Real Estate Roundup

Performance data

Performance data

October’s biggest movers in price terms are shown in the chart below.

For the second month running, Capital & Regional topped the list for share price growth: up 30.5% in the month – admittedly off a low base. The shopping centre landlord’s shares continued to rise after it agreed a deal to sell a majority stake to South African REIT, Growthpoint Properties. In the three-month period to the end of October, the company’s share price has risen 69.7%.

Central London landlord Capital & Counties’ shares have bounced after news that it was in discussions to sell its Earls Court development site broke in October. Reports that it had also received a bid for the whole company, which also includes extensive holdings in Covent Garden, also broke in October. RDI REIT’s shares rose 18.7% in the month after it announced full year results that included shedding a UK mall portfolio that had breached its debt covenant. Town Centre Securities, which outlined its own plans to further reduce its exposure to retail in full year results at the end of September, saw its share price jump 15.4% in October. Industrial specialist Hansteen Holdings and logistics landlord LondonMetric also made the top 10 as the sector continues to perform strongly.

U and I Group was among the worst performing of the established UK real estate companies in October, in terms of share price growth. This follows a jump in its share price in the month of September that saw it make the top 10 chart for best performing real estate companies.

Supported housing provider Triple Point Social Housing REIT saw its share price drop off slightly in October after yet another negative regulatory judgement was published on one of its tenants. During the month, the company made a series of acquisitions and extended its revolving credit facility to £130m. Dublin office and residential landlord, Hibernia REIT, saw its shares fall slightly as too did Secure Income REIT. It has been a relatively quiet couple of months for Secure Income REIT following the £347m sale of a hospital portfolio in the summer. LXi REIT, which owns a portfolio of long-let, inflation-linked properties, also creeped onto the bottom 10 performing companies list despite making further acquisitions progress in the month. Pan-African property company GRIT Real Estate Income Group was, for the second month running, on the list, while European office investor Globalworth saw shares fall after raising €264.3m in a share placing.

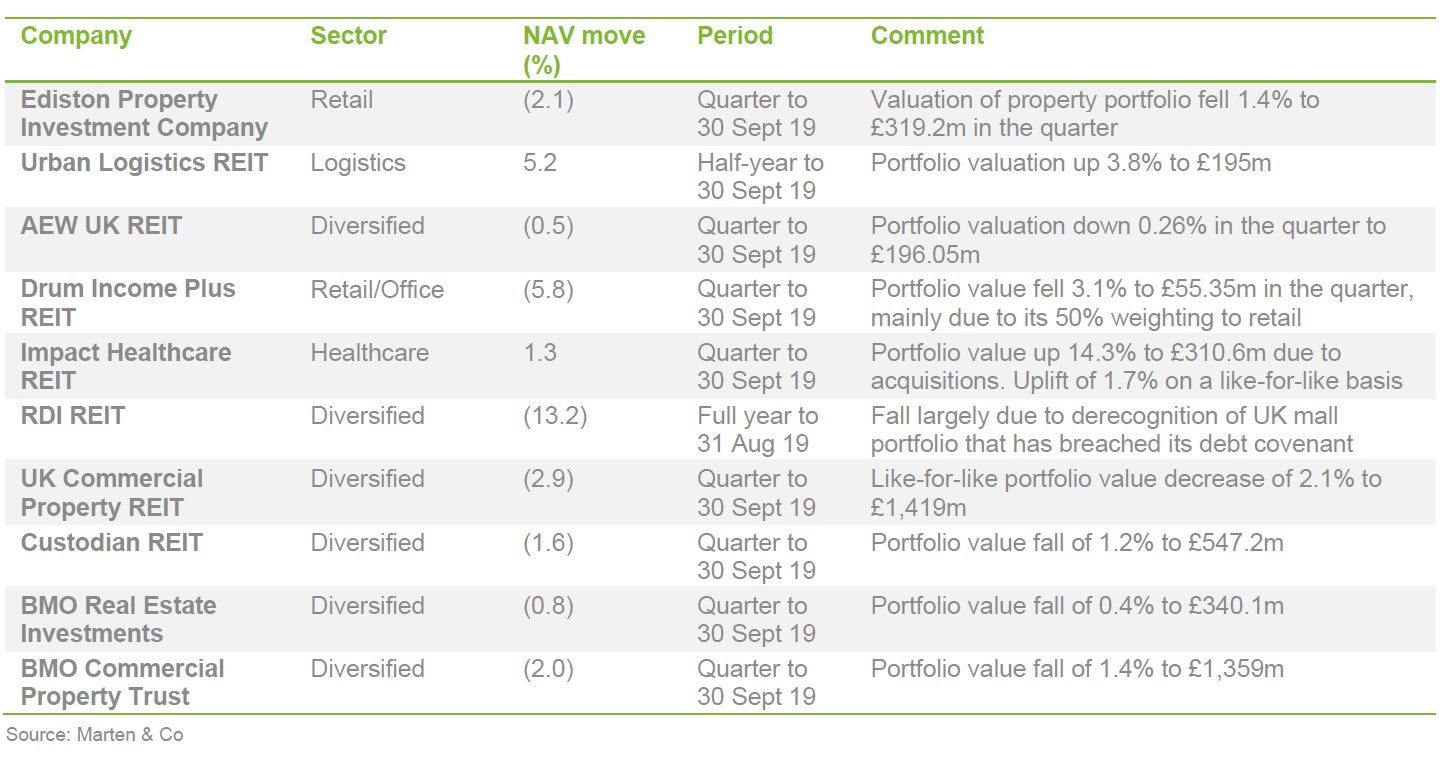

Valuation moves

Corporate activity in October

There were two fundraisings by property companies in October. Supermarket Income REIT raised £100m, double what it was originally looking for yet the issue was still oversubscribed. It has identified a pipeline of acquisitions that will boost earnings.

Central and Eastern European office investor Globalworth Real Estate Investors raised €264.3m. The proceeds will be used to fund the acquisition of five properties in Poland for around €320m.

Shopping centre landlord Capital & Regional agreed a deal to sell a majority stake in the company to South African REIT Growthpoint Properties. The deal will see Growthpoint invest around £150.4m for a 51% stake in the group. Shareholders will vote on the deal at an upcoming general meeting.

Phoenix Spree Deutschland, which specialises in Berlin residential real estate, commenced a share buyback programme of up to 10% of its shares to narrow its 24% discount to NAV. The company has been hit by plans to introduce rent controls in the German capital.

Real Estate Investors switched its existing variable rate £10m loan facility with Lloyds Bank to a fixed interest rate loan facility with an interest rate of 3.129% a year until 30 November 2023.

AEW UK REIT negotiated changes to the covenants on its loan with the Royal Bank of Scotland that permits the company’s borrowings to rise to 55% loan to NAV, from 45% previously. The company said the change will give it wiggle room should asset values fall.

Schroder REIT refinanced its debt, extending the life of a £129.6m loan with Canada Life Investment from 8.5 years to 16.5 years and reducing the interest rate from 4.4% to 2.5%. It paid a break cost of £25.8m to execute the deal, which has been funded by cash reserves. The interest saving of £2.5m a year will be paid to shareholders as an increased dividend.

London-listed, German real estate-focused Sirius Real Estate agreed an extension to its €64.8m debt facility with BerlinHyp to £180.2m. The new facility expires on 31 October 2023 and has an all-in fixed interest rate of 0.9%.

Managers’ views

A collation of recent insights on real estate sectors taken from the comments made by chairmen and investment managers of real estate companies – have a read and make your own minds up. Please remember that nothing in this note is designed to encourage you to buy or sell any of the companies mentioned.

Retail

Ediston Property Investment Company

The retailing environment remains challenging for both landlords and tenants. Many landlords are being forced to face up to the consequences of owning poorly configured space in the wrong locations, let at rents significantly above market levels. The value at risk becomes magnified when net income is eroded by high vacancy and there is a long-term structural imbalance between supply and demand in centres too large for modern retailing needs. Retailers are having to struggle with over-geared balance sheets, retail formats that do not chime with what customers want and an oversized and often over-rented bricks and mortar estate.

However, it is important to emphasise that retail is not in terminal decline. It is evolving, not disappearing as an economic activity. This is an opportunity for landlords, such as the company, who can provide accommodation to occupiers that meets the demands of this new retail world, and for investors who recognise this. Despite the difficulties in the wider retail market, over the 12 months to 30 September 2019 the company’s income has been resilient. The contracted rent across the retail warehouse portfolio has increased from £16.0m per annum to £16.2m per annum. Total contracted portfolio income is £21.4m per annum.

Despite the current uncertainty in the economic and political outlook, the investment market is continuing to function, albeit at lower levels of transactional activity. Nevertheless, values have drifted downwards, with the retail sector hit the hardest. We remain cautious about markets in the short term whilst this uncertainty persists. However, we remain confident about the performance of the company’s assets in the medium term given the attractive yield currently on offer, which is secured on affordable rents on parks where most tenants trade well.

Diversified

AEW UK REIT

Despite the backdrop of ongoing political uncertainty, the company remains confident in its ability to deliver on its objectives. The value of our assets has remained robust to date, particularly in the office and industrial sectors, where assets have either been acquired at conservative levels or provide exciting value-add opportunities. There has been some loss of value in retail assets, in line with the structural changes that we are seeing across the retail sector, however, this has been mitigated by the portfolio’s light exposure to the sector at 14.2% and also by value gains in other parts of the portfolio. EPRA Earnings cover of the quarterly 2 pence per share dividend remains healthy, at 106% this quarter.

The portfolio, now increasingly mature, is offering us numerous opportunities to undertake asset management initiatives which provide various potential routes to add value. Over the past quarter this has included the settlement of an industrial rent review in Bradford at an increase of 14% above the level of our valuer’s ERV. In addition, post quarter-end, we have completed a lease extension on an industrial unit in Basingstoke, which has been achieved at 46% above the previous passing rent due to its short term.

Despite our positive outlook for the portfolio, we are conscious of the opportunity to limit downside risk in an uncertain macro environment and, with this in mind, we have recently taken a number of steps to reduce risk associated with the company’s debt facility. In October 2018, we documented the extension of the loan’s term, pushing expiry from October 2020 to October 2023. In addition, earlier this month we completed an amendment to the loan agreement with RBSi, which increases the loan to NAV covenant from 45% to 55%, subject to certain conditions. Neither of these changes have increased the current ongoing cost of the facility, other than incurring up-front fees. Our aim is to continue to keep gearing at a conservative level in accordance with the company’s stated policy.

RDI REIT

The last 12 months have presented a number of challenges for the business. The current political and economic uncertainty, combined with material structural changes to the retail landscape, has resulted in a significant underperformance by UK REITs with higher than average retail exposure and balance sheet leverage. While the majority of our portfolio has continued to deliver robust operational results, the board recognises the discount of the current share price to NAV. In order to address this, our strategic priorities are being accelerated to deliver a cleaner, simpler investment proposition and a lower leverage capital structure. While we have made material progress in repositioning the portfolio to date; reducing our exposure to retail assets and lowering leverage, the board will continue to review all opportunities to maximise shareholder value, including the rigorous evaluation of all assets within the portfolio.

UK Commercial Property REIT

We took the opportunity to capitalise on good investor interest ahead of a potential lease break to sell our high street retail asset in central Manchester. We were also pleased to make further progress towards reducing our exposure to retail after the period end, when we signed an agreement to sell The Parade in Swindon, our only remaining shopping centre, to an investor with a different return and risk profile. Around half of the portfolio is now weighted towards the industrial and logistics sector of which more than half is of an urban nature – a sub-sector where we continue to see strong interest and rental prospects. Looking ahead, we will continue to assess further opportunities to recycle capital through strategic disposals whilst making investments to grow the portfolio.

Custodian REIT

The investment market has been notably quiet this quarter with transaction volumes down 20% from 2018 according to Knight Frank research. While reduced transaction volumes tell a story about demand, it is also an issue for supply. Opportunities that meet the investment criteria of Custodian REIT have been in very short supply, resulting in a third quarter where the company made no property acquisitions.

Custodian REIT’s investment strategy has always been weighted towards regional industrial and logistics assets, which has stood the company in good stead again this quarter. Valuation gains of 2.1% in this sector during the period point to both underlying rental growth and continued investment demand. There has been much focus in the press on the woes of retailers and the resulting impact on real estate. There is no doubt that the over-supply of shops on the high street needs to be addressed and, while a number of Company Voluntary Arrangements (CVAs) have reduced rents on specific assets, there remains widespread rental value decline as a result of this over-supply. Notwithstanding these falls in rental value, Custodian REIT has continued to focus on maintaining occupancy whilst securing cash flow. We have worked with tenants to retain them in occupation following CVAs and at lease expiry or break, resulting in 96.2% occupancy across our high street retail property portfolio.

We have previously forecast greater resilience in the out of town retail market, which benefits from a restricted supply, generally free parking and the convenience that is complementary to online sales for both ‘click & collect’ and customer returns. This forecast remains robust, although the read-across from the impact on high street retailers and investors generally turning away from the retail sector as a whole, for the moment is in turn having a negative impact on retail warehouse values.

New research

We have published an update note on Aberdeen Standard European Logistics Income. We have also published the first in a series of research notes on the different real estate sectors, starting with the retail market. Read it by clicking on the link or by visiting www.quoteddata.com.

The legal bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.