The show must go on

All eyes have been on India over 2021 as it has outperformed even the US, despite suffering from one of the deadliest waves of the COVID-19 pandemic earlier this year. Combined with improved stock selection and its new investment policy, India Capital Growth (IGC) has also seen its performance shine through.

All eyes have been on India over 2021 as it has outperformed even the US, despite suffering from one of the deadliest waves of the COVID-19 pandemic earlier this year. Combined with improved stock selection and its new investment policy, India Capital Growth (IGC) has also seen its performance shine through.

The adviser, Gaurav Narain, highlights the start of a new economic cycle and the returning of profitability which had previously been at all-time lows. Meanwhile India is also benefiting from extra capital via the China Plus One strategy and a government that is now prioritising growth over reform and giving extra support to private companies. These developments are particularly timely as IGC can enjoy increasing traction ahead of its redemption vote at the end of the year.

Mid- and small-cap listed investments in India

IGC’s investment objective is to provide long-term capital appreciation by investing (directly or indirectly) in companies based in India. The investment policy permits the company to make investments in a range of Indian equity securities and Indian equity-linked securities. The company’s investments are predominantly in listed mid- and-small-cap Indian companies.

Fund profile

IGC is an investment company listed on the Main Market of the London Stock Exchange. It invests in India, predominantly in listed mid- and small-cap Indian companies. The fund is aiming to generate capital growth for shareholders. IGC has not paid dividends in the past and the fund adviser says it is unlikely to do so in the near future.

While IGC’s main focus is on Indian mid- and small-cap companies, the fund can and does hold large-cap stocks as well. The board and the manager use the S&P BSE Mid Cap Index (total return) for performance evaluation purposes, although the portfolio is not constructed with reference to this index. The other funds in IGC’s peer group benchmark themselves against the MSCI Index and therefore we have included this index within the report as well.

Management arrangements

IGC has been managed since 2010 by David Cornell of Ocean Dial, a company owned by Avendus Capital Private Limited, which in turn is backed by KKR. He has been assisted in this since November 2011 by Gaurav Narain of Ocean Dial Asset Management India Private Limited, which is based in Mumbai. This month marks Gaurav’s ten-year anniversary as adviser to the trust, during which time the underlying portfolio has grown at a CAGR of c.14%.

Gaurav has over 25 years of experience in Indian capital markets, having started his career as vice president of research for SG Asia. The seven-strong investment team is split between London and Mumbai. Each of the analysts is assigned responsibility for several industry sectors. The manager is responsible for monitoring portfolio risk and all dealing is done from London.

Ocean Dial manages two funds investing in India: IGC and an open-ended fund, Gateway to India fund. Ocean Dial had AUM of $330m at the end of

October 2021.

Alignment of interest

Employees of Ocean Dial and members of IGC’s board collectively hold 381,581 shares in the company, which represents 0.34% of its issued share capital.

Redemption vote

The introduction of a redemption facility last year gave shareholders the right to request the redemption of part or all of their shareholding on 31 December 2021 and every second year thereafter at an exit discount equal to a maximum of a 6% discount to NAV per redemption share.

This means shareholders can exit the fund should they wish, but investors will also get the chance to buy stock at this level, which may look attractive if the trust’s discount continues to narrow and with India expected to outperform in the years to come. Furthermore, the board has determined that the exit discount for the December 2023 redemption point will be a maximum of 3%.

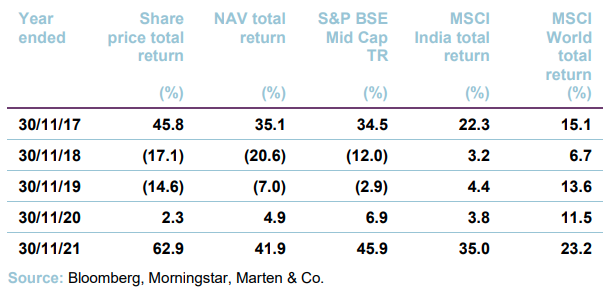

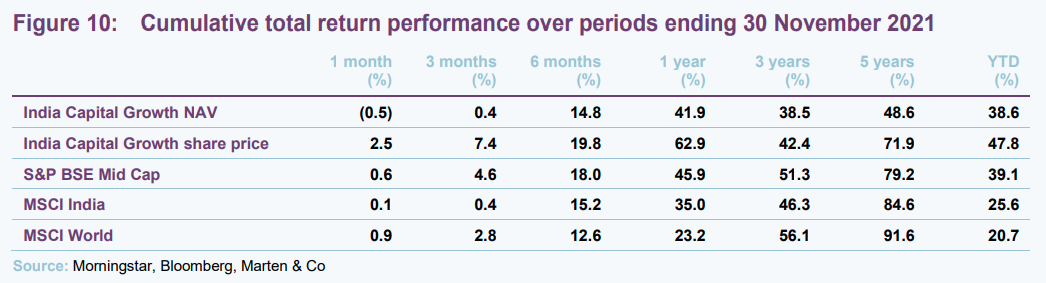

IGC is currently trading on a discount of 9.7%, which the board and the manager would like to see eliminated altogether (we talk more the company’s discount history on page 19). This may be possible, especially considering the strong performance numbers it has delivered this year and as revealed in its most recent results. For the six months to 30 June 2021, IGC’s share price total return was 31.7 per cent and its NAV return was 25.1 per cent, outperforming the BSE Midcap TR Index. Over the past six months, the discount has narrowed to as much as 4.95%, see in late October.

We continue to think that the trust would respond well to any improvement in India’s economy. We think that if the narrative change that the adviser highlights under the fund adviser’s view section continues, and IGC’s portfolio companies continue to see a marked uplift in performance, this is likely to provide momentum for the discount to continue to narrow, particularly as markets turn their focus towards India’s attractive valuations looking over the long-term.

Indian capital gains tax provisioning

IGC is liable for capital gains tax (CGT) in India. Although CGT is only payable at the point at which the underlying investments are sold, and capital gains are crystallised, IGC must provide for this additional cost. However, it should be noted that the actual capital gains tax paid may differ significantly from IGC’s provision and, depending on performance, it may not actually be crystallised.

For the year ended 31 December 2020, no CGT provision was necessary. However, IGC has accrued significant capital gains so far during 2021 which, in conjunction with a review from the India Tax Agent of the unrealised Indian CGT attributable to IGC’s investment portfolio as at 30 June 2021, IGC is required to accrue a deferred tax provision of £3.42m. This is equivalent to a reduction in IGC’s NAV of 3.04p per share, or 2.4% of the NAV as at 30 June 2021.

Since 30 July 2021, a deferred tax provision for Indian CGT has been reflected in IGC’s daily NAV estimate. IGC now discloses its NAV both before and after the CGT provision, which it says is to facilitate a meaningful comparison of investment performance.

Market outlook

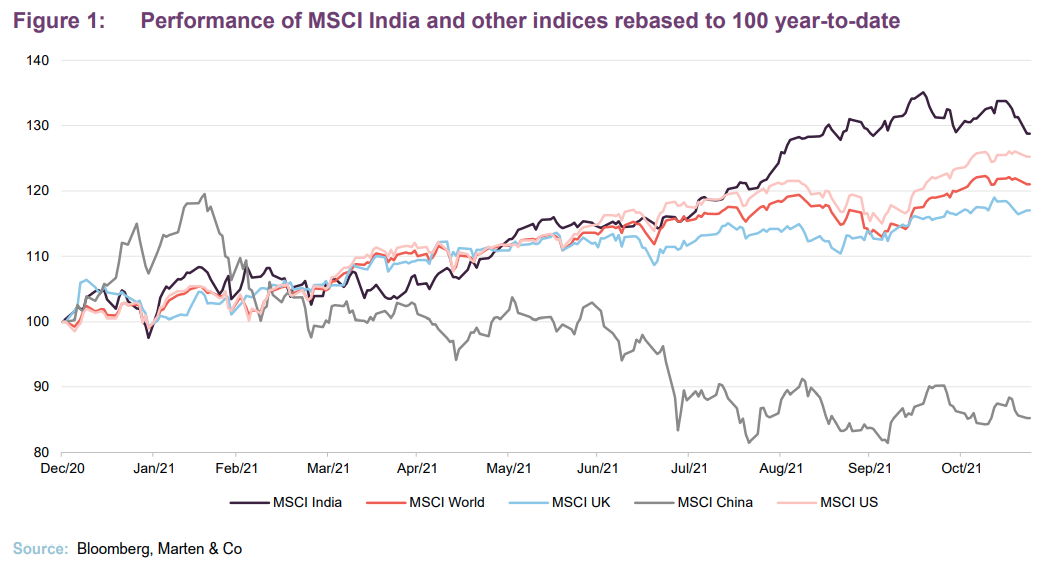

India has been one of the best performing markets of late, with the MSCI India returning 30.3% over the past 12 months ahead of even the MSCI USA, which has delivered 27.8% over the same period. India also tops the MSCI World which is up 23.3%, the MSCI United Kingdom, up just 16.9%, while neighbouring China is down 16.8% over one year.

This spectacular performance has come even as India became victim to a deadly wave of the coronavirus earlier this year, which saw more than 400,000 deaths and over 30m cases – and these are only reported instances. As outlined in our last note, Lessons Learnt, the country and its government learned from the mistakes it made during the first wave of the pandemic in 2020 when it imposed a full lockdown. This time around, states opted for more limited curbs which did initially temper consumer spending and dampen manufacturing activity but as the country began to re-open, economic conditions and investor confidence improved swiftly.

Notably, upbeat signals in the housing cycle, recovering capital spending, higher tax collections from goods and services and rebounding factory activity all point to an economy in the early stages of a recovery to pre-pandemic levels. Furthermore, investment bank Jefferies recently said India’s economic cycle suggests conditions are ripe for annual economic growth of between 8% to 9% over coming years.

While there is still uncertainty around the coronavirus, India’s economy is finally in a place to reap the rewards of years of regulatory reform, a focus towards growth and somewhat of a digital revolution. Meanwhile, capital is rotating out of China over worries around regulatory tightening across multiple sectors there while signs show global businesses are taking up the China Plus One strategy and avoiding investing only in China and diversifying into other countries. IGC says India has been one of the key beneficiaries of this. There have also been some IPOs in the Indian technology space which has attracted even further fresh capital, and Gaurav highlights the potential for a huge a pipeline to follow. We talk about this in more detail under the fund adviser’s view.

Foundations are being laid for the start of a highly anticipated pickup in economic growth with the market trading well above its long-term averages and earnings growth starting to pick up. Meanwhile, concerns from earlier this year such as the higher level of bad loans following the deadly second COVID-19 wave appear to be reversing.

Reform agenda playing out

Prime Minister Narendra Modi’s time in power has been largely taken up with reforming the country. The Goods and Services Tax and Insolvency and Bankruptcy Code have now been around long enough to see their positive impact while the larger banknote demonetisation among other reforms has weeded out a good chunk of India’s black money and corruption.

Companies have passed through the country’s new regulatory system, and many have come out the other side for the better. While banks have yet to fully start lending again, they are managing both their accounts and customers more efficiently.

More recent policy initiatives have also boosted sentiment, such as the National Monetisation Pipeline (NMP) unveiled by the finance minister in August this year. The government will lease out state-owned infrastructure assets, including roads, railways, airports and power plants, to private operators for a specified period, before reinvesting the returns into new infrastructure projects under the previously announced National Infrastructure Pipeline. This will provide the government with access to additional income streams to raise the capital required for new infrastructure investment and could also unlock efficiencies, particularly in areas of asset management and maintenance.

Meanwhile, the introduction of the government-backed so-called “bad bank” to clean up India’s $27bn debt mountain should help lenders’ balance sheets and provide fresh liquidity. It will take on stressed assets from these lenders and try to recover their value, which should eventually bolster credit growth and support economic activity. Whether it will be effective in tackling the root issue of poor lending practices remains to be seen.

With much achieved – and still proving fruitful – in terms of his reform agenda, Modi can now focus on the more mundane activities of running the country and put growth at the top of his list of priorities.

Fund adviser’s view

IGC’s adviser, Gaurav Narain, says the shift in the narrative that investors may have been looking for in India is finally here. After almost two years of continual outflows from institutional funds dedicated to Indian equities, he believes the fasting period is over and that India looks set to be the long-term investment of choice.

There are a number of reasons for this change but the themes he is focusing on at the moment are the promotion of growth to the top of the government’s agenda and the digitalisation of India’s economy. He also notes that confidence is returning to businesses across the country and that profits have held up relative to expectations despite the second lockdown, principally because the economy was able to continue as best as it could unlike the first “total” lockdown.

Earnings forecasts for the portfolio have been upgraded over the last three quarters and the team senses that a private sector investment cycle may be evolving after a long absence. This is not yet evident in corporate loan growth that remains below nominal GDP growth, but Gaurav anticipates this will recover in due course. Despite the positive picture, he cautions that the improving outlook has been largely priced into valuations over the short-term.

Entering a new growth cycle

Gaurav says there has been a critical shift in the government’s focus from restoring macro-economic stability to restoring growth through investment. India’s Budget in February this year set this tone, with an increase in infrastructure spending of 35% year over year, the intended privatisation of several public sector entities, an infrastructure monetisation programme, and the creation of a bad bank to ease banks’ balance sheet constraints.

Gaurav points out that the second COVID-19 wave between March and July 2021 delayed these initiatives, but that the growth agenda is still very much at the forefront. Production Linked Incentive Schemes (PLISs) were introduced across several sectors to encourage, or subsidise, the private sector to invest in capacity to manufacture products onshore that have been historically imported from China. This goes hand-in-hand with the China Plus One strategy, adopted by manufacturers wishing to diversify their sources of production away from the world’s second-largest economy and to wean their dependence on it. In some cases, this move was accelerated during the pandemic, as delegating particular segments of the production and supply chain closer to home was the only option.

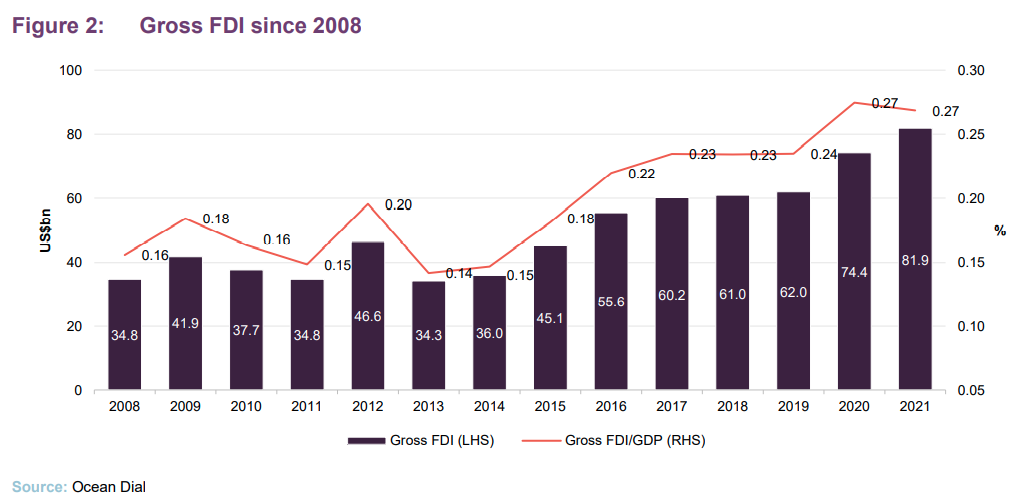

Meanwhile, foreign direct investment is reaching all-time highs (as shown in Figure 2) as is the value of exports, buoyed by the global economic recovery. Gaurav says there are significant improvements in India’s competitive positioning when compared with other emerging economies, and as such multinational corporations are adjusting long-term strategic planning on China, if only at the margin.

Though the adviser thinks it wise to always remain cautious, he says all signs suggest a strong and sustainable trajectory of growth and that the bounceback India experienced earlier this year was a good indication of things to come.

He highlights the improving housing cycle and a visible uptick in volumes and pricing while new regulatory and banking changes within real estate are also improving the landscape. Quality is picking up, he adds, while housing construction is a large job creator and has multiple economic linkages capable of driving an economic upturn.

Meanwhile, robust expansion in corporate profitability is expected to give a boost to growth prospects. Gaurav expects profit growth to increase further in the following years, led by the financials and other cyclical sectors. Businesses have also used the slowdown over the past six years to deleverage, creating space for the next economic upcycle.

Digital revolution

The pandemic forced people all over the world to stay at home which in turn, heightened the demand for digital solutions for simple needs from online grocery shopping to holding remote meetings with work colleagues. But Gaurav says in India, this has coincided with a major expansion of the country’s technological ecosystem and has grown at such a rate that he describes it as a digital revolution.

Certain industries have built upon their own tech offerings such as easier-to-use banking apps while sufficient fibre optic capacity nationwide, smartphone handsets at $50, and cheap mobile data have blended to enable a fully connected country. Gaurav says India is seven to eight years behind China in terms of internet users, e-commerce, and digital adoption, but expects to catch up at a higher growth rate. Meanwhile there is little representation in the listed equity markets currently. In the US, the digital and tech sectors represent around 30% of the S&P 500. In India, this is barely 1%, but the adviser says we are now at the critical inflection point.

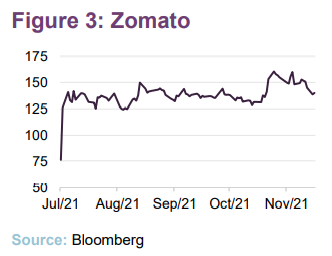

In July this year, Zomato, India’s equivalent of Deliveroo or GrubHub, was the first major tech company to list, with a market value of $14bn, 35 times subscribed with its share price rising 50% on day one (see Figure 3). Gaurav says this successful listing is expected to trigger a long pipeline of private equity and venture capital investors looking to raise both primary and secondary capital on India’s exchanges through the sale of digital and tech companies, giving listed investors the opportunity to benefit from this tectonic shift in consumer and commercial behaviour. Meanwhile, India’s tech unicorn market has grown by more than 30% over 2021 alone, with the country now home to over 60 firms valued at more than $1bn. This has come as China has strongly cracked down on tech firms through regulatory demands.

Gaurav says a lot of positive change has come from India’s shift from a patronage-based system to a rules-based business system, which has led to the country’s so-called digital evolution. This has in turn boosted IPO growth and with its renewed focus on growth, the government is supporting start-ups more than ever while the overhaul of ‘crony capitalism’ has made it harder for corrupt businesses to operate. These have since found themselves selling their stock to private equity businesses or directly to the market.

He adds that India has the right demand and supply dynamics to enjoy multi decadal growth in the new economy given the large addressable market, the successful role models that exists within the India diaspora, the entrepreneurial and talent availability on the ground and now the funding. This also shifts India’s investment narrative away from disappointing growth, disruptive reform and Covid, and towards the opportunities to invest in the new economy in a young and vibrant population.

Investment process – The ‘House of Ocean Dial’

Recent innovations

In our May 2020 note, we explained how Ocean Dial IGC had both refined its investment process and strengthened the advisory team. Tridib Pathak joined Ocean Dial in October 2019 as co-head of equities, working alongside Gaurav Narain, whom regular followers of IGC and readers of our research on the company will be very familiar with.

The analyst team saw some changes earlier this year with the addition of Ritika Behera and Dhaval Somaiya as analysts. Meanwhile assistant fund manager, Shahil Shah, was given responsibility on integrating ESG criteria into IGC’s investment process. Biographies of members of the investment advisory team are provided on pages 22 to 23.

Feet on the ground

Gaurav and the rest of the India-based team at Ocean Dial are bottom-up investors, operating in a market with historically strong and consistent earnings growth, where periods of elevated volatility have provided regular mispriced entry points.

Ocean Dial seeks out companies whose management practices are culturally aligned with theirs and whose business models are capable of creating long-term shareholder value in a sustainable manner. A focused universe of companies from which potential investments are scrutinised is referred to as the House of Ocean Dial. More specifically, companies with the following attributes are eliminated:

- Market capitalisation of below US$100m

- Environmental, Social, and Corporate Governance concerns

- Business models which are:

- incomprehensible

- not scalable

- driven by global commodity prices

- conglomerated; or

- unable to create sustainable economic value

- Business-to-Consumer companies where the consumers are predominantly based outside of India

- Insufficient knowledge to have an informed view on any of the above

This has resulted in a current universe of approximately 140 companies in which the managers can invest. Each analyst covers roughly 30 names and coverage entails forensic accounting, detailed financial modelling, and one-to-one corporate interaction twice annually.

Portfolio construction – aiming for 30 holdings

The House of Ocean Dial is a universe of companies on which the team can build focus. The manager will allocate to approximately 30 holdings which are independent both of IGC’s benchmark and the market capitalisation of the business. As at 30 November 2021, IGC holds 33 portfolio companies.

The starting point is to examine the highest ranked companies in the universe in terms of expected return, and from this the manager has discretion to dive deeper. In addition to meeting regularly with senior management, the team meets with suppliers, customers, and business competitors where relevant. The portfolio looks to invest with a minimum position size of 2%. This could range to up to 8% depending on the liquidity of the traded volume and the strength of conviction.

Investment committee

The House of Ocean Dial is a continuously evolving universe of investible opportunities. An investment committee (IC) ensures that existing names continue to pass filters set, and provides a forum for members of the investment team to propose new names for inclusion into the universe.

The IC meets regularly, and at least once a quarter, and acts as a gatekeeper for stocks under consideration, with any changes needing to be approved by the Committee. The agenda also includes the following issues:

- Mitigating behavioural risk

The team is cognisant of the challenge of distinguishing, without the benefit of hindsight, between temporary downward fluctuations caused by volatility, and a genuine loss of capital. To diminish the probability of the latter, the research process is structured to ensure that each investment thesis is constructed on a sound basis while allowing the decision-making framework to react effectively should a change in the thesis occur over the course of the holding period. All investments are documented on initiation to enable the manager to assess the effectiveness of decisions made without being clouded by viewing them through the lens of hindsight.

- Cognisant of the potential pitfalls of behavioural biases

Direct management interaction is limited, where appropriate, to twice a year, with healthy scepticism in order to ensure the team remains detached in its assessment of a given company. Moreover, the IC provides an open forum for discussion on price movements or changes in fundamentals to ensure a continuous and systematic re-assessment of each investment thesis. The universe-ranking tool provides a quantitative basis for guiding where the highest expected return opportunities exist, while triggering a re-assessment of holdings that are falling down the ranking.

- Valuation risk

A broad range of valuation techniques are used to compare the advisers’ analysis of a company’s current worth against its own history and in relation to its peer group. This is completed using Ocean Dial’s internal assessment of the company’s outlook rather than relying on sell side research or management’s own estimates. Using data analysis tools, each company model is incorporated into a “ranking tool” which provides the investment team with multiple ways with which to measure the upside to fair value for each portfolio candidate.

The ranking tool acts as a strong signal to the portfolio adviser as to where the most profitable opportunities in the universe lie. Its strength is as a guide to enable better resource allocation and decision making, not as a systematic final output of what the portfolio should be. Deeper due diligence in the form of further management interaction, background checks, and broader scrutiny of the competitive landscape is conducted by the team depending on the portfolio adviser’s requirement to build a fully informed thesis as to whether an investment decision should be recommended.

Asset allocation

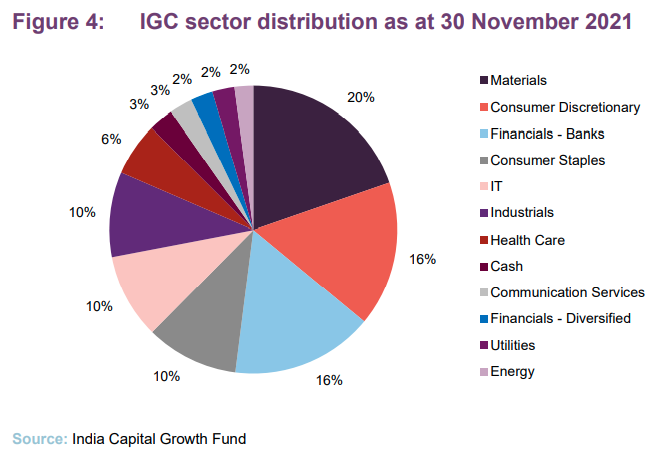

As was highlighted in our previous notes, Gaurav made a lot of changes throughout 2020 as the COVID-19 crisis continued. He reduced his exposure to banks, which was then built back up following February’s Budget, before coming back down to 16.0% as at the end of November 2021. Materials remains the biggest portfolio sector weighting at 20%. We note that materials in the context of IGC’s portfolio represents mainly cement and speciality chemicals as opposed to global commodities.

Gaurav continues to avoid stocks which are B2C export orientated as their future remains uncertain in the light of the pandemic and its long-term impact. Money has instead been deployed into more stable businesses such as those in the electronics manufacturing space.

IGC’s cash level fell to its lowest on record during the 12 months since June 2020, ranging between 1-2.2%, compared to a typical holding of between 3-5%. The net cash level has now reverted back to more traditional levels and as at 30 November 2021, stands at 2.8%.

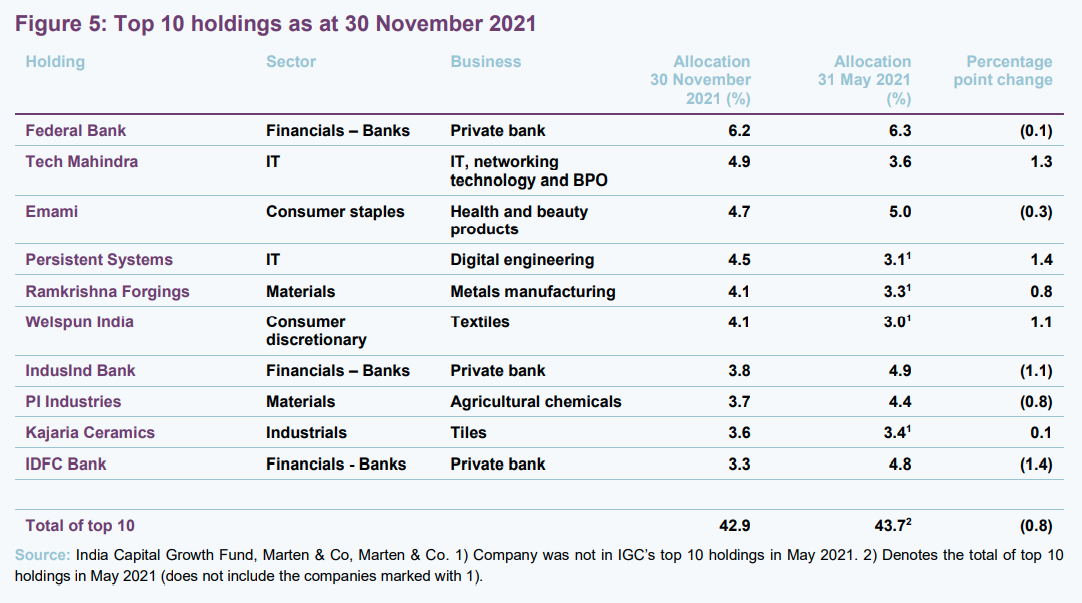

Top 10 holdings

Figure 5 shows IGC’s top 10 holdings as at 30 November 2021 and how these have changed since 31 May 2021 (the data as published in our last IGC note). New entrants to the top 10 since then are Ramkrishna Forgings, Persistent Systems, Welspun India and Kajaria Ceramics. Names that have moved out of the top 10 since then are Gujarat Gas, Aegis Logistics, Neuland Laboratories and JK Lakshmi Cement. We discuss some of the more interesting changes in the following pages. Readers interested in other names in the top 10 should see our previous notes, where many of these have been previously discussed (see end of this note).

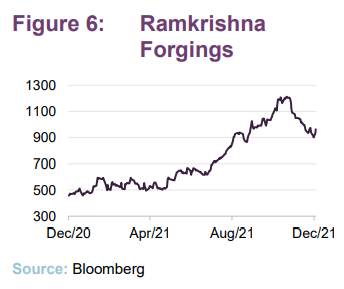

Ramkrishna Forgings

Ramkrishna Forgings (www.ramkrishnaforgings.com) has fluctuated in and out of IGC’s top ten several times since it was bought but always remains one of the company’s largest holdings. It now represents 4.1% of the trust. A manufacturer of large forgings for trucks, initially for heavy commercial vehicles in India, the company now gets 60% of its business from overseas, mainly North America and Europe. Gaurav says it has enjoyed new clients which it has gained from the China Plus One strategy and is an example of a company he has nothing but conviction in and knows well enough to double his exposure to in times of distress.

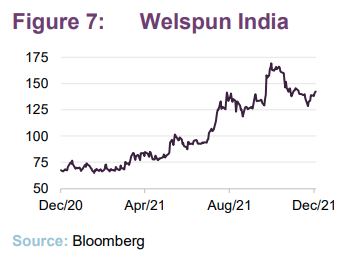

Welspun India

Welspun India (www.welspunindia.com) is India’s largest home textile company with a presence in cotton bedsheets, towels, rugs and carpets. It is Asia’s largest and the world’s second largest terry towel producer and exports more than 94% of its home textile products to more than 50 countries. Gaurav says the company’s strength is its integrated manufacturing facilities and focus on innovation. It has 32 patents with over 43% of revenues coming from innovative products while also diversifying its revenue base by launching its own brands in domestic and overseas markets. Return on capital ratios are set to rise to over 15% in the next three years, which Gaurav adds should lead to a rerating of the business.

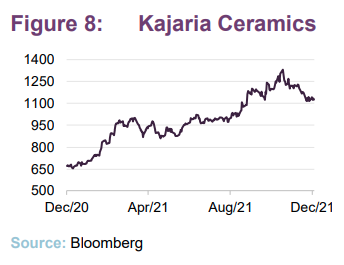

Kajaria Ceramics

Like Ramkrishna Forgings, Kajaria Ceramics (www.kajariaceramics.com) tends to fall in and out of IGC’s top ten holdings but always remains in the top 15 and is one of the company’s longer-term investments. Kajaria is the largest tile manufacturer in India and eighth largest in the world. Gaurav says the business is of ‘gold standard’ in its sector and is the name that competition look to benchmark themselves against. He says that through each economic cycle the company emerges stronger, reducing the volatility of its earnings profile, and allowing it to command a higher and more constant valuation multiple for the future.

Performance

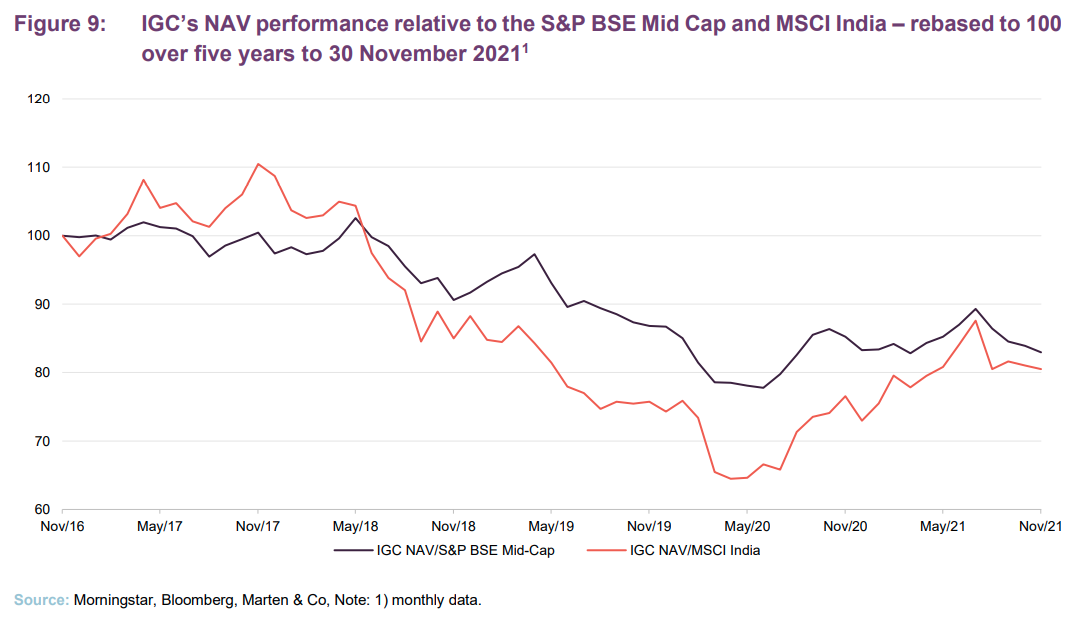

Year-to-date, IGC has been one of the best-performing trusts in its sector, delivering 43% in share price terms, behind only Ashoka India Equity. Looking over a three-year view, it lags behind Ashoka and also Aberdeen New India but this period has also seen a change in fate for the trust – with the implementation of new policies which had a positive impact on its discount (see more here) – as well as India as it finally enters a new economic cycle after nine years.

Small- and medium-sized Indian companies have generally underperformed larger ones, for much of the last five years which has impacted on IGC’s performance relative to the MSCI India Index. But as previously highlighted, a change in fate has seen this turn around over 2021, which may well continue as the country’s growth agenda takes centre stage.

Last year the team was vocal about its mistakes regarding stock selection and made public statements declaring the changes it would make to turn performance around. The improvement is particularly evident over the past 22 months, during which time ten new names have been added, which now make up 25% of the portfolio.

Attribution

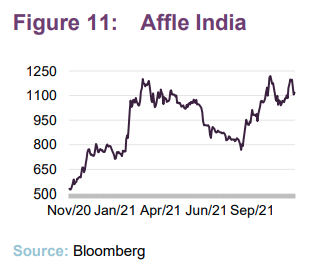

Affle India

The most recent addition to IGC is Affle India (www.affle.com), a digital ad-tech company operating only in the mobile space. Using data science algorithms, Affle enables advertisers to drive targeted marketing campaigns to acquire new customers or engage existing ones. It earns 89% of revenue through an ROI based cost-per-converter-user revenue model where Affle gets paid when a potential customer is converted. With increasing smartphone usage and online shopping, Gaurav believes Affle provides exposure to a large market opportunity across the digital ecosystem. He says it is a leader in its space and is expected to grow sales by an annual 47% over the next three years, with profits growing at a similar pace.

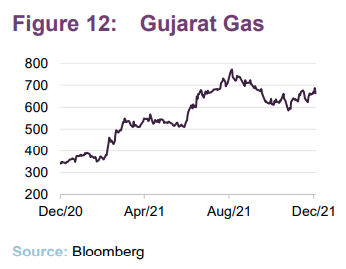

Gujarat Gas

Gujarat Gas (www.gujaratgas.com) is India’s largest city gas distribution company with volumes of around 12mmscmd (million metric standard cubic meter per day). It operates in 24 districts supplying gas to small industries (75% of revenues) with a network of 24,000+km of pipeline. Gaurav says demand is strong, which means the company can exercise considerable pricing power. Over the past six to eight months, it has been able to make two consecutive price increases of over 20% each with negligible volume impact. IGC believes Gujarat Gas will be able to maintain its margin while stability in earnings should drive a consistently high return on capital employed of around 30% versus around 19% in the previous five years.

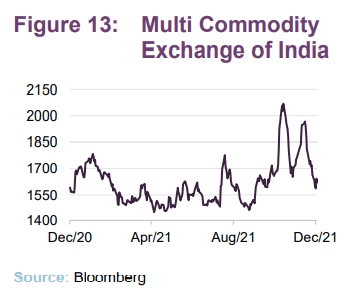

Multi Commodity Exchange of India

The Multi Commodity Exchange of India (www.mcxindia.com) is India’s largest commodity exchange with more than 90% of market share in commodity derivatives trading. It has an almost 100% share in non-agricultural commodities consisting of bullion, energy and base metals, and has maintained a strong monopoly over the last two years despite the entry of two strong competitors. With high cash levels on its balance sheet and a steady dividend payout, Gaurav says MCX is an attractive play on India’s financialisation story.

Peer group

IGC is a member of the AIC’s India sector, which comprises four members. All of these were members of the peer group when we last wrote about IGC. Within this peer group, IGC is the most-focused on small and medium-sized companies. Members of India sector will typically have:

- over 80% invested in Indian shares;

- an investment objective/policy to invest in Indian shares; and

- an Indian benchmark.

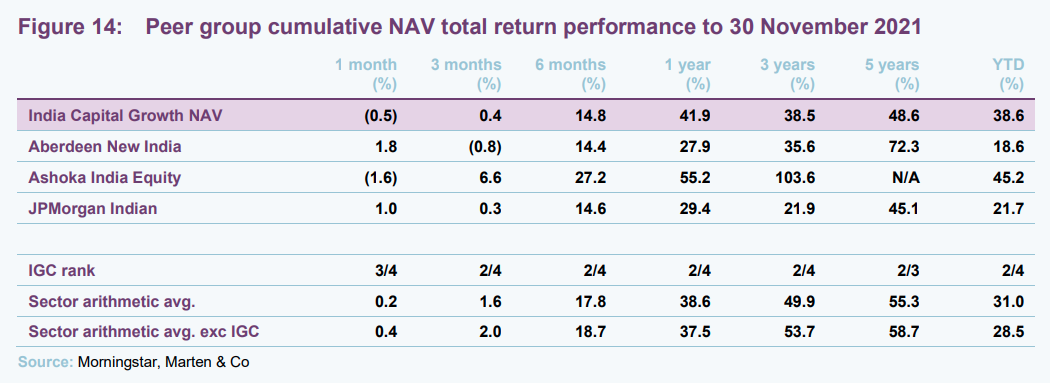

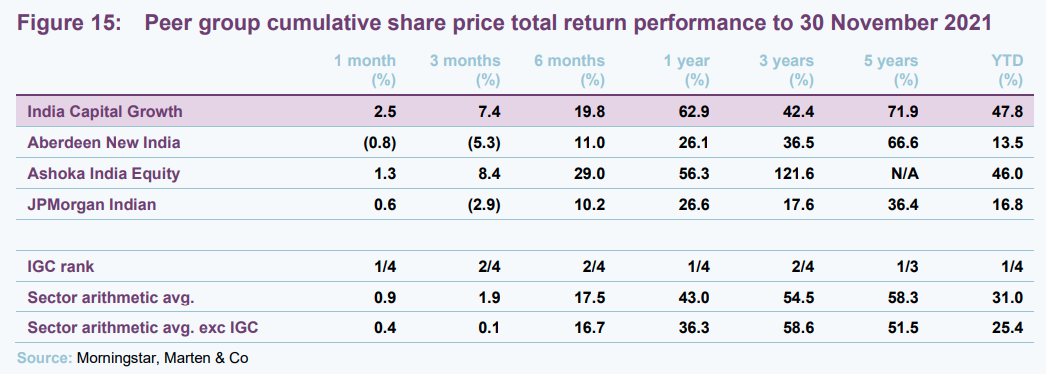

As highlighted in our last note and can be seen from Figure 14, there has been a marked improvement in IGC’s cumulative NAV total return performance relative to peers following the change in investment process. Performance over this period has been so strong that it has pulled up IGC’s performance over the longer-term periods. Figure 14 shows that IGC’s diluted NAV now ranks second over the five-year, one-year and six-month periods as well as year-to-date. The continued strong performance since our last annual overview in December 2020 reinforces the manager’s statement, at that time, that the changes to the investment process were bearing significant fruit, according to its own internal analysis. As we have said previously, if the adviser’s changes continue to drive outperformance, IGC will continue to move up the rankings over the longer-term periods as well.

Looking at Figure 15, an even better picture can be seen for IGC’s share price performance, where it ranks second over five years, one year, six, three and one months, and first year-to-date. Nonetheless, IGC’s discount is not out of line with those of the two largest funds in the sector. It is worth noting that, for a strategy such as this, longer-term time frames are generally considered to be more relevant to assessing performance, and we believe that the market may still be waiting to see if the recent strong performance is maintained.

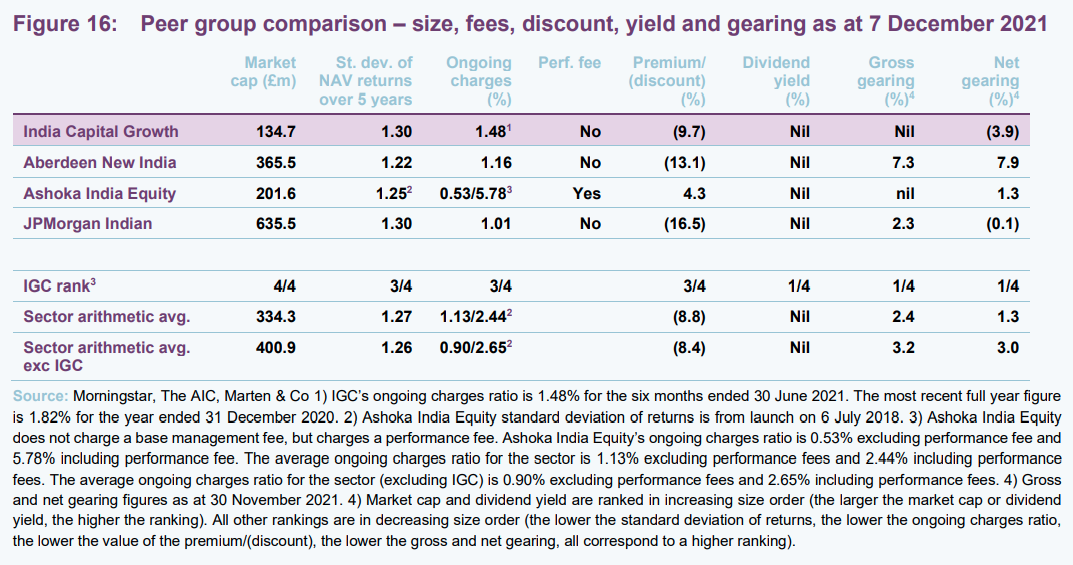

As illustrated in Figure 16, IGC is the smallest of the four funds focused on India and listed in London and this is a significant reason why it has the highest ongoing charges ratio of this peer group. Ashoka India Equity (the next smallest fund) has a particularly low ongoing charges ratio, because it does not charge a base management fee, but unlike the rest of the peers charges a performance fee of 30% of outperformance (capped), measured over three years, to compensate. Consequently, in years where the performance fee falls due, its ongoing charges ratio will increase accordingly, pushing it up the rankings. It is noteworthy that, including its performance fee, Ashoka India Equity is the most expensive fund by some margin with an ongoing charges ratio of 5.78%.

IGC is operating with the largest net cash position (unlike its peers, it does not utilise gearing). Volatility of NAV returns, as measured by the standard deviation of daily NAV returns over five years, are broadly comparable across the four peers, although IGC’s volatility is broadly in line with the sector average.

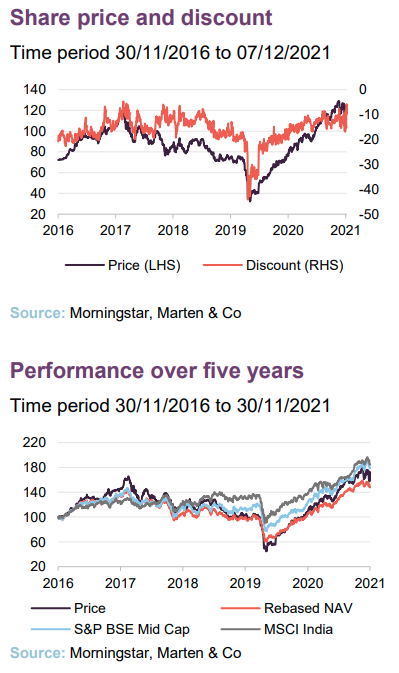

Premium/(discount)

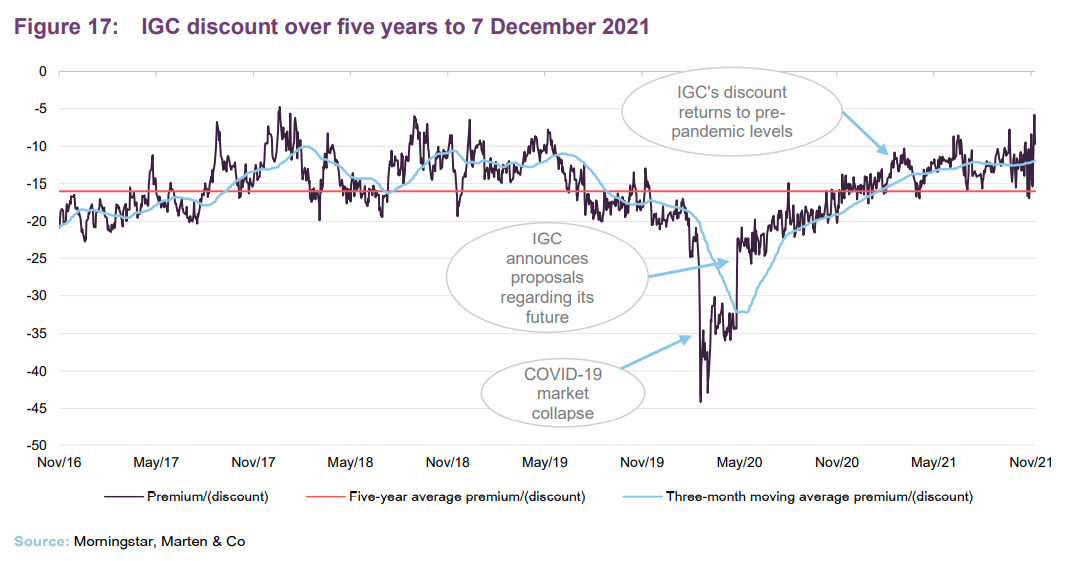

Over the year ended 30 November 2021, IGC’s shares have traded consistently on a discount, ranging from 20.2% to 7.8%, with an average discount of 13.7%.

At 7 December 2021, IGC’s shares were trading at a discount of 9.7%, which, as illustrated in Figure 17, is more akin to its levels immediately prior to the onset of the pandemic. It also reflects the forthcoming redemption opportunity that is discussed at the start of this note, and briefly below.

Like many other funds, IGC’s discount was impacted by the onset of the pandemic. As discussed in our notes published throughout 2020 and more recently in June 2021, IGC published a series of proposals regarding its future on 26 May 2020, which led to a dramatic narrowing of its discount. Following the announcement of these proposals, shareholders voted to approve IGC’s continuation on 12 June 2020. A summary of the proposals is provided as follows:

- the introduction of a redemption facility, giving shareholders the right to request the redemption of part or all of their shareholding on 31 December 2021 and every second year thereafter at an exit discount equal to a maximum of a 6% discount to NAV per redemption share;

- a change to the investment manager’s fee from 1.25% of total assets per annum to the lower of 1.25% of average market capitalisation (calculated on a daily basis) per annum or 1.25% of total assets per annum with effect from

1 July 2020 with a further review to the investment manager’s fee in 2022; and - IGC may seek to satisfy redemption requests by matching such requests with demand for new ordinary shares from incoming investors.

The board has also determined that the exit discount for the December 2023 redemption point will be a maximum of 3%.

As we highlighted in our previous notes since the proposals were put into place, IGC has until December 2021 to prove itself and, as discussed previously and in the performance section of this note, its discount narrowing is in part a reflection of its performance and the strong potential that India offers. We think that, if it continues to perform and India continues to grow strongly, attracting investors’ attention, there is room for the discount to continue to narrow from here.

Fees and costs

The investment manager is entitled to receive a management fee payable jointly by IGC and ICG Q Limited equivalent to 1.25% per annum (pre 1 July 2019 1.5%) of the lower market cap and gross assets less current liabilities. Either side must give 12 months’ notice to end the contract. There is no performance fee.

The administrator is Apex Fund Services (Guernsey) Limited. The custodian of IGC’s assets is Mumbai-based, Kotak Mahindra Bank Limited. Cash is held in both Mauritius and India.

The ongoing charges ratio for the year ended 31 December 2020 was 1.82%, slightly lower than the equivalent figure for 2019 (1.85%). The decrease reflects the reduction in management fee (noted above), which occurred halfway through the year. As at 30 June 2021, the annualised ongoing charges ratio had fallen again to 1.48%, reflecting the increase in the size of the fund (fixed costs being spread over a wider base).

Looking to the year ended 31 December 2021, IGC’s ongoing charges ratio should benefit from having a full year of the management fee being charged at the new lower rate.

Capital structure and life

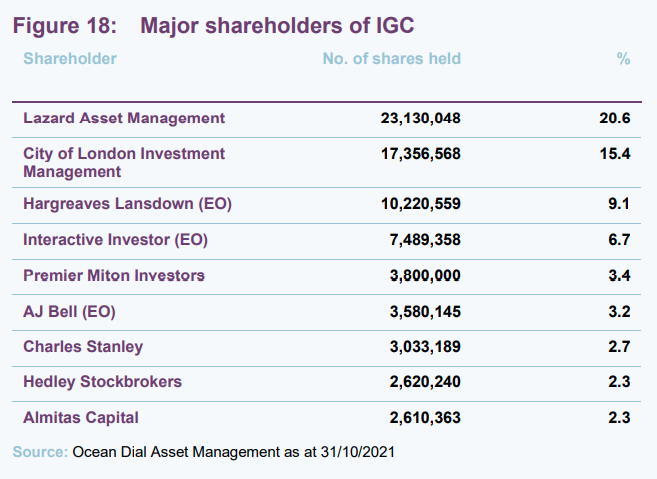

IGC has a simple capital structure with one class of ordinary shares in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 30 November 2021, there were 112,384,673 of these in issue with 117,500 held in treasury. IGC has the authority to buy back up to 14.99% of its issued share capital, a power that it renews at each AGM. Figure 18 shows the major shareholders in IGC at 31 October 2021.

IGC maintains an ungeared portfolio

Although permitted to, the manager does not employ gearing in the management of the fund. This reflects the relative volatility of the Indian stock market. The manager will normally keep cash of 3–4% on hand to take advantage of attractive investment opportunities as they arise.

Unlimited life with a full redemption opportunity every two years

The introduction of a redemption facility, which we talk about in more detail at the front of this note, gave shareholders the right to request the redemption of part or all of their shareholding on 31 December 2021 and every second year thereafter at an exit discount equal to a maximum of a 6% discount to NAV per redemption share.

Financial calendar

IGC’s financial year end is 31 December. The annual results are usually released in March (interims in September) and its AGMs are usually held in June of each year. IGC does not pay a dividend.

Investment advisory team

Since our last annual overview, which was published in December 2020, there have been some changes to the investment and advisory team, mainly the appointment of two new analysts and the introduction of a dedicated ESG analyst.

Gaurav Narain – fund adviser and co-head of equities

Gaurav Narain joined Ocean Dial in November 2011 and has been involved with the Indian markets for more than 25 years. He has held senior positions as both a fund manager and an equities analyst for New Horizon Investments, ING Investment Management India and SG (Asia) Securities India. Gaurav holds a Master’s degree in Finance and Control and a Bachelor of Economics from Delhi University, and is based in Mumbai.

Tridib Pathak – co-head of equities

Tridib Pathak has had a career in the Indian financial markets that spans over 30 years, with stints in project finance, credit analysis and latterly pan-Asia equity research for UBS Securities. His buy-side career began in 1999, since which he has been investing in Indian equities for both domestic and international investors at firms including Lotus Asset Management and DBS Cholamandalam, where he served as CIO. Tridib joined Ocean Dial in 2019 from the Enam Group, where he was Senior Portfolio Manager for four years. He is a Chartered Accountant from the Institute of Chartered Accountants of India.

Shahil Shah – assistant fund manager & ESG analyst

Shahil Shah was part of the original investment team which was set up in 2005 and specialises in telecommunications, consumer, healthcare, and media sectors and is responsible for integrating ESG analysis into the investment process. He holds a Master’s degree in Commerce and Finance from Mumbai University and is based in London.

Saurabh Chugh – analyst

Saurabh Chugh was the part of the original investment team and joined in 2006. He specialises in information technology, energy, transport, infrastructure and soft commodities. He holds an MBA in Finance from Nirma Institute of Management, Ahmedabad, and is based in Mumbai.

Ashutosh Garud – analyst

Ashutosh Garud joined Ocean Dial in 2020 after working as associate portfolio manager in the Avendus Wealth Management Team. Prior to joining Avendus, he worked with Reliance Wealth Management. Ashutosh holds an MBA in Finance from Chetana Institute of Management Studies, a Bachelor of Commerce & Economics from Mumbai University, and is a CFA charterholder. He is based in Mumbai.

Ritika Behera – analyst

Ritika Behera joined Ocean Dial in April 2021 and has 12 years’ experience in equity research covering the BFSI sector. She previously worked at Elara Capital, as lead analyst for diversified financials, covering non-banking financials, insurance and brokers. She has an MBA in Finance and is based in Mumbai.

Dhaval Somaiya – analyst

Dhaval Somaiya joined Ocean Dial in January 2021. He has four years of experience in public equities and FinTech, previously working for PhillipCapital with a primary focus on the Indian real estate sector. Prior to this, he worked for Ebix Cash Financial Technologies. Dhaval holds a Masters in Finance from Jamnalal Bajaj Institute of Management Studies (JBIMS), Mumbai.

Board

The board currently consists of four non-executive directors, all of whom are independent of the manager and who do not sit together on other boards. Peter Niven, who has sat on the board for just over a decade is due to step down at the end of the year. He is replaced by Lynne Duquemin, who was appointed in May 2021.

Any director who has served for more than nine years stands for re-election annually, and one third of the remaining directors retire by rotation at each AGM and seek re-election. The maximum total payable to the directors is set in the articles of association as £200,000.

Elizabeth Scott (chair)

Elisabeth Scott has over 35 years’ experience in the asset management industry, having started as a US equity fund manager in Edinburgh in 1985. She went to Hong Kong in 1992, where she remained until 2008, most recently in the role of managing director and country head of Schroder Investment Management (Hong Kong) Limited and chairman of the Hong Kong Investment Funds Association. She is also chair of Allianz Technology Trust and the Association of Investment Companies (AIC).

Patrick Firth (chair of the audit committee)

Patrick Firth is a chartered accountant. He qualified with KPMG and has worked in the investment and funds industry in operations and management in Guernsey for nearly 30 years. Patrick Firth is also a non-executive Director of ICG Longbow Senior Secured UK Property Debt Investments Limited, Riverstone Energy Limited and NextEnergy Solar Fund Limited and chairman of AIM-traded GLI Finance Limited.

Peter Niven (director – until the end of 2021)

Peter Niven has over 40 years’ experience in the financial services industry, both in the UK and offshore. He was a senior executive in the Lloyds TSB Group until his retirement in 2004, and until July 2012 was the chief executive of Guernsey Finance LBG, promoting the island as a financial services destination. He is a Fellow of the Chartered Institute of Bankers and a chartered director. He is due to retire from the board at the end of the year.

Lynne Duquemin (director)

Lynne Duquemin is the newest member of IGC’s board having been appointed in May 2021 to replace Peter Niven, who will retire at the end of the year. She has over 30 years’ experience in financial markets, initially in London before being seconded by Credit Suisse to Guernsey, where she is still based. She is a Fellow of the Chartered Institute for Securities and Investment and a Chartered Wealth Manager. She is also a Chartered Director and Fellow of the Institute of Directors.

Previous publications

Readers interested in further information about IGC may wish to read our previous notes. You can read the notes by clicking on them or by visiting our website.

| Title | Note type | Publication date |

| Compounding machine | Initiation | 23 March 2016 |

| Indian powerhouse | Update | 8 July 2016 |

| India at a significant discount | Update | 21 October 2016 |

| Full steam ahead | Annual overview | 29 March 2017 |

| Moving to the main board | Update | 30 January 2018 |

| A return to earnings growth | Annual overview | 26 June 2018 |

| Shakeout uncovers value | Update | 29 November 2018 |

| Discounted value | Annual overview | 1 October 2019 |

| Needs more time | Update | 26 May 2020 |

| A win-win scenario | Annual overview | 15 December 2020 |

| Lessons learnt | Update | 17 June 2021 |

The legal bit

This marketing communication has been prepared for India Capital Growth Fund Limited by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.