Real Estate Quarterly Review

Kindly sponsored by abrdn

Storm clouds gather

Fears that a perfect storm is brewing has weighed on the real estate sector. Central banks’ move to raise interest rates to curb spiralling inflation has stoked concerns that investors will turn away from real estate to less risky alternatives, such as bonds. Meanwhile the cost of debt has also increased and is approaching the average property investment yield in some locations and markets, meaning a hit on earnings as interest payments balloon.

The share prices of property companies have almost indiscriminately been hit. Only a handful showed gains in the quarter, led by companies with long-dated inflation-linked income. The industrial and logistics sector, for so long the darling of the real estate sector, was the hardest hit following a bleak earnings update from Amazon that suggested its expansion was over. Some companies seem to have been oversold and now trade on attractive discounts to NAV.

Merger and acquisition (M&A) activity continued during the quarter, with LXI REIT and Secure Income REIT finalising their merger and Capital & Counties and Shaftesbury progressing with their own union. M&A may continue to be a theme for the rest of the year, with many companies trading at significant discounts to NAV.

Performance data

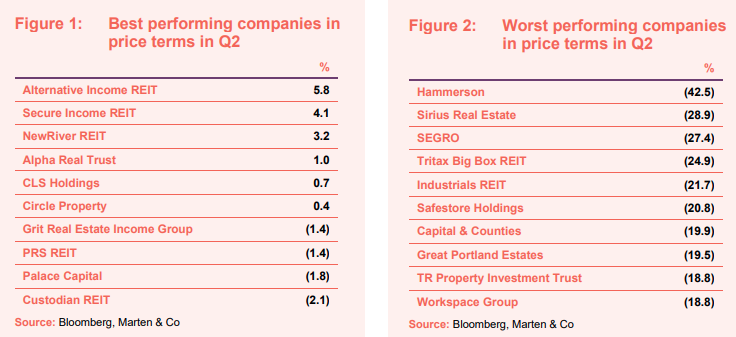

Best performing companies

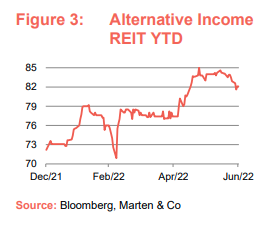

There were few real estate winners in the second quarter of 2022, as fears mounted for a recession. However, a handfuls of funds did post share price gains, led by long-income specialists Alternative Income REIT and Secure Income REIT.

Both benefit from long inflation-linked leases, which offer some protection against soaring inflation. Secure Income REIT’s share price was also boosted by its merger with fellow long-income fund LXI REIT (which became effective on 6 July – see page 7 for more detail).

Retail specialist NewRiver REIT continued its share price recovery after it said it had returned to positive capital value growth, suggesting valuations in the retail sector were stabilising after years of decline. Over the course of the quarter its share price was up 3.2%.

Micro-cap Alpha Real Trust, which has a portfolio of property and property loans, announced a tender offer for up to 10% of its share capital, to combat the group’s shares trading at a significant discount to NAV.

Office landlord CLS Holdings announced a proposed tender offer of its shares if its discount persists. Following the news, its share price was up slightly in the quarter, however, its discount still languishes at around 35%.

Circle Property was the only other fund to see its share price rise in the quarter. It has previously announced that it would sell assets and return capital to shareholders after suffering a persistently wide discount.

Worst performing companies

Industrial and logistics specialists and office-focused funds dominated the share price fallers list; however, it was the retail-focused Hammerson that topped the list of worst performing funds, with 42.5% wiped off its market cap.

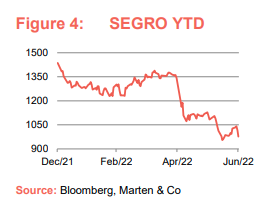

Amazon’s bleak earnings update and admission that its warehouse expansion was over hit the share price of many of the logistics focused property companies. This coupled with an expected squeeze on retail spend and the tight margins involved in online retailing saw investors convey caution towards the sector that has for the past several years seen exponential growth. SEGRO, the largest listed property company, saw 27.4% wiped off its value during the quarter, while Tritax Big Box REIT was close behind with 24.9%. Both companies are now trading on wide discounts to NAV (see page 6 for details).

The uncertain outlook for the office sector – including working from home and hybrid trends depressing demand and halting rental growth, and rising interest rates curbing investors’ appetite for real estate – impacted the office specialists. Sirius Real Estate, which owns business parks in Germany and the UK, was the most affected, with a 28.9% fall in its share price.

London office landlords were also heavily impacted, with Great Portland Estates (down 19.5%) and Workspace Group (down 18.8%) both suffering heavy losses.

Shareholder revolt over the possible merger of central London retail and hospitality landlords Capital & Counties and Shaftesbury (more detail on page 7) saw the share price of both fall by double-digits (19.9% and 15.5% respectively).

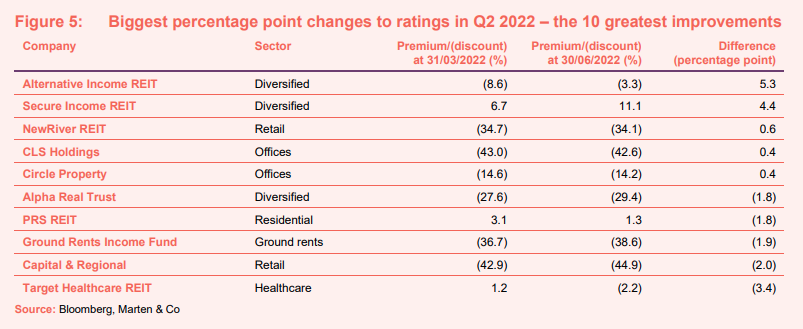

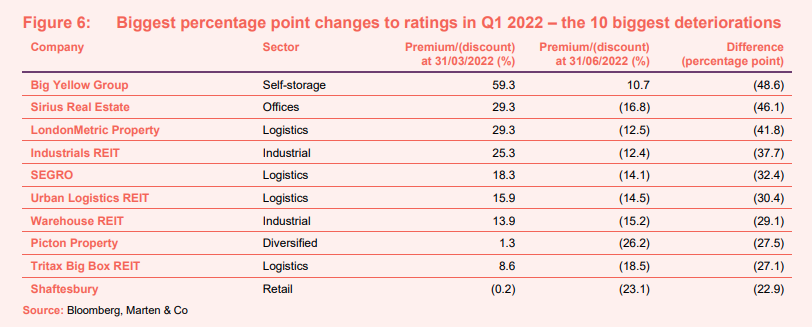

Significant rating changes

Figures 5 and 6 show how premiums and discounts to NAV have moved over the course of the quarter.

Many of the positive rating changes were discussed in the previous section. Of the others, private rented sector residential developer PRS REIT saw a slight narrowing of its premium to NAV as its share price fell just 1.8% in the quarter (versus an average fall across listed real estate companies of 10.2%). Demand for rented accommodation could grow as interest rates rise, leaving homeownership out of reach for many would-be first-time buyers and forcing others in to renting.

The uncorrelated nature of the care home sector with the wider economy could be behind Target Healthcare REIT’s share price performance (down 3.4% in the quarter) compared to the wider real estate sector.

Shopping centre owner Capital & Regional saw its share price stabilise somewhat (after months of heavy falls) as market indicators suggest mall values may have hit the bottom and investment levels pick up.

Again, many of the funds mentioned in the biggest discount deteriorations during the quarter were covered earlier. Self-storage specialist Big Yellow Group topped the list after reporting a significant increase in its NAV (22.9%) while seeing its share price fall 14.6%.

Major corporate activity

Fundraises

The ongoing war in Ukraine and heightened fears for a recession meant that fundraises were again muted in the second quarter, with just three issues of shares. The total was up on the previous quarter, however, with just under £600m raised. Supermarket Income REIT led the way with a £300m substantially oversubscribed issue and a further £6.7m through a PrimaryBid offer. The total raised eclipses the original £175m target. The company will deploy the proceeds into a pipeline of investment opportunities.

Home REIT also smashed its fundraise target, raising £263m – significantly above its initial target of £150m. The proceeds of the raise will be used to tackle the ongoing critical need for homeless accommodation in the UK, with the company having a £300m acquisition pipeline.

Impact Healthcare REIT raised £22.3m in a placing and offer for subscription, which it will use with other financial resources to acquire from its pipeline of care home assets worth £169m.

Mergers and acquisitions

Shaftesbury and Capital & Counties Properties reached an agreement on a £3.5bn all-share merger. The merger would create a REIT, which would be called Shaftesbury Capital Plc, focused on the West End of London with a £5bn portfolio across Covent Garden, Carnaby, Chinatown and Soho.

Shareholders of both LXI REIT and Secure Income REIT voted in favour of a merger of the two trusts. Under the terms of the merger, each Secure Income shareholder received 3.32 new LXI shares per one Secure Income share. The merger became effective on 6 July. The combined company has a portfolio worth £3.9bn and net assets of £2.8bn.

The acquisition of McKay Securities by Workspace Group completed in May. Under the terms of the acquisition, each McKay shareholder received 209 pence per share in cash and 0.115 new Workspace shares.

Other major corporate activity

CLS Holdings proposed a tender offer of its shares due to its persistent and unjustified share price discount to net tangible assets. The size of the tender will be scaled to ensure the group’s loan-to-value is within an acceptable level. The terms of the tender offer will be announced following the group’s half year results on 10 August 2022.

Matthew Howard will succeed Peter Lowe as lead manager of CT Property Trust (formerly BMO Real Estate Investments) from 19 July 2022. Howard is currently the fund manager of the RSA Shareholders Real Estate Fund and deputy manager of BMO Commercial Property Trust. He joined BMO REP in July 2017, having spent the previous six years at Hermes Investment Management (now Federated Hermes). He is a member of BMO REP’s Investment Committee.

Palace Capital’s chief executive Neil Sinclair stepped down from the board. Sinclair co-founded Palace Capital in 2010 and helped grow the business through a combination of corporate and property acquisitions, with the company moving up from AIM to the Main Market in 2018 and converting to a REIT in 2019. Steven Owen, currently non-executive chairman, has assumed the role of interim executive chairman.

Warehouse REIT announced its proposed admission to the premium segment of the main market and the cancellation of its trading on AIM, which should happen in July. The move should open up its shares to a wider pool of investors and improve their liquidity.

Target Healthcare REIT and Supermarket Income REIT both moved up into the FTSE 250 Index.

Major news stories

- Tritax Big Box REIT let 1m sq ft across four buildings at its Symmetry Park Rugby development site to a global leader in storage and information management services. Two of the buildings are from the company’s speculative development programme, and the other two are being pre-let and will be constructed on a built-to-suit basis.

- Life Science REIT completed the acquisition of Oxford Technology Park, a 20-acre science and technology park, for £120.3m, meaning it has now fully deployed the proceeds from its IPO in November 2021.

- Derwent London exchanged contracts to acquire the Moorfields Eye Hospital and the UCL Institute of Ophthalmology, for £239m. The site is being sold by Moorfields Eye Hospital NHS Foundation Trust and UCL and is subject to final Treasury approval, which is expected by the end of 2022. Derwent plans to redevelop the 2.5-acre site into a 750,000 sq ft campus.

- Land Securities agreed a deal to sell 32-50 Strand, in London, for £195m, representing a net initial yield of 4.2%, to Sinarmas Land Limited, a real estate company listed on the Singapore Exchange. The disposal is in line with Landsec’s strategy to recycle capital into higher return opportunities.

- Workspace will look to sell a light industrial portfolio that was acquired as part of its takeover of McKay Securities earlier in May. It said that it received several unsolicited approaches for the acquisition of the entire portfolio, last valued at £137m at 30 September 2021.

- UK Commercial Property REIT acquired a hotel development site in Leeds for £62.7m. The group will fund the development of the 305-room hotel, which is scheduled to complete in 2024 and will have a 25-year franchise agreement in place with Hyatt Hotels. The hotel will be operated under a lease by Interstate Hotels & Resorts, with UKCM’s rental income based on the income generated from the operation of the hotel.

- Regional REIT acquired three offices for a total of £26.5m, reflecting an overall blended net initial yield of 8.0%. It has bought 1 North Bank, in Sheffield for £8.5m, Thorpe Park, in Leeds for £8.6m, and Albion Street, also in Leeds for £9.4m.

- British Land agreed a deal to sell a 75% stake in its Paddington Central assets to GIC for £694m, representing a 1% discount to September 2021 book value and a net initial yield of 4.5%.

- BMO Commercial Property Trust and BMO Real Estate Investments have both changed their name, to Balanced Commercial Property Trust and CT Property Trust respectively, following the acquisition of BMO by Columbia Threadneedle. CT Property Trust’s new ticker is CTPT, while Balanced Commercial Property Trust remains BCPT.

- Standard Life Investments Property Income Trust also changed its name – to abrdn Property Income Trust Limited, with a new ticker of API.

Selected QD views

Real estate research notes

Grit Real Estate Income Group – Transition underway

Civitas Social Housing – Fundamentals remain strong

Standard Life Investments Property Income Trust – Resilient income in uncertain times

abrdn European Logistics Income – Logistics safe haven with growth on horizon

Legal

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority). This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access. No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.