Focus on tomorrow’s world

With the roadmap out of lockdown and into economic recovery in place, Standard Life Investments Property Income Trust (SLI) has turned its attention to future-proofing its portfolio. This has put environmental, social and governance (ESG) at the forefront of its decision-making process for asset disposals and acquisitions, with longevity of income considered critical to the process. Identifying lasting trends that have developed and accelerated during the pandemic, such as the growth in online retailing and how the office will be used, and its impact on future tenant demand for space, has become mission critical.

Rent collection figures of 93% for 2020 and a 3.3% valuation uplift in the final quarter of 2020 reflect the resilient nature of its portfolio. Further growth is expected to come from savvy asset recycling.

Commercial UK property exposure

SLI aims to generate an attractive level of income, along with the prospect of both income and capital growth, by investing in a diversified portfolio of UK commercial property assets, primarily in three principal commercial property sectors: industrial, office and retail. SLI uses gearing with the aim of enhancing returns, with the current loan-to-value (LTV) ratio at 23.0%.

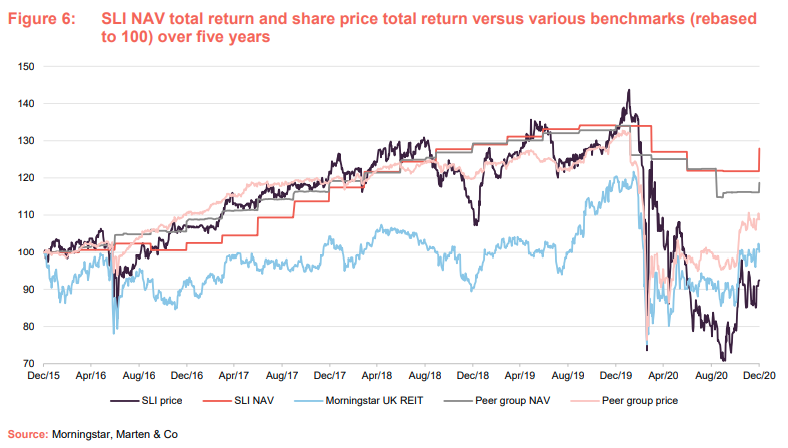

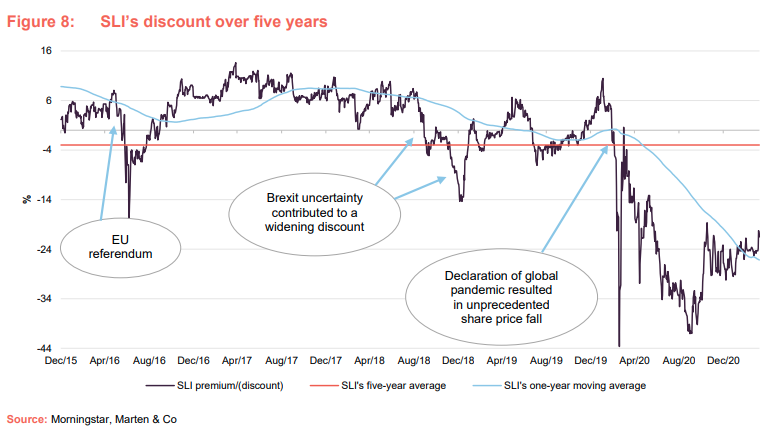

The outbreak of COVID-19 saw SLI’s rating fall from a 9.8% premium to net asset value (NAV) to a 43.6% discount in a matter of days, alongside a mass stock market sell-off. The rating has been up and down since, as successive lockdowns impacted its share price. The good news on vaccines in November 2020 and the success of the rollout has seen SLI’s discount narrow and it is currently trading at a discount of 21.5% (as at 9 April 2021).

SLI’s share price was hit harder than the Morningstar UK REIT index at the height of the pandemic and has lagged the recovery since. In NAV terms, it has recovered some of the losses from its portfolio valuation write downs, with further progress expected (see page 9 for more detail).

| wdt_ID | Year ended | Share price total return (%) | NAV total return (%) | Morning-star UK REIT total return (%) | Peer group NAV total return (%) | MSCI UK total return (%) |

|---|---|---|---|---|---|---|

| 1 | 31 Dec 2016 | 7.00 | 2.50 | -7.40 | 8.30 | 19.20 |

| 2 | 31 Dec 2017 | 13.70 | 14.60 | 12.70 | 9.00 | 11.80 |

| 3 | 31 Dec 2018 | -8.30 | 9.80 | -13.30 | 9.50 | -8.80 |

| 4 | 31 Dec 2019 | 18.00 | 3.90 | 33.10 | 3.80 | 16.50 |

| 5 | 31 Dec 2020 | -29.80 | -4.50 | -16.90 | -9.90 | -13.20 |

Future proofing the portfolio

The real estate sector has gone through profound change during the COVID-19 pandemic. Lockdown has highlighted the vulnerability of sectors such as non-essential retail and hospitality, has cast doubt on the future of the office and has emphasised the strength of the logistics sector. In truth, change had been underway for a number of years, but trends that developed and accelerated during the last year have held a huge magnifying glass up to the sector.

For SLI’s manager Jason Baggaley, it has been about identifying and responding to future real estate requirements. SLI has always been on the front foot in this regard. For several years, pre-COVID, it had shifted its portfolio focus towards industrial and logistics – which it now has a 48.2% exposure to – and away from retail. This provided it with some resilience during the past year. It had also been focusing on providing more amenities, such as bike storage and shower facilities, at its offices, as employee wellness crept up the agenda.

These are changes that any forward-thinking property manager would have been making. The pandemic has moved the bar further. In light of that, SLI’s focus now is on what impact this will have on demand for real estate space in the future.

ESG at heart of investments

The Environmental, Social and Governance (ESG) credentials of potential investment acquisitions have become the top priority for SLI as it looks to future-proof its property portfolio. Assets with high ESG credentials will have sustainable income that can be grown, Jason argues. It means future investments may not be quite as high-yielding, as assets with strong ESG gradings tend to come with a ‘green premium’. But instead of thinking of it as a ‘green premium’, Jason believes that non-ESG conforming assets should be thought of as having a ‘brown discount’. Properties with strong ESG credentials are often newly built and so come with less risk of future capital expenditure needs and also greater prospects of longevity of income growth. The quality of the buildings, and the sustainability features, are more appealing to prospective tenants, and with ESG continuing to move up the agenda of all businesses, they will have greater income growth potential well into the future. Tenants are increasingly becoming more sensitive to the sustainability of the buildings they occupy and are willing to pay a higher rent for them, Jason says. From an investment perspective, investors are willing to pay more for property with higher ESG credentials, supporting long-term valuations.

Sustainability features that SLI are looking for in future acquisitions include top Energy Performance Certificate (EPC) ratings on energy efficiency, but also solar panel installations and rainwater harvesting facilities. On the ‘social’ element, SLI is focused on properties that provide employee amenities, mostly in offices. Amenities such as shower facilities, bike storage and studio space for events and classes all factor into social wellbeing and productivity of workers.

SLI has carried out a number of ESG initiatives on its existing portfolio, including office refurbishments to incorporate some of the features mentioned above. In June 2020 it also completed the installation of a major Photo Voltaic (PV) solar panel scheme on one of its assets, the largest undertaken by Aberdeen Standard Investments in the UK. The power is sold to the tenant, with SLI receiving a yield of around 7% from the £500,000 investment. The scheme is expected to save the equivalent of 229 tonnes of CO2 in its first year of operation, and the power output is the equivalent of the yearly electricity usage of 230 homes. SLI is looking to roll out solar panel installations across its industrial portfolio. It is working with a number of tenants on further sustainability initiatives, including the adoption of a ‘nil rubbish to landfill’ policy.

Industrial versus logistics

SLI made a number of disposals from its portfolio towards the end of 2020, most notably four multi-let industrial assets for £37.75m. Jason believes that the future growth prospects of the multi-let industrial sector, which is comprised of smaller units usually let to small and medium sized businesses (SMEs), is limited as the risk of tenant failure is heightened due to the economic impact of COVID-19. The sub-sector has not benefitted from the move to online retailing. This is not the case in single-let logistics properties, which are thriving due to a marked increase in online retailing and supply chain enhancements. This likely polarisation in performance has not yet been recognised by most investors, and the sales gave SLI the chance to crystallise profits on the assets.

Opportunities in other sectors

Just as he can take advantage of investment sentiment in the industrial sector, Jason believes the same can be said for other less-favourable property sectors, including the retail market, where there is a disconnect between price and quality of asset. Not all retail is bad, and some investment opportunities could exist for the right type of asset – namely retail warehouses. Units on retail parks that are let on low, sustainable rents and are operationally a strong performer for the essential retail tenant are the ideal proposition. That was the case with SLI’s acquisition of a B&Q retail warehouse in Halesowen, West Midlands, in September 2020. Further investment opportunities that provide strong income growth potential could exist in this sector at the right price.

Asset allocation

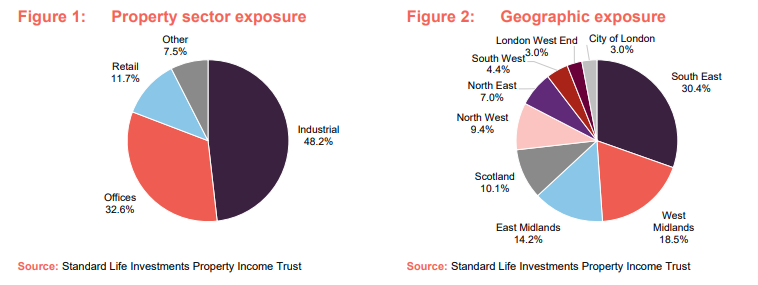

SLI’s portfolio of 50 assets was valued at £437.7m on 31 December 2020 and is primarily allocated across three sectors: industrials (48.2%), offices (32.6%) and retail (11.7%).

In the final quarter of 2020, SLI’s portfolio increased in value on a like-for-like basis by 3.3%, with its weighting to industrial behind much of the increase with a 6.5% like-for-like rise. All sectors increased in value, with offices up by 0.3%, retail up by 0.4% and other (a data centre and two leisure assets) up by 1.7%.

Top 10 holdings and tenants

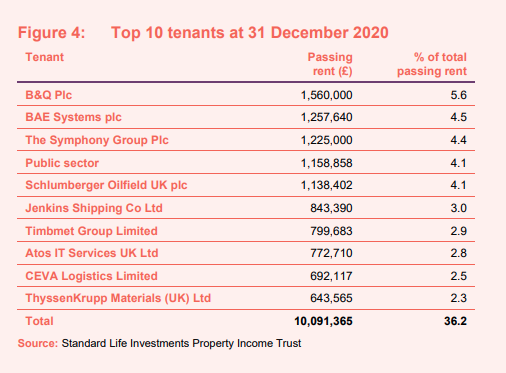

The aforementioned acquisition of the B&Q retail warehouse in Halesowen was the only big change in the group’s top 10 holdings, with the DIY retailer becoming SLI’s top tenant by income, accounting for 5.6% of total passing rent, as shown in Figure 4.

Rent collection figures

For the whole of 2020, SLI has collected 93.6% of rent due. SLI has supported its tenants that are struggling, through rent deferrals or rent-free periods, in exchange for amended lease terms (generally extensions) and, in a small number of cases, rental write-offs. It has made a provision of £2.58m for bad debts in its accounts. Some of SLI’s tenants have abused government restrictions on landlords being able to enforce lease covenants, and chosen not to pay and not to engage with SLI even when they have the capacity to pay (these have generally been companies with private equity ownership). SLI has said it will chase those tenants with vigour as and when government restrictions allow (current restrictions have been extended to the end of June 2021).

For the first quarter of 2021, SLI has collected 84.4% as at 29 March 2021, which is likely to increase in the coming weeks and months.

Sales

SLI completed a number of sales at the end of 2020 totalling £45.6m. The bulk of this was made up of four multi-let industrial assets, which were sold for a combined £37.75m. SLI also sold a retail warehouse in North Shields for £3.55m, on which it had recently concluded a lease regear, extending it to 15 years to expiry. The rent was reduced from £18 per square foot to £15 per square foot, and SLI believed the future rent prospects for the asset were only for further falls. The final disposal was an office building in Derby, which was sold for £4.3m. The capital expenditure required to bring it up to the standard to make it fit for the future of the office (i.e. with amenity space – as outlined earlier) was too great. A further two asset disposals are planned in the coming weeks.

The proceeds were used to pay down the £35m drawn from the group’s £55m revolving credit facility (RCF), while it assesses investment opportunities.

Acquisition pipeline

SLI will look to redeploy £35m to £45m from the RCF on a number of investments in its acquisition pipeline. The most significant being the acquisition of speculatively built (without a tenant signed up) logistics facilities. The group is in negotiations with several logistics developers to acquire mid-box (80,000 sq ft to 160,000 sq ft) logistics buildings on completion of construction. SLI is not taking development risk (The risk of things such as construction costs increasing and delays occuring) but is taking letting risk.

The sites all have planning permission in place and construction (which usually takes between nine to 12 months) is ready to start once terms are agreed. The yield on cost is expected to be in the region of 5.25% and 5.5%, which compares favourably to investment yields in the prime mid-box logistics market of around 4.0%.

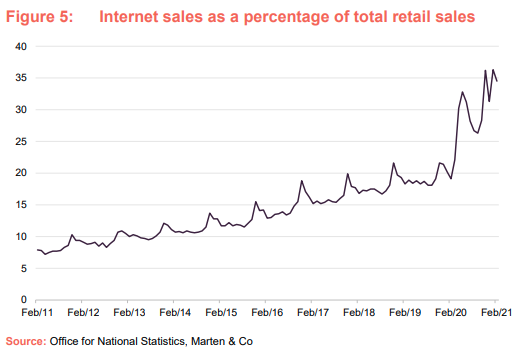

Tenant demand for logistics space is at an all-time high for several reasons. Online retail sales had been increasing for a number of years, as shown in Figure 5, but the rate accelerated hugely during the pandemic as non-essential retail was locked down for large periods of the year. Online retailing accounted for 34.5% of all retail sales in February 2021 compared to 19.1% in February 2020. Online retailers and parcel carriers have been scrambling for space to cope with the surge in demand for home deliveries. Mid-box logistics units are a vital link in the distribution network, as goods are transported from national and regional distribution centres to the front door.

The COVID-19 pandemic laid bare how quickly supply chains can be disrupted when they span many different countries and continents. It has led to a ‘reshoring’ of supply chains (bringing manufacturing back to the UK or holding more stock here, for example), the result of which has been an increase in demand for logistics space in the UK. The future trading relationship with the EU, following the Brexit deal, has created barriers to trade and it is expected companies will look to restructure their supply chains further to gain greater operational efficiencies.

SLI is also looking at investment opportunities in other property sectors, including self-storage and aparthotels, as well as being open-minded to opportunities in the retail warehouse sector.

Performance

SLI’s NAV total return has, for all periods (from three months to 10 years), beaten that of the AIC’s Property – UK Commercial peer group average, as illustrated in Figures 6 and 7. For a strategy such as SLI’s, where assets tend to be held for the long term, we consider that the longer-term periods are the most relevant when assessing the effectiveness of the strategy. In this regard, SLI has markedly outperformed the peer group averages.

Despite SLI’s superior NAV recovery over the last six months, its share price recovery has lagged that of its peer group and the Morningstar UK REIT index, which seems perverse.

We have used the Morningstar UK REIT Index and the MSCI UK Index as comparators to SLI’s short- and long-term performance. From an inflation comparison, SLI’s NAV total return has been markedly ahead of inflation (as measured by both RPI and CPI) over five- and 10-year periods. In Figure 7, we have used RPI, RPI + 2%, CPI + 3% and Libor + 5%.

Premium/(discount)

The outbreak of COVID-19 saw SLI’s rating fall from a 9.8% premium to a 43.6% discount in a matter of days, with a mass stock market sell-off. Its rating has been up and down since as successive lockdowns impacted its share price. The news of vaccine success in November 2020 saw its discount narrow and it is currently trading at a discount of 21.5% (as at 9 April 2021).

SLI is authorised to repurchase up to 14.99% and issue up to 10% of its issued share capital (renewal of these authorities is sought annually at the company’s AGM). Purchase of shares will only be made at prices below the prevailing NAV to enhance shareholder value.

Since November 2020, SLI has repurchased 9.9m shares for just under £6m at an average price of 60.1p in an ongoing share buyback programme. These shares are held in treasury.

Fund profile

SLI launched on 19 December 2003. It is domiciled in Guernsey, has a premium main market listing on the London Stock Exchange and, to maintain a tax-efficient structure, migrated its tax residence to the UK on 1 January 2015, when it also became a UK Real Estate Investment Trust (REIT).

SLI aims to provide investors with an attractive level of income, together with the prospect of income and capital growth. It aims to achieve this by investing in a diversified portfolio of UK commercial property. These are principally direct holdings within the three main commercial property sectors: office, industrial and retail, although it can also hold assets in the alternatives sector.

The board’s and manager’s preference is towards properties that are in good, but not necessarily prime, locations, where it is perceived that there will be good continuing tenant demand. The manager also looks for properties where it can add value using asset management initiatives. There is a focus on tenant quality, and as part of SLI’s strategy, tenants are treated as key stakeholders and the manager works closely to understand their needs. The aim is to achieve greater tenant satisfaction and retention, and hence lower voids, higher rental values and stronger returns.

SLI has full use of the wider Aberdeen Standard Investments (ASI) team, which has 270 people globally working on property. This provides access to specialist transactions, ESG, debt and research teams, as well as providing a risk management framework.

Previous publications

QuotedData has published three previous notes on SLI. You can read these by clicking the links.

KYT (know your tenant), initiation note, published July 2019

Adding value in cautious times, update note, published February 2020

Building for a new normal, annual overview, published September 2020

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Standard Life Investments Property Income Trust.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.