A long term play

CEIBA Investments (CBA), the foremost foreign investor in Cuban real estate, has seen its share price fall to all-time lows with a combination of harsh US sanctions on Cuba, the COVID-19 pandemic, and economic and political instability hitting sentiment. There are optimistic signs of improving fortunes on all three fronts, however.

In June, the first measures to ease the US-Cuban embargo were put into effect – the first steps made by President Biden to come good on his campaign promise to reverse the harsh economic sanctions imposed by President Trump. Meanwhile, tourist arrivals to the country continue to grow as international travel resumes – good news for CBA’s four hotel assets (with a fifth on the way in 2023) as the Caribbean high season approaches. In time, economic and political reforms in the country should have a positive effect on the Cuban economy.

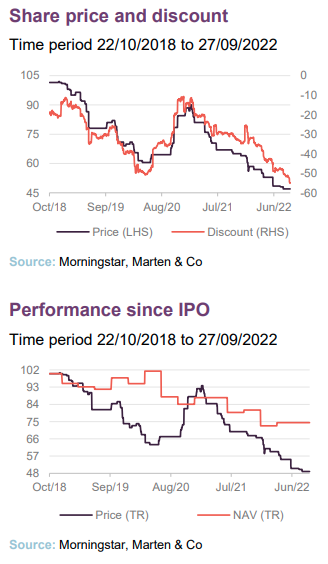

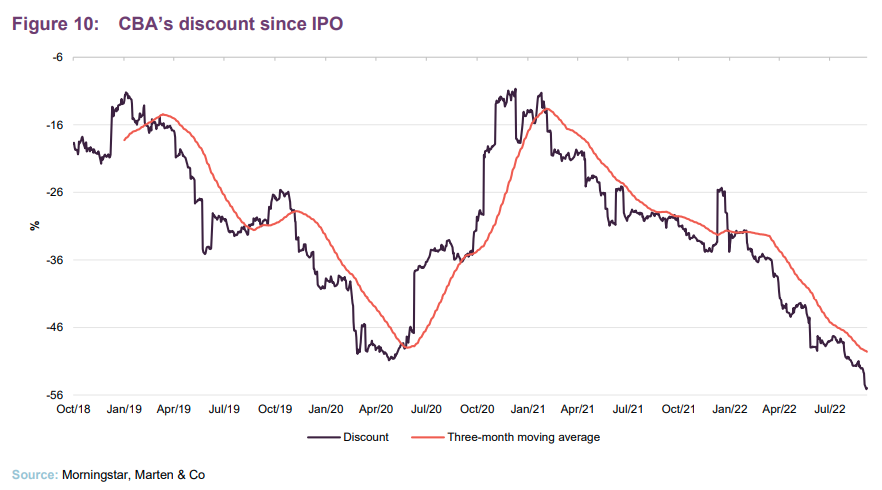

The current share price discount to NAV of 55.0% seems to be an attractive entry point, given the long-term upside potential.

Tourism and commercial property in Cuba

CBA invests in and manages a portfolio of Cuban real estate assets, focused on commercial and hotels, with the aim of providing a regular level of income and capital growth.

Fund roundup

CEIBA Investments (CBA) is a country fund with a primary focus on Cuban real estate assets, and owns a portfolio of commercial and hotel properties. It was incorporated in October 1995 and started making investments in Cuba in 1996. It was listed on the Irish Stock Exchange between 1996 and 2002 and what was then called the Channel Islands Stock Exchange, between 2004 and 2011. In 2002, a new management team was appointed, headed by current lead manager Sebastiaan Berger.

On 22 October 2018, the company completed an IPO raising a further £30m, and listed all of its ordinary shares (total market cap of close to £137m) on the Specialist Fund Segment of the London Stock Exchange.

CBA is a unique investment company, and the value of its real estate assets is largely linked to the US and the status of its embargo on Cuba; political and economic instability in the country; and the level of tourist arrivals in Cuba (which have been heavily impacted by the coronavirus pandemic). Combined, these have contributed to the group’s current wide discount to NAV. But there are optimistic signs that situations are improving on all three issues.

US embargo: small steps could lead to giant leaps

Up until a couple of months ago, nothing had changed in the relations and the harsh economic sanctions placed on the Caribbean nation by the US under the Trump administration, despite President Biden stating that he intended to reverse them during his campaign to become president. It took more than a year from his inauguration in January 2021 before there was any movement to make good on that promise.

We explained in more detail the embargo and impact on Cuba in our initiation research note on CBA (which can be read here). However, in summary, direct foreign investment into Cuba was significantly impacted during the term of the Trump administration, increased restrictions were placed on US citizens travelling to Cuba, US cruise ships were banned from calling at Cuban ports and family remittances were severely limited.

In May 2022, the Biden administration announced its first measures to ease the US Cuban embargo and on 8 June 2022, amendments to the Cuban Assets Control Regulations were published in the US Federal Register. The summary reads:

“The Department of the Treasury’s Office of Foreign Assets Control is amending the Cuban Assets Control Regulations … to increase support for the Cuban people. This rule authorises group people-to-people educational travel to Cuba and removes certain restrictions on authorised academic educational activities, authorises travel to attend or organize professional meetings or conferences in Cuba, removes the $1,000 quarterly limit on family remittances, and authorises donative remittances to Cuba.”

Although these are only small steps in reversing the policies imposed by Trump, CBA’s manager believes that these should have a positive impact on Cuba’s economy and that they could be the first of many. The success of US politicians in the state of Florida is unequivocally linked to policy on Cuba. Once campaigning for the US mid-term congressional elections is completed in November 2022 (where 28 US Representatives from Florida will be elected and the Florida US Senate is being contested), more steps to reverse the restrictions may be taken – including lifting the ban on US visitors to Cuba. The potential upside for the Cuban economy, if relations with the US improve and the number of US visitors increases again, is vast.

Tourist visitor numbers improving

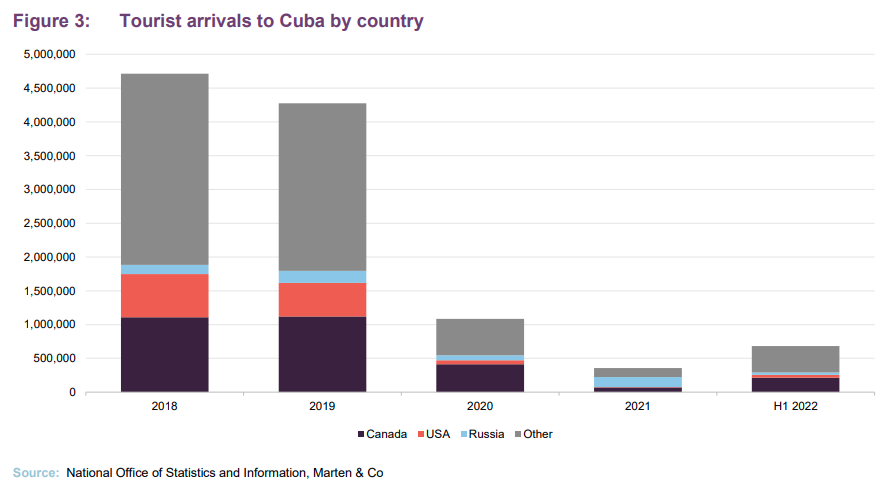

The lifting of restrictions on US citizens visiting Cuba would have a seismic impact on the occupancy and performance of CBA’s hotel assets as they come out of the pandemic. US visitors accounted for 13.5% (637,907) of all tourists to Cuba in 2018 before greater restrictions on US citizens visiting the island were put in place by the Trump administration in 2019.

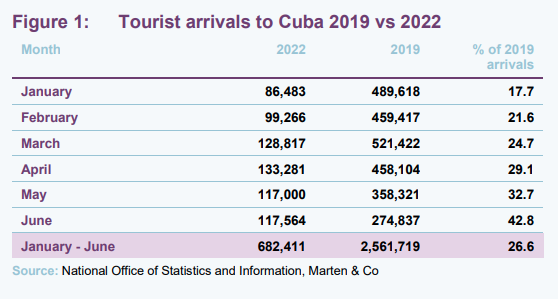

Travel restrictions in the wake of the COVID-19 pandemic had a huge impact on tourist numbers and occupancy across CBA’s hotels. As Figure 1 illustrates, tourist arrival numbers are improving month on month as a percentage of the pre-pandemic levels and in June they were 42.8% of 2019. This is encouraging as the Caribbean high season of December to April approaches. CBA’s manager states that the hotels within its portfolio (details of which can be found on page 8) are currently operating at around 50% occupancy and that it expects this to rise to 65% when the high season starts. As the number of long-haul flights from Europe to Cuba increases as air travel gets back to normal, visitor numbers and hotel occupancy levels are expected to improve further.

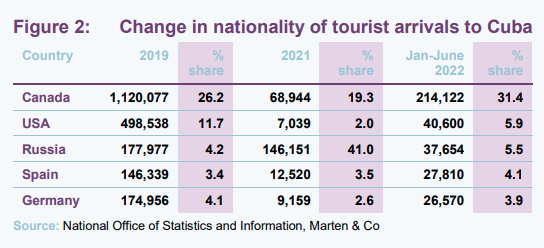

The number of Russian tourists to Cuba hardly fell throughout the pandemic, as shown in Figure 2, with 146,151 arrivals in 2021 compared to 177,977 in 2019, giving Cuba a much-needed boost as arrivals from other countries substantially dropped. However, Russia’s invasion of Ukraine has seen the number of tourists from Russia to Cuba fall dramatically this year, with the vast majority of the 37,654 visits so far this year coming before 24 February, when the invasion began. Russian visitors are unlikely to return any time soon.

Canadian tourists are again the dominant source of arrivals to Cuba this year, making up 31.4% of all arrivals in the first six months, having seen numbers depress significantly in 2021. Canadian arrivals are still below pre-pandemic levels, but with the high season approaching at the end of the year, figures could be boosted further.

Economic and political stability

Cuban economic reforms were announced in 2020 and accelerated in 2021 with the intention of providing greater autonomy to companies and stimulating private sector initiatives and foreign direct investment. This comes alongside political reforms. Miguel Diaz-Canel Bermudez succeeded Raul Castro as president in April 2018, becoming the first president that is not a Castro family member since 1976, while Raul Castro stepped down from the government altogether last year.

The economic reforms include monetary reforms and currency unification. Currency unification and exchange rate harmonisation was brought into effect on 1 January 2021, ending the dual currency system operating in the Cuban economy. The two Cuban currencies – the Cuban peso (CUP) and the convertible peso (CUC) – were unified through the elimination of the CUC. The CUP has an exchange rate of 1US$ to 24CUP.

The elimination of the double currency was intended to improve financial discipline, transparency and accountability within Cuba’s state-owned enterprises. However, economic uncertainty and the continuation of US sanctions has had a negative impact on the liquidity position of the country and complicated the implementation of the reforms. Significant inflation has ensued due to the scarcity of hard currency income to pay for imported products, triggering a fall in the informal exchange rate to around 150CUP to 1US$. This has provoked an undesired monetary arbitrage, with joint ventures, international airlines and all state-owned businesses obliged to use the official rate of 24CUP to 1US$.

Monetary reforms also include the decentralisation of hard currency payments made outside the country (including payment of dividends to foreign investors). The manager believes that this is a very significant step forward for the operations of Cuban foreign investment vehicles, providing them with real financial autonomy and reducing their dependence on centralised foreign exchange decisions. The ability of the Cuban government to implement the new financial autonomy rules has been weakened by ongoing liquidity constraints on the Cuban economy, but in time and with a full recovery of the Cuban tourism sector, the manager expects that the new rules will provide a sound and predictable basis to manage their international obligations in a timely fashion, including the payment of dividends to the foreign shareholder.

Whilst the monetary reforms and unification of currencies definitely adds short-term risk – especially given the poor liquidity position of the country due to the impact of the US sanctions and COVID – the changes that are being implemented should have a positive effect on the operations of the Cuban companies in which CBA has an interest, on future opportunities for the company, and on the attractiveness of the country as a foreign direct investment territory over the medium term.

Asset allocation

CBA’s real estate assets are owned though Cuban joint venture companies. CBA’s corporate structure was explained in more detail in our initiation note.

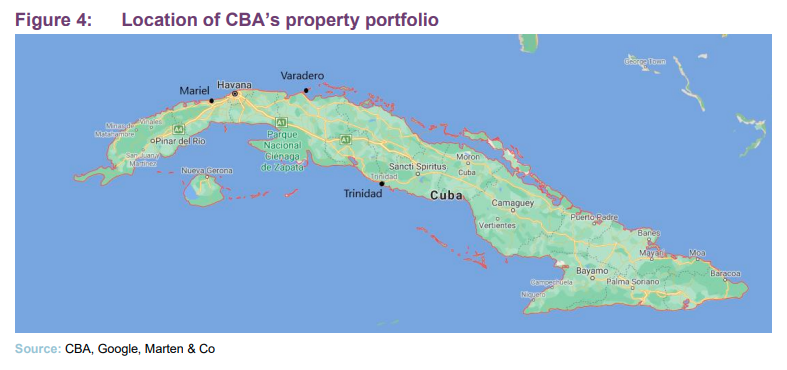

CBA’s portfolio comprises the Miramar Trade Centre office complex, the adjacent Meliã Habana Hotel, three hotels in Varadero (next to Cuba’s only 18-hole golf course), a new hotel construction in Trinidad, an industrial development in Mariel and various financial assets.

CBA’s assets are valued twice a year by independent RICS valuer Abacus using the discounted cash flow method. A higher discount rate was applied to value the portfolio at 30 June 2022 to reflect the economic issues facing the country.

Miramar Trade Centre

CBA owns a 49% interest in Monte Barreto, the Cuban joint venture company that owns the Miramar Trade Centre, with CBA’s interest valued at $53.1m on 30 June 2022 (December 2021: $67.7m) driven by an increase in the discount rate to 19.75% (December 2021: 12.8%) applied in the discounted cash flow model. The 55,530 sqm office complex is made up of six mixed-use office buildings at the core of the Miramar business district in Havana. It is the premier commercial office complex in Cuba and is the largest in terms of net rentable area. Space is let on short lease terms (typically one to two years) in order to facilitate the repositioning of tenants and the rapid resetting of rent levels. The complex has limited competition and in 2021 maintained 96.6% occupancy throughout the year and the manager expects occupancy levels to remain in the mid- to high-90% this year.

Net income in 2021 reached $15.6m for the year (up 8.5% on 2020), making 2021 the most profitable year since the incorporation of the joint venture. However, principally as a result of Cuba’s present liquidity situation and the uncertainty of the impact of Cuba’s monetary reforms on the joint venture company, CBA made a $12.3m provision regarding outstanding dividend receivables and lowered the fair value of its interest in the joint venture company.

Hotels

CBA has interests in four hotels in Cuba: a five-star hotel in Havana and three (four- and five-star) hotels in Varadero. The hotels have a total of 1,834 rooms and are all managed and operated by Meliã Hotels International (MHI).

CBA owns a 65% interest in HOMASI, with MHI owning the other 35%. HOMASI owns a 50% interest in Miramar, the Cuban joint venture company that owns the four hotels. Via this structure, CBA has an ultimate economic interest of 32.5% in the hotel assets. CBA’s stake in the four hotels was valued at $94.8m at 30 June 2022 (December 2021: $94.5m).

All four of the hotels currently operating under volatile and unpredictable market conditions, and the outlook for 2022 remains uncertain and depends on the recovery of international travel.

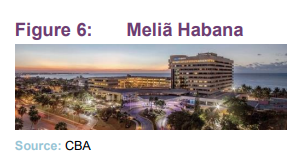

Meliã Habana Hotel

A 397-room (including 16 suites), five-star business hotel located on prime ocean-front property directly facing the Miramar Trade Centre, 10 minutes from the city centre and 15 minutes from the airport. The hotel offers conference facilities, numerous meeting rooms, a business centre and three executive floors.

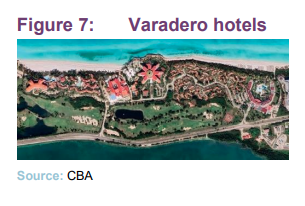

Meliã Las Americas Hotel

The Meliã Las Americas Hotel is a five-star luxury beach resort hotel located next to the Varadero Golf Course. It has 340 rooms, including 90 bungalows and 14 suites. It is located on 400 metres of beachfront and operates as an all-inclusive beach resort.

Meliã Varadero Hotel

The five-star Meliã Varadero Hotel is located adjacent to the Meliã Las Americas Hotel and the golf course. It has 490 rooms, including seven suites, and is located on 300 metres of beachfront. It operates as an all-inclusive beach resort.

Sol Palmeras Hotel

The four-star Sol Palmeras Hotel is located next to the Meliã Varadero Hotel and also borders on the golf course. It has 607 rooms, including 200 bungalows, of which 90 are of suite or deluxe standard. It is located on 500 metres of beachfront and operates as an all-inclusive beach resort.

Melia Trinidad Playa Hotel construction

CBA has a 40% economic interest in the TosCuba joint venture company that owns a hotel development project on a four-hectare beachfront site, just outside the town of Trinidad on Cuba’s southern coast. Trinidad and the nearby Valle de los Ingenios (the site of many historic sugar mills) are UNESCO world heritage sites. The hotel will, once completed, be a 401-room, four-star resort hotel.

Due to the pandemic, construction of the hotel stalled but the pace of construction has now ramped up to pre-pandemic levels and the estimated completion of construction is by the first quarter of 2023. CBA raised €25m in new funds through the issue of convertible bonds (with a coupon of 10% per annum) in March 2021, which is being used in part to complete the construction of the hotel.

Industrial development project in Mariel

In December 2020, CBA acquired a 50% interest in a new multi-phase industrial and logistics project in the Special Development Zone of Mariel. Construction of the first four warehouses of the project, which will total 11,000 sqm, began in the first quarter of 2021. In total, 12 to 16 warehouses can be built on the 11.3-hectare site. CBA paid an initial $303,175 for its 50% interest. The full investment of the company in the project is expected to be $1.5m.

The Special Development Zone of Mariel is located around 27 miles to the west of the city of Havana. It is connected by new road and railway links and its port is strategically positioned on the principal shipping route of the Gulf of Mexico, south of Florida and north of the Panama Canal.

As a Special Development Zone, the site has a distinct legal regime and special rules governing corporate, banking, tax, employment and other matters. There are 26 foreign capital companies and 12 joint venture companies currently operating or setting up operations in Mariel, including companies owned by Unilever, Nestlé and British American Tobacco.

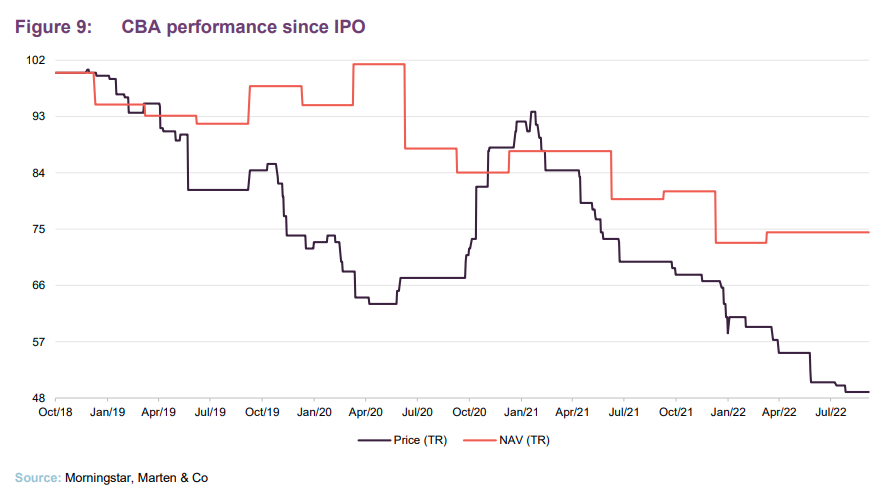

Performance

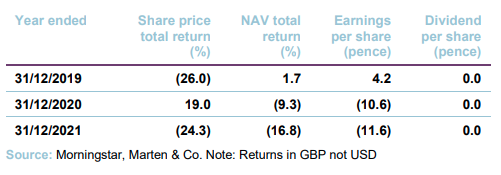

CBA’s NAV fluctuated from launch as the US sanctions on Cuba escalated under the Trump administration and impacted on the valuation of CBA’s portfolio, especially the hotel assets. The NAV is reported in both US dollar and sterling. The NAV here is in sterling and has been influenced by the prevailing dollar/sterling exchange rate. In dollar terms, the NAV has been less volatile. CBA’s NAV slumped to its lowest point in December 2021 as the valuation of its assets, especially the hotels, were heavily impacted by the COVID-19 pandemic, ongoing US sanctions and economic uncertainty in Cuba.

Discount

CBA’s discount to NAV had narrowed substantially from its lows in early 2020 during the pandemic after President Biden won the US election and the probability that US sanctions on Cuba would be reversed rose. This has taken longer to materialise than the market had been expecting which, when coupled with the spread of the Omnicom variant derailing the opening of international travel, widened the discount again and at 27 September 2022 stood at 55.0% (using an exchange rate of £1.00 : $1.0733 and CBA’s NAV at 30 June 2022 of $1.12).

Previous publications

QuotedData has previously published an initiation note on CBA – Primed for long-term growth, on 14 May 2020.

The legal bit

This marketing communication has been prepared for CEIBA Investments by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.