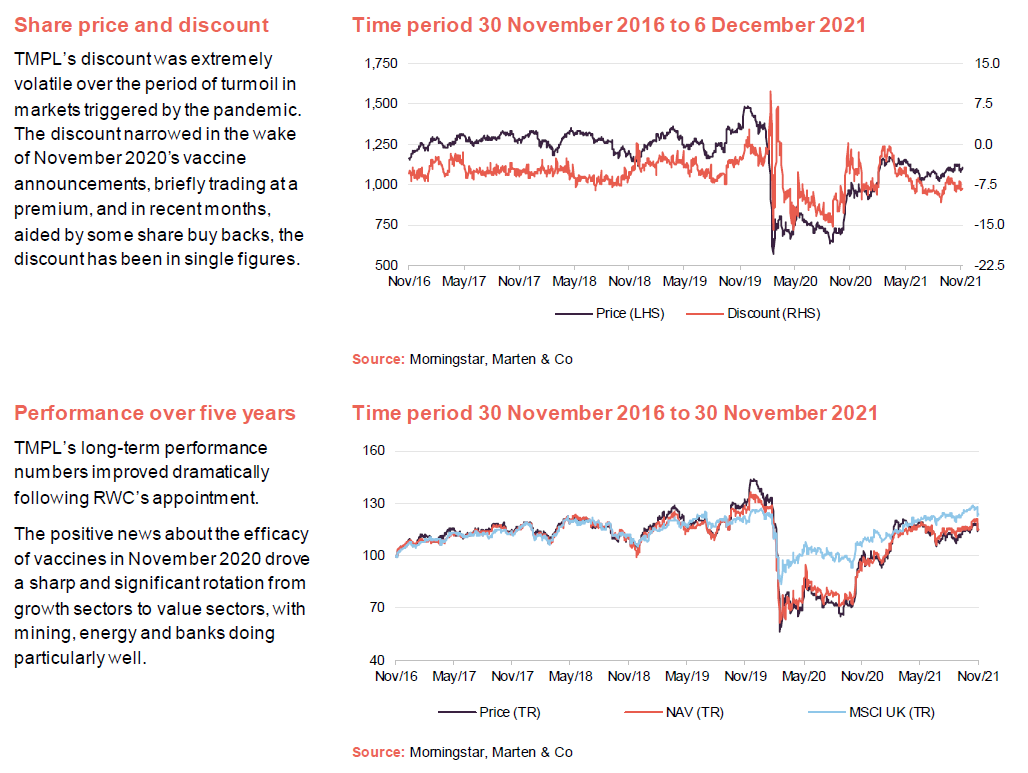

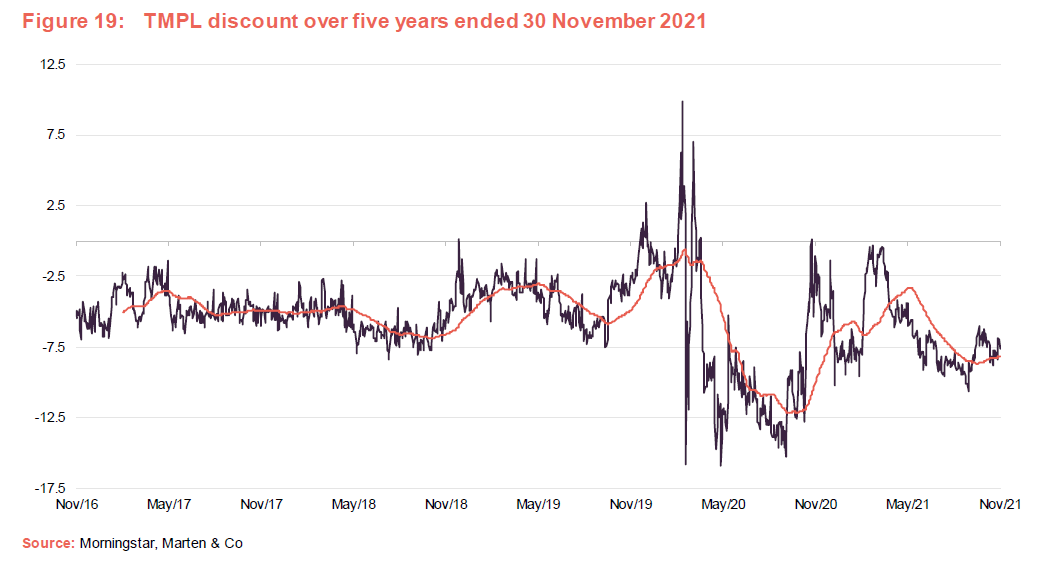

Discount

TMPL’s discount was extremely volatile over the period of turmoil in markets triggered by the pandemic. The discount narrowed in the wake of November’s vaccine announcements, briefly trading at a premium, and in recent months, aided by some share buy backs, the discount has been in single figures.

Over the 12 months ended 30 November 2021, TMPL’s shares traded between a 10.7% and a 0.3% discount. The average discount over that period was 6.4%.

At 6 December 2021, TMPL was trading at a discount of 8.4%. This seems unjustified to us and, aided by the share buybacks, we may see that narrow in coming months.

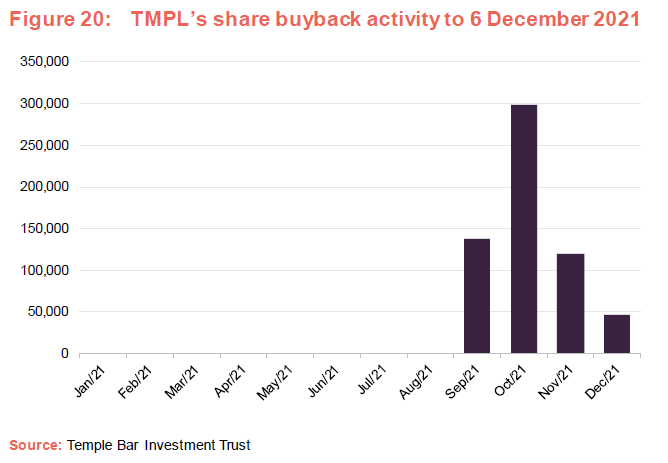

At each annual general meeting (AGM), the board asks shareholders for permission to buy back and issue shares within the usual parameters. Repurchased shares are held in treasury. At the AGM in May 2021, shareholders granted the board permission to repurchase up to 10,024,227 shares. In practice, this authority was not used until 29 September 2021, when the board gave direction to the broker (Cenkos Securities) to repurchase shares within certain parameters. Figure 20 shows the pattern of buybacks.

Fees and costs

RWC’s management fee is calculated as 0.35% of net assets. However, to offset the costs that the trust incurred in connection with its appointment and in recognition that the previous manager’s contract was not terminated until 20 April 2021, RWC did not charge a fee until 30 June 2021. There is no performance fee.

RWC’s appointment was for an initial period of 18 months, following which the contract can be terminated on six months’ notice.

On 30 October 2020, TMPL appointed BNYM to act as its custodian and depositary, entered into a fund administration agreement with LAFA and appointed Company Matters as its new company secretary.

At 30 June 2021, TMPL’s ongoing charges were calculated at 0.42%. However, this reflects a period where there was no management fee for two months. An adjusted ongoing chares ratio, factoring in a more normal level of management charges, gives a figure of 0.49%.

Capital structure

At 6 December 2021, TMPL had 66,872,765 ordinary shares in issue of which 601,336 were held in treasury. The number of shares with voting rights on that date was 66,271,429.

TMPL has a £50m 4.05% private placement loan which is repayable on 3 September 2028, and a £25m 2.99% private placement loan which is repayable on 24 October 2047. The two loans are secured by a floating charge over the assets of the company.

Management team

Nick Purves joined RWC in August 2010 from Schroders, where he was a senior portfolio manager with responsibility for both Institutional Specialist Value Funds and the Schroder Income Fund and Income Maximiser Fund, together with Ian Lance. He worked at Schroders for 16 years, having moved from KMPG, where he qualified as a chartered accountant.

Ian has 30 years of experience in fund management and started working with Nick at Schroders in 2007 before joining RWC in August 2010. While at Schroders, he was a senior portfolio manager, managing the Institutional Specialist Value Funds, the Schroder Income Fund and Income Maximiser Fund, together with Nick. Previously, Ian was the head of European equities and director of research at Citigroup Asset Management and head of global research at Gartmore.

Board

TMPL’s board comprises four non-executive directors, all of whom are independent of the manager, and who do not sit together on other boards. Each of the directors was re-elected at the AGM on 30 March 2021. There is a good spread of experience and length of service within the board.

The longest serving director is the chairman, Arthur Copple, who has been a director for over nine years. The board does not believe that long service should automatically mean that a director should be considered as non-independent. However, in recognition of the AIC Code of Corporate Governance, the board has agreed that a director will ordinarily serve on the board for a maximum of nine years. The board felt that, given the significant change undergone by the company in recent times, it wanted the chairman to stay on for two more years. We believe that a new director will be appointed in coming months and the chairman will likely step down at the AGM in May 2022.

The board has said that its fees will be reviewed in the autumn of 2021 and any change will likely be announced in next year’s annual report.

Arthur Copple

Arthur has specialised in the investment company sector for over 30 years. He was a partner at Kitcat & Aitken, an executive director of Smith New Court Plc and a managing director of Merrill Lynch. He is currently a director of Montanaro UK Smaller Companies Investment Trust Plc and The University of Brighton Academies Trust.

Lesley Sherratt

Lesley was formerly investment director for the Save & Prosper and Fleming Flagship range of funds, and chief executive officer and chief investment officer of Ark Asset Management Ltd. She has over 20 years’ experience investing in the financial sector, including investment trusts, and served as a director and chair of US Small Companies Investment Trust. She is currently a director of a private foundation, a trustee of the Medical Research Foundation and the Global Alliance for Chronic Diseases, she lectures in global business ethics at King‘s College London and is the author of ‘Can Microfinance Work? How to Improve its Ethical Balance and Effectiveness‘.

Richard Wyatt

Richard is a former group managing director at Schroders, Lazard and a vice chairman at Rothschild. He was chairman of the media agency Engine Group and served on the Regulatory Decisions Committee of the FSA (now the FCA). He is currently chairman of Loudwater Partners Limited and a director of a number of other companies.

Shefaly Yogendra

Shefaly Yogendra, PhD was appointed a director in 2019. She was most recently the COO of Ditto AI, a symbolic AI startup. Shefaly built her career in corporate venturing in the technology industry, followed by strategy advisory to investors, regulators and leaders of operating companies on strategic investment in emergent and regulated technologies. She focuses on digital and tech leadership and governance, organisational growth, risk, and decision-making. She is an independent governor of London Metropolitan University, and a non-executive director on the board of the LSE-listed JP Morgan US Smaller Companies Investment Trust Plc. She was listed among the “100 Women To Watch” in the 2016 edition of the Female FTSE Board Report.

Previous publications

QuotedData has published two notes on TMPL. You can read these by clicking the links in the table below or by visiting our website.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Temple Bar Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.