Happy birthday to ya!

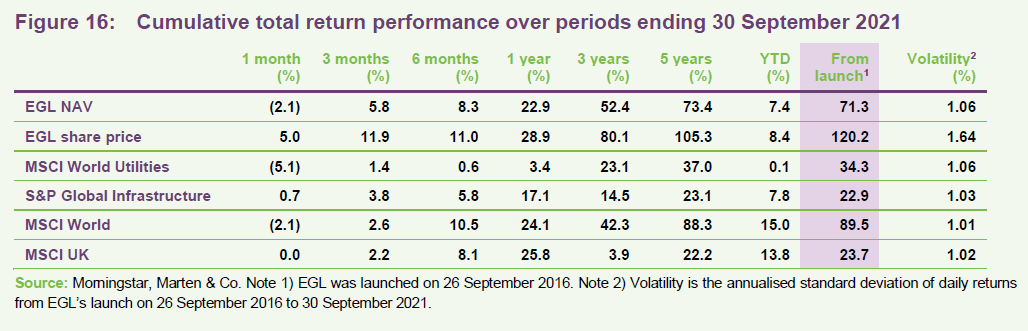

Ecofin Global Utilities and Infrastructure Trust (EGL) has just had its fifth birthday. As at end September 2021, since its launch, EGL had provided NAV and share price total returns of 11.3% and 17.1% per annum respectively (cumulative returns of 71.3% and 120.2% in just over five years); and has outperformed global utilities YTD, during what the manager thinks has been a challenging period. EGL has benefitted from a sustained narrowing of its discount, over the last three years, allowing it to grow to the benefit of all shareholders.

The manager remains excited about the growth prospects of the companies in EGL’s portfolio, driven by the world’s need to decarbonise, and the attractive valuations these can be acquired at. He believes that the future remains bright.

Developed markets utilities and other economic infrastructure exposure

EGL seeks to provide a high, secure dividend yield and to realise long‐term growth, while taking care to preserve shareholders’ capital. It invests principally in the equity of utility and infrastructure companies which are listed on recognised stock exchanges in Europe, North America and other developed OECD countries. It targets a dividend yield of 4% per annum on its net assets, paid quarterly, and can use gearing and distributable reserves to achieve this.

Market outlook and valuations update

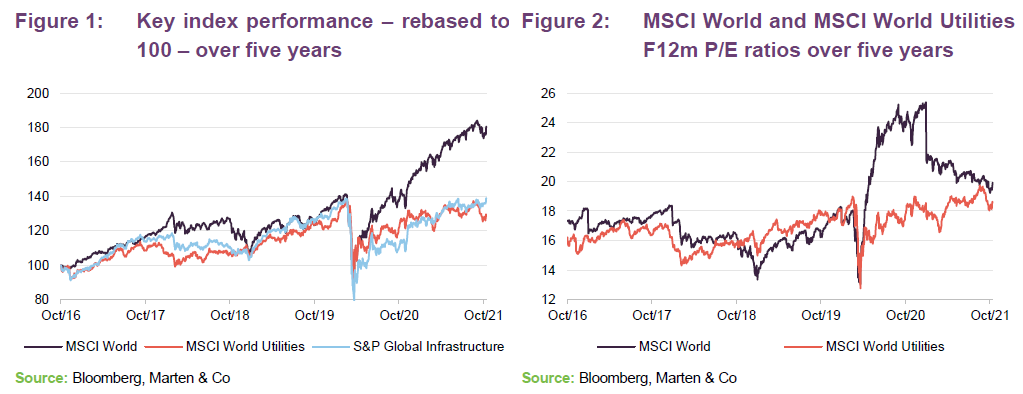

As we explore in greater detail in the performance section on page 15, EGL has generated substantial outperformance of both the MSCI World Utilities Index and the S&P Global Infrastructure Index over the year ended 30 September 2021 and came close to matching the MSCI World Index. However, the utilities sector has lagged the global index by a substantial margin over that period. EGL’s manager, Jean-Hugues de Lamaze think that this presents an ongoing opportunity.

EGL’s sectors are utilities (power, water, environmental services) and other economic infrastructure (transportation services). As financial markets collapsed last year, governments and monetary authorities pumped considerable stimulus and liquidity into markets and economies. Markets rebounded strongly. Against this backdrop, global utilities earnings were resilient and their valuation multiples remained stable relative to history. However, the same could not be said for global equities more broadly. The F12m P/E ratio for the MSCI World rocketed, and whilst a recovery in their earnings has seen these companies grow back into their valuations, global equities are still more highly valued on this basis relative to their pre-pandemic levels, while utilities continue to look cheap by comparison.

Over 2021 utilities and infrastructure appear to have moved in and out of favour as markets have shifted their focus between cyclicals and value stocks, or defensive and growth stocks, as the outlook for re-opening has improved, or investor uncertainty has been raised by the prospect of new variants or inflationary concerns.

Jean-Hugues thinks that utilities and infrastructure sectors remain attractively valued given their long-term structural growth prospects. He also points out that they are now cheaper than they were immediately prior to the crisis and, on relative yield terms, utilities continue to look attractive to him on a long-term basis.

Manager’s view

Another interesting year

Jean-Hugues observes that 2021 has been another interesting year that has seen marked shifts in sentiment towards and away from EGL’s primary areas of investment. He highlights the three main drivers as being:

• shifting inflation expectations, which has given rise to movements in the yield curve;

• rising power prices, driven by rising commodity prices, rising carbon prices and scarcity of supply; and

• M&A activity across EGL’s investment universe.

He comments that, overall, the market has been very ‘risk-on’ this year, reflecting the re-opening of economies. However, the utilities space has a lot of exposure to renewables, and generalist investors are sceptical of these at the moment.

Steepening yield curve

Jean-Hugues says that in the first quarter of 2021, fears that inflation may start to increase led to a modest steepening of the yield curve, partly driven by the election of Joe Biden as President in the US, and his spending agenda. Rising interest rates are generally considered to be negative for utilities and infrastructure names, which tend to have significant levels of long-term debt in their capital structures. This change in sentiment put downward pressure on utilities and infrastructure names although, as we have discussed in previous notes, the cost of such interest rate rises can often be passed through to the customer, often with a lag, and so the picture is much more mixed.

Jean-Hugues comments that whilst it affected their share prices, the yield curve shift had minimal impact on the underlying operations of these companies. The integrated utilities were more affected by this than most, but the impact on EGL has been limited as the manager shifted some exposure away from pure regulated names given we have likely reached the lows on longer term yields. Moreover, where EGL owns pure regulated names, the manager has focused on those that have inflation pass throughs in their formulas (the UK and Italy). Reflecting this, the manager exited REN (which owns the Portuguese electricity and gas grids) and reinvested the proceeds in Terna (which operates Italy’s transmission grid). This has been a very profitable trade for EGL.

Commodity and carbon price pressure

Moving into the second quarter of 2021, inflationary concerns seemed to subside (markets generally taking the view that this was a short-term phenomenon) and the yield curve flattened in response. Utilities did not react immediately, but rallied somewhat in July and August. Although, in recent days the yield curve has started to steepen again as supply chain bottlenecks and rising energy prices have reinforced inflation fears.

Upswing in M&A activity in EGL’s sectors

This year also showed a sharp rally in commodity prices (for example natural gas and coal) that, coupled with the cost of CO2 certificates also increasing dramatically and the phase-outs of coal and nuclear in many markets, has led to a dramatic increase in power prices worldwide. The UK, which has one of the thinnest reserve margins in Europe, has seen wholesale power prices double since January.

Whilst this environment has been difficult for conventional generators, it has been a boon to profitability for the renewables generators, with the benefits of the increased power price largely falling through to the bottom line.

Jean-Hugues says that with the world obsessed by decarbonisation, the consequent switch to renewables – with their inherent intermittency – coupled with battery technology that is not yet sufficiently developed to allow these to provide baseload power means that the market will be prone to spikes in pricing for the next few years.

He says that significantly higher power prices will flow through to utilities’ profits but not to the extent they once did as business models have been de-risked – merchant (conventional generation) has shrunk as a percent of EBITDA while renewables and power grids businesses have grown to form the majority of earnings and cashflows. In terms of PPAs in Europe, the longest contracts are in the hands of the largest renewables developers which are the big listed names in EGL’s portfolio. These have underperformed this year due to concerns about renewables developers’ ability to pass through higher materials costs to PPA prices. Jean-Hugues says that their channel-checks are reassuring on this point and that contract periods are getting longer in Europe.

Chinese decarbonisation theme continues

As discussed in our December 2020 note (see page 6 of that note), China is aggressively decarbonising, and Jean-Hugues added two Chinese wind operators (China Longyuan Power Company and China Suntien Green Energy) that provide exposure to this theme. Combined, the two holdings account for about 6% of EGL’s portfolio. Jean-Hugues says that both companies offer very good growth prospects.

The Chinese government is evolving its approach and wants to present aggressive decarbonisation plans (full decarbonisation by 2060) which would be fairly astonishing given China’s current reliance on coal. Jean-Hugues expects the political and regulatory context to be lenient toward wind developers and that valuations for EGL’s two holdings are a fraction of their international peers. Risk management is of course crucial for these positions. Jean-Hugues says that the Biden administration in the US has been highly vocal about its climate-related reforms and he believes that the Chinese do not want to be seen to be left behind. He thinks that whilst the Chinese government will not offer subsidies for renewables generators as has been seen in the west, the political risk has reduced and they will not find their profitability under regulatory attack.

Asset allocation

Comparing EGL’s exposures at the end of September 2021 and the end of November 2020 (the most recently-available data when we last published), there have not been any significant changes in the geographic allocations.

The allocation to renewables has increased recently because the Chinese holdings have performed extremely strongly and some other holdings were increased over the summer after relative price weakness. The allocation to renewables has increased by five percentage points to 30%, with pure regulated utilities falling by three percentage points to 20%, integrated utilities falling by two percentage points to 36% and transportation holding steady at 14%. The number of holdings as at the end of September 2021 was 45, an increase of two relative to when we last published.

Portfolio activity

Since we last published, EGL’s manager has:

• been increasing exposure to business models with inflation pass-throughs (for example, exchanging Redes Energeticas Nacionais (REN), which owns both of the national electricity and gas grids in Portugal, for Terna, which operates Italy’s transmission grid);

• been increasing exposure to names with above-average exposure to commodity/carbon price strength (for example Drax and Uniper), and transportation infrastructure (Atlantia);

• sold A2A after strong gains in a relatively short period;

• sold or reduced lower conviction names to make room for some new holdings (American Electric Power and AES Corporation).

EGL also participated in Acciona’s IPO, added to the US renewables exposure, re-initiated a position in Neoen and added PPL Corporation, all of which are discussed below.

Jean-Hugues says that, despite economies re-opening, he has been very reluctant to add airports, but is looking to play this and transport more generally in other ways. For example, by:

• adding to Ferrovial (see top 10 holdings section below);

• establishing a ‘watch list’ position in Atlantia, which has exposure to both airports and toll roads. It derated heavily after the collapse of The Morandi Bridge in Genoa, where it was the concession holder, but is now repositioning itself; and

• adding to Atlas Arteria, an Australian company with exposure to French toll roads that we discussed in detail in our October 2019 note. The company, which was previously known as Macquarie Atlas Roads, was created out of the reorganisation of Macquarie Infrastructure Group (a private equity vehicle managed by Macquarie Bank), into two separate ASX-listed toll road groups in 2010. Jean-Hugues says that reflecting its history, it is off-radar for most investors and therefore under-appreciated by the market.

Acciona Energia – market did not appreciate wind portfolio value at IPO

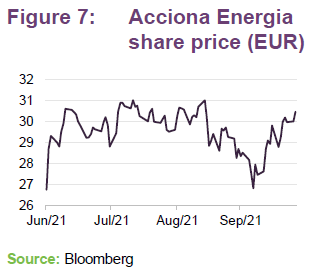

Acciona Energia (acciona-energia.com) is the renewable energy arm of the Spanish multinational conglomerate Acciona, (acciona.com). Following its IPO, the company listed on the Bolsa de Madrid at the end of June 2021 at €26.73 per share, which was towards the bottom end of its price range.

Jean-Hugues says that this business has a high-quality portfolio of renewable energy assets (it built some of the first Spanish wind farms, for example) but that its previous ownership structure meant that it was not well understood by the market. However, he says that the IPO has given rise to a material change in direction at that, by participating in the IPO, EGL was able to get an allocation at a time when the market did not appreciate the value of the renewables portfolio. As is illustrated in Figure 7, Acciona Energia’s share price is up 14% since listing. Despite this share price appreciation, Jean-Hugues says that he still has full conviction in the stock and thinks it is very attractively valued.

Jean-Hugues thinks that the low valuation is in part due to regulatory risk of the Spanish government, given its previous attempts to roll back on its commitments to subsidies for renewables. However, its exposure to Spain has been coming down over time and it has increased investment in the US and Australia. He acknowledges that there have been issues in other areas of the broader Acciona business, but says that execution within the renewables segment has been very good, that it has a strong balance sheet having been recapitalised prior to the IPO and that earnings are growing quickly.

US portfolio reshuffled

Jean-Hugues says that his ambition has been to grow EGL’s exposure to the US as he sees the potential for US utilities to pivot away from traditional thermal sources of generation towards renewables in the way that has occurred in Europe during the last decade. He adds that in Europe, conventional power generation has moved from around 50% of utilities’ cash flows in the late 2000s to around 10% today. Meanwhile, renewable power generation, which accounted for less than 10% a decade ago now represents more than 30% of cash flows. The proportion of regulated networks has also increased. Overall, the industry has become more contracted and predictable. Jean-Hugues expects to see a similar phenomenon in the US, aided by Biden’s climate plan, which is accelerating renewable development.

Recently, Jean-Hugues has reshuffled EGL’s portfolio, reallocating into names that are better positioned and have meaningful low-carbon ambitions. Holdings in FirstEnergy, Edison International and Algonquin Power & Utilities have been exited.

Additions to EGL’s portfolio include: DTE Energy (a Detroit-based energy company with interests in electricity and gas), American Electric Power (one of the largest power generators and distributors in the US, serving Ohio, Michigan, Indiana and other midwestern states) and Alliant Energy (an integrated utility serving the Mid-West, primarily Wisconsin and Iowa). Jean-Hugues says that the regulatory environment is supportive of regulated growth in this part of the US. He also comments that Alliant Energy has been well rewarded for burying cables, which is a relatively inexpensive, and has upgraded its targets for growing its renewables portfolio.

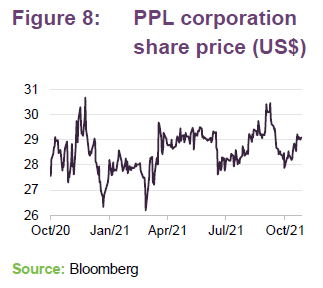

PPL Corporation – added on expectation of sale of its UK electricity distribution asset should spark a revaluation

PPL Corporation (pplweb.com) is a regulated utility operating in Pennsylvania, Kentucky and the UK. It is a FORTUNE 500 company and one of the largest utility companies in the US. The company, which has more than 2.5m utility customers and around 7,500 megawatts of regulated generation capacity, was added to EGL’s portfolio earlier this year on the manager’s expectation that the sale of its UK electricity distribution business, Western Power Distribution (westernpower.co.uk), would achieve a price tag in excess of market consensus expectations. EGL’s manager felt that such a sale should then lead to a revaluation for PPL’s shares. (Note: Western Power Distribution is the electricity distribution network operator for the Midlands, South Wales and the South West.)

In March 2021, PPL Corporation and National Grid (see further discussion below) announced an asset swap whereby National Grid is to acquire Western Power Distribution from PPL for $19.4bn in cash (1.7 x rate base), whilst PPL will acquire National Grid’s Rhode Island utility, Narragansett Electric, for $3.8bn plus the assumption of $1.5bn of that business’s debt.

Jean-Hugues says that, in acquiring Narragansett Electric, PPL has secured a prime asset in Rhode Island, which is a new and fast-growing geography for the company. He thinks that this should be very positive for PPL over time.

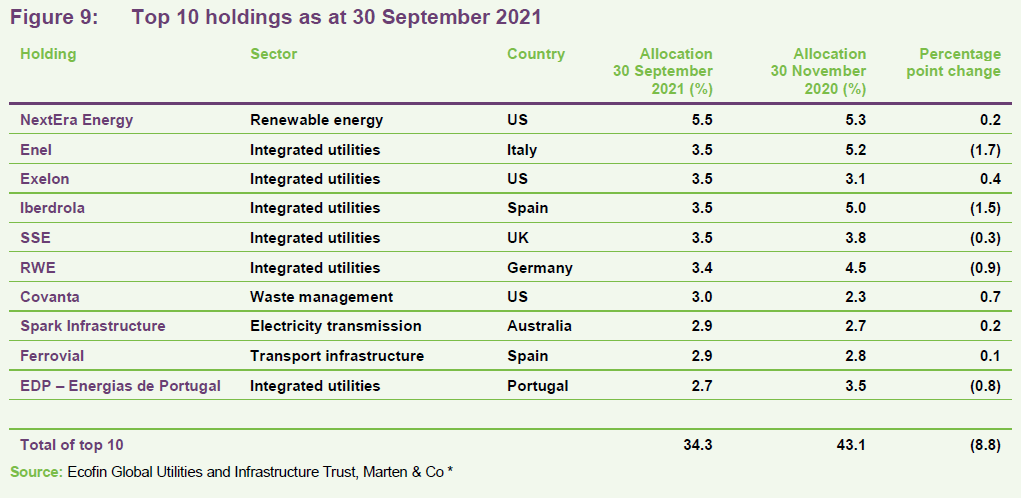

Top 10 holdings

Figure 9 shows EGL’s top 10 holdings as at 30 September 2021 and how these have changed since 30 November 2020 (the most recently-available data when we last published). Names that have moved up into the top 10 are Covanta, Spark Infrastructure and Ferrovial. Names that have moved out of the top 10 are Brookfield Renewables, EDF and National Grid. We discuss some of the more interesting changes in the following pages. Readers interested in other names in the top 10 should see our previous notes, where many of these have been previously discussed. Updates on China Suntien Green Energy, Endesa, EDP and Evergy have been provided in the Appendix – see page 34.

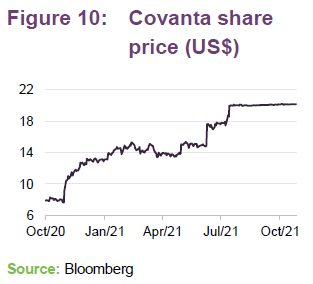

Covanta – take-over bid significantly undervalues waste-to-energy company

US based Covanta (covanta.com) is a leading provider of waste-to-energy services (circa 70% share of the US market) that has long been a constituent of EGL’s portfolio (we first discussed it in our May 2017 initiation note and have followed up a number of times since, most recently in our June 2020 note). The majority of its operations are in the US, but it also has three facilities in Europe and one in China.

Previously, we have noted that Jean-Hugues thinks that Covanta’s facilities are now seen as being part of a long-term sustainable solution to waste management and that it is the only player well-placed to open new facilities (either by expanding existing sites or by using its track record to secure new facilities). Other desirable attributes that EGL’s manager has identified are that Covanta has high revenue visibility (it generates stable cash flows, backed by contracts and hedges on 85% of revenues, and further supported by solid 25% EBITDA margins); low capex requirements as its assets are already established, offers around a 6% dividend yield; and has attractive assets (although these are not without controversy, as proposed new sites tend to create considerable local opposition, which gives Covanta a defensive moat).

Jean-Hugues’s positive view on the stock has since been rewarded as Covanta received a bid from Sweden’s EQT Infrastructure of US$20.25 per share, in cash, on 14 July 2021 (a premium of 37% to the undisturbed price of US$14.86 on 8 June, which was prior to press speculation emerging). The deal, which included the assumption Covanta’s net debt obligations, values the company at US$5.3bn. It was unanimously approved by Covanta’s board and is expected to close by the end of the year. However, EGL’s manager believes that the bid significantly undervalues the company. It has written to Covanta’s board twice to express its dissatisfaction and fully explain its rationale and models. It also voted against the proxy.

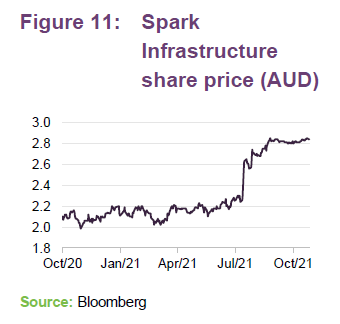

Spark Infrastructure – bid highlights the valuation gap between private and listed infrastructure assets

Spark Infrastructure (sparkinfrastructure.com) is the primary power distribution network company in Australia. Its subsidiaries include SA Power Networks (the sole electricity distributor in the state of South Australia); CitiPower and Powercor (two of the largest electricity distribution networks in Australia that supply power to over 11m homes in Victoria); TransGrid (which owns and operates a high voltage electricity transmission network in New South Wales and the Australian Capital Territory); and Spark Renewables.

Jean-Hugues says that the company has already been growing strongly and that it has a long runway for further growth, due to the significant investment that will be required in Australia’s grid infrastructure, with the expansion of renewable power generation. He says that previously it has been under the radar for many investors, creating a valuation opportunity (he felt that it was under-valued given both the scarcity of its assets and its strong long-term growth potential).

In August 2021, Spark’s board approved a bid from a consortium led by KKR and a Canadian pension fund, the Ontario Teachers’ Pension Plan. Jean-Hugues says that he is happy with the final bid of AUD2.95 per share, which values the company at AUD5.2bn. Jean-Hugues comments that the consortium had to raise its bid twice (from UAD2.64 to AUD2.74 to AUD2.95) to get board approval, which he thinks reflects both the scarcity of the company’s assets as well as the expertise of the management team. Jean-Hugues thinks that there are read-throughs for other Australian names, such as Atlas Arteria, as well as for similar assets in other jurisdictions. He also feels that it underlines that the valuation discrepancy between private and listed infrastructure assets is unsustainable, a topic that we discussed in our December 2020 note, following Ecofin’s white paper on the subject that highlighted that private equity is paying much higher multiples for these assets than they are being valued at by public markets.

Jean-Hugues observes that the Australian market is dominated by superannuation funds and he believes that the combined effects of the above will create incremental momentum to the pricing of these assets, even after the recent good run of performance.

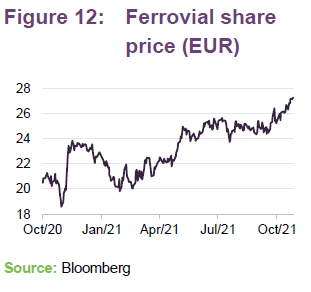

Ferrovial – benefitting as economies re-open

Ferrovial (ferrovial.com) is primarily a transport infrastructure company. It manages 1,474m km of roads in nine countries, and Heathrow, Glasgow, Aberdeen and Southampton airports. It also has a construction company with a strong presence in the transportation sector as well as a services company with operations in the water treatment and electricity sectors, amongst others (the services business continues to be up for sale).

We last discussed Ferrovial in our June 2020 note, where we noted that Jean-Hugues had been gradually expanding the holding on share price weakness. Ferrovial’s toll roads and airports operations were hit by COVID-19 restrictions, with the airports the worst affected, although the impact on its construction activities in Spain were much less affected. We also noted that Ferrovial had a strong balance sheet approaching the crisis, with €1.6bn of free cash outside of its infrastructure assets, which provided it with strong capacity to weather the storm.

Ferrovial is the main shareholder in Heathrow and Jean-Hugues thinks that the UK government looks set to approve the building of a third runway, which will be very positive for the company. He also thinks that the company’s mix of assets, which includes both airports and toll roads assets, is a very good exposure to hold at the current time.

As is illustrated in Figure 12, Ferrovial’s share price received a strong boost during the vaccine rally in November 2020, but retrenched significantly during January 2021 as COVID-related restrictions continued to impact travel in particular. However, since then, it has recovered strongly as vaccine roll-outs have allowed economies to move along a path of re-opening, boosting road traffic and slowly opening up the prospect of increased air travel.

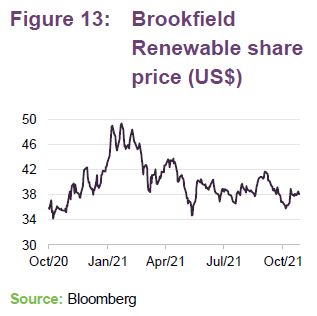

Brookfield Renewable – has not been rewarded for asset sales

Brookfield Renewable Partners (bep.brookfield.com) is a global renewable energy company with an emphasis on North American hydroelectric assets (these account for approximately 64% of its generating portfolio), which we discussed in our December 2020 update note. Following its merger with Terraform Power, which saw Brookfield Renewables Partners (BEP) absorb Terraform Power’s operations, the combined company became one of EGL’s largest holdings. The company provided a strong performance in 2020 and, consequently, was a big driver of the performance of EGL’s portfolio, as well as its allocation to North America, with the manager trimming the position into strength.

More recently, Brookfield has benefitted from rising power prices in the US, although the increase has not been as stark as seen in Europe. However, after a stellar performance for the shares in 2020, the stock suffered as the yield curve steepened earlier in the year, and the decision to sell some assets to Orsted and NextEra Energy Partners (possibly to build a war chest to fund growth or M&A) does not appear to have been well received by the market.

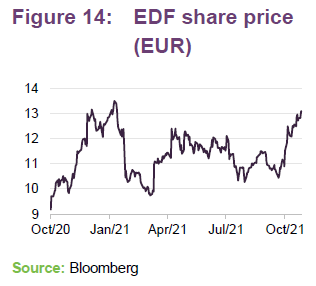

EDF – market’s focus on regulatory dynamics is obscuring substantially improved fundamentals

EDF (www.edf.fr) is a French multinational electric utility company that is largely state-owned. In Our December 2020 note, we explained that this was an opportunistic investment that requires a deep understanding of French politics. EDF operates France’s entire active nuclear generation fleet, which comprises some 58 reactors, across 19 sites, all of which are pressurised water reactors (PWR). The French government has ambitions to reduce France’s dependency on nuclear power but, in 2019, it asked EDF to develop proposals for three new replacement nuclear power stations.

In July 2021, EDF’s share price fell some 10%, bucking the trend and making it the only real detractor to EGL’s performance that month. This occurred when the French government confirmed that a much-anticipated reshuffling of EDF’s structure was unlikely to happen in the near-term. However, this saw some reversion in August as a number of integrated utilities names, EDF included, reported generally strong first half numbers, surprising consensus, giving some upward momentum to share prices in the space, aided by ongoing strength in commodity, power and carbon prices.

Overall, Jean-Hugues thinks that the market’s excessive focus on the regulatory dynamics surrounding EDF is currently preventing its share price from catching up with its substantially improved fundamentals. He thinks this is unsustainable over the longer term, and is happy to hold this position.

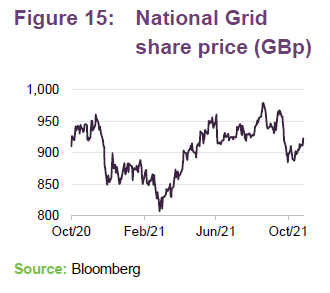

National Grid – PPL asset swap signals positioning for a future based on electrification

National Grid (nationalgrid.com) is another long-term EGL holding. The company owns the high-voltage electricity and high-pressure gas transmission system in England and Wales, and is responsible for balancing supply and demand on the electricity network across Great Britain. It also has a presence in the US where it provides electricity to Massachusetts, upstate New York, Rhode Island and Vermont, and natural gas to customers in New York, Massachusetts and Rhode Island.

As detailed above, National Grid and PPL Corporation announced an asset swap in March 2021 (PPL is selling its UK electricity distribution business to National Grid for $19.4bn in cash, while National Grid has sold its Rhode Island utility, Narragansett Electric, for $3.8bn, with PPL taking on $1.5bn of that business’s debt). Jean-Hugues says that, for National Grid, the deal is a strong signal of its direction of travel and that the company is positioning for a future based on electrification. National Grid has also committed to sell down a majority stake in its UK gas transmission business and to use the proceeds to increase investments on the electric side. The shift in the UK’s generation mix towards renewables requires more investment in the power grid, which should underpin National Grid’s growth, and Jean-Hugues believes that the deal with PPL will be beneficial to the company’s long-term growth.

Performance

Strong long-term performance record

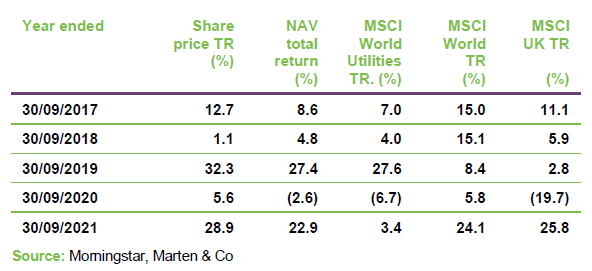

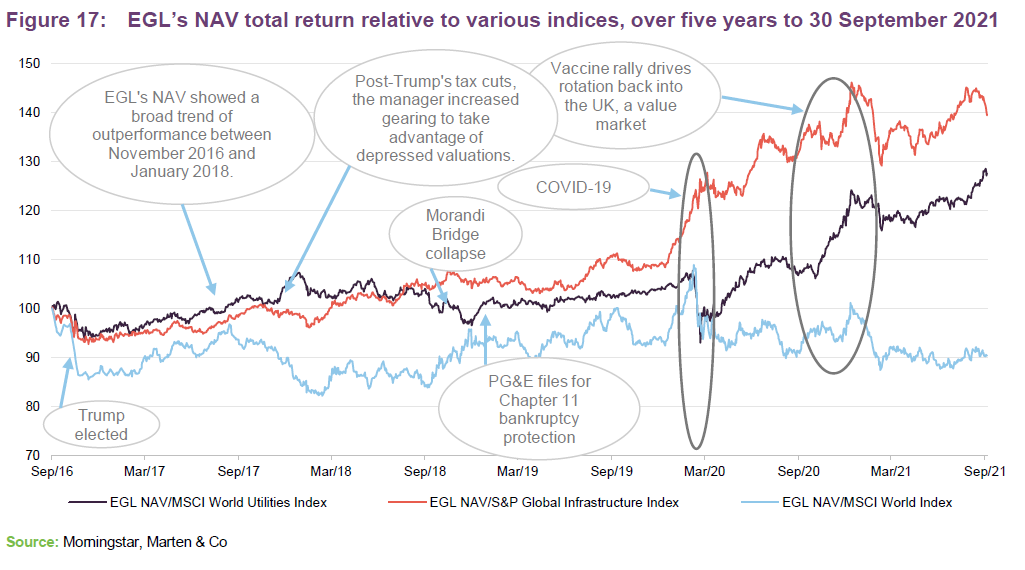

As illustrated in Figure 17, since its launch EGL’s NAV total return has outperformed the return of the MSCI World Utilities Index (EGL has provided more than double the return) and both the S&P Global Infrastructure Index and the MSCI UK indices (in both cases, EGL’s return was just over three times that of the index). Reflecting the marked narrowing of the discount during its life, EGL’s share price total returns are markedly superior to its NAV, even surpassing the return on the broader MSCI World index.

Strong outperformance of MSCI World Utilities Index YTD

As illustrated in Figure 16, EGL has had a very good year so far, with its NAV and share price total returns strongly outperforming the MSCI World Utilities Index, while being broadly in line with the S&P Global Infrastructure Index. YTD, EGL’s NAV total return has underperformed the MSCI World and MSCI UK Indices, arguably reflecting the ongoing rally in global equities more generally as economies have continued to re-open and, in the case of the UK, a reduction in uncertainty relating to Brexit as transition periods come to an end.

Utilities and infrastructure have been amongst the poorer-performing areas within the MSCI World universe this year, despite strong earnings reports and the gradual improvement in operations and prospects for toll road and airports. Although this has seen some reversion more recently as rising commodity prices and carbon prices have given rise to steep increases in power prices, renewables have struggled against a backdrop of rising long-term interest rates and falling longer-term estimates of power prices. EGL’s manager comments that comments that, given the performance of the sector indices this year, stock selection has been highly successful and it is happy with EGL’s performance and positioning.

As highlighted in the section below, a majority of the largest 10 positions in the portfolio this year have been non-index stocks. Stock selection has been successful and Jean-Hugues has utilised the full breadth of EGL’s investment universe in generating returns. He highlights the alpha that had been generated even while the portfolio’s renewables focussed stocks have been out of favour.

Year-to-date performance to 30 September 2021

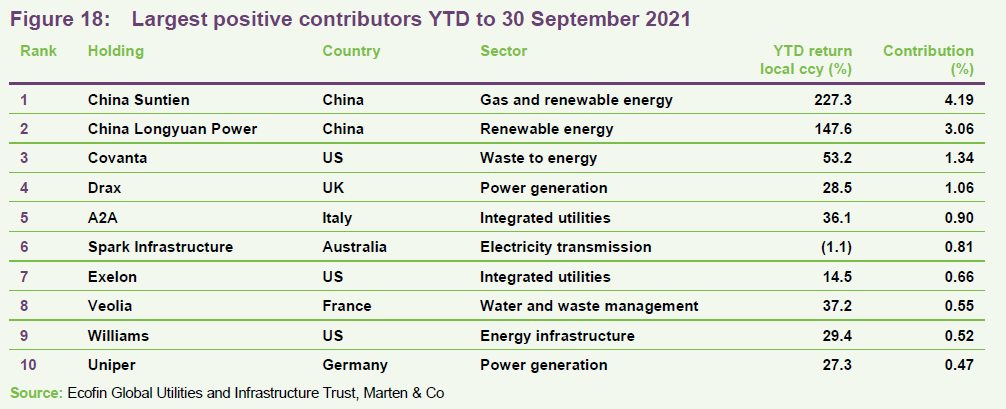

EGL’s manager has kindly supplied us with some performance data for EGL’s largest positive contributors to performance, which has been reproduced in Figure 18.

Strongest positive contributions have come from:

• China Suntien (see page 34), like China Longyuan Power above, has benefitted from rising commodity prices driving power prices higher as well improving sentiment towards Chinese renewables.

• China Longyuan Power, Chinese renewables have seen a resurgence this year, both as a function of higher commodity price and consequently power prices, as well as a marked improvement in sentiment following as the Chinese government has shifted away from trying to trim the returns that renewable companies earn.

• Covanta – as discussed on page 11, this has received a bid from Sweden’s EQT Infrastructure (which EGL’s manager thinks significantly undervalues the company).

• Drax – has benefitted from a robust operational and trading performance in 2021, which was reflected in its recent interim results and a 10% increase in its dividend. The company has reduced its generation emissions by over 90% since 2012, making it one of the lowest carbon intensity power generators in Europe. It also says that it has significantly advanced its plans for bioenergy with carbon capture and storage (BECCS) and could be delivering millions of tonnes of negative emissions by 2030.

• A2A – share price has grown strongly through much of the year, aided by strength in power prices. Jean-Hugues exited the position fully in June after a strong run, rotating the proceeds into better value holdings elsewhere.

• Spark Infrastructure, as discussed on page 12, has benefitted from a bid from a bid from a consortium led by KKR and the Ontario Teachers’ Pension Plan.

• Exelon – the largest regulated electric utility in the US and the largest operator of nuclear power plants in the US, announced plans in February 2021 to split its utility and competitive energy businesses into two publicly-traded companies. The market appears to have welcomed the news, with the share price steadily gaining ground since. Jean-Hugues topped up EGL’s holding in May on the back of short-term weakness and EGL has benefitted since.

• Veolia – the French utility was one of the worst-performing stocks in the utilities space in 2020. EGL benefitted as Jean-Hugues exited a holding in late 2019/early 2020, but he re-initiated a position late in 2020 as he considered that Veolia’s share price had decoupled from fundamentals, providing an attractive entry point, and EGL has been rewarded as the stock has recovered. Jean-Hugues considers that with the integration of Suez, there is a strong outlook for earnings growth.

The largest performance detractors year-to-date have been the large renewables specialists amongst the major utilities (Iberdrola, Brookfield Renewables, Enel, Endesa, EDF, RWE).

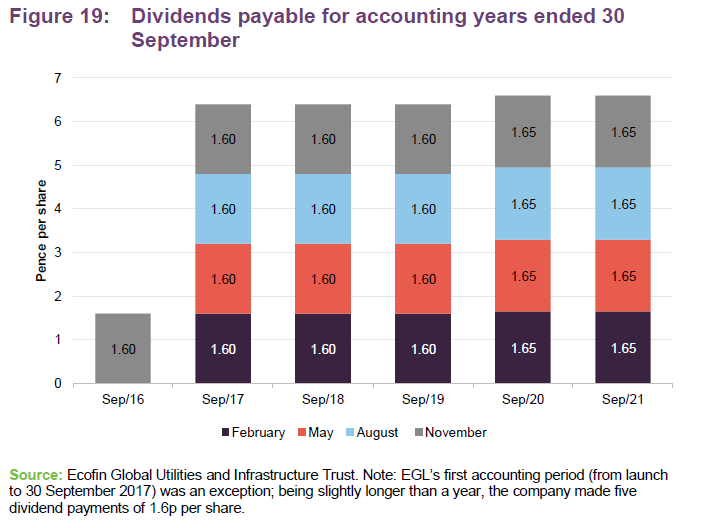

Quarterly dividend payments targeting 4% of NAV per annum

EGL targets a dividend yield of 4% on its net assets and can use gearing and, if necessary, distributable reserves (the result of cancelling its share premium account) to make up any shortfall in its dividend target. For a given financial year, the first interim dividend is paid in February, and the second, third and fourth interim dividends are paid in May, August and November, respectively. Dividends are paid on the last business day of the respective month.

For the year ended 30 September 2021, EGL paid four dividends of 1.65p per share totalling 6.6p matching last year’s figure. For the 2020 year, the 6.6p compared to revenue income of 4.97p equating to dividend cover of 0.75x (2019: revenue income 5.48p per share, sufficient to cover the dividend of 6.4p 0.86x).

Improving dividend cover

The dividend rate was increased slightly just before the pandemic (from 1.6p to 1.65p per quarter). Reflecting to the resilience of dividends in EGL’s sectors, the Board took the decision to maintain the dividend level, even if the cover ratio declined, given the manager’s confidence that any regional pressures (for example, France) would be temporary and the longer-term forecast for income generation from the portfolio was healthy. At the interim stage, the manager reported that it expected a 15% increase in income from investments this year so dividend cover should improve significantly. The chairman said that this should enable a resumption of EGL’s strategy of increasing its dividends.

EGL has said that it is expecting 15% year-on-year revenue growth for the year-ended 30 September 2021, with 7% year-on-year growth for the following financial year. This suggests that, with the current quarterly dividend rate of 1.65p per share, coverage will be in the region of 0.9x for the year ended 30 September 2021, and 1.0x for the following year.

For the year ended 30 September 2021, the total annual dividend of 6.6p for the year is equivalent to a yield of 3.3% on the share price of 202p as at 26 October 2021.

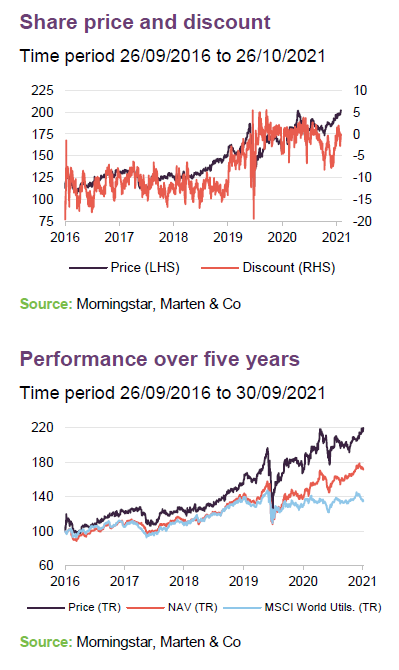

Premium/(discount)

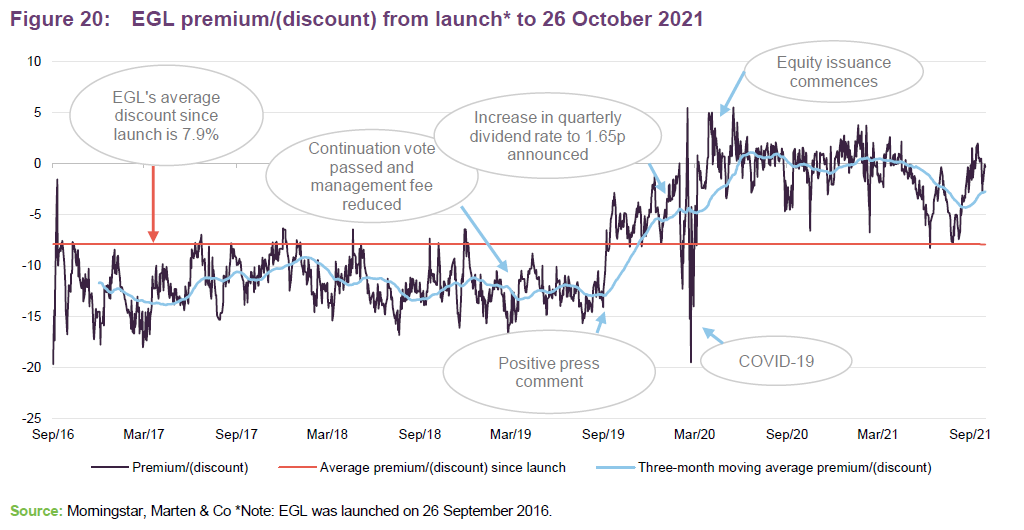

EGL now trades on a structurally tighter discount/sensible premium

Since we published our first note on EGL in May 2017, the discount seemed to be somewhat out of step with the strong NAV performance, to the frustration of both the board and the manager. This was despite efforts by the manager and board to raise the profile of the trust, the continuation vote passing and the implementation of a 25bp reduction in the management fee (this took effect from 5 March 2019 – see page 11 of our April 2019 update note). However, there was a step change in EGL’s premium/discount performance from the end of September 2018.

Three years on, EGL now trades at a much tighter discount and regularly trades at a premium, allowing the trust to regularly issue stock (4.3m shares or 4.3% of its issued share capital since the beginning of the year). All of these shares were issued at a premium to asset value in accordance with EGL’s policy on share issuance. This has the effect of enhancing the NAV for existing shareholders. Expanding the trust could also have the twin benefits of improving liquidity in the shares and lowering the ongoing charges ratio as fixed costs are spread over a wider base.

During the last 12 months, EGL’s shares traded between a discount of 8.3% and a premium of 3.8%, and averaged a 1.2% discount. At 26 October 2021, EGL’s shares were trading at a discount of 0.3%.

Fees and expenses

Management fee

Under the terms of its investment management agreement, Ecofin Advisors Limited is entitled to a management fee of 1% per annum of EGL’s net assets up to £200m, and 0.75% per annum of net assets thereafter. The management fee is calculated and paid quarterly in arrears. There is no performance fee.

Secretarial and administrative services

Prior to 1 April 2021, BNP Paribas Securities Services S.C.A., London branch, provided both administrative and secretarial services to EGL. While it still provides administrative services, Maitland Administration Services Limited has provided company secretarial services to EGL since 1 April 2021 (see page 16 of our October 2018 note for details of the previous fee structure).

Depositary and prime brokerage agreement

Under the terms of EGL’s depositary agreement, Citibank UK limited acts as EGL’s depositary. For these services, it charges EGL a fee of 3.75bps per annum of net assets. The depositary agreement can be terminated by either party on 90 days’ notice. Citigroup Global Markets Limited acts as EGL’s prime broker and custodian. It also provides borrowings to EGL (see page 22).

Allocation of fees and costs

EGL’s investment management fee and finance costs are charged 50% to revenue and 50% to capital. All other costs are charged wholly to revenue. For the year ended 30 September 2020, EGL’s ongoing charges ratio was 1.48%. In EGL’s interim report for the six months ended 31 March 2021, an estimate of EGL’s ongoing charges ratio for the year ended 30 September 2021 was given at 1.46%.

Capital structure and trust life

EGL has a simple capital structure with one class of ordinary share in issue. Its manager has discretion to borrow up to 25% of EGL’s net assets, but its articles of association state that it will not have any structural gearing. EGL’s ordinary shares have a premium main market listing on the LSE and, as at 26 October 2021, there were 100,963,423 in issue with none held in treasury.

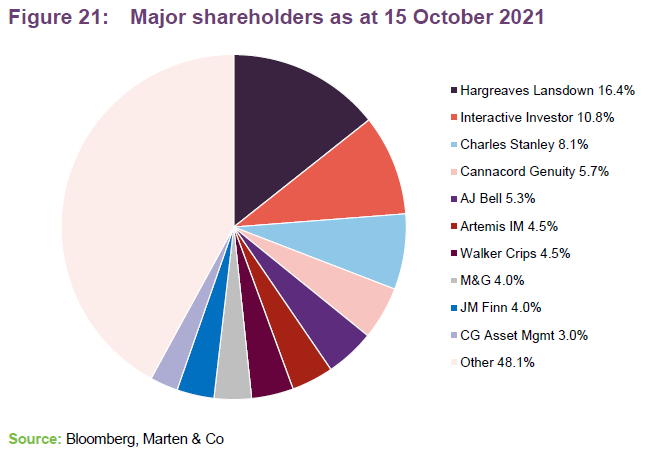

Diversified share register

Figure 21 shows EGL’s largest investors, EGL’s share register includes an array of institutions, private wealth managers and retail holders. The top 10 largest investors accounted for 51.5% of EGL’s issued share capital as at 31 August 2021.

Gearing

EGL has a has a prime brokerage facility with Citigroup Global Markets Limited and benefits from a flexible borrowing arrangement. The interest rate on borrowings under the Prime Brokerage Agreement depends on the currency of the borrowing, but is generally 50 basis points over the applicable LIBOR figure. The gearing is not structural in nature and borrowings can be repaid at any time. At the end of September 2021, EGL had gross gearing of 18.3% and net gearing of 12.5%.

Unlimited life with five-yearly continuation votes

EGL has been established with an unlimited life, but offers its shareholders a continuation vote at five-yearly intervals. The last continuation vote was conducted at the AGM in March 2019. The resolution was passed with 97.5% of votes cast in favour of continuation. The next continuation vote is scheduled for the company’s AGM in 2024.

Financial calendar

The trust’s year-end is 30 September. The annual results are usually released in December (interims in May) and its AGMs are usually held in March of each year. As discussed on page 18, EGL pays quarterly dividends on the last business day of February, May, August and November each year.

Board

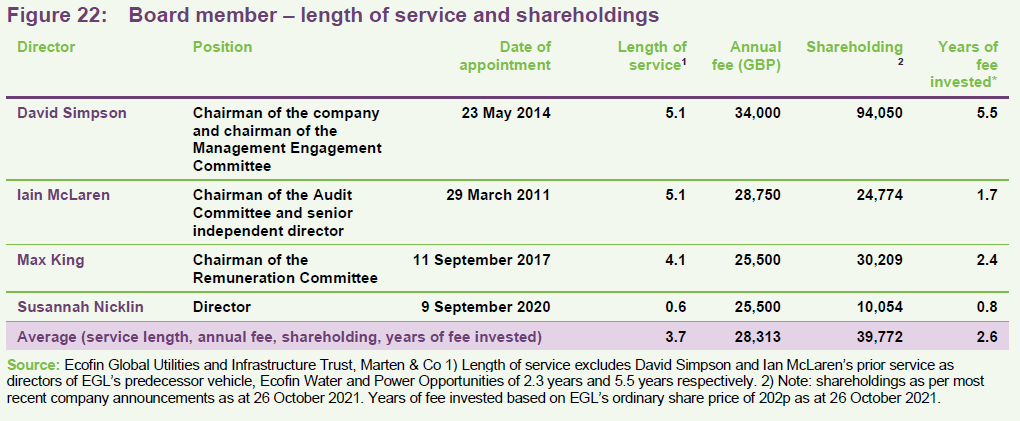

EGL’s board is comprised of four directors, all of whom are non-executive and are considered to be independent of the investment manager. The board has undergone a modest refresh recently with the appointment of Susannah Nicklin on 9 September 2020 in advance of the retirement of Martin Nègre at this year’s AGM on 9 March 2021. Short biographies of all board members are provided below.

EGL’s articles of association require that all board members offer themselves for re-election annually and limit total directors’ fees to £200k per annum. The total fee for the current board structure is £113,750 for the year ending 30 September 2021, an increase of 2.5% for the equivalent structure using the fee rates for the prior year. Other than EGL’s board, its directors do not have any other shared directorships and, as illustrated in Figure 22, all of the directors have personal investments in the trust.

Recent share purchase and disposal activity by directors

Susannah Nicklin purchased 10,054 shares in August 2020, just prior to joining EGL’s board in September 2021, while Iain McLaren’s holding in EGL has continued to tick up as he has reinvested his dividends in the trust. Max King’s beneficial ownership was increased by 10,000 shares in May 2021. None of the directors have made any share sales during the last 12 months.

David Simpson (chairman)

David is a qualified solicitor and was a partner at KPMG for 15 years until 2013, culminating as global head of M&A. Before that he spent 15 years in investment banking, latterly at Barclays de Zoete Wedd Ltd. He is chairman of M&G Credit Income Investment Trust Plc, and a director of Aberdeen New India Investment Trust Plc, the British Geological Survey and ITC Limited, a major listed Indian company.

Iain McLaren (Audit Committee chairman and senior independent director)

Iain is a chartered accountant and was a partner at KPMG for 27 years, including senior partner in Scotland from 1999 to 2004, retiring from the firm in 2008. He is a non-executive director of Edinburgh Dragon Trust Plc, Wentworth Resources Plc and Jadestone Energy Inc. Iain is a past president of the Institute of Chartered Accountants of Scotland.

Malcolm (Max) King (director)

Max is a chartered accountant and has over 30 years’ experience in fund management, having worked at Finsbury Asset Management, J O Hambro Capital Management and Investec Asset Management. He is currently a non-executive director of Henderson Opportunities Trust Plc and of Gore Street Energy Storage Fund Plc.

Susannah Nicklin (director)

Susannah is an experienced non-executive director and financial services professional, having been in executive roles in investment banking, equity research and wealth management at Goldman Sachs and Alliance Bernstein in the U.S., Australia and the U.K. She has also worked in the impact sector with Bridges Ventures and the Global Impact Investment Network, and holds the Chartered Financial Analyst qualification.

Previous publications

Readers interested in further information about EGL may wish to read our previous notes. You can read the notes by clicking on the links or by visiting our website.

Structural growth, low volatility and high income, initiation note, published May 2017

Delivering the goods, update note, published November 2017

On the contrary…, update note, published March 2018

Staying nimble, annual overview note, published October 2018

Unrecognised outperformance, update note, published April 2019

Compelling three-year track record, update note, published October 2019

Resilient income, annual overview note, published June 2020

A wealth of opportunities, update note, published December 2020

Appendix 1 – Fund profile

Developed markets utilities and infrastructure exposure with an income and capital preservation focus

Ecofin Global Utilities and Infrastructure Trust Plc is a UK investment trust listed on the main market of the London Stock Exchange (LSE). The trust invests globally in the equity and equity-related securities of companies operating in the utility and other economic infrastructure sectors. EGL is designed for investors who are looking for a high level of income, would like to see that income grow, and wish to preserve their capital and have the prospect of some capital growth as well.

Reflecting its capital preservation objective, EGL does not invest in start-ups, small businesses or illiquid securities, as these may involve significant technological or business risk. Instead, it invests primarily in businesses in developed markets, which have ‘defensive growth’ characteristics: a beta less than the market average; dividend yield greater than the market average; forward-looking EPS growth; and strong cash-flow generation.

It also operates with a strict definition of utilities and infrastructure as follows:

• electric and gas utilities and renewable operators and developers – companies engaged in the generation, transmission and distribution of electricity, gas, liquid fuels and renewable energy;

• transportation – companies that own and/or operate roads, railways, ports and airports; and

• water and environment – companies operating in the water supply, wastewater, water treatment and environmental services industries.

EGL does not invest in telecommunications companies or companies that own or operate social infrastructure assets funded by the public sector (for example, schools, hospitals or prisons).

No formal benchmark

EGL does not have a formal benchmark and its portfolio is not constructed with reference to an index. However, for the purposes of comparison, EGL compares itself to the MSCI World Utilities Index, the S&P Global Infrastructure Index, the MSCI World Index and the All-Share Index in its own literature. We are using a similar approach here, but are using the MSCI UK Index to represent the UK market. Of the three indices, we consider the MSCI World Utilities to be the most relevant – although it should be noted that this index has a strong bias towards US companies.

Manager

Ecofin Advisors Limited is EGL’s investment manager and AIFM. Ecofin Advisors is a subsidiary of TortoiseEcofin Investments, LLC a privately-owned US-based firm which owns a family of investment management companies. At the end of September 2021, TortoiseEcofin had approximately US$8.3bn of client funds under management.

EGL’s senior portfolio manager is Jean-Hugues de Lamaze. He has worked for Ecofin since 2008 and has managed both EGL and its predecessor, Ecofin Water & Power Opportunities (EWPO) since March 2016. Prior to joining Ecofin, Jean-Hugues co-founded UV Capital LLP and served as its chief investment officer. Previously, he oversaw the Goldman Sachs European Utilities research team and prior to that he was a senior European analyst and head of French Research & Strategy at Credit Suisse First Boston.

Jean-Hugues’s professional career began at Enskilda Securities. He is a CFAF-certified analyst and a member of the French Financial Analysts Society SFAF. Jean-Hugues completed the INSEAD International Executive Programme, graduated from Paris-based business school Institut Supérieur de Gestion and earned a LLB in Business Law from Paris II-Assas University. He was voted Top 10 Buy-Side Individual – All Sectors and Top 3 in the Utilities category in the 2018 Extel survey.

Jean-Hugues leads a team of nine investment professionals – eight of which are based in London and one that is based in Kansas City. He is also draw on extensive resources in Kansas City.

Appendix 2 – The attractions of listed infrastructure

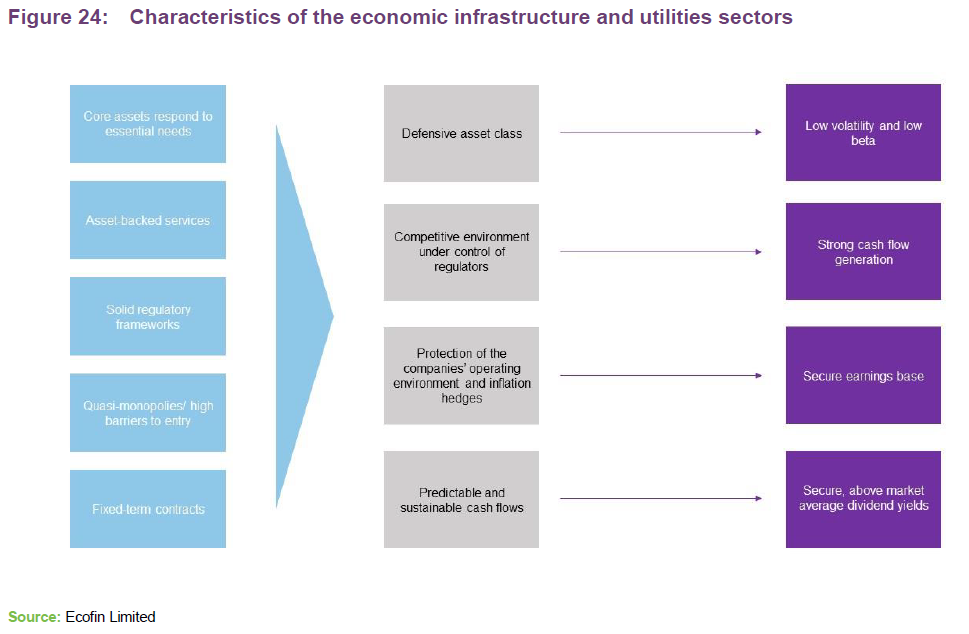

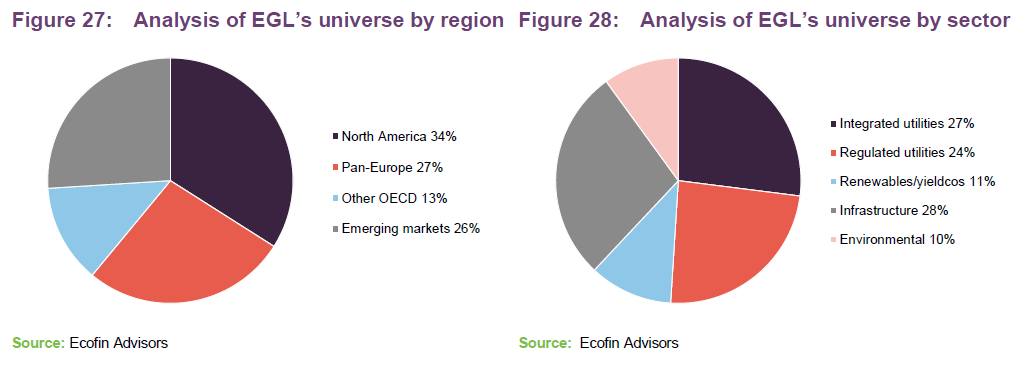

The manager believes that the economic infrastructure and utilities sectors have a number of unique attributes that make them attractive to investors as is illustrated in Figure 24.

Considerable investment is needed in the sector, both to decarbonise power and support new renewable technologies, and to make historic infrastructure safe, sustainable and environmentally friendly. The sums involved are vast – measured in trillions of dollars per year.

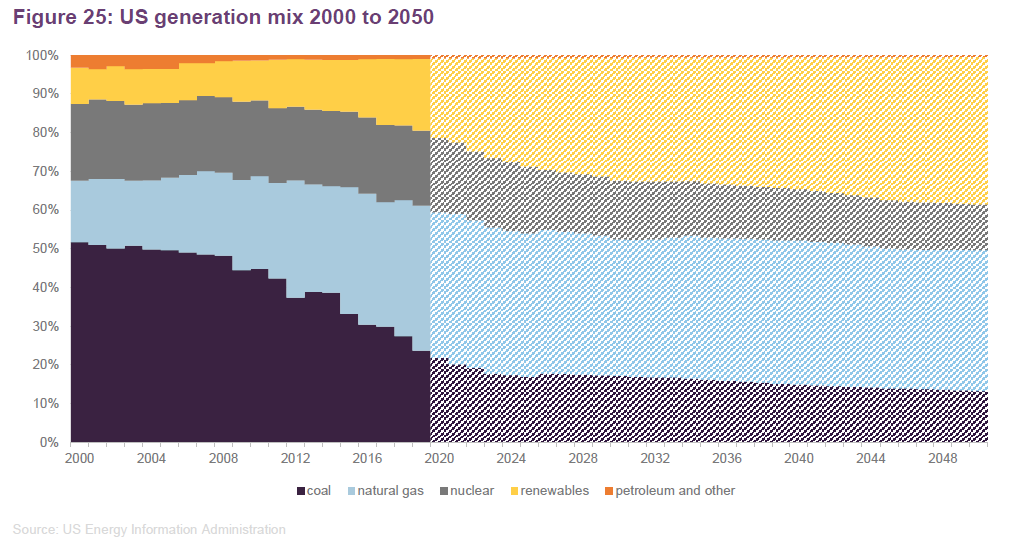

The pace of change in the energy generation sector is illustrated by this forecast from the US Energy Information Administration, which shows the historic and predicted generation mix for the US from 2000 to 2050. The doubling in the share of renewables generation between 2019 and 2050, represents significant growth and investment. However, these figures, and the persistence of coal in the mix, are said by many to represent a significant underestimate of the likely shift away from fossil fuels.

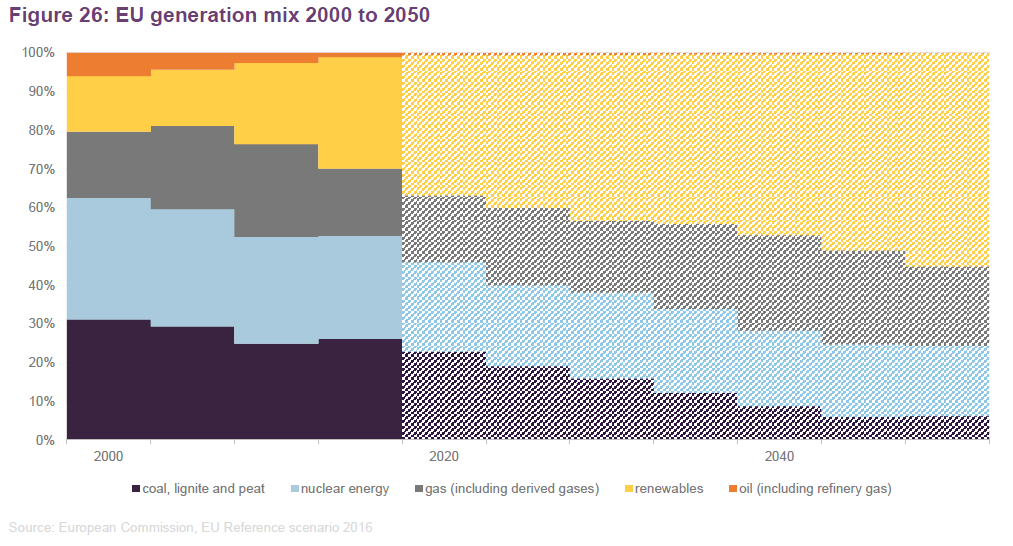

Contrast the US picture with a similar analysis for the EU, which is shown in Figure 26.

Exploiting the shift to renewables is an important theme within EGL’s portfolio. At the end of September 2021, just 10% of the electricity produced by the generation companies in EGL’s portfolio was coal-fired (versus 18% for the companies in MSCI World Utilities Index) and 31% was coming from renewables (20.0%). In terms of CO2 emissions, EGL’s electricity generators’ emissions were 21% less than the MSCI World Utilities Index per $1 invested.

Infrastructure – an important diversifier

In its most recent interim report, EGL’s manager commented that the trust’s allocations to more economically cyclical sub-sectors, such as waste management services, airports, and energy and road infrastructure, have tended to move in and out of stock market favour. Some of these areas, particularly those exposed to road traffic, and particularly air traffic, have found themselves at the sharp end of the slow down and uncertainty remains about the extent and the timing of their recovery (anecdotally, Jean-Hugues is confident that the steady roll-out of effective vaccines will enable a resumption of normal travel trends, both nationally and internationally).

This has led some to question the benefits of including them in a portfolio such as EGL’s. In response, Jean-Hugues comments that, while some of the areas have faced difficulties during the pandemic, they nonetheless remain important diversifiers in an infrastructure portfolio. His view is that they act as ballast more generally, and provide exposure to a recovery in industrial activity and transport volumes. He also believes that these holdings provide exposure to the longer-term opportunities that will come from the replacement of aged infrastructure (the pandemic has illustrated the frailties of older infrastructure, even in the developed world).

Appendix 3 – Investment process

EGL’s portfolio is managed using an investment process that is driven primarily by bottom-up stock selection, based on extensive fundamental research of potential investments, which is coupled with a top-down overlay that informs the overall geographical and sector positioning.

There are 391 companies classified as listed infrastructure that have a market cap greater than $3.84trn and average daily value traded greater than $1m. Companies that do not meet these thresholds would not normally be considered for inclusion within EGL’s portfolio.

Idea generation

Ideas are generated through a number of sources, both quantitative and qualitative. Analysis of industry drivers and subsector trends direct the manager and analysts’ research effort, informing them on where to look for potential opportunities.

Further to this, Ecofin is a recognised specialist in the utilities and infrastructure space, and due to its strong reputation, management teams of investee or potential investee companies are keen to meet the Ecofin team. EGL’s manager says that this supports ideas generation, and with its access to management teams, Ecofin is able to undertake superior analysis and gain stronger insight than a non-specialist manager might be able to achieve.

Analysis

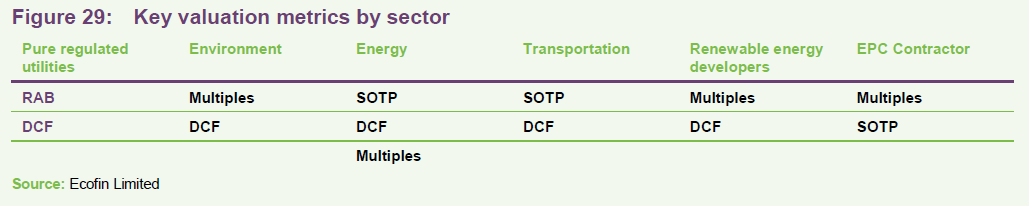

Ecofin does not rely on sell-side analysts’ estimates, and instead conducts its own in-house research and builds its own proprietary models. This allows it to identify situations where it has a different view to that of the market and where there may be a potential opportunity. A wide range of valuation metrics are used to make assessments of the risk/reward characteristics of potential investments. The choice of metrics reflects the needs of the various sub-sectors. The managers use what they describe as a ‘multi-angle valuation approach’ to build confidence in their estimates. Figure 29 illustrates the key valuation metrics used in the main subsectors in which EGL invests.

• Regulatory asset base (RAB) – regulatory formula is used to derive future earnings. The manager assesses the premium/discount, to the RAB valuation, at which a company is trading.

• Discounted cash flow (DCF) is used in situations where a business generates visible and forecastable cash flow streams.

• Sum of the parts (SOTP) is used when a business has multiple divisions. It is used to measure hidden value and to assess the potential for value-accretive disposals.

• Valuation multiples (Multiples) are used for more cyclical stocks. The manager looks to identify earnings and cash flow momentum and so focuses on forward looking metrics. The price-earnings ratio (P/E), cashflow per share and EV/EBITDA are all key.

Catalysts are key to investment decisions

Having identified a difference in its valuation of a stock versus the market, the manager then looks to identify suitable catalysts for the market to reshape its expectations about the stock. The manager says that this is a key part of the investment process. The team may be able to identify a valuation anomaly, but this is of limited use if there is no opportunity to monetise the differential. Ideas are challenged amongst the investment team to ensure they have high conviction.

Portfolio construction

EGL maintains a diversified portfolio of between 40 and 60 holdings. Position sizes will typically range between 1.25% and 5.0% and are determined by the manager’s assessment of risk versus reward. A position could be outside these bounds where, for example, the manager is working to increase or reduce a holding or has a particularly strong view. However, the manager is disciplined in trimming holdings as they rise (although the formal limit is 15% of NAV, the manager says that 8% is his limit as he wants to avoid a situation where one position dominates the portfolio). The manager expects portfolio turnover per annum to be in the range of 40–60%.

When constructing the portfolio, no consideration is given to the split between utilities and infrastructure – the manager is looking for the best opportunities at any given time, but likes to maintain a balance between regulated and unregulated exposures. The portfolio is constructed to have what the manager describes as ‘defensive growth’ characteristics. EGL’s holdings currently have betas in the range of 0.5 (e.g. UK regulated utilities) to 1.2 (e.g. renewable energy companies) with an average of 0.4–0.6.

Analysis by the risk management team, discussed below, also influences portfolio construction.

Top-down overlay

Top-down macroeconomic analysis informs the shape of EGL’s portfolio in terms of geographic and sectoral positioning. Consideration is given to:

• differing regulatory regimes and trends in legislation;

• government energy policies;

• demand growth;

• energy commodity prices;

• industry capex trends;

• credit market conditions and ease of access; and

• interest rates.

Risk management

The risk team works closely with the portfolio manager to assist in investment decisions. It has automated in-house tools that provide real-time risk monitoring and details of exposures. The team monitors hard risk limits, guidelines and typical ranges, and uses a traffic light system to indicate which limits are coming under pressure. Where a position moves to ‘orange’, the risk management team will work with Jean-Hugues to move the position back to green. Key metrics for the traffic light system are portfolio beta, volatility, dividend yield and liquidity.

The risk team also analyses potential biases within the portfolio (geography, sector, market cap, momentum and valuations) and exposures to key risk factors (e.g. correlations to energy, interest rates etc.); conducts scenario analysis; and stress-tests the portfolio.

Investment restrictions

It is expected that EGL will primarily invest in the UK, Continental Europe, the US, Canada and other OECD countries. However, its articles of association state that EGL can invest up to 10% of its portfolio in non-OECD countries. The company is permitted to invest up to 10% of its assets in debt securities and a significant portion may be comprised of cash from time to time.

EGL is also permitted to invest up to 15% of its portfolio in other collective investment schemes, including UK investment companies, but it is not permitted to invest in vehicles that are also managed by its own investment manager. No single position can exceed 15% of the portfolio, at the time of investment, although the manager takes a more conservative approach, limiting investments to a maximum of 8% of NAV.

EGL does not invest in unquoted equities. Furthermore, it does not invest in unlisted securities, save for certain bond or derivative instruments which are typically not listed.

EGL does not invest in telecommunications companies, companies which own or operate social infrastructure assets funded by the public sector (for example schools, hospitals or prisons), or early-stage listed companies which involve significant technological or business risk.

Although not a formal requirement, all of EGL’s holdings pay a yield (currently at least 2%). EGL’s managers say that non-yielding companies do not typically meet their investment requirements.

EGL is permitted to use currency hedging instruments, but usually its portfolio is unhedged.

Focus on stocks with above-average dividend growth

The manager invests in companies that he expects to exhibit strong dividend growth characteristics.

Appendix 4 – Updates on China Suntien Green Energy, Endesa, EDP and Evergy

China Suntien Green Energy – a play on Chinese decarbonisation

We first discussed China Suntien Green Energy (suntien.com/en) in our last note, published in December 2020, where we commented that the company had been a new addition to EGL’s portfolio, which had performed strongly since its inclusion. EGL’s managers added the company to its portfolio when it IPO’d on the Shanghai stock exchange in June 2020, although the company has been publicly traded for much longer, having IPO’d on the Hong Kong exchange in October 2020.

China Suntien is a green energy company that describes itself as only outputting clean energy. It is primarily a developer and operator of wind generation capacity (4.3GW), but also has significant interests in gas transmission and distribution, as well as interests in solar and nuclear. The company is building an LNG terminal in Hebei province, where it already supplies some 20% of gas demand, that is expected to handle 5m tonnes of LNG by the end of 2022.

Jean-Hugues says that, like China Longyuan Power, which was also a new entrant in 2020 that is a play on Chinese decarbonisation, China Suntien is a fast-growing company. He felt that, when it had its IPO on the A-share market, China Suntien was undervalued, given its significant growth prospects, and offered an attractive yield. He thinks that the company is well positioned to benefit from the switch from coal to gas in what is a very polluted region.

Jean-Hugues says that Chinese renewables companies offer massive growth, yet trade at a massive discount to their western peers. For example, Suntien trades at around 8x F12m P/E, while Orsted trades at 40-50 x F12m P/E. He also says that the Ecofin team are much more confident on the outlook for Chinese renewables than they were a year ago, when the Chinese government was attempting to trim the returns these companies were generating. He says that the Chinese government is evolving its approach as it wants to present aggressive decarbonisation goals for COP 26 and beyond. The country is aiming to be carbon neutral by 2060, which is only a decade later than developed nations. Jean-Hugues does not expect China to offer subsidies for renewable generation, as has been done in the west, but does expect the regulatory stance to be lenient and encouraging of renewables build-out.

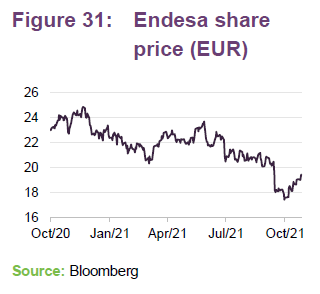

Endesa – position size increased on weakness

We last discussed Endesa (endesa.com/en) in our December 2020 note, where we noted that the company is Spain’s largest energy utility and the second-largest in Portugal (after EDP). Around 70% of the company is owned by Italy’s Enel (also an EGL holding). The company is an example of a utility that has been pivoting away from traditional thermal generation and has been investing heavily in renewable energy generation (hydro, wind and solar) and areas such as smart meters and EV charging. Endesa’s remaining mainland coal plants are scheduled to be phased out by 2022.

A position was established for EGL in April 2020, following a run of poor share price performance that, in Jean-Hugues’s view, had left the company trading at an attractive value (it offered around an 8% yield when he began to build the position). The company performed strongly following its inclusion in EGL’s portfolio but, in common with most utilities and renewables names, Endesa’s share price came off at the end of 2020 and as yield curves steepened this year, affecting utilities, infrastructure and renewables more generally for their perceived interest rate sensitivity.

As a high-conviction holding, Jean-Hugues took the opportunity to increase EGL’s exposure to Endesa as these concerns weighed on markets, and further to Spain’s announcement of a proposal to claw back the excess returns that utilities are earning on the back of higher energy and power prices. Spanish utilities corrected at the time to reflect the increased risk and the Ecofin team felt that this presented a buying opportunity.

EGL’s management team considers that if the measure was imposed as originally suggested, this could cause a double-digit headwind to Endesa’s EPS. However, the team does not expect the measure to be introduced as proposed, with Jean-Hugues noting that similar interventions have been proposed in the past and have not made it onto the statute books. The increase allocation to Endesa, on

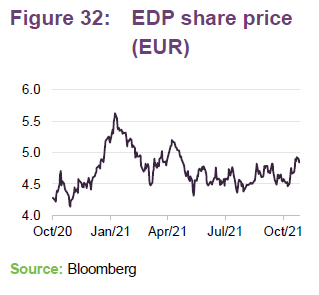

EDP – weighed down by negative sentiment, manager remains positive on long-term outlook

EDP (edp.com) is a Portuguese electric utilities company headquartered in Lisbon that, like many other large European utilities, is moving away from traditional thermal sources and regulated revenues to renewable energy sources and contracted revenues. EDP is Portugal’s dominant power company and a global leader in renewables generation. We last discussed it in detail in our October 2019 note (see page 8 of that note) following shareholders’ rejection of an opportunistic bid from China Three Gorges Group (CTG – a Chinese state-owned power company and a significant shareholder in EDP), which Jean-Hugues felt undervalued the company (EDP itself said that the premium was “significantly below what is customary for cash transactions in the European utilities sector”).

EDP’s share price has struggled this year, weighed down by steepening yield curves impacting long duration business models including renewables. However, EGL’s manager maintains strong conviction in the long term for the stock, which fits nicely with EGL’s focus on the growth in renewable generation.

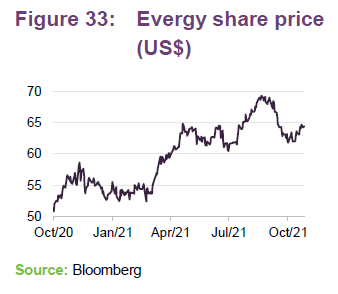

Evergy – ripe for consolidation

In our December 2020 note, we commented how Evergy’s performance had been lacklustre when compared to peers that had rallied, despite having strong value drivers in place. Evergy reportedly received a bid from NextEra in November 2020 in the region of US$15bn (at around US$65 per share), but this was rejected and its share price drifted back down thereafter, assisted by the steepening yield curve during the first quarter of 2021.

However, in January 2021 Evergy added two new directors in an agreement with the activist investor Elliott. In return, Elliott agreed to support current management until 2022. One of the new directors is John Wilder, a utility industry veteran who has previously supported Elliott in some of its other campaigns in the power sector through his investment firm Bluescape Energy Partners. As part of the deal, Bluescape purchased US$115 million of new Evergy shares, and has the option to buy additional stock at a 20% premium to market price over a three-year period.

EGL’s stake was built during a period of share price weakness as COVID-19 hurt both commercial and industrial sales of power. However, Jean-Hugues saw a number of positive attributes to the Evergy story – the company plans to invest $7.6bn over the next five years, but says it has sufficient liquidity and no need to raise additional equity; it has a cost-cutting programme in place (linked to the merger) and is exceeding its targets in this area; and no new regulatory rate determination is planned until 2022. Its generation mix is changing as the company invests in renewable energy (both on its own balance sheet and through PPAs) and also upgrades its power grid.

Jean-Hugues says that, while Evergy has Elliott’s support for now to continue with its standalone strategy, the company is ripe for consolidation. He says that a consolidation/M&A spree is expected in this space and it is believed that Elliott has been building a stake with the intention of pushing through a spin-off of the company.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Ecofin Global Utilities and Infrastructure Trust.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.