Logistics safe haven with growth on horizon

As events unfold in Ukraine and inflation rages, the European logistics property sector should prove to be a safe haven for investors. One of the largest investors in the space, abrdn European Logistics Income (ASLI), has a growing portfolio that has significant inflation protection, with all of its rental income linked to inflation indexes and almost two-thirds uncapped (meaning it will rise annually with the rate of inflation).

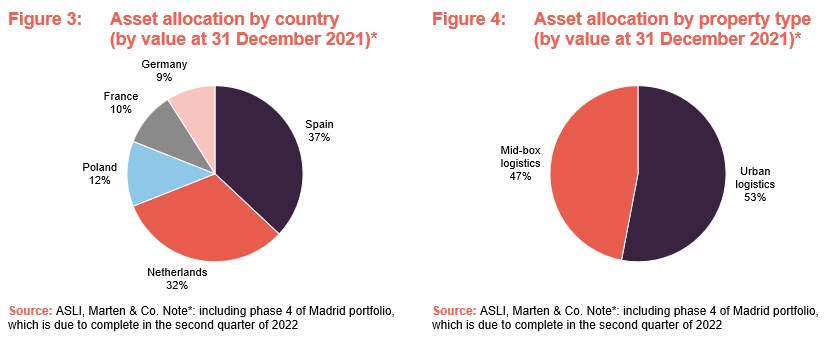

It has been a busy period of growth for the company, with the manager putting the proceeds from recent capital raises to good use. Its focus has been on urban logistics assets, which now account for 53% of the portfolio and which the manager says display superior rental growth potential. The group acquired an Amazon-anchored portfolio of urban logistics assets in Madrid for €227.3m in December, making the online retail giant its largest tenant. It is again on the acquisition trail following its most recent fund raise, and is in exclusive negotiations on the purchase of four new assets.

Mid box and urban logistics across Europe

ASLI invests in – and actively asset-manages – a diversified portfolio of logistics real estate assets in Europe with the aim of providing its shareholders with a regular and attractive level of income return, together with the potential for long-term income and capital growth (it has a target total return of 7.5% a year in euros).

Market overview

A lot has happened at ASLI since we published our last note on the company six months ago. The group raised £125m in September 2021 in a significantly oversubscribed placing and used the proceeds to acquire a portfolio of urban logistics assets in Madrid (details of which can be found on page 9). Earlier this year the company raised more money to satisfy near-term funding requirements. The success of this was heavily impacted by market volatility following an interest rate rise announcement and the escalation of the Russia-Ukraine war during the marketing period (more detail on page 11). However, it still managed to raise £38m (€45.6m) and with new debt facilities planned, the group is progressing with the acquisition of four new assets.

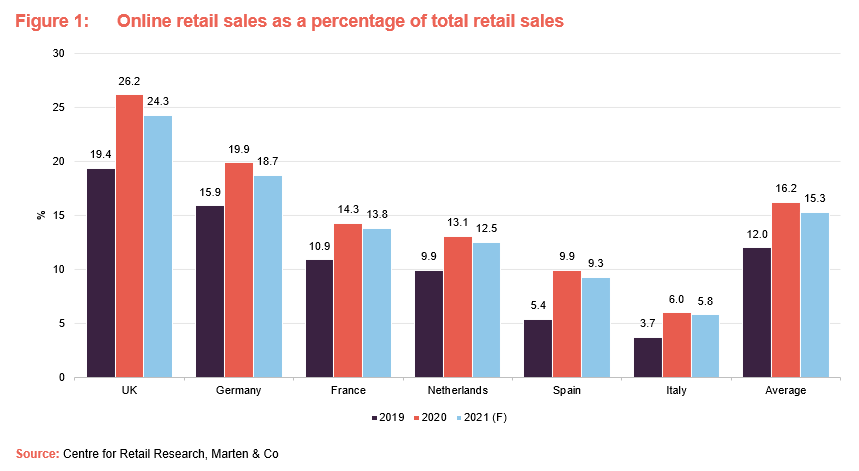

ASLI’s manager is eager to grow the portfolio during a period of significant tailwinds for the logistics sector. QuotedData has written about the favourable structural dynamics at play in the industrial and logistics sector many times, and those drivers are not going away any time soon (see page 14 of this note for details of our previous notes). To recap, an exponential growth in demand for logistics space in Europe has been brought about by a rise in online retailing and a strengthening of supply chains. This trend had been formed well before the pandemic, but has accelerated over the past two years as restrictions to curb the spread of COVID forced more retail sales online. Although online retailing penetration rates were expected to plateau and then fall slightly as physical retail stores fully re-open across Europe, as shown in Figure 1, the net gain during the pandemic is still expected to be considerable.

Much of this growth is expected to stick, with a whole new cohort of the population – such as older generations and other late adopters – and many retailers overcoming barriers to online retailing out of necessity and becoming comfortable in buying or selling goods in this manner. Forrester Research forecasts that online retailing will average 25% of all retail sales across Europe by 2025 (from around 15% today).

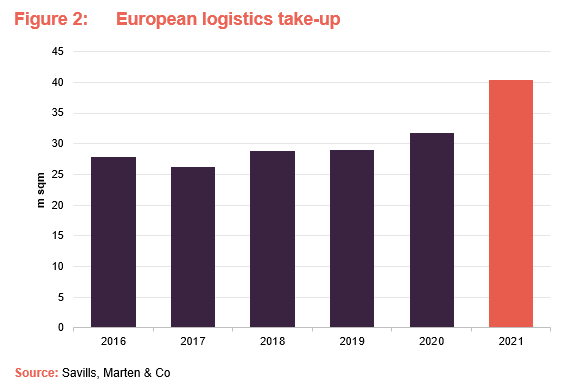

Whilst online retail is the biggest driver of demand for logistics space, it is not the only factor. Supply chain resilience has moved up the agenda for businesses following shocks during the pandemic. This is expected to result in shorter supply chains, with a re-shoring of manufacturing to Europe from Asia and an increase in inventory levels of around 5% to 10%, according to US logistics behemoth Prologis. The take-up of logistics space reflects these trends, as shown in Figure 2, where European logistics take-up reached just over 40m sqm in 2021, marking a record year of leasing activity and 40% ahead of the previous five-year average, according to Savills. Germany (8.6m sqm), the Netherlands (6.9m sqm) and Poland (7.3m sqm) drove leasing activity, whilst France (+63%) and Spain (+62%) performed the strongest against their five-year average take-up levels.

Supply of new, modern logistics facilities has not kept pace with rising demand, resulting in European logistics vacancy rates falling from 5.1% to 3.5% over the course of 2021, according to Savills. The manager says speculative development (whereby developers build property with no tenant signed up) has not progressed at any meaningful rate, with most logistics development being made on a build-to-suit basis (whereby developers build new property with a tenant already signed up to the scheme). Supply constraints are exacerbated by the scarcity of land around most major European cities and competing property use classes, such as residential.

The supply-demand imbalance has led to significant rental growth across Europe, with prime rents rising by 5% year-on-year, according to Savills (prime property is the most desirable, and therefore typically the most expensive, property in a particular location). The manager expects sustained rental growth across the major European logistics markets over the next few years.

Given the favourable characteristics at play in the European logistics sector, it was no surprise that investment volumes reached record highs in 2021 of €62bn, according to Savills, a 79% increase on the five-year average. Savills’s research also shows that the weight of capital targeting European logistics has seen average prime yields compress by 27 basis points (0.27%) to 4.2% over the last six months.

Focus grows on urban logistics

Although the supply-demand dynamics are positive for the logistics market as a whole, ASLI’s manager believes that these are amplified in the urban logistics sub-sector. Accordingly, the manager has progressively increased the group’s exposure to the sub-sector over the past few years, and following its most recent acquisition of a portfolio in Madrid, it now makes up 53% of the portfolio – with the rest made up of mid-box assets (more detail on the portfolio make-up is on page 7).

Urban logistics assets are characterised as being the final part of a product’s journey in the supply chain to homes or businesses. They are located close to towns and cities, and on arterial roads, and are typically between 5,000 sqm and 20,000 sqm in size. The growth in e-commerce has resulted in strong growth in demand for urban logistics space, where tenants (often third-party logistics operators) can be as close to consumers as possible.

The manager says that being close to customers solves two of the biggest problems for e-commerce companies – delivery times and transportation costs. The cost of renting a logistics facility pales in comparison to the delivery costs and being close to major conurbations makes financial sense to tenants, the manager states. As consumers have become accustomed to speedy delivery times for online orders – often same-day or next-day – location is mission-critical for e-commerce companies.

Supply of urban logistics properties is even more acute than the wider logistics sector, the manager states. Land close to large cities is at a premium and decades of industrial land being lost to residential development has seen supply dwindle. This adds up to substantial rental growth expectations, the manager states.

Increasing exposure to assets with high growth expectations – such as urban logistics assets – is one of the manager’s three-pronged strategy for achieving greater returns. The other two are focused on high yielding assets – such as properties in Poland where yields are around 125 basis points (1.25%) higher than in more mature markets – and value-add opportunities where the value of the asset can be enhanced by asset management initiatives such as building extensions on the site and adding income producing solar panels to roofs.

Impact of rising inflation

ASLI’s portfolio is in good shape to capture the rising rate of inflation in Europe, measured at 5.1% in January 2022 across the Eurozone, through its 100% index-linked income. All of ASLI’s leases are linked to inflation, with 65% uncapped – meaning it will rise in line with inflation, which could top 7% this year or even higher, depending on events in Ukraine. A further 28% of the income is inflation-linked with a cap in place (an upper limit) – usually between 2% and 4% per annum.

The manager says that the high inflation rates being felt in the construction sector (for example the cost of steel has almost doubled over the last year) should not be too much of an issue for the logistics sector, with higher construction costs feeding through to higher rents.

Russia-Ukraine war – limited impact on European logistics sector

Historically, as geopolitical uncertainty increases, safe haven investments have thrived. With the structural fundamentals of the European logistics sector in good health, as described above, and not likely to change, the contractual rental income and long-term visibility of income makes logistics real estate a safe haven investment, the manager argues. As mentioned previously, with inflation already rising and the potential for further sharp increases in energy costs as the war in Ukraine progresses, the inflation linkage in ASLI’s revenues is another attraction.

Asset allocation

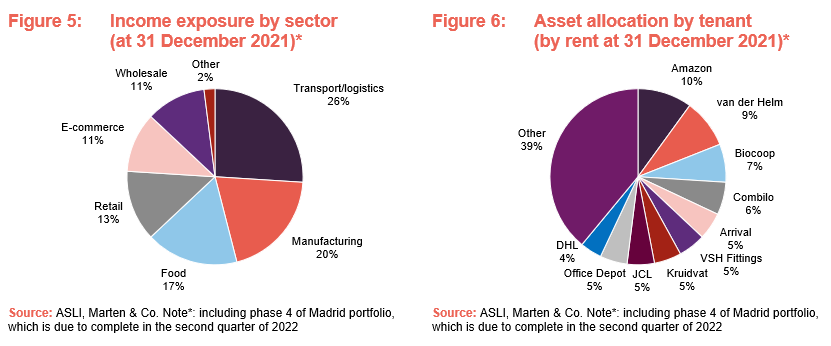

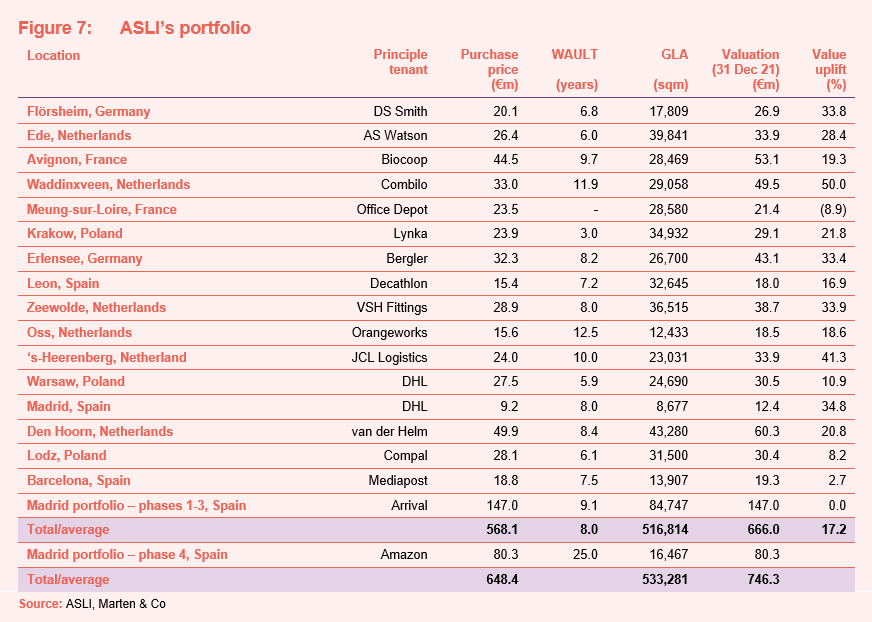

In December 2021, ASLI acquired a portfolio of urban logistics assets located in Madrid for €227.3m. The portfolio consists of seven logistics assets and one development site, which is pre-let to Amazon – more detail on the portfolio is on page 9. Following the acquisition, ASLI’s portfolio now consists of 24 assets valued at around €746m and located across five European countries. ASLI’s portfolio has 50 tenants, with Amazon being its largest tenant by income, and has a weighted average unexpired lease term (WAULT) of just over nine years.

Urban logistics assets now make up 53% of the portfolio, following the Madrid portfolio acquisition, where the manager believes greater growth potential exists, as mentioned earlier. All of ASLI’s income is linked to inflation, with 65% uncapped – meaning it will rise in line with the relevant inflation index in place in that country. A further 28% of the income is inflation-linked with a cap in place – usually between 2% and 4% per annum.

The group collected 98% of rent due in 2021. The outstanding rent relates to Office Depot France, the sole tenant at ASLI’s Meung-sur-Loire asset in France, which fell into administration in February 2021. Stationery and office supplies retailer Nouvelle Victoire acquired the majority of the Office Depot France business and integrated the majority of the Office Depot stores into its existing network. Nouvelle Victoire has terminated its tenancy of the warehouse, but the manager says that it has requested to use around half of the space until July 2022, for which it will continue to pay rent. Rent owed in respect of the property amounts to €503,000 and the manager expects this to be paid now after the administrator sold the inventory stored in the building. ASLI also has a three-month rental security deposit held at bank that it can recoup. In the meantime, the manager says that it is confident of finding a new tenant and has carried out several recent viewings. Such is the manager’s confidence, the group recently rejected a bid for the asset, which was above its current valuation of €21.4m.

The Madrid portfolio

After raising £125m in September 2021, ASLI acquired a portfolio of urban logistics assets located just outside Madrid for €227.3m, reflecting a net initial yield of 3.4%. The portfolio was acquired in four phases and consists of seven newly-built warehouses and an under-construction property. The rental income of €7.7m is subject to annual uplifts linked to inflation, with the leases having a WAULT of 14.8 years (8.7 years to first break). Online retail and logistics giant Amazon makes up 43% of the income across two assets, while other tenants include Carrefour, Arrival, MCR and Talentum. The portfolio’s location, in Gavilanes, is one of the leading last-mile logistics areas in both Madrid and the wider Spanish market, according to the manager, with a population of almost six million people accessible within a 30-minute drive time.

Phase one

Phase one comprises two warehouses that were built in 2019. The first building extends to 21,713 sqm and is let to Talentum, an online marketing company, for a further eight years with annual uplifts linked to IPC (Spanish Consumer Price Index) capped at 3%. The second building, measuring 11,264 sqm, is let to Amazon for a further 8.5 years, with a break option after 1.6 years. The rent is also linked to IPC with a cap of 3% per annum.

Phase two

The three warehouses that make up phase two include Carrefour’s first Spanish e-commerce facility. The French supermarket giant has 14.6 years left on its lease at the 8,241 sqm warehouse. MCR, a Spanish electronics and IT hardware distributor (which lists Amazon as its main client) occupies the second building, which extends to 6,660 sqm. Its lease expires in four-and-a-half years. Both leases are linked to IPC with a 2% cap. The third building is 6,356 sqm and is vacant, with a 12-month rental guarantee from the vendor.

Phase three

Phase three is made up of two newly-developed warehouses, measuring 16,500 sqm and 10,665 sqm, both let to Arrival for just under 10 years, linked to IPC. Nasdaq-listed Arrival makes electric delivery vans and counts global logistics specialist UPS as one of its clients. The manager says that the site, which was completed in 2019, is one of Arrival’s key European hubs.

Phase four

Phase four is currently under construction and comprises a 16,467 sqm parcel delivery hub and an adjacent multi-storey van parking station fully equipped for electric vehicles. It is pre-let to Amazon on a 25-year lease, with upward only annual rent reviews linked to IPC (capped at 3%). The development is expected to complete in the second quarter of this year.

ESG

ASLI has been awarded four green stars out of a maximum of five by the Global Real Estate Sustainability Benchmark (GRESB) survey after making significant progress with ESG across its portfolio. The portfolio’s GRESB score of 84/100 compares favourably to many peer groups – it is first out of six listed European industrial funds; eighth out of 57 European industrial companies; and sixth out of 94 in the listed European sector. The company was also awarded Regional Sector Leader status.

ESG initiatives include a significant roll-out of solar panel installations, a tenant satisfaction survey, LED lighting in all buildings and 100% data collection across the portfolio linked to Envizi, which is used to analyse energy consumption. Rooftop solar panel systems exist on 10 properties within its portfolio, generating €260,000 of income annually and green energy for tenants. The manager is actively exploring the possibility of adding to or enhancing rooftop solar panels across its portfolio during 2022.

Equity raise and near-term funding pipeline

On 2 February, ASLI announced that it had raised €45.6m (£38m) through a placing and retail offer under its share issuance programme. The manager says that the group was hoping to raise more, but macro events made the timing difficult – with the announcement of interest rate rises and the Russia-Ukraine conflict intensifying during the fundraising efforts. ASLI’s share price fell below that of the issue price of 110p for part of the marketing period but recovered towards the closing date.

The group now plans to put in place finance to fund its near-term investment requirements. This will bring its loan to value ratio close to its target 35%, from 25% currently.

The near-term funding requirements include €73m to acquire phase four of the Madrid portfolio, mentioned above, which is due by the end of June 2022. The manager is also in exclusive negotiations on the acquisition of four assets, a mix of urban logistics and mid box distribution properties for around €49m. Three assets are located in France, on long-term leases with a French national third-party logistics provider, and the fourth asset is located in the Netherlands let to a food-focused operator. The manager says that all four assets have low site coverage, offering potential development opportunities in the future, while benefitting from inflation-linked rental income.

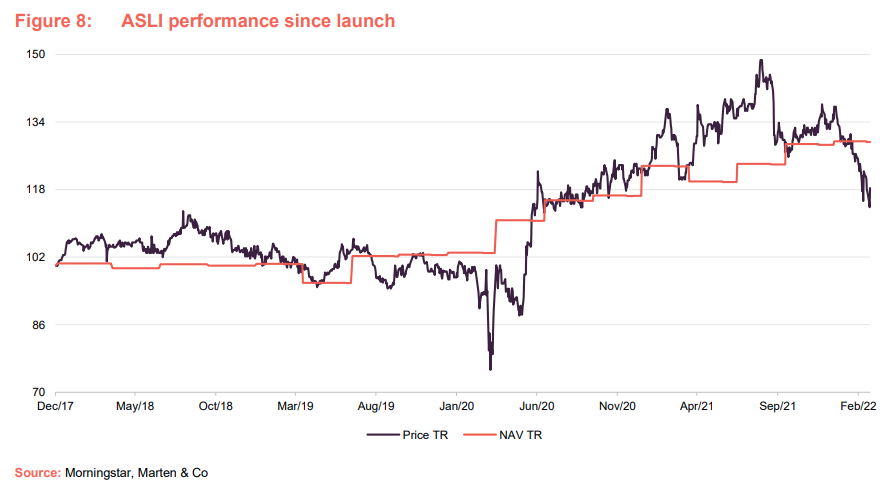

Performance

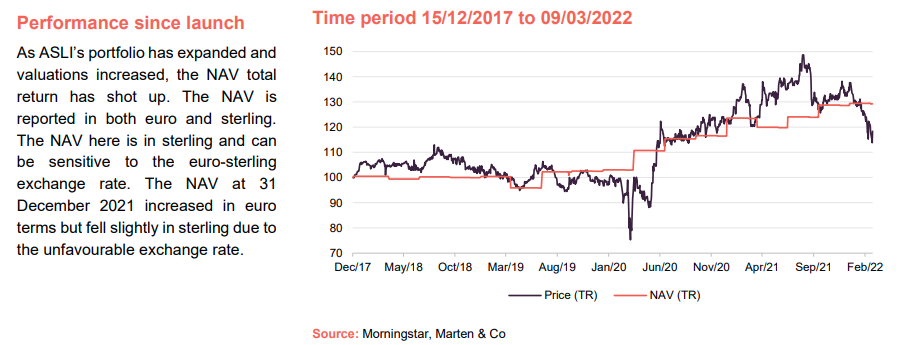

ASLI’s NAV initially made modest progress from launch, with rising property values offset by expenses incurred in establishing the portfolio. As the portfolio has expanded and valuations increased, the NAV total return has shot up. The NAV is reported in both euro and sterling. The NAV in Figure 8 is in sterling and can be sensitive to the euro-sterling exchange rate. The NAV at 31 December 2021 increased in euro terms but fell slightly in sterling due to the unfavourable exchange rate.

Peer group

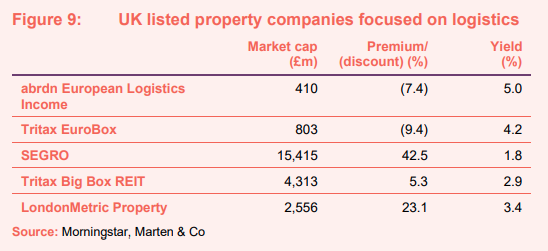

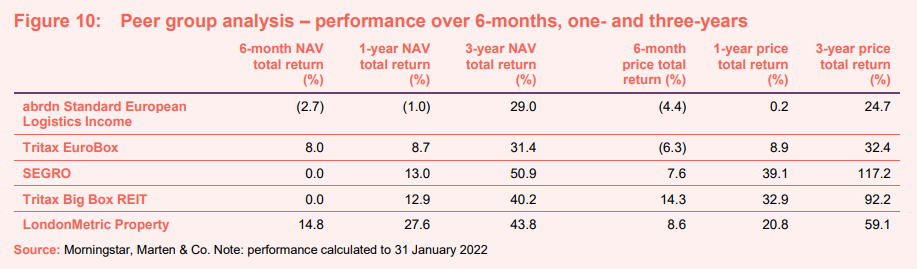

Most of those investing in European logistics are unlisted funds or subsidiaries of larger groups. The listed peer group we have assembled consists of: Tritax EuroBox, ASLI’s closest peer; SEGRO, which owns a mixture of ‘big box’, urban and industrial space (about a third of which is located in continental Europe); Tritax Big Box; and LondonMetric Property. The latter two are UK-focused.

ASLI is at the smaller end of this peer group, as it continues to grow its portfolio. The yield is superior to peers, and over the last three years it has produced solid NAV and share price total returns.

Premium/(discount)

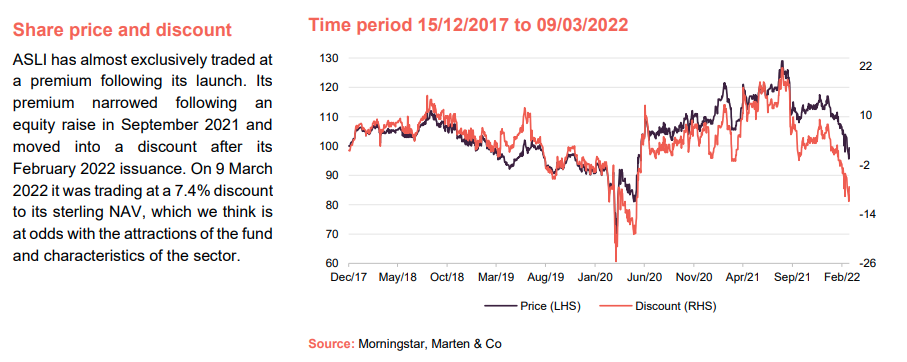

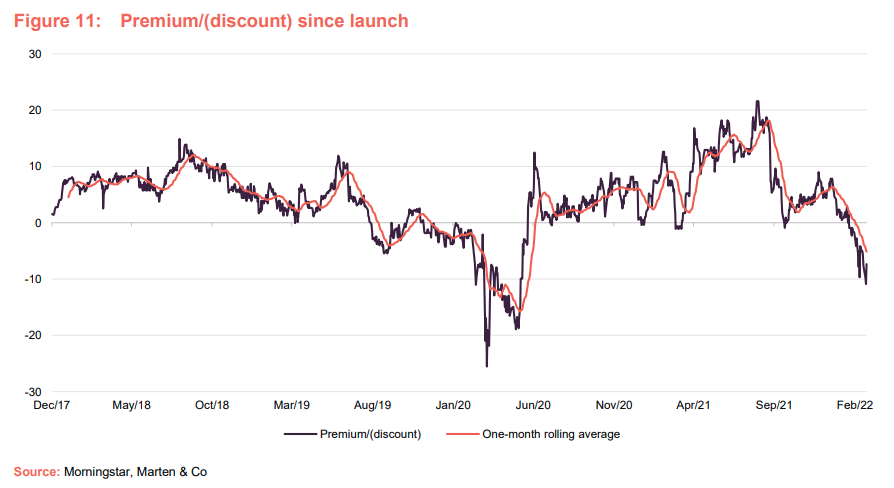

ASLI almost exclusively traded at a premium following its launch. Its share price slumped in March 2020 as part of a wider market sell-off as the COVID-19 pandemic hit, with its discount to NAV widening to 26%. It quickly regained its losses and as the market recognised the strength of its portfolio and the burgeoning logistics market, its rating moved to a premium. Its premium narrowed following its equity raise in September 2021 and moved into a discount after its February 2022 issuance. On 28 February 2022 it was trading at a 4.1% discount to sterling NAV, which is at odds with the attractions of the fund and characteristics of the sector mentioned on previous pages.

Fund profile

ASLI invests in a portfolio of European logistics assets, diversified by both geography and tenant, with a focus on well-located assets at established distribution hubs and within population centres. ASLI’s aim is to provide its shareholders with a regular and attractive level of income return, together with the potential for long-term income and capital growth (it has targeted a total return of 7.5% a year in euros).

ASLI has an annual dividend yield target of 5% of the IPO price (100p). Dividends have historically been paid in sterling, with the assets and the income derived from them predominantly in euros. The manager may use currency hedging to help reduce the volatility of the income, but there is no current intention to hedge the capital value of the portfolio. Going forward, shareholders will also be able to elect to receive distributions in euros.

ASLI’s portfolio management services are undertaken by Aberdeen Standard Investments (ASI), led by Evert Castelein. Aberdeen Standard Investments Real Estate is the second-largest European real estate investment manager, managing €45bn of real estate, and has an extensive regional presence, with over 225 real estate investment professionals and offices in eight countries across Europe.

In 2021, ASI acquired a 60% stake in Tritax Management, the manager of Tritax Big Box REIT and Tritax EuroBox. As part of the deal, Tritax partners will lead ASI Real Estate’s Global Logistics team. Tritax and ASI have said that Tritax Big Box, EuroBox and ASLI would retain their investment decision-making autonomy and control following the deal. ASLI’s manager says that the tie-up will improve the ability to source deals for the fund.

Previous publications

QuotedData has published five previous notes on ASLI. You can read them by clicking the links below.

Poised to grow? – initiation note, published March 2019

On the crest of a wave – update note, published October 2019

Resilient to COVID-19 – annual overview, published June 2020

Expansion on the radar – update note, published December 2020

Handbrake off in growth drive – annual overview, published September 2021

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on abrdn European Logistics Income Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.