Real estate quarterly report

Kindly sponsored by abrdn

Chinks of light

It has been another quarter of pain for real estate investment trusts (REITs) and listed property companies, with share price weakness continuing and average falls of 13.7% across the sector (as shown in the chart to the right). There are chinks of light appearing amongst the gloom, however.

Although still at elevated levels, inflation has started to ease in the UK, raising the likelihood that interest rates have peaked or are close to peaking. That should give the commercial real estate investment market confidence in their return appraisals, precipitate greater deal flow and a turnaround in valuations. Values among REITs have been showing signs of stabilisation for a couple of quarters now (and validated by asset sales), following a sizeable decline at the end of 2022, especially in sub-sectors that are displaying strong occupational performance and rental growth prospects. This has not been reflected in share prices, however, and discounts to net asset value (NAV) have widened to unprecedented levels.

As a result of the wide discounts, merger and acquisition (M&A) activity continues to be a real threat. Tired of its long-standing and wide discount to NAV, Ediston Property Investment Company decided to throw in the towel and sold its entire portfolio to Realty Income, while LondonMetric completed the acquisition of its smaller peer CT Property Trust.

In this issue

- Performance data – Offices were once again out of favour with investors

- Corporate activity – After an extended hiatus, real estate companies were raising equity again

- Major news stories – Dedicated real estate stock exchange, IPSX, is winding down

Performance data

Best performing property companies

Ediston Property Investment Company saw its share price jump more than 20% over the quarter on news that it was selling its entire portfolio to US REIT giant Realty Income (see page 7 for more details).

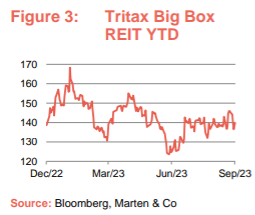

Logistics specialist Tritax Big Box REIT’s share price bounced back in the quarter after reporting an uplift in NAV for the first half of the year. It also continued to execute its disposal programme to recycle proceeds into its higher yielding development pipeline (see page 9).

UK Commercial Property REIT also posted a positive NAV uplift for the quarter to the end of June, further evidence of values stabilising in commercial real estate.

Empiric Student Property continued its solid share price performance this year – gaining 6.3% over the quarter. This is recognition of the highly favourable supply-demand dynamic and rental growth prospects in the student accommodation sub-sector.

Worst performing property companies

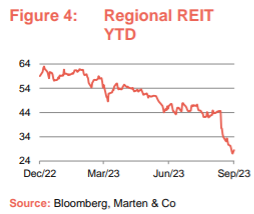

Regional REIT suffered a heavy sell-off of its shares after the surprise announcement that it would cut its dividend. The company also reported a drop in NAV, as values in the office sector continue to fall.

Investor sentiment towards the office focused companies continues to be negative as several elements stack up against the sub-sector. The long-term implications of hybrid working on demand and valuations, the consequences of any future energy regulations and the current economic uncertainty continues to weigh on the sector. Central London office developer Helical and UK and European office investor

CLS Holdings also made the list of worst performing property companies in the third quarter.

Berlin residential landlord Phoenix Spree Deutschland reported another fall in the value of its portfolio due to the impact of high interest rates.

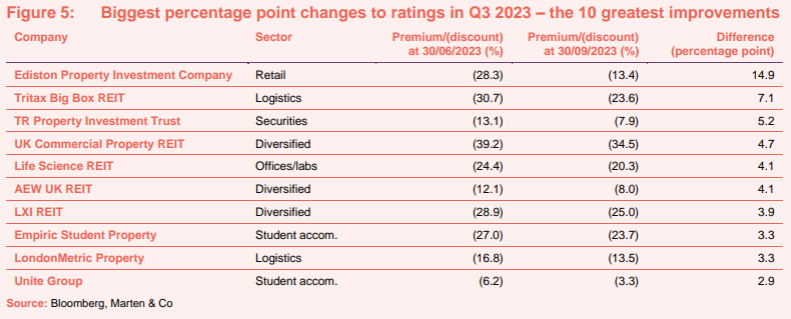

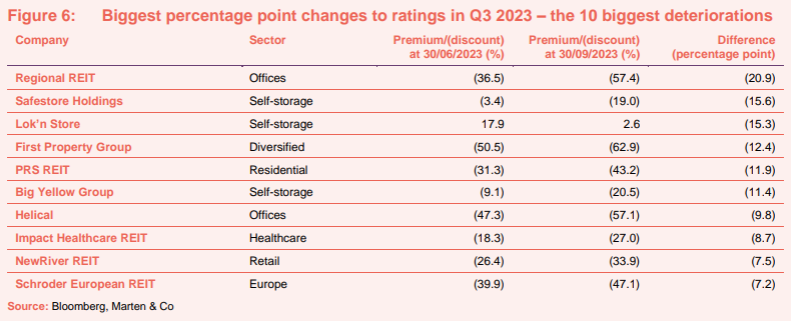

Significant rating changes

Discounts to NAV in the property sector remain some of the widest in the investment trust world. Figures 5 and 6 show how premiums and discounts to NAV have moved over the course of the quarter.

We discussed some of the names on this list in the previous section. Ediston Property’s share price bounce brought its discount in 14.9 percentage points.

TR Property, which owns listed property companies across Europe, saw its share price rise 6.0% in the quarter.

Life Science REIT saw its NAV fall slightly, while also witnessing a small uplift in its share price as the market recognises the strength of its investment case – essentially to transform offices into lab space for burgeoning life science companies at hefty rental premiums.

AEW UK REIT’s share price was rewarded after reporting its NAV had nudged up off the back of strong asset management and valuation stability.

LondonMetric’s share price also rose in anticipation of a boost in NAV following the completion of its acquisition of CT Property Trust (see page 7).

The plunge in Regional REIT’s share price saw its discount to NAV widen to 57.4% at the end of the quarter.

All three self-storage providers – Safestore Holdings, Lok’n Store and Big Yellow Group – saw their ratings suffer as recent trading updates revealed some softness in business demand related to macroeconomic uncertainty was creeping in.

Private rented housing developer PRS REIT’s NAV uplift was not reflected in its share price, as was the case with care home investor Impact Healthcare REIT.

Major corporate activity

Fundraises

£345.5m was raised by property companies during the quarter.

For the first time in more than a year, the sector raised equity from investors.

Unite Group raised a massive £300m in a placing of shares at an issue price representing a discount of 4.2% to the prevailing share price. The proceeds will be used to develop two new purpose-built student accommodation schemes and accelerate asset management initiatives.

Shopping centre owner Capital & Regional raised £25m in an open offer, the proceeds of which was used to part-fund the acquisition of the Gyle Shopping Centre in Edinburgh. Growthpoint, the company’s largest shareholder, subscribed for over 80% of the money raised and as a result now owns 67.64% of the company.

Lok’n Store raised £20.5m through the issue of shares at a 12.1% discount to its prevailing share price. Proceeds will be used to fund its development pipeline.

Mergers and acquisitions

LondonMetric completed its acquisition of CT Property Trust.

LondonMetric completed the acquisition of CT Property Trust. As part of the acquisition 105.6m new LondonMetric shares were issued to CT Property shareholders. LondonMetric’s portfolio is now valued at £3.2bn and generates £160m of rental income per annum.

Ediston Property Investment Company completed the sale of its entire portfolio to RI UK 1 Limited (a subsidiary of Realty Income) for a total of £196.8m. Shareholders will vote on the voluntary liquidation of the company and the return of cash to shareholders (expected to be 72.0p per share) at the end of the year.

Other major corporate activity

Embattled Home REIT changed its investment policy as it looks to stabilise its business following the appointment of AEW as investment manager. Changes included extending the permitted use of properties to include any form of residential during a two-year stabilisation period, in an effort to increase rent collection. Following the stabilisation period, it proposes to invest in “social use” residential accommodation, including for homelessness.

Shaftesbury Capital agreed a new £200m loan with Aviva Investors for a 10-year term secured against a portfolio of assets within the Carnaby estate in London’s West End. The facility will sit alongside existing debt with Aviva Investors of £130m and £120m, which mature in 2030 and 2035 respectively and share in the asset security of the Carnaby estate. The additional financing has been priced with reference to 10-year UK gilt yields and when blended with the existing Carnaby term loans, the annual cash interest rate in respect of the overall amount of £450m will be 4.7%. The proceeds of the facility will be used to repay in part the £576m unsecured loan which was drawn in April 2023 to fund the repayment of the Shaftesbury Plc secured bonds.

Warehouse REIT completed a debt refinancing for a new £320m facility, extending the tenure to June 2028. It comprises a £220m term loan and a £100m revolving credit facility (RCF) with a club of four lenders – HSBC, Bank of Ireland, NatWest and Santander. The debt covenants have been improved, with the minimum interest cover now 1.5 times compared to 2.0 times and the maximum LTV extended to 60% from 55%. Both the term loan and the RCF attract a margin of 2.2% plus SONIA for an LTV below 40% or 2.5% if above. The company has £230m of interest rate caps in place of which £200m fixes SONIA at 1.5% and the remaining £30m fixes SONIA at 1.75%.

Supermarket Income REIT refinanced a large portion of its debt. It cancelled two shorter-dated debt facilities – a £77.5m secured revolving credit facility (RCF) with Barclays and Royal Bank of Canada, and a £62.1m unsecured debt facility provided by a syndicate of banks. It reduced and extended an existing £150m RCF with HSBC to a new £50m, secured, three-year RCF with a £75m uncommitted accordion option at a margin of 170 basis points (bps) over SONIA. It also completed a new unsecured £67m debt facility with Sumitomo Mitsui Banking Corporation, for a three-year term. The debt facility has two one-year extension options and a margin of 140 bps over SONIA. As a result of the refinancing loan-tovalue (LTV) has reduced to 34% (from 40%) and the weighted average term of debt is now in excess of four years and the weighted average all-in cost of debt is 3.1%.

PRS REIT completed the refinancing of its £150m RCF with RBS and Lloyds Banking Group. A new £102m facility of fixed-rate debt for 15 years has been secured with Legal & General Investment Management, together with a further £75m of floating-rate debt agreed for two years with RBS. An interest rate cap will be put in place on the floating rate debt. The company did not disclose the interest rates agreed on the new facilities.

Urban Logistics REIT put in place £57m of new debt on fixed rate terms, refinancing existing floating rate debt. The facility, with Aviva Investors, means the company has £367m of drawn debt and a further £51m undrawn, at an all-in rate of 4.2% and an average maturity of 6.0 years.

Major news stories

- The dedicated real estate stock exchange – IPSX (International Property Securities Exchange) – is winding down having struggled to find new investment. Launched in 2019, the exchange has just three companies listed.

- Meta (Facebook) surrendered its lease with British Land at 1 Triton Square – one of the two buildings it has leased at Regent’s Place in London – paying the landlord £149m. The decision reflects the shift in office occupation with firms scaling back space as more employees work from home.

- The majority of Home REIT’s board will be replaced over the next 12 months. The board – made up of Lynne Fennah, chairman, Simon Moore, Peter Cardwell and Marlene Wood – oversaw the tumultuous period of wrongdoing at the REIT’s former investment manager from inception in 2020.

- Phoenix Spree Deutschland accelerated plans for condominium sales, reflecting the wide discrepancy between values and its share price. With the proceeds, the company will look to reduce overall debt levels and return capital to shareholders.

- Tritax Big Box REIT sold an asset let to Howdens in Raunds for £84.3m, in line with its June 2023 valuations, and reflecting a net initial yield of 4.0%. The company has now sold £235m of assets in 2023 and is targeting a further £100-£200m of sales in the remainder of this year. Proceeds will be put into its development pipeline.

- Empiric Student Property is exploring bringing on board a joint venture partner to grow its portfolio of student accommodation properties. The company has engaged PwC to find a suitable partner that would put up the capital to buy properties that would be operated under Empiric’s student brand.

- Tritax EuroBox sold an asset in Hammersbach, Germany for €64.6m – broadly in line with the valuation as at 31 March 2023. It was the first in its €150m disposal programme.

- Grit Real Estate Income Group concluded the final phase in the acquisition of controlling interests in developer Gateway Real Estate Africa (GREA) and asset manager APDM. Grit now owns a direct interest of 51.48% in GREA and a 78.95% shareholding in APDM. The acquisitions are expected to have a positive impact on group LTV and future growth.

- Helical signed contracts with the Transport for London (TfL) for a joint venture to develop offices above or close to London tube stations at Bank, Paddington and Southwark, totalling 600,000 sq ft.

- LondonMetric Property sold four multi-let industrial estates for £40.5m, in line with March 2023 valuations and reflecting a net initial yield of 6.2%. The sales were in line with its focus on aligning its portfolio to triple net leases.

Selected QD views

Real estate research notes

An update note on Grit Real Estate Income Group (GR1T). The company has been reborn, with the acquisitions of a developer and asset manager making annual return targets of 12-15% more achievable.

An update note on abrdn Property Income Trust (API). The manager’s focus focus continues to be on growing income, and asset management initiatives within the portfolio have seen its vacancy rate drop to below 5%.

An annual overview note on Tritax EuroBox (EBOX). After rapid value declines due to higher interest rates, optimism has grown that prices are stabilising. The company’s is in a good place to increase annual rent through its quality portfolio.

An update note on abrdn European Logistics Income (ASLI). The company is riding out the storm of market valuation declines, with a focus on managing its portfolio and securing income.

Legal

This report has been prepared by Marten & Co and is for information purposes only. It is not intended to encourage the reader to deal in any of the securities mentioned in this report. Please read the important information at the back of this note. QuotedData is a trading name of Marten & Co Limited which is authorised and regulated by the Financial Conduct Authority. Marten & Co is not permitted to provide investment advice to individual investors categorised as Retail Clients under the rules of the Financial Conduct Authority.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access. No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.