Grit Real Estate Income Group

Real estate | Annual overview | 8 May 2024

Building on steadier ground

Having successfully undertaken its latest act of corporate engineering, Grit Real Estate Income Group (Grit) is in a good place to realise substantial capital value and income growth over the medium term. The sale of two assets to meet a capital call by its majority-owned development partner (Gateway Real Estate Africa – GREA) means GREA is well capitalised to deliver a near-term pipeline of developments, including a diplomatic housing scheme pre-let to the US government. Further projects (including more residences for the US embassy as well as hospitals, industrial and data centres) will provide Grit with substantial NAV and earnings growth when they complete and are stabilised.

We expect this will have a positive impact on Grit’s share price. The group’s wide discount reflects (among other things) its expensive debt, with interest greater than its portfolio yield. A plan is in hand to reduce the impact of this through further sales of non-core property.

Pan-African real estate

Grit is a pan-African real estate company that invests in and actively manages a diversified portfolio of assets in selected African countries (excluding South Africa). It aims to deliver strong and sustainable income for shareholders, with the potential for income and capital growth, and targets a total shareholder return of between 13% and 15% a year.

Fund profile

The company’s website is www.grit.group

Grit has a primary listing on the premium segment of the London Stock Exchange’s main market and a secondary listing on the Stock Exchange of Mauritius (SEM). Its focus is on investment in pan-African real estate, and it actively manages a diversified portfolio of assets in selected African countries (excluding South Africa).

Assets underpinned by hard currency leases – predominantly US dollar and euro

It offers access to the growth potential of Africa that is de-risked from a currency perspective. The company’s assets are underpinned by predominantly US dollar- and euro-denominated long-term leases to a range of blue-chip multinational tenant covenants.

The company, which employs 160 people in six countries, aims to deliver strong and sustainable income for shareholders, with the potential for income and capital growth and is currently targeting a net total shareholder return inclusive of NAV growth of between 12% and 15% per annum.

Grit has taken a number of steps to enhance its corporate structure with the ultimate aim of facilitating its inclusion in the UK FTSE Index series and improving liquidity in its shares. In 2020, it moved its corporate domicile from Mauritius to Guernsey, stepped up to the premium listing segment of the London Stock Exchange, and converted to a sterling quotation. The group also de-listed from the Johannesburg Stock Exchange in 2021, making the London Stock Exchange its primary listing.

Market overview

Grit’s recent focus has been on corporate activity to engineer the acquisition of a controlling stake in pan-African developer Gateway Real Estate Africa (GREA) and its development manager Africa Property Development Managers (APDM). Having achieved this in June 2023 (with Grit now owning – directly and indirectly – 54.2% of GREA and 78.95% of APDM), Grit has repositioned itself as a growth company and is set up for substantial growth through new developments (yielding between 10% and 12%) and new income streams through asset management fees.

In time, Grit’s portfolio will be transformed (as we discussed in our previous note Grit 2.0), with new developments focused on diplomatic housing (let to the US embassy and others), logistics, data centres and healthcare. It has also made good progress in disposing of assets in non-core sectors such as retail and hospitality (see page 9 for details). The addition of substantial fee income from the development and property management business (US$6.8m in the final six months of 2023 and expected to be between 10% and 15% of gross rental income over the medium term) gives the company an added dynamic.

Grit’s share price has suffered in recent years as it firstly navigated the COVID-19 pandemic, conducted a substantially discounted capital raise to acquire GREA, and cancelled its dividend to preserve cash (which has now been reinstated – see page 14). Its most recent act of corporate engineering was the sale of two assets to GREA to fund a capital call by the developer (more detail below). Now that this has been executed, and GREA has been consolidated onto its balance sheet (the effects of which will be apparent in future results), the company appears to be on steadier ground on which to build.

Funding GREA’s US$100m capital call

Grit met GREA’s US$100m capital call by selling two assets

On 29 January 2024, Grit announced that it would fund its portion of a US$100m capital call by GREA through two disposals. Here we discuss the details of the sales, the opportunities that a capitalised GREA can deliver and its potential long-term impact on Grit’s NAV and earnings.

Deal enables cash injection of US$48.5m from PIC

GREA’s capital raise, importantly, included US$48.5m from its other shareholder – the Public Investment Corporation of South Africa (PIC) – allowing it to press ahead with its near-term development pipeline (details of which are on page 5). However, with Grit trading at a substantial discount and the debt market extremely expensive, the usual mechanisms for it to raise capital to fund the capital call were not available.

To facilitate GREA’s capital call, Grit sold its interest in Bora Africa (a pan-African industrial and logistics platform) and part of its stake in the Acacia Estate (a diplomatic housing asset in Mozambique) to GREA.

Bora Africa and stake in Acacia Estate sold for total of US$70.3m

The price agreed for Bora Africa was US$50.7m and the 48.5% stake in Acacia Estate was US$19.6m. Grit retained a 5% stake in the Acacia Estate (GREA already owned 46.5% of the asset). These values were in line with the independent appraised value at 30 June 2023, adjusted slightly after a reappraisal at 30 November 2023. The US$18.8m balance from the agreed sales price (US$70.3m) and the capital call (US$51.5m) will be used to reduce Grit’s debt (and therefore reduce its finance cost) and top up its working capital facilities.

On top of this, GREA’s low LTV of around 30% has had a beneficial impact on Grit’s group LTV after it was consolidated onto Grit’s balance sheet in January, which will start to be seen in annual results to June 2024. This will have a positive impact on Grit’s LTV.

Bora Africa

The Bora Africa platform was set up in October 2023 as part of Grit’s strategy to create sub-structures to facilitate increased marketability to third-party investors. It will in time include logistics, light industrial, manufacturing, and digital infrastructure properties (such as data centres). It currently consists of three operational industrial assets; the Orbit complex and Imperial distribution centre, both in Kenya, and the Bollore warehouse in Mozambique. GREA has a pipeline of developments, with a development value of around US$120m, composed of data centres, logistics and light industrial.

The International Finance Corporation (IFC), a member of the World Bank Group, has been issued a subordinated hybrid note in the sum of US$16.9m, which will be used to fund Bora Africa’s initial pipeline. Bora Africa is in advanced discussions with IFC in respect of the issue of a further subordinated hybrid note in the sum of US$13.1m.

Acacia Estate

Another sub-structure set up by Grit is DH Africa, which comprises diplomatic housing projects across the continent. The 76-unit Acacia Estate is located in Maputo, Mozambique and let to the US Embassy and Total. It will be incorporated into the DH Africa platform, which currently comprises Rosslyn Grove in Kenya and Elevation in Ethiopia – both let to the US Embassy on long-term, triple net leases.

The capital raise will be used to fund the construction of a diplomatic housing project in Mali (again pre-let to the US Embassy). A longer-term pipeline of diplomatic housing projects worth around US$400m exists in Senegal, Ghana, Mozambique, Ivory Coast, Malawi, Zambia and Djibouti.

Fee income

Grit to receive asset and development management fees

Through the deal, Grit retains a substantial economic interest in Bora Africa and Acacia Estate (through its 54.2% ownership of GREA) and therefore a substantial portion of the income stream. On top of this, the company will receive management fees through its ownership of APDM, renamed as Grit Real Estate Solutions (GRES).

GRES provides asset management and advisory services to GREA. As part of the asset management and advisory services contract, a management fee is payable to GRES that will not exceed 1.5% per annum of GREA’s total assets under management. Therefore, Grit’s subsidiary will receive 100% of the asset management and development management fees on Bora Africa and DH Africa through GRES, while only incurring 54.2% of the cost by virtue of its ownership of GREA.

Targeting fee income of 2% of NAV

GRES plans to expand its operations to more third-party companies and real estate owners such as pension funds in Africa. Typically, it charges 0.75% of the market valuation for its asset management services, 2.5% to 5% of rent collections for its leasing services, and between 15% and 20% of operational costs for facilities management.

GREA’s development pipeline

GREA will use the proceeds of the capital raise to fund the development of its near-term pipeline. This comprises the US Embassy-let diplomatic housing project in Mali (as mentioned previously), the Coromandel Hospital, in Mauritius, and an industrial scheme in Kenya on land located next to the group’s Imperial Warehouse asset.

DH Mali

The Mali diplomatic housing scheme, located in Bamako, will have 45 units across 10,182 sqm of space. Construction is expected to complete by the end of 2025, when a nine-year lease to the US Embassy will commence. The lease is triple net and denominated in US dollars.

Coromandel Hospital

The Coromandel Hospital, in Mauritius, will sit in a third sub-structure of Grit that was established to accommodate healthcare assets. It will be joined by one existing asset – Fulcan Curepipe Hospital, also located in Mauritius – once construction is complete in the first quarter of 2025. The hospital is let to Falcon Healthcare Group on a triple net, euro-denominated lease. The lease term is 15 years, with an annual rental escalation of 2%.

Industrial development, Kenya

GREA also intends to use the proceeds of the capital raise to fund the development of an industrial scheme in Kenya, on land that it owns next to its Imperial distribution centre asset. The site offers GREA various development options, which are being worked through.

GREA’s longer-term pipeline

GREA’s pipeline includes several diplomatic housing let to the US government

We have mentioned some of GREA’s longer-term development projects already, with the cornerstone being its diplomatic housing projects. These are potentially very lucrative projects, with the US Embassy lined up as tenants, essentially providing US government-backed long-term income. GREA has a long relationship and strong track record working with the US Department of State, where it has so far delivered two projects – in Ethiopia and Kenya – and is currently onsite in Mali. As mentioned previously, there are a further seven projects in the pipeline in partnership with the US Embassy across Africa over several years.

Other longer-term development projects include data centres, logistics schemes and light industrial assets that will form part of the Bora Africa platform (worth around US$120m). Grit says that there is a structural undersupply of industrial property across Africa, and the continent benefits from favourable demographics (the population of Africa is expected to double by 2050, accounting for up to 40% of the world’s under-25s, and rapid urbanisation is set to follow) and growing demand-side pulls (with the digital transformation and internet penetration rates resulting in e-commerce footprints accelerating rapidly).

The final element of GREA’s long-term development pipeline is in the hospital/healthcare sector, where it has plans to build several facilities in Kenya and Cameroon (worth more than US$350m).

GREA targets a 16% IRR on development. Historically, it has had a development yield of around 10.5%, and as the asset has become established, the property has tended to be revalued at yields between 8.5% and 9%. It is these potential capital value gains (and therefore NAV growth) that Grit expects to capture going forward.

Investment process

Grit’s investment strategy centres around being the long-term real estate partner for multinational corporate companies operating in Africa. Multinational corporate companies, such as Total and Vodacom (Vodafone in the UK), have tended to own their own real estate in Africa because of a lack of trusted real estate partners. However, due to its corporate governance structure and balance sheet, Grit has become the real estate partner of choice for many multinational companies. These companies often trade in hard currencies, which support US$ or euro leases.

Grit is focused on property asset classes that it perceives to have strong real estate fundamentals and meet the current and future needs of multinational company tenants. It is focused on growing its exposure to the office, corporate accommodation, industrial/data centre and healthcare sub-sectors. Grit ensures its lease covenants are signed by the parent company, or backed by a parental guarantee or counterparty, which heavily reduces the risk of default.

Grit will only operate in jurisdictions it regards as safe, where it has the ability to move money into the country and repatriate money to Mauritius and where there is no risk of expropriation of funds. Consequently, countries such as Algeria and Angola should not feature in the portfolio. Countries that have challenges around land ownership are also avoided. The company favours countries where it has boots on the ground and where debt can be secured at relatively inexpensive rates (compared to others across the continent).

Characteristics of target countries include:

- stable governance/political maturity;

- strong inflow of foreign direct investment;

- hard currency-based economies;

- sustainable high economic growth rates, with acceptable GDP/spending power per capita;

- natural synergies with the European tourism and local retail market;

- strong urbanised and youthful middle class;

- acceptable sovereign ratings and outlook by ratings agencies;

- solid economic fundamentals;

- favourable policy reform; and

- a clear tax regime.

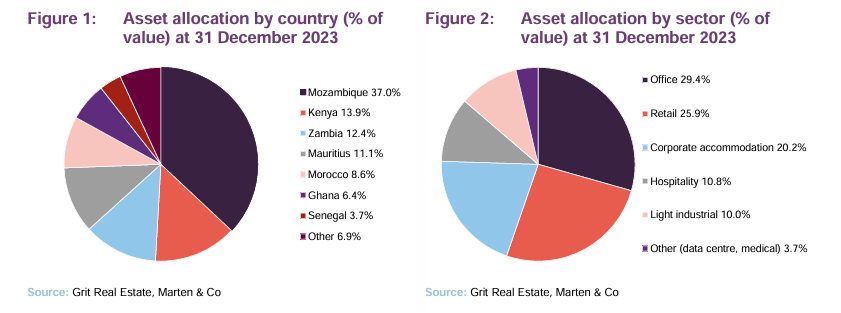

It aims to have half the portfolio invested in investment-grade African countries, such as Morocco, Botswana and Mauritius, and no more than 30% of gross assets exposed to one country (although it is currently overweight in Mozambique, which makes up 37% of the portfolio by value).

When looking at investment opportunities, the company puts a high degree of importance on return on equity (ROE) over the property yield. This means that tax leakage and other administrative costs when returning money back to Mauritius are significant factors in acquisition appraisals. Its target ROE on acquisitions is 8.5% and above, which improves to double-digit returns when leveraged using debt.

Risk mitigation

Grit mitigates operational and other risks associated with African real estate investments through the following measures:

- Country risk. Pre-determined/approved selection of target jurisdictions, which satisfy key investment criteria;

- Repatriation risk. Comprehensive understanding of regulations surrounding repatriation of funds and robust relations with local central banks;

- Currency risk. Prioritisation of assets with US$ or combined US$/euro denominated leases and tenants with hard currency revenues;

- Tenancy risk. Prioritisation of long-term leases with blue-chip multinational tenants, supported and strengthened by parent company guarantees;

- Operational risk. Detailed pre-investment assessment of the ease and cost necessary to ensure the functional operation of the asset, and the selection of reputable, experienced in-country partners and property managers;

- Over-exposure risk. A defined diversification strategy, with strategic limits in place related to any or a combination of the following factors:

- size and value of any single investment; and/or

- country level; and/or

- sectoral level; and/or

- exposure to any single tenant; and

- Political risk: Political risk insurance (PRI) – covering all of the group’s overseas operating jurisdictions – taken out to cover US$ liquidity and expropriation of funds, providing additional layers of protection against repatriation risk.

Portfolio

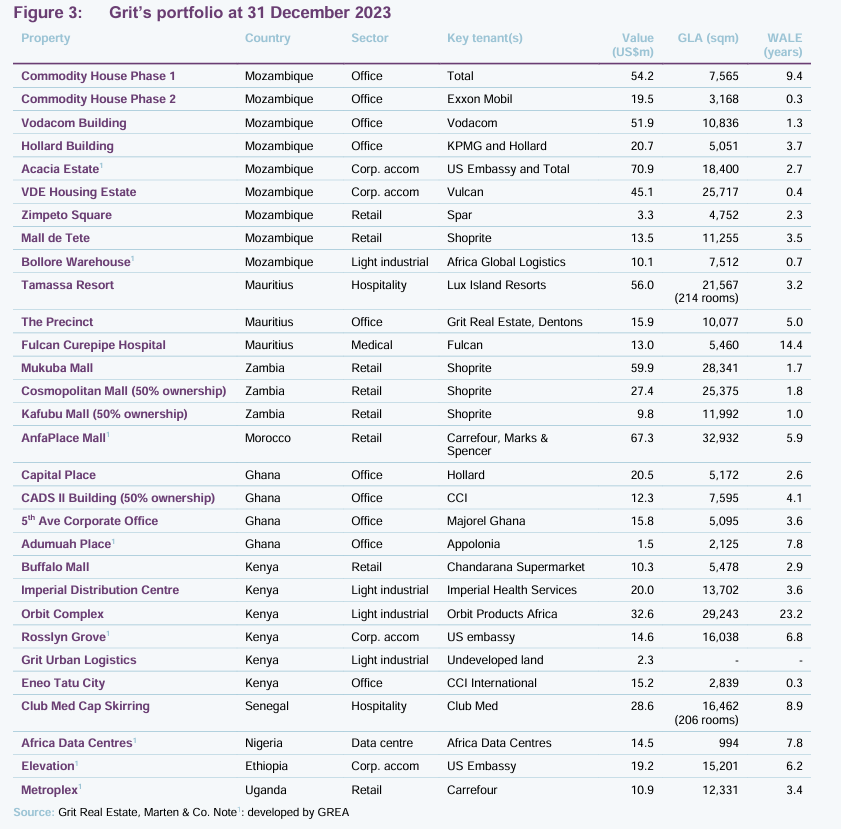

At 31 December 2023, Grit’s portfolio consisted of 33 assets located across 11 countries and seven asset classes, valued at US$780.2m, reflecting a net initial yield of 8.5% and a topped-up net initial yield of 8.6%. The group’s portfolio vacancy rate was 4.5% and weighted average lease expiry (WALE) was 4.7 years. The vast majority (79%) of income is underpinned by a wide range of blue-chip multinational tenants across a variety of sectors and has a weighted average contracted lease escalation of 3.1% per annum. Rents are predominantly collected monthly, of which 95% are collected in US$, euro or pegged currencies.

Grit’s portfolio has evolved over the past 18 months, having achieved its target of US$160m of disposals, and it will continue to evolve with further sales (US$100m target) and the completion of further GREA developments. The US Embassy is now its top tenant, as shown in Figure 3, and the exposure will continue to grow following the completion of further diplomatic housing projects. A hospital – the Fulcan Curepipe, in Mauritius – was added to the portfolio in May 2023 and a further hospital (also in Mauritius) will be added when development is completed by GREA. As mentioned earlier, industrial assets is a focus of growth for the company and will likely make-up around 20% over the next two years. Retail and hospitality will both halve as a proportion of the portfolio through a combination of sales and the other sectors growing.

Completed developments and growth in portfolio rents saw Grit’s net operating income increase 15.6% on a like-for-like basis in the six months to 31 December 2023 – evidence of the recycling strategy paying off. Diplomatic housing, healthcare and data centre assets have replaced earnings disposed of in the hospitality segment.

Top 15 tenants

US Embassy

With the integration of new corporate accommodation assets in Kenya and Ethiopia from the GREA portfolio, adding to existing residences in Mozambique, the US Embassy now accounts for 10.4% of Grit’s income. As already mentioned, GREA has a strong relationship with the United States Bureau of Overseas Buildings Operations (OBO) to develop embassy housing for it across Africa. GREA is developing an additional diplomatic residence let to the US Embassy in Mali, with a further handful in the pipeline.

The Ethiopian corporate accommodation tower is a co-development and equity partnership between US-based Verdant Ventures and GREA. It comprises 112 units and is located in Ethiopia’s capital city, Addis Ababa, which hosts over 130 diplomatic missions and is the third-largest diplomatic community in the world behind Washington DC and Brussels.

The Kenyan diplomatic housing project in Nairobi is composed of 90 diplomatic apartments and townhouses. It marked GREA’s first development in Kenya and a second development in conjunction with US-based developer Verdant Ventures.

The Mali diplomatic housing project, located in Bamako, is less than a kilometre from the US government embassy. The project consists of the development of a 45-unit diplomatic residential complex consisting of a multi-block mid-rise complex with high security requirements. The US government will occupy 100% of the premises. GREA will take part in the development in partnership with OCCEL Engineering, a contracting and development company in Nigeria.

Total

Oil and gas giant Total is Grit’s second-largest tenant, making up 9.8% of income. The company occupies office space and corporate accommodation in Mozambique. Grit extended Total’s lease at the office building, Commodity House, for a further 11 years in 2023. In exchange, Grit did not pass on an 11% increase in rent due under its PPI inflation-linked lease. Instead, the rent will increase 5% in the first year and 4% for the next two years, followed by 3%, before reverting back to annual PPI uplifts. Grit says that the lease extension has been positive for the valuation of the building.

Total’s Mozambique operations were significantly boosted by a US$15bn financing agreement to fund the construction of its liquefied natural gas (LNG) project. The site was the biggest natural gas find in the southern hemisphere in the last 50 years and is expected to take two-and-a-half years to get to the production phase.

Vulcan

Vulcan, part of the $18bn Indian conglomerate Jindal Group, is Grit’s third-largest tenant, accounting for 9.8% of rental income through the leasing of the VDE Housing Estate corporate accommodation asset in Mozambique. Vulcan signed a short-term lease to occupy the estate after acquiring the nearby Moatize coalmine from Brazilian mining giant Vale, which had vacated the corporate accommodation following the sale of the mine to Vulcan.

The VDE Housing Estate has been heavily marked down by valuers in recent periods due to the uncertainty over the tenancy (from US$50.2m in June 2023 to US$45.1m in December 2023), but negotiations for the renewal of the lease (which expires in April 2024) are at an advanced stage. A renewal of the lease is expected to result in a recovery in the value of the asset. Grit is also in discussions over the possible sale of the asset to Vulcan.

Vodacom

Vodacom occupies a 10,836 sqm office in Mozambique and accounts for 6.9% of Grit’s income. Vodacom is one of the biggest telecommunications operators in Africa. Outside of its domestic market of South Africa, its customer base grew 11.6% to 53.7m in the year to 31 December 2023 and the group posted revenue growth of 12.6% across international operations (which comprise Mozambique, the Democratic Republic of the Congo, Tanzania and Lesotho). The group’s mobile banking platform, M-Pesa, processed US$367.6bn of transactions over the year to 31 December 2023, with M-Pesa revenues up 18.3%.

Lux

Grit owns the Tamassa Resort, operated by Lux (which accounts for 5.7% of income), and does not take any risk associated with the hotel operation through a triple net lease, whereby the tenant bears all costs associated with the assets. The creditworthiness of the lease covenant is strong, with Lux’s parent company being large Mauritian conglomerate IBL Group. The company received significant support from the Mauritian government during the pandemic. In terms of rent receipts, it has fully caught up with rent arrears that were afforded to it during 2021.

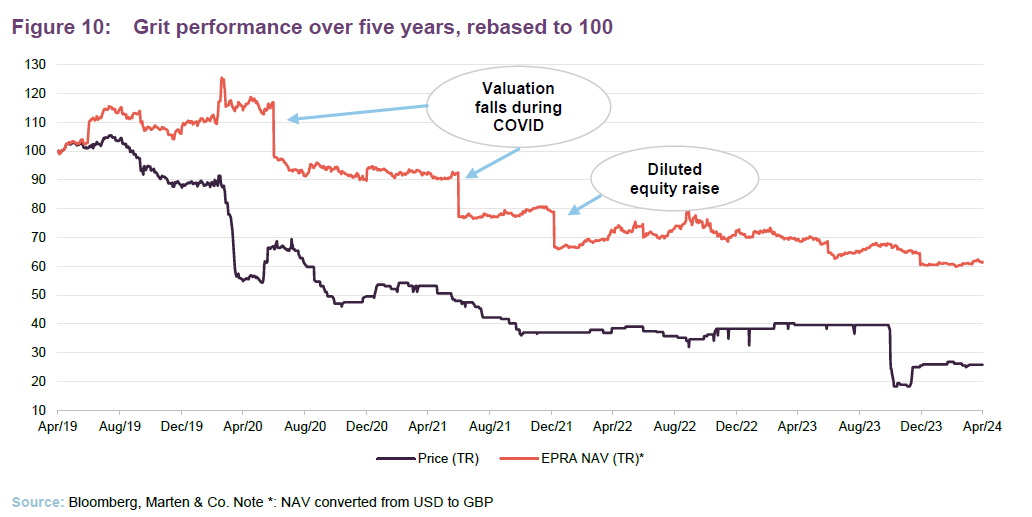

Performance

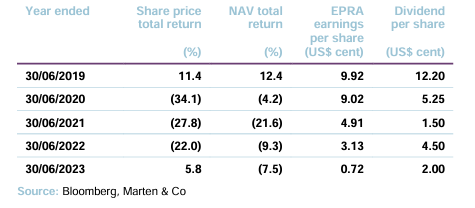

Following Grit’s conversion to a sterling quotation on the London Stock Exchange in August 2020, we have converted its historic NAV and share price from US$ to sterling in Figure 10. Grit’s NAV has been fairly stable over the last two years, having fallen dramatically, firstly due to portfolio valuation write-downs during COVID and secondly due to the dilutionary effect of the issuance of the new ordinary shares in December 2021.

Grit’s share price had not recovered following the drop at the outbreak of COVID-19 in early 2020, but plummeted further in October 2023 after announcing the cancellation of its final dividend for its 2023 financial year (more details follow).

Dividend

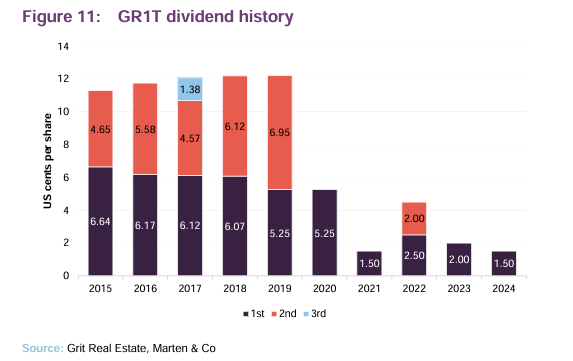

Grit resumed its dividend, declaring a dividend of 1.5 US cents per share for the first half of its financial year to 30 June 2024, following the cancellation of its final dividend for 2023 to support its cash requirements (acquiring GREA and repaying debt), leaving it with a payout from distributable earnings of 46.6% in 2023. The board expects that dividends will be back to normal levels (at least 80% of distributable earnings) in time. Guidance on a final dividend for 2024 should be announced in the company’s trading update in June.

Grit has historically had one of the largest dividend yields of property companies listed on the LSE, distributing 12.20 US cents per share in 2019 – a 10.3% dividend yield on its 31 December 2019 share price. However, its dividend has failed to reach these levels since the COVID-19 pandemic, as shown in Figure 11, but there is cause for optimism that the company can substantially raise its dividend level over time as the implementation of its strategy progresses.

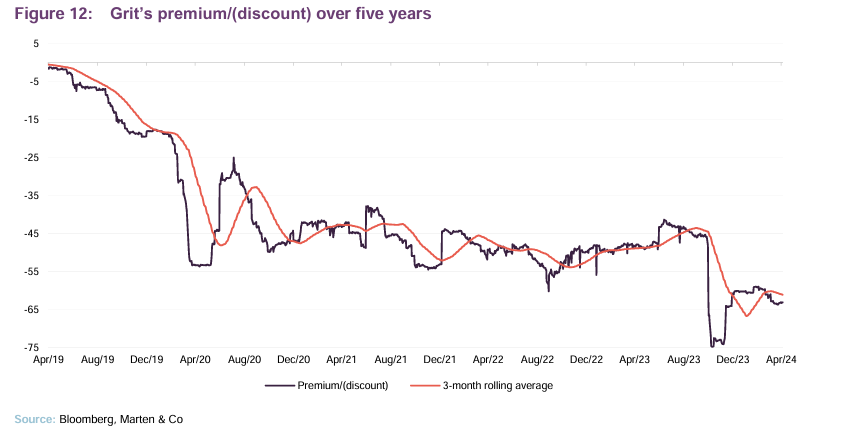

Premium/(discount)

Grit’s discount widened dramatically on the outbreak of COVID-19 at the start of 2020, from which it has yet to recover. The discount widened further after the cancellation of the dividend (as mentioned previously), but has started to narrow. At 3 May 2024, the discount stood at 63.2%.

Now that GREA is embedded into the company and new developments become fully operational, plus the added fee income from the asset management business, we expect a re-rating of Grit’s share price. This would be further helped by the reductions in its debt cost (see following pages for more detail) and the re-establishment of its dividend policy.

Debt facilities

Grit had debt totalling US$411.7m at 31 December 2023, with a weighted average cost of debt (WACD) of 9.6% (up from 7.5% at the end of December 2022) and a weighted average debt expiry of 2.76 years. The leap in the WACD contributed to a 10.4% increase in net finance costs during the period. Group LTV at the end of December 2023 was 47.6% (up from 44.8% at 30 June 2023). The consolidation of GREA onto its balance sheet will have a positive impact on Grit’s LTV. Grit’s medium LTV target is 35%-40%.

The cost of debt is a major sticking point, being greater than the income yield of the portfolio. The increase in WACD was due to the expiration and consequent replacement of an interest rate hedge over US$100.0m notional (which gave protection against LIBOR rates above 1.58% to 1.85%) in October 2023, with a new interest rate hedge for the same notional amount but with a new protection level above 4.75% against SOFR three-month rates. The group has total hedging instruments in place amounting to US$200m to mitigate the impact of further interest fluctuations.

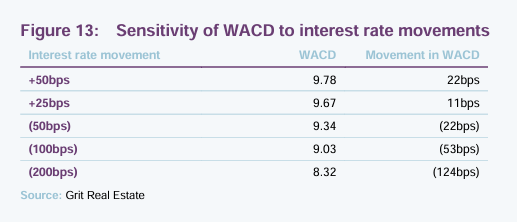

Figure 13 shows the sensitivity of Grit’s WACD to interest rate movements, from the 9.56% WACD reported at the end of February 2024 (including hedges). A fall in interest rates of 200bps will see the group’s WACD fall below the portfolio’s current net initial yield of 8.5%.

The focus of the company is on paying down the most expensive debt facilities (with some costing more than 11.5% in interest) from the proceeds of asset sales – with the opportunity for US$4.1m per annum finance cost savings. The company is also looking to refinance some of its debt on long-dated terms at reduced interest costs.

In October 2022, Grit concluded a major refinancing of its debt facilities, consolidating seven existing loans into a single US$306m facility. A syndication of banks, including Standard Bank of South Africa, ABSA Group and Nedbank Group, participated in the multi-jurisdictional debt facility, which covers Grit’s assets and debt facilities in Mozambique, Zambia, Ghana and Senegal and a corporate level revolving credit facility (RCF). The facility has a sustainability-linked element to it that gives financial incentives for reducing carbon emissions and meeting gender equality targets.

Outside of the syndication are debt facilities with the State Bank of Mauritius totalling US$57.0m (which matures on 31 March 2025), debt held against the AnfaPlace Mall (which also matures in March 2025, but the asset is for sale) and the Kenyan asset facilities, which are to be separately refinanced.

A perpetual note was issued in early December 2021 for the principal amount of US$31.5m. The note is treated as equity for IFRS accounting purposes and has a cash coupon of 9% per annum and a 4% per annum redemption premium. The yield of the note up to the fifth anniversary will be floored at 13% per annum and capped at 16% per annum. Although it has no fixed maturity date, the note carries a material coupon step-up provision after the fifth anniversary, which is expected to result in Grit redeeming the note on or before the fifth anniversary. The note has a further potential maximum 3% per annum return which is linked to the performance of Grit’s share price over the duration of the note.

The management team

The following are key members of Grit’s senior management team.

Bronwyn Knight

Bronwyn is the chief executive officer of Grit. She played an instrumental role in the JSE listing of Delta Property Fund Limited in 2012, where she held the positions of chief financial officer and chief operating officer prior to taking up the leadership role at Mara Delta Property Holdings. During her tenure at Delta Property Fund Limited, Bronwyn spearheaded the diversification of the REIT’s funding sources in the debt capital markets, leading to the establishment of a ZAR2bn Domestic Medium Term Note Programme (DMTN Programme). In addition, she co-headed the team responsible for growing assets under management from ZAR2.2bn at listing to ZAR11.8bn in May 2016. Bronwyn is a founder member and served as non-executive director on the board of Mara Delta Property Holdings Limited (now Grit), where she played a significant role in the listing and conversion of the fund to its current pan-African focus, underpinned by dollar-based leases. She assumed the role of chief executive officer in the lead-up to the fund’s merger with Pivotal to form Mara Delta. Bronwyn has grown the portfolio from US$220m at inception to around US$800m currently, and in November 2019, she was awarded the 2019 EY World Entrepreneur Award – Southern Africa.

Greg Pearson

Greg co-founded Grit with Bronwyn. He was previously head of Africa for AECOM, the US-listed infrastructure firm, where he established many of his client relationships with multinational companies operating across the African continent. Greg was instrumental in sustaining Grit’s rapid growth from its inception in 2014 through to 2018, when he left to focus his attention on GREA. He has since successfully completed a series of developments across the office, retail, leisure, education, and healthcare sectors.

Gareth Schnehage

Gareth joined the company as chief financial officer in February 2024, replacing Leon van de Moortele, who stepped down for personal reasons, having been on medical leave since December 2023. Gareth is a chartered accountant with over 15 years of leading roles at multinational corporations, including extensive experience operating in African jurisdictions and executing asset-backed debt financing solutions.

Previous publications

QuotedData has published six previous notes on Grit. You can read them by clicking the links or visiting our website.

Figure 14: QuotedData’s previously published notes on Grit

| Title | Note type | Date |

| Africa, substantially de-risked | Initiation | 15 July 2020 |

| On the path to recovery | Update | 17 February 2021 |

| Showing some grit | Annual overview | 7 December 2021 |

| Transition underway | Update | 4 July 2022 |

| Going for growth | Annual overview | 20 December 2022 |

| Grit 2.0 | Update | 27 September 2023 |

Source: Marten & Co

IMPORTANT INFORMATION

This marketing communication has been prepared for Grit Real Estate Income Group by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.