Going for growth

Pan-African property company Grit Real Estate Income Group (Grit) is on track to complete the acquisition of a controlling stake in developer Gateway Real Estate Africa (GREA) by May next year, which would unlock considerable potential for net asset value (NAV) and income growth for the fund.

GREA’s attractive pipeline of development projects includes diplomatic housing let to the US government across the continent. Consequently, the composition of Grit’s portfolio will change dramatically over the next two years, with corporate accommodation exposure growing materially and the US Embassy becoming Grit’s largest tenant. Industrial and data centres are also prominent in the pipeline, while sales of properties in the retail and hospitality sectors will further shape the portfolio towards favourable asset classes.

The recent major restructuring of its borrowing facilities (see page 18) and plans to further reduce its loan to value (LTV – borrowings plus cash as a percentage of portfolio valuation) have put the group on a firm financial footing. Meanwhile, the re-establishment of its dividend track record should contribute to a re-rating of its share price (its shares currently trade on a 49.5% discount to NAV).

Pan-African real estate

Grit is a pan-African real estate company that invests in and actively manages a diversified portfolio of assets in selected African countries (excluding South Africa). It aims to deliver strong and sustainable income for shareholders, with the potential for income and capital growth, and currently targets a net total shareholder return including NAV growth of 12% a year.

Fund profile

Grit has a primary listing on the Premium segment of the London Stock Exchange’s main market and a secondary listing on the Stock Exchange of Mauritius (SEM). Its focus is on investment in pan-African real estate and it actively manages a diversified portfolio of assets in selected African countries (excluding South Africa).

It offers access to the growth potential of Africa that is de-risked from a currency perspective. The company’s assets are underpinned by predominantly US dollar- and euro-denominated long-term leases to a range of blue-chip multinational tenants.

The company, which employs 123 people in six countries, aims to deliver strong and sustainable income for shareholders, with the potential for income and capital growth and is currently targeting a net total shareholder return inclusive of NAV growth of 12.0% per annum.

Grit has taken a number of steps to enhance its corporate structure with the ultimate aim of facilitating its inclusion in the UK FTSE Index series and improving liquidity in its shares. In 2020, it moved its corporate domicile from Mauritius to Guernsey, stepped up to the Premium listing segment of the London Stock Exchange, and converted to a sterling quotation. The group also de-listed from the Johannesburg Stock Exchange last year, making the London Stock Exchange its primary listing.

Growth on the agenda

Grit is making solid progress on implementing its new strategy for growth, which is focused on achieving greater returns from development projects and securing fee income from asset and property management services. The strategy was put in place just over a year ago and centred around the acquisition of pan-African property developer Gateway Real Estate Africa (GREA) and development manager Africa Property Development Managers (APDM). Grit raised a total of US$76.1m in an open offer and placing – short of its target of US$135m – meaning that it has had to build up its holding in GREA in phases. The final phase is due in May 2023 and this will give it a controlling stake.

With the proceeds from the raise, the company acquired a controlling interest in APDM of 77.95% and increased its stake in GREA to 26.3%. In August, Grit increased its stake in GREA to 35%. Grit has the option to acquire a further 13.6% interest in May, which would bring its direct shareholding to 48.6%. The exercise of the option would prompt the issue of a free 10% incentive carry to APDM through a performance incentive that becomes effective on a defined exit event. This would bring Grit’s direct and indirect stake in GREA to 51.66%.

Gaining control of GREA and the development manager APDM gives Grit an identifiable route to capital value growth and increased dividends. The benefits of acquiring GREA and APDM include:

- a material acceleration in the group’s ability to access development returns from risk-mitigated development projects;

- the delivery of strong NAV growth over the next 24 to 36 months as projects are completed, including access to an extensive pipeline of US diplomatic housing and data centre development opportunities;

- the resumption of dividend payments (with a target to pay 4.5 to 5.5 US cents per share for the financial year to June 2023);

- the potential for new revenue and fee income streams from its clients and other third parties through APDM;

- diversifying the group’s geographic exposure (in particular reducing the company’s current overexposure to Mozambique, which at 30 June 2022 stood at 36.7%); and

- an expected increase in Grit’s total targeted shareholder return from 12% to between 13% and 15% per annum over time.

Unlocking GREA’s potential

As mentioned, Grit should take a controlling stake in GREA by May next year. This will provide it with access to an appealing pipeline of development projects across the continent – most notably developing diplomatic embassy housing for the United States Bureau of Overseas Buildings Operations. It has so far completed the development of two diplomatic residences for the US Embassy (in Kenya and Ethiopia) with a third approved in Mali and more in its pipeline. GREA also has projects at various stages of development in sectors including offices, industrial, data centres and hospitals.

The returns on offer through development are potentially far greater than buying and asset managing built properties. The attraction of the GREA business and development pipeline is that the letting risk usually associated with development is absent. The group partners with multinational companies looking for real estate solutions in Africa and secures land in conjunction with them before putting a spade in the ground.

Grit says that GREA’s development yield has historically been around 10.5% and as the asset becomes established, the property has been revalued at yields between 8.5% and 9%. It is these potential capital value gains (a fall in yields implies an increase in value) and therefore NAV growth that Grit expects to capture going forward.

Once Grit completes the transaction to take a controlling stake in GREA, the developer’s low LTV of 20% will beneficially impact on Grit’s LTV, lowering it by 3.9 percentage points.

Plan in place to negate impact of interest rate rise

As is likely to be the case across the real estate sector around the world, higher interest rates will have an impact on Grit’s earnings. The group’s weighted average cost of debt (WACD) increased to 7.1% at 30 June 2022 from 5.7% a year prior, and could rise further to 8.6% with an increase in base rates. The company completed a major refinancing of a large portion of its debt structure in October at pretty attractive terms given the volatility in the market (more details on page 18). The interest margin over the Secured Overnight Financing Rate (SOFR) base rate agreed on the new US$306m facility was 559 basis point (bps – equivalent to 5.59%) versus 525bps previously, but will drop back down to 525bps provided that certain environmental, social and governance (ESG) goals are met.

The squeeze on earnings from a higher cost of borrowing should be largely offset by income from management fees secured by APDM. The company provides asset management, real estate management and facilities management services on all assets developed by GREA, charging a 1.5% management fee on their value. It also provides services to third-party companies and plans to do it more widely for several real estate owners such as pension funds in Africa. This growth in fee income is an attractive proposition for Grit as it looks to offset the increase in finance charges.

A further reduction in the cost of borrowing should be made with the repayment of some loan facilities from asset sales. The company expects to sell US$160m worth of assets by the end of 2023 (more detail on page 15), a portion of which will be used to repay debt.

Outlook for African real estate

The outlook for African real estate is positive following the challenges inflicted by the COVID-19 pandemic in 2020 and 2021. This is reflected in the performance of Grit’s portfolio. The retail and hospitality sectors, which were heavily impacted, are showing signs of positive recovery, while assets in the office, corporate accommodation and industrial sectors continue to perform well.

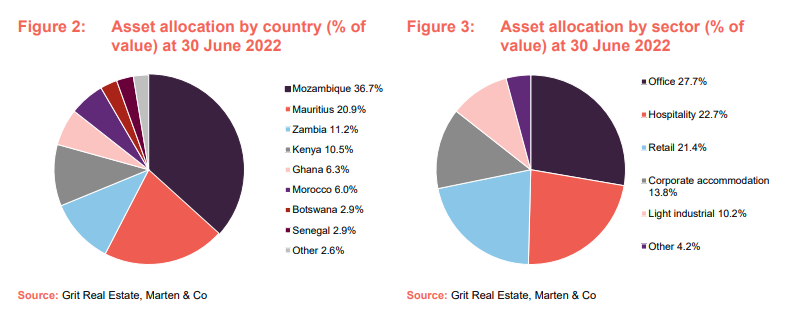

The value of Grit’s portfolio increased 6.9% overall (including completed GREA assets) and 4.1% on a like-for-like basis in functional currencies in the year to June 2022, as shown in Figure 1.

However, due to the strength of the dollar (mainly affecting the euro-denominated hospitality assets), in reported US dollar values the like-for-like portfolio valuation fell 0.3% to US$808.2m. This stability in valuations follows a decline of 14.2% in the 18-month period during the height of the COVID-19 pandemic between December 2019 and June 2021.

Corporate accommodation

Grit plans to increase its exposure to the corporate accommodation sector over the next few years as GREA’s pipeline of US Embassy-let residencies complete. This is a key area of growth for Grit over the coming years and should be rewarded with significant NAV growth as developments turn to established assets, reflecting the long lease lengths and the strength of the tenant covenant.

Retail

Pressure on the retail sector has been abating over the last year, having suffered heavily during the pandemic, with footfall returning to and in some cases surpassing pre-COVID levels. Grit has reported strong levels of letting activity across its portfolio of retail assets – mainly focused on smaller ‘strip’ malls, which have a more non-discretionary food and service retail occupier base. The occupancy levels across the ‘strip’ malls in Zambia (consisting of Kafubu, Mukuba and Cosmopolitan malls) are all close to 100%, with the three assets recording a valuation uplift of 19% over the year to 30 June 2022.

Grit’s only large shopping centre (AnfaPlace in Morocco) is showing signs of recovery (having performed poorly during the pandemic), with footfall up 61% year-on-year and a host of lettings. It was redeveloped in 2019, leaving large parts of the centre vacant just as the pandemic struck. The company has managed to bring the vacancy rate down from 27% at the end of 2020 to 18%, but at lower, turnover-based rents (where a tenant pays a percentage of their turnover rather than a fixed monthly rent). The company is in the process of selling the asset (more details on page 15).

Hospitality

Grit says that hospitality operators in Mauritius (where it owns four hotels) are experiencing strong forward bookings and evidence of robust tourist demand buoyed by an increase in flight capacity to the island after all travel restrictions were lifted in January 2022. The group’s Mauritian hotels are currently averaging room occupancy of around 80%.

In Senegal, where Grit owns a recently-refurbished scheme that opened in December 2021, occupancy of more than 85% is expected throughout December 2022. Grit says that it will commence a €25m expansion of the resort in April 2023.

Industrial

Grit says that the industrial and logistics sector across various African locations is showing the same supply/demand imbalance that has been evidenced in Europe over the past few years, which should lead to significant rental and capital value growth. The continent remains undersupplied for good-quality industrial property, and through GREA’s development capabilities, Grit says that it intends to further grow its exposure to the sector with the establishment of an industrial asset platform to capitalise on this in the near future (more detail on page 14).

Offices

Grit says that it expects office assets in core African countries to continue to perform well with little change in occupation levels and ongoing strong demand. Lack of consistent internet connection and stable power supply has made the global work-from-home phenomenon less relevant in Africa. Demand for office space in Mozambique remains strong (reflected in the leasing performance and valuation of Grit’s four offices in the country). Grit has noted an increase in demand for call centres in region, and recently pre-let an office development in Tatu City in Nairobi, Kenya to a call centre. The Ghanaian office market is showing signs of re-leasing risks and tenant rotations, Grit adds.

Investment process

Grit’s investment strategy centres around being the long-term real estate partner for multinational corporate companies operating in Africa. Multinational corporate companies, such as Total and Vodacom (Vodafone in the UK), have tended to own their own real estate in Africa because of a lack of trusted real estate partners. However, due to its corporate governance structure and balance sheet, Grit has become the real estate partner of choice for many multinational companies. These companies often trade in hard currencies, which support US$- or euro-denominated leases.

Grit is agnostic as to property asset classes and instead is driven by the real estate needs of its multinational company tenants. It owns offices, corporate accommodation, retail, industrial, data centres and hospitality resorts. Grit ensures its lease covenants are signed by the parent company, or backed by a parental guarantee or counterparty, which heavily reduces the risk of default.

Grit will only operate in jurisdictions it regards as safe, where it has the ability to move money into the country and repatriate money to Mauritius and where there is no risk of expropriation of funds. Consequently, countries such as Algeria and Angola should not feature in the portfolio. Countries that have challenges around land ownership are also avoided. The company favours countries where it has boots on the ground and where debt can be secured at relatively inexpensive rates (compared to others across the continent).

Characteristics of target countries include:

- stable governance/political maturity;

- strong inflow of foreign direct investment;

- hard currency-based economies;

- sustainable high economic growth rates, with acceptable gross domestic product (GDP)/spending power per capita;

- natural synergies with the European tourism and local retail market;

- strong urbanised and youthful middle class;

- acceptable sovereign ratings and outlook by ratings agencies;

- solid economic fundamentals;

- favourable policy reform; and

- a clear tax regime.

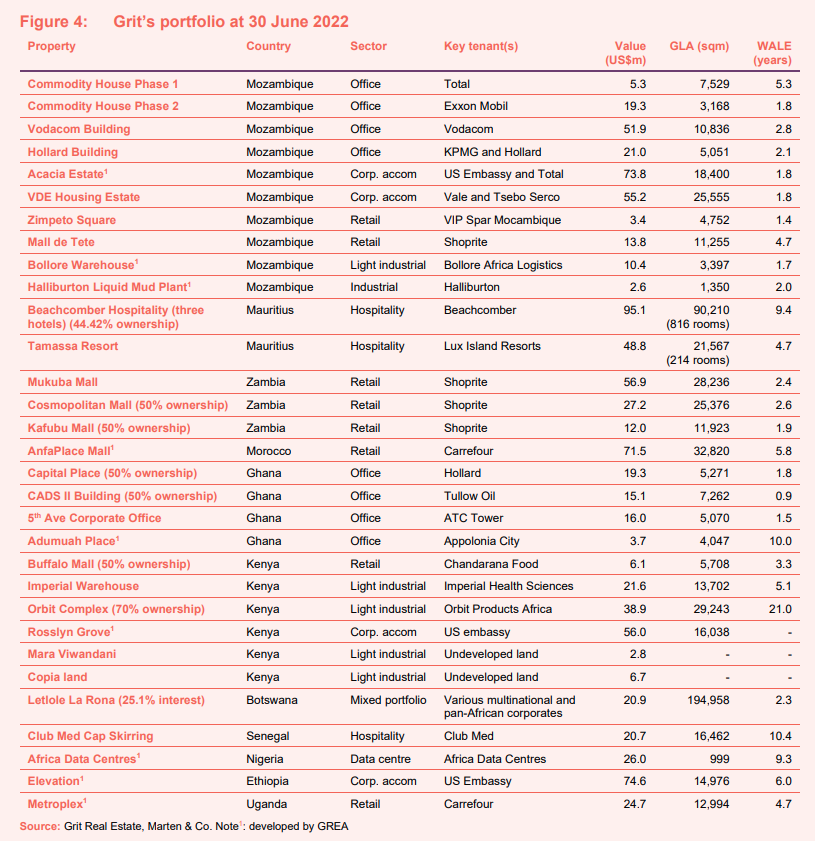

It aims to have half the portfolio invested in investment grade African countries, such as Morocco, Botswana and Mauritius, and no more than 30% of gross assets exposed to one country (although it is currently overweight in Mozambique, which makes up 36.7% of the portfolio by value).

When looking at investment opportunities, the company puts a high degree of importance on return on equity (ROE) over the property yield. This means that tax leakage and other administrative costs when returning money back to Mauritius are significant factors in acquisition appraisals. Its target ROE on acquisitions is 8.5% and above, which improves to double-digit returns when leveraged using debt.

Risk mitigation

Grit mitigates operational and other risks associated with African real estate investments through the following measures:

- Country risk. Pre-determined/approved selection of target jurisdictions, which satisfy key investment criteria;

- Repatriation risk. Comprehensive understanding of regulations surrounding repatriation of funds and robust relations with local central banks;

- Currency risk. Prioritisation of assets with US$ or combined US$/euro denominated leases and tenants with hard currency revenues;

- Tenancy risk. Prioritisation of long-term leases with blue-chip multinational tenants, supported and strengthened by parent company guarantees;

- Operational risk. Detailed pre-investment assessment of the ease and cost necessary to ensure the functional operation of the asset, and the selection of reputable, experienced in-country partners and property managers;

- Over-exposure risk. A defined diversification strategy, with strategic limits in place related to any or a combination of the following factors:

- size and value of any single investment; and/or

- country level; and/or

- sectoral level; and/or

- exposure to any single tenant; and

- Political risk: Political risk insurance (PRI) – covering all of the group’s overseas operating jurisdictions – taken out to cover US$ liquidity and expropriation of funds, providing additional layers of protection against repatriation risk.

Asset allocation

At 30 June 2022, Grit’s portfolio consisted of 59 assets located across 12 countries and eight asset classes, valued at US$808.2m, reflecting a net initial yield of 7.7% and a topped up net initial yield of 8.2%. The group’s portfolio vacancy rate was 4.7% and weighted average lease expiry (WALE) was 4.8 years. The vast majority (85.5%) of income is underpinned by a wide range of blue-chip multinational tenants across a variety of sectors and has a weighted average contracted lease escalation of 5.4% per annum. Rents are predominantly collected monthly, of which 91.5% are collected in US$, euro or pegged currencies.

The composition of the portfolio has changed and will continue to change with the completion of GREA developments – Figure 4 shows the GREA assets that have been incorporated into Grit’s portfolio and Figure 10 details GREA’s development pipeline. Among the recent additions to the portfolio are two corporate accommodation assets let to the US Embassy – in Kenya and Ethiopia. Grit says that the US Embassy will become its top tenant within the next two years, with the completion of further diplomatic residences (corporate accommodation will grow to around 20% to 25% according to the company). Two hospitals will be added to the portfolio when development is completed by GREA, while industrial assets (currently 10% of the portfolio but likely to grow to 20%) is also a target growth sector for the company. Retail and hospitality will both halve as a proportion of the portfolio through a combination of sales and the other sectors growing.

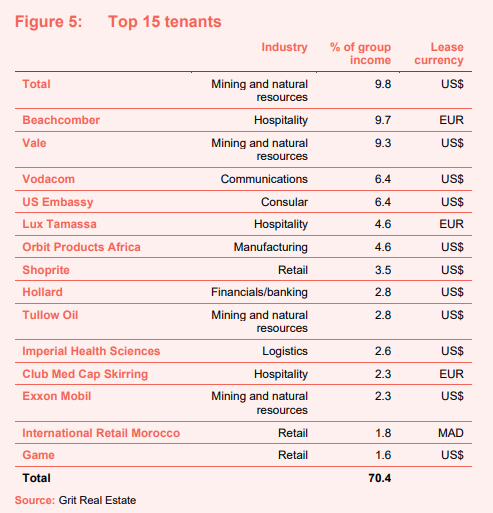

Top 15 tenants

Total

Oil and gas giant Total is Grit’s largest tenant, making up 9.8% of income. The company occupies office space and corporate accommodation in Mozambique. Following a negotiation, Grit recently extended Total’s lease at the office building, Commodity House, for a further 11 years. In exchange, Grit did not pass on an 11% increase in rent due under its producer price index (PPI) inflation-linked lease. Instead, the rent will increase 5% this year, 4% for the next two years, followed by 3%, before reverting back to annual PPI uplifts. Grit says that the lease extension has been positive for the valuation of the building. Total’s Mozambique operations were significantly boosted by a US$15bn financing agreement to fund the construction of its liquefied natural gas (LNG) project. The site was the biggest natural gas find in the southern hemisphere in the last 50 years and is expected to take two and a half years to get to the production phase.

Beachcomber/Lux

The two Mauritian hospitality groups in Grit’s portfolio, Beachcomber and Lux, account for 14.3% of total group income combined. Grit does not take any risk associated with the hotel operation through triple net leases, whereby the tenant bears all costs associated with the assets. The creditworthiness of the lease covenants is strong, with both companies’ parents being large conglomerates. Both companies received significant support from the Mauritian government to see them through the pandemic. In terms of rent receipts, both operators are fully caught up with rent arrears that were afforded to them during 2021. Grit has indicated that it is aiming to dispose of some of its holdings in the hospitality sector in the next year (more detail on the company’s asset disposal strategy is on page 15).

Vale

Brazilian mining giant Vale currently accounts for 9.3% of Grit’s income, through the leasing of Grit’s VDE Housing Estate corporate accommodation asset in Mozambique, with a further year left on its lease and plans to vacate. Vale announced in late January 2021 that it was consolidating its ownership of the Moatize mine and the Nacala Corridor infrastructure project, both in Mozambique, and divesting its coal assets ahead of a possible exit from Mozambique. The VDE Housing Estate has been heavily marked down by valuers and at 30 June 2022 was valued at US$55.2m (down 4% from US$57.5m in June 2021). Vale sold the Moatize coalmine to Indian conglomerate Jindal Group at the end of 2021. Grit says that it has opened negotiations with Jindal over leasing the corporate accommodation. Grit says that the quality of the asset and location to the mine gives it confidence in re-letting the asset on similar terms to another mining company, which would see the value recover.

Vodacom

Vodacom occupies a 10,659 sqm office in Mozambique and accounts for 6.4% of Grit’s income. Vodacom is one of the biggest telecommunications operators in Africa. Outside of its domestic market of South Africa, its customer base grew 4.9% to 41.7m in the year to 31 March 2022 and the group posted revenue growth of 5.6% across international operations (which are comprised of Mozambique, the Democratic Republic of the Congo, Tanzania and Lesotho). The group’s mobile banking platform, M-Pesa, now serves 47.1m customers and processes more than 52m transactions a day worth US$324.6bn over the year to 31 March 2022.

US Embassy

The US Embassy now accounts for 6.4% of Grit’s income with the integration of new corporate accommodation assets in Kenya and Ethiopia from the GREA portfolio, adding to existing residences in Mozambique. GREA has a strong relationship with the United States Bureau of Overseas Buildings Operations (OBO) to develop embassy housing for it across Africa. GREA is developing an additional diplomatic residence let to the US Embassy in Mali, with a further handful in the pipeline. Grit says that the US Embassy should become its top tenant by income within two years.

The Ethiopian corporate accommodation tower is a co-development and equity partnership between US-based Verdant Ventures and GREA. It comprises 112 units and is located in Ethiopia’s capital city, Addis Ababa, which hosts over 130 diplomatic missions and is the third largest diplomatic community in the world behind Washington DC and Brussels.

The Kenyan diplomatic housing project in Nairobi comprises 90 diplomatic apartments and townhouses. It marked GREA’s first development in Kenya and a second development in conjunction with US-based developer, Verdant Ventures.

The Mali diplomatic housing project, located in Bamako, is less than a kilometre from the US government embassy. The project consists of the development of a 45-unit diplomatic residential complex consisting of a multi-block mid-rise complex with high security requirements. The US government will occupy 100% of the premises. GREA will take part in the development in partnership with OCCEL Engineering, a contracting and development company in Nigeria.

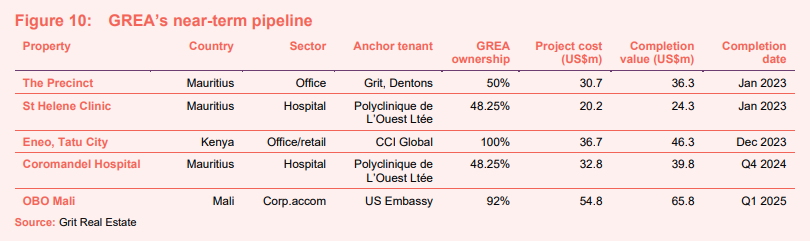

GREA pipeline

Figure 10 details GREA’s current development projects, which have a range of completion dates over the next two years. Beyond this, GREA’s future development pipeline is mainly focused on three sectors – industrial, data centres and corporate accommodation.

Industrial platform

Grit plans to scale up its industrial holdings in a separate platform in which it will seek co-investors. It intends to bind up its current assets and GREA’s future industrial development assets into a single platform and look to sell stakes to investors such as African pension funds. Earlier this year it sold a 30% stake in its Orbit warehouse scheme in Kenya (details below), and this will act as the blueprint for the platform. GREA is seeking land acquisitions across the continent for the development of industrial property. As well as receiving a cash injection from the co-investors, Grit will also receive management fees on the platform for services delivered by APDM.

Data centres

GREA completed the development of a data centre in Lagos, Nigeria earlier this year and has a pipeline of further developments including one in Morocco. Grit says that there is high demand for the data centres across Africa as the implementation of technology, and therefore the use of data, increases.

Corporate accommodation

As detailed earlier, GREA pipeline of diplomatic residences let to the US Embassy is highly attractive. Grit says that there is potential for the development of a further six to eight projects in partnership with the US Embassy across Africa over several years. Its dilemma is how to fund them. Each projects costs in the region of US$50m to US$60m and could mean a capital requirement of around US$200m over the next two years. One option is to take on further debt in GREA – but given the high interest rate environment, this is not the most attractive avenue. What is more likely is a capital call to investors in GREA, in which Grit would have to participate around 50%.

To fund the potential capital call, Grit will use some of the proceeds from its asset recycling programme where it plans to sell around 20% of its non-core portfolio (totalling around US$160m). Grit will also use some of the proceeds to reduce its debt.

Asset recycling

Grit has so far sold US$28.2m of assets (or part interests in assets) of its target of US$160m. It says that it has visibility of achieving its target by the end of 2023. In June 2022, Grit sold Absa House, in Mauritius, for US$12.2m. It has also sold a 4.9% stake in Letlole La Rona (LLR – reducing its interest in the Botswanan listed property company from 30% to 25.1%) for US$3.4m and introduced LLR as a 30% co-investor in the first phase of the Orbit complex asset in Kenya for a sum of US$7.2m.

Most of the future sales will be made from its retail and hospitality portfolios. It had been in advanced negotiations to sell its largest retail asset, AnfaPlace in Morocco, but talks broke down with the interested party. Grit says that it has now engaged other interested parties, adding that it was not prepared fire sell the asset (which was valued at US$71.5m on 30 June 2022).

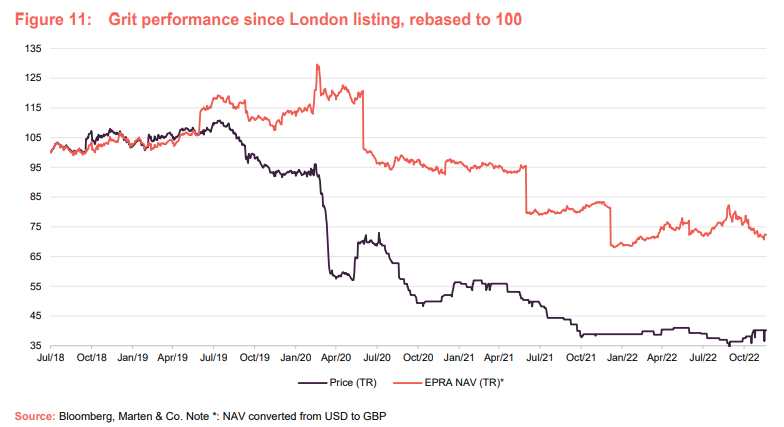

Performance

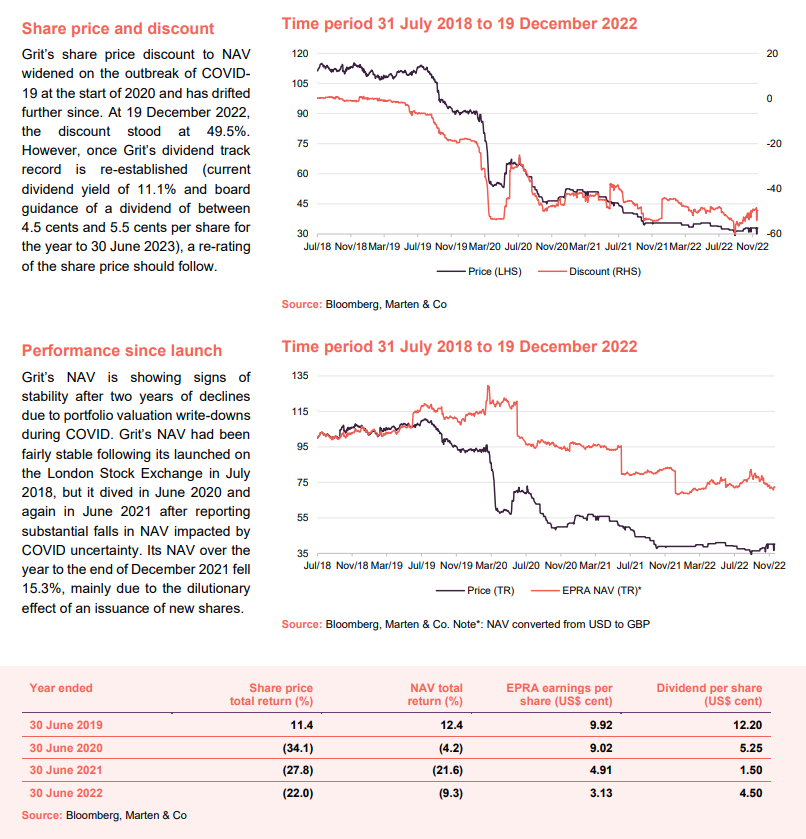

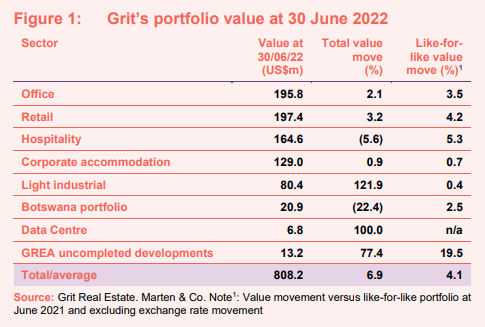

Following Grit’s conversion to a sterling quotation on the London Stock Exchange in August 2020, we have converted its historic NAV and share price from US$ to sterling in Figure 11. Grit’s NAV is showing signs of stability after two years of cuts due to portfolio valuation write-downs during COVID. Grit’s NAV had been fairly stable following its launched on the LSE in July 2018, but it dived in June 2020 and again in June 2021 after reporting substantial falls in EPRA NRV (net reinstatement value – Grit’s preferred metric for reporting NAV which represents the asset value that would be required to rebuild the portfolio from scratch) off the back of portfolio valuation write-downs impacted by COVID uncertainty. EPRA NRV at December 2021 fell 15.3%, principally due to the dilutionary effect of the issuance of the new ordinary shares.

Grit’s share price rose initially, but started to fall in the second half of 2019 and plummeted following the outbreak of COVID-19 in early 2020. Its share price tailed off further as the pandemic continued to have a significant impact on its portfolio and has yet to recover.

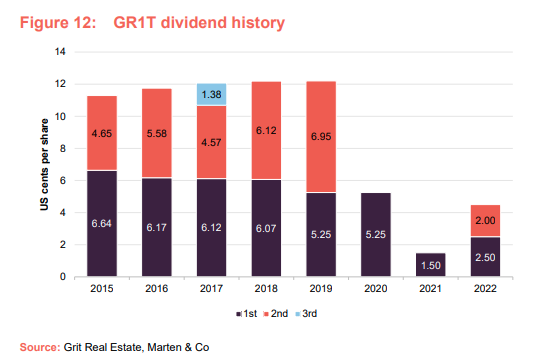

Dividend

Grit paid a dividend for the financial year to 30 June 2022 of 4.5 US cents per share. It has historically had one of the largest dividend yields of property companies listed on the LSE, distributing 12.20 US cents per share in 2019 – a 10.3% dividend yield on its 31 December 2019 share price. Its dividend has been hit during the past two years due to the impact of COVID-19 on its portfolio. The company declared and paid a dividend for the first half of its 2020 financial year (1 July 2019 to 31 December 2019) in line with the previous year, but due to slower rent collections as a result of COVID-19, the board decided to suspend its dividend in the second half of the year. The group declared an interim dividend of 1.50 US cents per share for the first half of its 2021 financial year, but again decided against recommending a final dividend for the financial year ended 30 June 2021, reflecting the board’s caution against a backdrop of the global COVID-19 pandemic. The board expects that dividends will be back to normal levels (at least 80% of distributable earnings) in time following the acquisition of GREA and normalised rent collection levels. For the financial year to 30 June 2023 it is targeting a dividend of 4.5 US cents to 5.5 US cents per share.

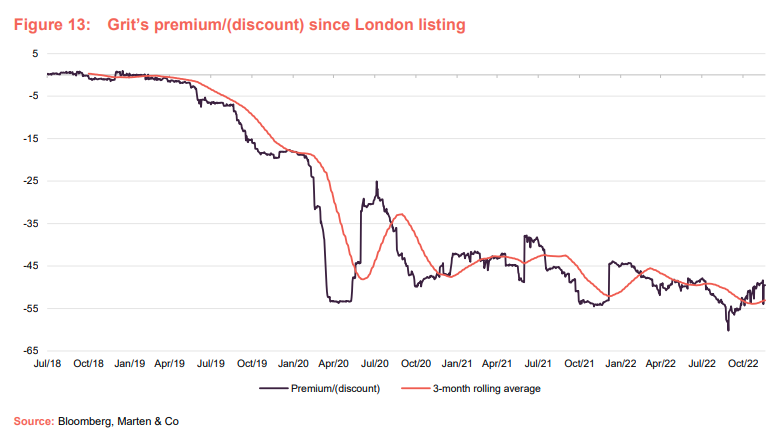

Premium/(discount)

Grit’s share price had fluctuated between trading at a slight premium and a slight discount to NAV for much of its first full year on the LSE before its discount to NAV widened during the course of the second half of 2019. The discount to NAV widened further on the outbreak of COVID-19 at the start of 2020 and the resultant cutting of the dividend. It narrowed as a clean-up of its corporate structure took place, but widened again as the impact of COVID-19 on its retail and hospitality portfolio continued to weigh heavily. At 19 December 2022, the discount to NAV stood at 49.5%.

Once Grit’s dividend track record is re-established (current dividend yield of 11.1% and board guidance of a dividend of between 4.5 cents and 5.5 cents per share for the year to 30 June 2023), a re-rating of the share price should follow.

In October, Grit announced a six-month share buyback and liquidity management programme, which is intended to complement its dividend distribution as a further means to returning capital to shareholders. Shares will not be purchased at a price above Grit’s NAV and the buyback will not exceed US$400,000 per calendar month. As part of the programme, Grit may also issue shares out of treasury, but only at a higher price than when these shares were acquired. The ultimate goal of the programme is to improve the liquidity of the group’s shares. As at 19 December 2022, the company had repurchased 246,782 shares for a total of just over £77,000 at an average of £0.3128 per share.

Borrowing facilities

In October 2022, Grit concluded a major refinancing of its borrowing facilities, consolidating seven existing loans into a single US$306m facility. A syndication of banks, including Standard Bank of South Africa, ABSA Group and Nedbank Group, participated in the multi-jurisdictional debt facility, which covers Grit’s assets and debt facilities in Mozambique, Zambia, Ghana and Senegal and a corporate level revolving credit facility (RCF). The facility has a sustainability-linked element to it that gives financial incentives for reducing carbon emissions and meeting gender equality targets (which Grit says it is on the way to achieving).

The refinancing significantly streamlines Grit’s debt structure. As at 30 June 2022, Grit had a total of US$471.5m in debt, made up of US$425.4m reported and US$46.1m held within its associates. This new facility replaced US$279.1m of existing debt and secured additional funding earmarked for the group’s Club Med Senegal hotel redevelopment project. A US$76.4m Bank of China facility (which matured earlier this year) was fully repaid as part of the refinancing.

Further details include:

- US$66m of the total facility was drawn and priced in Euros with the remaining balance dispersed in US$, to better align with the group’s overall Euro asset exposures.

- The weighted average facility life is 4.3 years, which resulted in an increase to Grit’s weighted average debt expiry profile to over 3.7 years (from 1.25 years).

- The weighted average interest margin over base rates has increased from 525bps (on replaced debt) to 559bps on the new facility. The company said that the cross-collateralisation and link to sustainability targets meaningfully contributed to limiting Grit’s increase in credit spreads, despite material upward pricing pressure in the broader high-yield debt market in 2022.

- The group currently has interest rate swaps and collars over notional debt exposures of US$100m that expire after October 2023 and is implementing additional hedges over a further US$100m notional as part of this refinance, utilising basis swaps and interest rate collars.

Excluded from the syndication were debt maturities on the State Bank of Mauritius facilities totalling US$57.0m (which have been extended to 31 March 2025), debt held against the AnfaPlace Mall (which has also been extended to March 2025, with the asset for sale – as detailed earlier) and the Kenyan asset facilities, which are to be separately refinanced.

At 30 June 2022, Grit’s LTV was 46.7%, down from 53.1% at June 2021 following the equity issue and subsequent repayment of debt. Completion of the acquisition of a controlling stake in GREA in May 2023 will see the LTV fall by a further 3.9 percentage points. The weighted average cost of debt was 7.1%.

A perpetual note was issued in early December 2021 and used to part-finance the acquisition of Orbit in Kenya. The principal amount of the note was US$31.5m, with US$27.5m being issued initially. The note will be treated as equity for IFRS accounting purposes and has a cash coupon of 9% per annum and a 4% per annum redemption premium. The yield of the note up to the fifth anniversary will be floored at 13% per annum and capped at 16% per annum. Although it has no fixed maturity date, the note carries a material coupon step-up provision after the fifth anniversary, which is expected to result in Grit redeeming the note on or before the fifth anniversary. The note has a further potential maximum 3% per annum return which is linked to the performance of Grit’s share price over the duration of the note.

The management team

Following completion of the acquisition, the APDM management team joined Grit while GREA’s chief executive (and co-founder of Grit), Greg Pearson, joined Grit as chief investment officer and remains as chief executive of GREA. GREA’s chief financial officer, Krishnen Kistnen, will remain in that role at GREA in the enlarged group. The following are key members of Grit’s senior management team.

Bronwyn Knight

Bronwyn is the chief executive officer of Grit. She played an instrumental role in the JSE listing of Delta Property Fund Limited in 2012, where she held the positions of chief financial officer and chief operating officer prior to taking up the leadership role at Mara Delta Property Holdings. During her tenure at Delta Property Fund Limited, Bronwyn spearheaded the diversification of the REIT’s funding sources in the debt capital markets, leading to the establishment of a ZAR2bn Domestic Medium Term Note Programme (DMTN Programme). In addition, Bronwyn co-headed the team responsible for growing assets under management from ZAR2.2bn at listing to ZAR11.8bn in May 2016. She is a founder member and served as non-executive director on the board of Mara Delta Property Holdings Limited (now Grit) where she played a significant role in the listing and conversion of the fund to its current pan-African focus, underpinned by dollar-based leases. She assumed the role of chief executive officer in the lead-up to the fund’s merger with Pivotal to form Mara Delta. She has grown the portfolio from US$220m at inception to around US$800m currently. In November 2019, Bronwyn was awarded the 2019 EY World Entrepreneur Award – Southern Africa.

Greg Pearson

Greg co-founded Grit with Bronwyn. He was previously head of Africa for AECOM, the US-listed infrastructure firm, where he established many of his client relationships with multinational companies operating across the African continent. Greg was instrumental in sustaining Grit’s rapid growth from its inception in 2014 through to 2018, when he left to focus his attention on GREA. He has since successfully completed a series of developments across the office, retail, leisure, education and healthcare sectors.

Leon van de Moortele

Leon is the chief financial officer of Grit. He has served in the global risk management services team within PwC, where he became the senior manager in charge of data management. He is a chartered accountant and also holds an Honours Degree in Accounting Science. In 2004, Leon moved to Solenta Aviation, where he became group finance director, during which time the group expanded from 12 aircraft to 48 aircraft, operating in eight African countries. Leon joined Grit in April 2015 as chief financial officer, where he has continued to utilise his tax structuring knowledge and experience in operating in Africa to expand the asset base of the group.

Oteng Keabetswe

Oteng is group chief investment officer of Grit. He has extensive experience in leading debt, mezzanine and private equity investments on behalf of institutions and previously served as investment principal and later acting chief investment officer at the Botswana Development Corporation (BDC) where he was overseeing the BDC’s investment function. Oteng has a BA (Hon) in Finance, Accounting & Management from the University of Nottingham and is a Chartered Global Management Accountant (CGMA). He currently serves as an independent non-executive director on the board of Coca Cola Beverages Botswana (Pty) Ltd and Letlole La Rona Limited.

Previous publications

QuotedData has published four previous notes on Grit. You can read them by clicking the links.

Figure 14: QuotedData’s previously published notes on Grit

Source: Marten & Co |

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Grit Real Estate Income Group.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.