Industrial property market – the gift that keeps on giving

Industrial property market – the gift that keeps on giving

The industrial and logistics sector has been on a tremendous run over the past five years or so. It is hard to think now, given the current dynamics in the property industry, that retail and offices were the sectors of choice for investors for many years with industrial cast aside by most.

All that changed, primarily off the back of a fundamental shift in consumer buying habits. Amazon has become a behemoth and online-only retailers have popped up and taken significant market share from their high street rivals – operating from a network of warehouses across the country. The trend towards ecommerce, and its effect on both the industrial and retail sectors, is well-known. Consumer spending online has been growing dramatically to the point now where just under 20% of all retail transactions in the UK are made on the internet.

This has meant that traditional retailers, as well as their online-only peers, have been scrambling to get their distribution networks functioning efficiently. Long gone are the days of one huge warehouse in the middle of the country that served a retailer’s shops. It now needs several distribution centres that serve not only the shops but smaller logistics hubs close to major towns and cities, which in turn serve home deliveries. The invention of same-day – and even one-hour – deliveries has intensified the need for an efficient network and ultimately more industrial and logistics space.

The run of success in the sector, which has been on a continuous upward trajectory for more than five years, raises the question: how long can it last? How much further can rental growth go? Are investment yields, which are sub-4% for prime stock, sustainable? Is there too much speculative development in the market?

Here we explore the undercurrents that continue to drive the sector, further opportunities that exist and the threats that could curtail growth.

The different sub-sectors

The industrial property sector has several different sub-sectors that each have their own dynamics and nuances. It is important to understand each sub-sector, the fundamentals behind them, their role in the supply-chain and the companies that operate in each.

‘Big box’

At one end of the spectrum you have the so-called ‘big boxes’. As the name suggests, these are large warehouses used as distribution centres, ranging in size from 350,000 sq ft plus and more often close to and over 1m sq ft. They are strategically located close to major motorways and other transport hubs, such as rail freight, airports and shipping ports, and are usually let to a single tenant. They serve as the national or regional distribution centre for the tenant, most often an ecommerce business (which accounted for 53% of lettings in 2018) and are where goods or products start their journey to the customer’s doorstep or the shop floor. ‘Big boxes’ are highly automated, with tenants spending hundreds of millions of pounds (in most instances, far more than the building is worth) on technology to efficiently store and pick goods.

Of course, it’s not all about ecommerce. Tenants from an array of industries are active occupiers in the sub-sector, especially automotive businesses, which have historically been a big contributor to take-up. Listed companies operating in the sub-sector are SEGRO and Tritax Big Box REIT.

Logistics

The next sub-sector is logistics facilities. These are effectively parcel hubs located on the outskirts of towns and cities that predominantly service ecommerce deliveries to people’s homes and offices. They come in a wide range of sizes, with the big logistics facilities being between 200,000 sq ft and 350,000 sq ft.

Urban logistics is a fast-growing part of the sub-sector and, as the name suggests, are logistics facilities located very close to town and city centres and are in the 20,000 sq ft to 200,000 sq ft size bracket. With the growth of ecommerce, they have become more and more popular with retail companies and third-party logistics operators, which service retailer contracts, as they try to streamline their supply chains. The high level of demand from occupiers – coupled with a severe lack of supply given land constraints around most major cities – has pushed rents up and seen capital values increase.

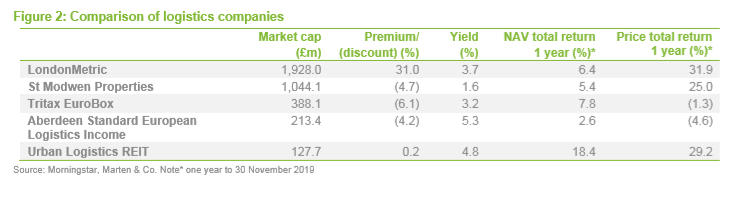

Companies in this sub-sector include Aberdeen Standard European Logistics Income, LondonMetric, SEGRO, St Modwen Properties, Tritax EuroBox and Urban Logistics REIT.

Industrial

The industrial sub-sector is made up of multi-let industrial estates with individual units sub-10,000 sq ft in size. Tenants of industrial estates are often small and medium sized companies, the life blood of the economy, and operate in a diverse number of industries. The supply of industrial estates has been diminishing over time, as schemes get bought up for residential redevelopment while new build stock is scarce. Leases tend to be a lot shorter in this sub-sector, owing to the nature of the tenants, and the assets are require more asset-management activity. Rental growth, as a result, is high. Companies in this sub-sector include SEGRO, Stenprop and Warehouse REIT.

Current state of play in the market

The sustained and prolonged nature of growth in the industrial and logistics sector has led some to declare that the sector is somewhere near the top of the market.

Strong occupational demand is still evident, however. Lettings transactions in the first half of 2019 were 28% up on the long-term average for the first half of the year, coming in at just over 16m sq ft, according to commercial real estate consultant Savills. The second quarter stats in isolation show that 9.55m sq ft was transacted, making it the second-highest level of second quarter take-up on record, only beaten by 2014. MSCI data shows that over the last five years, rents have increased for ‘big box’ distribution warehouses by 3.9% each year, on average.

The structural shift in consumer spending patterns has not just revolutionised the retail market, but is starting to spread into other areas. Demand for dark kitchens (warehouses that are kitted out with several kitchens for the purpose of home deliveries), for example, has surged as more and more people order food through apps such as Deliveroo, Just Eat and Uber Eats. Another example is reverse logistics. The growth in ecommerce, generous return policies and new consumer expectations have caused a real headache for retailers with regards to how they handle and efficiently deal with returned merchandise. Whilst returns have historically been a necessary cost of business, the growth in volume has presented a huge increase in demand for space specifically designed for processing returned items.

Technological enhancements, such as driverless vehicles, automation, artificial intelligence and predictive analytics, have and will continue to have a huge role to play in the future of the sector. Factor in the historically-low unemployment levels in the UK, and the issues that occupiers will continue to have with accessing sufficient labour pools, and the reliance on technology enhancements and innovations will only heighten. This will have a huge bearing on both future location hotspots for distribution centres and the design specifications of new facilities.

Developers have responded to the prolonged levels of strong demand. Nationwide, supply has risen in 2019 and now stands at more than 34m sq ft, according to Savills. However, vacancy rates are still low at 6.62% (against a 10-year average of around 12.5%). The rise in supply has predominantly come from speculative development and there are currently 34 units totalling 7.15m sq ft being built speculatively.

Most commentators state that the level of speculative development is sustainable given the high levels of demand that continue to exist for industrial and logistics facilities. However, the impact of speculative development – which has seen the proportion of supply that is classified as Grade A (the highest quality rating) rise to 56%, with the proportion forecast to grow further still – is likely to be some pressure on rental growth. Market forecast house Realfor has suggested that rental growth in ‘big box’ warehouses could be more subdued going forward, estimating a level of 1.8% rental growth a year until 2023.

Where will future growth come from?

Despite a prolonged period of growth and the sector exhibiting late-cycle tendencies, many opportunities for significant further rental growth exist in certain sub-sectors.

London

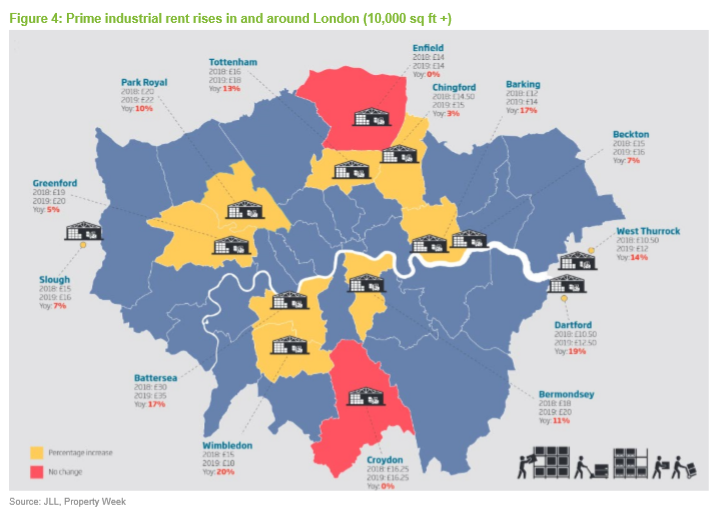

Many regions in the UK are severely supply-starved, due in part to chronically slow planning systems and a gradual loss of industrial land to other uses, such as residential. Unsurprisingly, the London market is the prime example of this. London’s population is expected to grow from 8.9 million today to 10 million by 2031, according to the Office for National Statistics (ONS). In a bid to satisfy this demand for housing, London’s industrial land has been sacrificed by London boroughs. Over the past decade, the capital has lost around 100 hectares of industrial land annually. At the same time demand for industrial and logistics space in and around the capital has skyrocketed due to increased consumer demand for online shopping and deliveries to homes or workplaces. This has put a huge strain on the logistics supply chain and created the perfect storm for rental growth. Demand has outstripped supply to such an extent that rents for industrial units in some areas of London have increased by as much as 20% in the last year alone. Figure 4 shows year-on-year rental growth in 14 locations around London.

Industrial and logistics developers are having to get creative to try to meet the demand. One such initiative that will become commonplace in the London industrial market is multi-storey development. If you can’t build out, build up. There is only one multi-storey industrial unit in the country, located close to Heathrow airport and owned by SEGRO (which inherited the asset as part of its acquisition of rival developer Brixton in 2009). It was built in a different era and although it is now fully-let, this is mainly due to the lack of supply rather than the characteristics of the building. SEGRO is leading the way on multi-storey development, however. It is yet to press the development button in London, but has proof of concept in Paris and Munich and it is only a matter of time before it implements the blueprint in the UK.

SEGRO’s Paris asset, Air2 Logistique, is let to Ikea and French DIY chain Leroy Merlin, and opened in March this year. SEGRO bought the site, five miles from central Paris, in 2013 and took the decision to speculatively build the 678,000 sq ft two-storey building. The gamble has paid off handsomely, with the company fully letting the building 11 months before practical completion. Its success is all down to the huge supply-demand imbalance and the design features, which include a 10m-wide ramp that allows vehicles to pass in both directions and a significant loading yard on the first floor so that the occupier gets as much operational effectiveness and efficiency as it does on the ground floor.

SEGRO has said it believes London shares similar characteristics to Paris, in terms of supply and demand, and is now looking at several sites in and around the capital to accommodate such a scheme. Obviously, the rental model for such an asset is appealing to developers, especially when land prices are at all-time highs. In all likelihood, rent on the upper floor is going to be slightly lower than the ground floor, but maximising rent from a confined plot of land will be a huge positive for the sector.

Another innovative solution to building the much-needed industrial and logistics space in London is the so-called ‘sheds and beds’ concept, whereby logistics facilities sit side-by-side with residential schemes. The concept is a simple solution to two of London’s biggest challenges: the desperate need to build more homes and the need to create more employment space, with London boroughs under huge pressure to provide both.

You may think people would balk at the idea of living next door to a warehouse, but it is something that has proven a success and mixed-use schemes like these are becoming the norm. In a city like London, where land is scarce, but population is growing, it is the only way. Although, perhaps it could only work in London, where living in close proximity to noisy establishments (be that a train station or bars and restaurants) is part and parcel of urban living.

SEGRO is currently on site with a ‘sheds and beds’ scheme at the former Nestlé factory site in Hayes, west London. The company sold two-thirds of the 30-acre site to residential developer Barratt London, which will deliver 1,386 flats, with SEGRO building 250,000 sq ft of industrial and logistics space across four units. Barratt London will use special noise-restricting glass on units closest to the warehouse to reduce any potential noise pollution and a row of trees will separate the two buildings.

Industrial mixed-use development is a concept that is only going to become more prevalent, and may even evolve. Builder’s merchant Travis Perkins has already worked in partnership with student accommodation providers, including Unite Group, to build units above some of its central London sites and is looking to roll out the concept across more of its estate. Commercial property consultant JLL said it was aware of at least 30 industrial schemes, which include multi-storey or mixed-use elements, that are in various stages of pre-planning, planning or development.

Severe supply shortage will continue to drive urban logistics

It is not just the London market that is experiencing severe supply shortages. Many regions across the UK have supply rates below 5%, and it is even more scarce in certain sub-sectors. One such sub-sector is urban logistics. The urban logistics sector has been one of the best-performing sub-sectors of the logistics market in terms of rental growth in recent years, and is expected to continue to outperform the wider market. Nationwide, rents are expected to grow on average 3% a year through to 2022, according to Savills.

Very few new urban logistics facilities are being built, especially outside of London and the South East, due to several factors including the high price of land and small scale of the buildings making construction non-viable for most developers. It has meant that the huge demand for the facilities from retailers is being met by an increasingly diminishing number of buildings. Some 8.5m sq ft of space was let in the UK in 2018 in the under-200,000 sq ft category. That, however, compares with new-build development running at 2.5m sq ft a year. This chronic shortage of new stock is likely to sustain buoyant rental growth for good-quality urban logistics assets for some time.

This is why LondonMetric has been steering its portfolio towards the sub-sector and was the driver behind its £415m acquisition of A&J Mucklow earlier this year. LondonMetric’s shift away from retail into the industrial sector, over the last few years has rightly been lauded as a masterstroke. It is now in the process of further refining its portfolio to be majority urban logistics. The Mucklow deal boosted the group’s urban logistics holdings to £826m, reflecting 35% of its total portfolio, and increased the value of its wider logistics platform to £1.65bn.

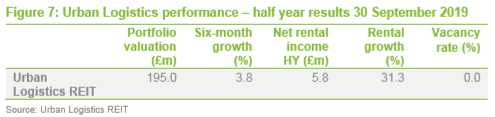

While LondonMetric is moving into the sub-sector, Urban Logistics REIT has been fully focused on the urban ‘last mile’ sub-sector from the outset. Launched in 2016, the company has amassed a portfolio worth £195m with a business model focused around growing rents through intensive asset management and improving the terms of shorter leases as they mature. In comparison, LondonMetric, which focuses on long-term income. Urban Logistics REIT operates in the 20,000 sq ft to 200,000 sq ft size bracket, with an average asset size of 60,000 sq ft, and the majority located in the South East and Midlands, where demand is strongest. In half-year results to the end of September 2019, Urban Logistics REIT reported income growth on a like-for-like basis of 3.1%, supporting a property value increase of 3.8% in the same period.

Against long-held convention in the property sector, it is actually better for logistics-focused companies to be buying property with short-term lease agreements in place in this current market, so that they can carry out asset management initiatives and re-let them at rates well above the previous level.

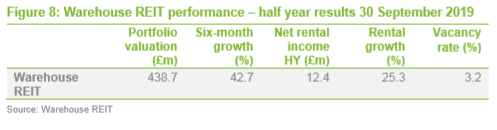

This model has proved successful for Warehouse REIT. In the six months to the end of September 2019, the company completed lettings on 43 vacant units across its portfolio at an average of 8% ahead of estimated rental values (ERV). The statistics on lease renewals are even more impressive. It conducted 57 renewals in the period at an average of 23.4% ahead of previous rents. The best example of this was a Boots-let warehouse in Basingstoke that had less than 1.5 years left on the lease when Warehouse REIT purchased it. In conventional property markets, this would be deemed a risky acquisition, but given the supply-demand dynamics and consequent upward pressure on rents, plus the group’s due diligence that identified the property as a key part of Boots’ supply chain, it proved a winner. In August 2019, Boots signed a 10-year lease renewal, with no breaks, at a rent that was 42% ahead of the previous level.

Serviced industrial model

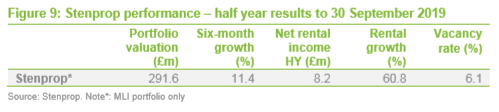

Stenprop, which listed in London in June 2018 and is building up a multi-let industrial portfolio, is providing a serviced industrial model to its tenants – much like the one that exists in the office market. It has proved to be very successful in the office sector, but arguably the model is probably best placed in the industrial sub-sector where a large majority of tenants are small and medium sized businesses. The concept is not new. Prior to the financial crash, several industrial-focused property companies had developed serviced operating platforms. However, the companies didn’t survive the recession and most of these models fell by the wayside. Stenprop has picked up the baton and run with it.

The company’s serviced industrial model works in the same way as serviced office space, fundamentally. Tenants pay a certain rate for the space that will cover utilities, IT and security, in addition to racking and machinery such as forklift trucks. Stenprop’s rationale is that by offering far more than the space it can significantly boost its revenue. Other real estate sectors, like student accommodation, have been successful in this and have seen 20% of operator revenues come from providing additional services.

Stenprop is also offering greater flexibility to tenants and is moving away from the traditional leasing model to allow customers to sign up for as little as six weeks on its Smart Lease online platform. Another benefit to the new flexible leasing structure is that it is three pages long, taking the friction out of moving in. The simpler format will cut the time it takes for a tenant to move in by 75%, thus reducing void periods.

Industrial property is also benefitting from the structural supply-demand imbalance of the wider sector. There is very limited supply because the cost of building an industrial estate is so high. Outside Greater London, where developers can get it to work because rents are higher, there is little-to-no new supply coming through. On the flip side, smaller businesses are driving demand. The number of small businesses in the UK has grown by 69% since 2000, according to the ONS, and they are attracted to industrial properties because of their location and versatility. They are also the cheapest form of real estate.

The industrial property market has benefited from the structural shift to ecommerce. There are many examples of independent shops, that once sold to the town, migrating their business online and moving to industrial estates in order to sell to the whole country.

The intensive asset management approach to growing income has been very successful, and only this month, Hansteen – the master of asset management in the industrial sector – announced it had agreed a deal to sell the company to Blackstone for around £500m.

Europe

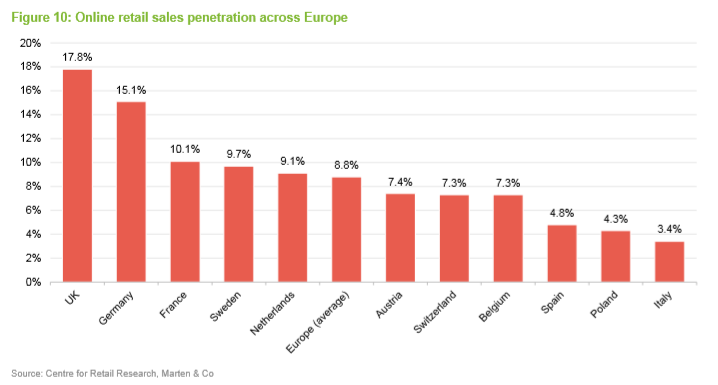

The UK is ahead of most western countries in terms of online sales as a percentage of total retail sales, where it is now pushing 20%. Sustained rental and capital growth over the past five years has seen yields in the UK market tighten to historically-low levels of around 4%. Although behind the UK, the European market is on a similar growth trajectory to that witnessed in the UK over the past five years.

In the UK, Savills identified a tipping point of 10.7% of total retail sales being online, which created rapid growth in occupational demand for warehouse space. Several countries, including France, Sweden and the Netherlands, have online penetration rates approaching 10.7% and it is expected that these countries will follow a similar trajectory in take-up volumes to that of the UK.

With less than 5% of total retail sales currently made online in Spain and Italy, these two markets are forecast to see the strongest online retail sales growth of all Western European markets over the next five years, according to Savills, at 17% a year and 21% a year respectively. Likewise, Central and Eastern Europe are predicted to witness an average growth of 17.5% a year.

Both Aberdeen Standard European Logistics Income (ASLI) and Tritax EuroBox expect to benefit from significant rental and capital growth going forward as penetration of online sales starts to kick in in Europe. Vacancy rates across Europe’s main markets are at historic lows, and in 2018 dropped to just 5.5%. These supply/demand dynamics should create significant rental growth, especially in more land-constrained urban locations.

Investment prices are comparatively better value than the UK – with average yields at circa 5% across Europe. Factoring in the significantly better financing costs in Europe, where financing costs are around 100 basis points (1%) lower than the UK, the yield spread (the gap between the rental yield and the cost of debt) is very favourable for European assets.

Development

Tritax Big Box REIT is in the process of transforming its business from the highly successful forward-funding model – whereby it would fund the development of a ‘big box’ facility that was already pre-let – to becoming the developer. In February this year, it bought an 87% stake in UK developer db symmetry, and its 2,800-acre land bank, for £373m.

The deal will allow the company, which has a portfolio of ‘big box’ warehouses totalling £3.8bn, to control the way in which it builds its portfolio, and bring forward development at a 7%-8% yield on cost. Yields in the ‘big box’ sub-sector have compressed to sub-4%, so moving into development was a logical next step for the company.

It has said that it aims to build 2.8m sq ft of distribution facilities per year, and has announced its first development since the acquisition: a 661,000 sq ft unit in Biggleswade, Bedfordshire, pre-let to The Co-operative on a 20-year inflation-linked lease.

The symmetry deal also allows the group to adapt to market conditions and deliver at an attractive price point. The majority of the land is on options, meaning that the developer has already struck a deal with landowners, giving it the option to buy the land at a later date at a discount to its future value. The company has said that typically they have been agreed at a discount of around 75% to 85% – a huge competitive advantage.

St Modwen Properties, long focused on housebuilding and retail, is growing its exposure to industrial and logistics through development. In its half-year results to the end of May 2019, industrial and logistics made up 39% of its portfolio by value and the company has stated that it could make up as much as 80% or 90% in the next few years.

The majority of development, on land that the company has amassed over a number of decades, is through speculative development (the majority of which is in the sub-150,000 sq ft size band). The total development cost of its committed pipeline of 1.6m sq ft was £142m in May 2019, with an estimated rental value of £10.4m, delivering a yield on cost of 7.7% when fully let.

Its long-term pipeline has the potential to deliver over 15m sq ft (10m sq ft of which already has planning permission) with an estimated rental value of £60m and a yield on cost of 8%.

There is no doubt that owning a land bank in locations that are supply starved and demand rich puts you at an advantage, especially when prices in the sector continue to rise.

Potential threats

Could an online sales tax throw a spanner in the works?

The prospect of an online sales tax is gaining traction. Retailers and the property industry have been campaigning for years about the unfair and archaic nature of business rates, and have lobbied government for an overhaul. This includes cutting business rates on bricks-and-mortar shops by 20% and making up the shortfall with a 2% levy on all online retail sales.

A campaign by a group of high-profile retailers, led by Tesco, called on the government to introduce an online sale tax in February 2019. A parliamentary inquiry issued a proposal for an online sales tax to help “level the playing field” and provide “meaningful relief” for bricks-and-mortar retailers that have been hit with higher taxes due to business rates.

Business rates are based on ‘rateable values’, calculated every five years by reference to property rental values and a multiplier that rises annually in line with inflation. The subject of business rates was addressed by all the major parties in the run-up to the general election, and it would appear that change is on the way. Whether that change will include an online sales tax remains to be seen. It was certainly mooted by former chancellor of the exchequer Philip Hammond.

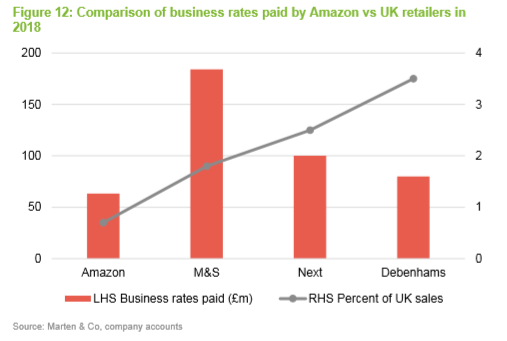

Figure 12 is a comparison of Amazon’s business rates bill last year, which amounted to £63.4m on sales of £8.8bn in the UK – around 0.7%, compared to traditional high-street retailers.

The effect of a 2% levy on pure-play online retailers would be huge. Amazon’s UK business would have to pay an additional £160m a year, according to UBS. Whilst this would still be less than 1% of Amazon’s group profit, other online-only retailers could be significantly impacted. ASOS, for example, would see pro-forma group profit before tax decline by 36%, according to UBS. It would probably have to increase its prices in a bid to offset the declines – making it less competitive and potentially impacting its future expansion plans.

Other firms with industrial exposure

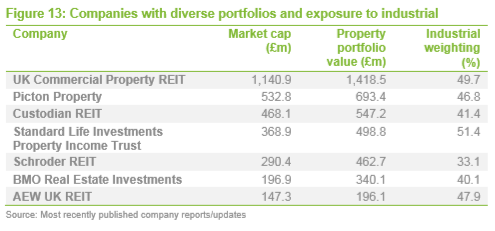

Many of the listed property companies have diverse portfolios with differing weightings to industrial. Here we round up those companies that have an exposure to industrial properties of more than 30% and compare their performance and strategies.

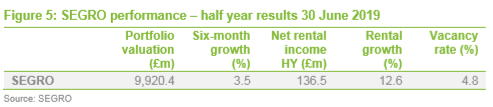

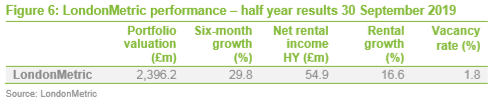

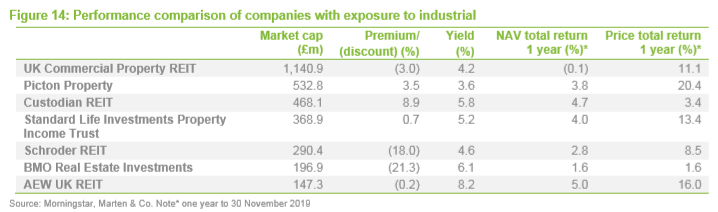

All seven companies mentioned above have significant exposure to the industrial sector. This has meant that their overall performance, has been better than their peers, with diverse portfolios more weighted towards other sectors such as retail and offices. The industrial sector has consistently outperformed the other core sectors in terms of capital growth and total returns for a sustained period of time. Figure 14 below shows the performance of the companies in the last year.

The legal bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.