Resilient income in uncertain times

Standard Life Investments Property Income Trust’s (SLI’s) portfolio has performed strongly over the past year, posting a NAV total return of 30.7%. It is reaping the rewards of its manager pivoting to the industrial and logistics sector many years ago (it now makes up 55% of the portfolio). This has allowed the manager to crystallise profits in a buoyant investment market for industrial assets; selling property that it believes does not fit future occupier needs – specifically, on sustainability features.

The company has around £45m available for new investments and the manager has set its sights on lower-yielding, quality assets that have strong ESG credentials, which it believes will provide it with resilient long-term income with superior growth potential. Despite recent valuation gains, the company’s share price has not kept pace, and it currently trades on an attractive discount of 23.7%.

Commercial UK property exposure

SLI aims to generate an attractive level of income, along with the prospect of both income and capital growth, by investing in a diversified portfolio of UK commercial real estate assets in the industrial, office, retail and other sectors. SLI uses gearing with the aim of enhancing returns, with the current loan-to-value (LTV) ratio at 18.6%.

Market outlook

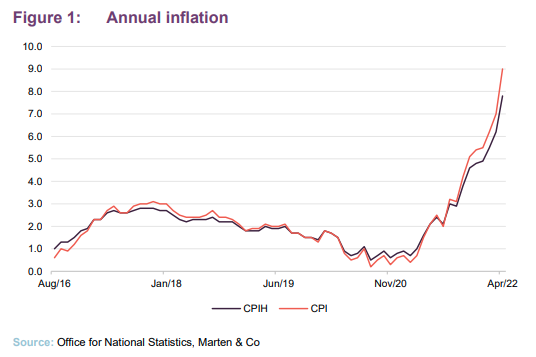

Recently, the UK economy has lurched from one crisis to another. No sooner had the UK cautiously moved away from a restrictions-based approach to dealing with the COVID-19 pandemic to a ‘living with the virus’ mentality, than a cost-of-living crisis arose with inflation at a 40-year high (forecast to soar to double digits over the next couple of months) and energy prices spiralling – both exacerbated by the war in Ukraine. For an already-fragile property sector, aside from the logistics market which has many structural tailwinds in its favour, the ramifications of a squeeze on disposable income could be great.

SLI is relatively well protected from inflation (although it is difficult to see how any industry sector is going to get full protection in the short term). Around 21% of its leases are either index-linked or have fixed annual increases embedded in them. However, most of the index-linked leases have a cap in place of either 3% or 4% (far below inflation predictions for the rest of 2022) and the fixed uplifts are mostly at 2.5%. One form of better protection for property companies is exposure to assets with higher rental growth prospects, such as logistics.

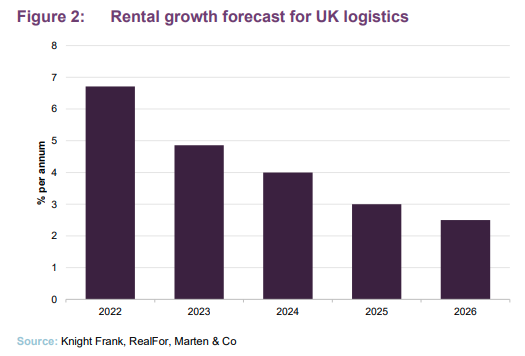

The company’s exposure to the industrial and logistics market was just over 55% at the end of March 2022. We have talked extensively on the structural tailwinds behind the growth in logistics real estate in previous notes (see page 12 for links to these previous notes). Supply of logistics property remains tight, and according to CBRE, the UK-wide vacancy rate has fallen to below 2%. The manager says that the level of new development is unlikely to satisfy demand, and anticipates robust rental value growth to continue in this sector. Rental growth is forecast to reach almost 7% in the UK this year, according to Knight Frank, and to be even more pronounced in certain markets like London.

In response to high inflation, the Bank of England has tightened its monetary policy, with the base rate rising to 1.0% earlier this month. The manager expects interest rates to peak at 1.75% or 2.0% in 2023. Although low in a historical context, base rates and the feed through to the bond market has the potential to act as a natural cap on any further yield compression, particularly for the lower yielding areas of the real estate market, such as logistics.

Cautious on logistics pricing

Pricing levels in the industrial and logistics sector have become very keen, with yields in some markets at or below 3%. The manager says that he is concerned that the market is not differentiating between good-quality units that serve occupier needs (standard things like a yard big enough to allow HGVs to adequately manoeuvre) and ones that do not. The manager believes that the future growth prospects of the multi-let industrial sector are limited, as the risk of tenant failure is heightened due to the SME nature of the tenant base. This is why the company sold a number of industrial assets, which it felt were not future-fit, over a year ago and crystallised profits from a buoyant market.

It has led SLI’s manager to look at other avenues for greater yield return. One of the recent logistics purchases was a pre-let development funding – where the return on offer is greater – and the company is under offer on a deal to fund the development of a speculatively built logistics facility. The manager has also looked at other sectors, including retail warehouses and hotels, aparthotels and student housing. Other investors, in search of yield and attracted by the fundamentals of retail warehouses, have also piled into that sub-sector leading to substantial yield compression. The manager says a B&Q-let retail warehouse that it acquired 18 months ago at a yield of 7.5% would trade keener than 5.5% today. Retail parks let to good tenants (such as budget operators, DIY companies and food retailers) on affordable rents have been particularly attractive to investors, especially as their values are underpinned to some extent by alternative uses such as logistics assets.

The manager says that investors should accept that yields are much lower than five years ago. If the company is going to have reliable income streams that are going to grow, then it needs to have high-quality assets. Service to tenants, the manager argues, has become far more important and there is good prospect of rental growth on assets that meet occupier needs, especially around energy and ESG.

Energy rating legislation

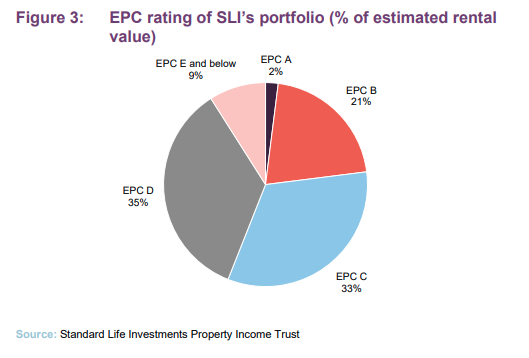

New legislation is expected to come into force requiring that commercial properties have Energy Performance Certificate (EPC) ratings of at least C by 2027 and B by 2030. It is a potential cliff-edge moment for the property market, as the capital expenditure required to meet these standards has not been factored in by some landlords. The legislation, which has not passed into law yet, is expected to come with some exemptions including around not being economically viable, although these have yet to be specified and the manager’s view is that assets without the requisite energy rating (exempt or not) will have reduced liquidity and be valued less. Scotland has a different methodology for assessing EPC ratings and different legislation for minimum standards, such that most ratings are lower than they would be in the rest of the UK, and trading in them is not restricted.

As detailed in our last two notes on SLI (see page 12 for links to previous publications), the manager has over the past few years placed a greater degree of emphasis on the energy performance of its current portfolio and target investments. Upgrades have been made on its portfolio, through refurbishments, and all new investments have good energy ratings. The manager says that the portfolio is being assessed and re-rated upwards (certification was conducted many years ago in most cases and the latest rating process uses much more informed modelling than it did in the past). At the end of 2021, 56% of SLI’s portfolio was rated EPC C and above.

The manager has said that it is very clear on what needs to be done to bring the rest of the portfolio to a C rating and is currently taking advice and assessing the route to a B rating. The route to a B rating, the manager says, involves electrification of heating systems. With huge technological advancements in the energy saving sector expected to come, the manager says that rushing in today to try to meet the B standard would be wasteful.

Most works to bring SLI’s portfolio up to the required standards are planned over the next five to seven years, and the manager calculates that the additional capital expenditure required will be between 10% and 15% a year higher than it currently spends. The company’s total capital expenditure on its portfolio last year was around £1.8m, £4.9m in 2020 and £4.6m in 2019.

Asset allocation

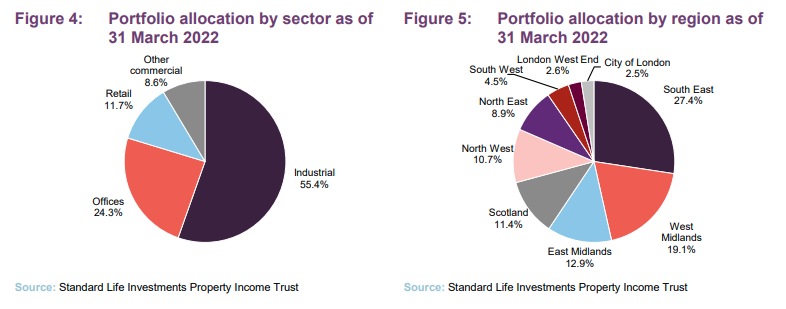

SLI’s portfolio was valued at £521.8m on 31 March 2021 (December 2021: £499.9m) and consists of 49 assets, primarily allocated across three sectors: industrials 55.4%, offices 24.3% and retail 11.7%. The ‘other commercial’ sectors make up 8.6% of the portfolio and consist of a data centre, a leisure complex in north London with redevelopment potential, and land.

The portfolio has a WAULT of 5.9 years and an occupancy rate of 91.4%. The group has collected 96% of the rent due for the whole of 2021, and for the first quarter of 2022 it has so far received 90% of rent billed. The manager expects this figure to rise to between 95% and 97%.

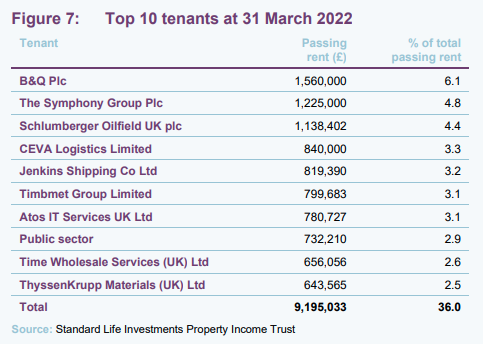

Top 10 holdings

Since our last note, SLI has made three acquisitions. The first was a forward funding development deal for an industrial scheme in St Helen’s. The total commitment will be £15.05m at the completion of the development (set for early 2023). It is a tripartite deal, with SLI funding the development, and a pre-let to St Helen’s Borough Council, which is sub-letting it to a not-for-profit organisation that will use the building as a research and development facility, focusing on improving the environmental impact of glass manufacture. The council has signed a 15-year term with five-yearly index-linked rent reviews, generating a net initial yield of 4.25%. A fixed-price contract has been signed with a developer, which is targeting an EPC A and a BREEAM very good/excellent rating.

The second acquisition was an off-market transaction for an industrial unit in Washington, Tyne and Wear, for £7.735m, reflecting a net initial yield of 5.75%. It is let to Griffith Textile Machines Ltd until 2035. The manager says the tenant has committed to improvement works at the building and is in discussions on how it can enhance sustainability features including adding solar panels to the roof. Another attraction to the asset was a vacant plot of land on the site. The manager says that this was not priced into the deal and gives it asset management options, including developing a new industrial facility or extending the existing building.

The third acquisition, made in April 2022, was for a car showroom in Stockton-on-Tees for £5m, reflecting a net initial yield of 6.5%. The deal was structured as a sale-and-leaseback from Motorpoint, which has entered into a new 25-year lease (with a tenant option at the end of 15 and 20 years).

The group has around £45m to spend on new assets (through cash and its undrawn revolving credit facility) and the manager says the company is under offer on a number of potential investments including the speculative funding of a mid-box logistics unit in the North West, for which agreements are in place and planning permission has been submitted. It would mean SLI taking the letting risk on the unit, but the manager says that it doesn’t believe this risk to be high in the current market.

Lettings and vacancy

At the end of 2021 SLI secured a letting at its second largest vacancy in the portfolio, at an industrial unit in Dover where it secured £611,000 per annum of rent from DEFRA, the government’s food standard control. Vacancy across the portfolio is still at 8.6%, which the manager says is above its long-term average.

The majority of the vacant space within its portfolio comes within the office sector. The group let two fitted office suites at 54 Hagley Road in Birmingham in the final quarter of 2021, but the asset remains 27% vacant and is now the largest void within the portfolio. The manager says that occupier interest in office space is picking up, but remains slow. The manager adds that it expects office occupiers to focus more on ‘best-in-class’ accommodation, with strong sustainability and wellbeing credentials. Poorer-quality accommodation, it says, will struggle to attract interest and a polarisation in rents and valuations will start to show in the sector.

The fitted office solution is appealing to occupiers, the manager says, and is where SLI is getting the most success and is currently under offer on a number of lettings across its office portfolio. In the first quarter of 2022 the group let four office suites across its portfolio. SLI has been offering fitted office solutions for four years now and the manager says that it has learned what works and what doesn’t. Creating banks of soundproof booths for people to have privacy for Zoom or Teams calls is popular, as is multi-use, break-out and collaboration space. The manager adds that there is a large difference in approach by different businesses and that SLI can be flexible to those needs due to the scale of its operation.

ESG initiatives

As detailed in previous notes, ESG and sustainability is at the heart of all of the manager’s investment decisions. SLI made a significant purchase in September 2021 in its aim to be carbon net zero, acquiring 1,471 hectares of upland rough grazing and open moorland in the Cairngorm national park, in Scotland, for £7.5m that is expected to offset a large proportion of carbon emissions from the portfolio.

At a portfolio level, SLI has undertaken a major Photo Voltaic (PV) installation across its industrial portfolio, the largest undertaken by abrdn in the UK. It currently has six operational PV schemes providing 1.2MWp and a further 13 projects that are at an advanced stage (offering up to 2.8MWp). It is also in discussions on another seven potential installations.

Performance

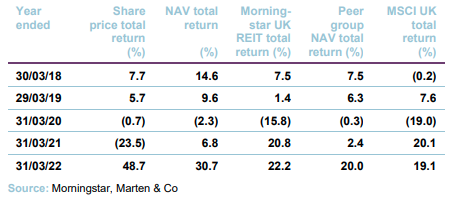

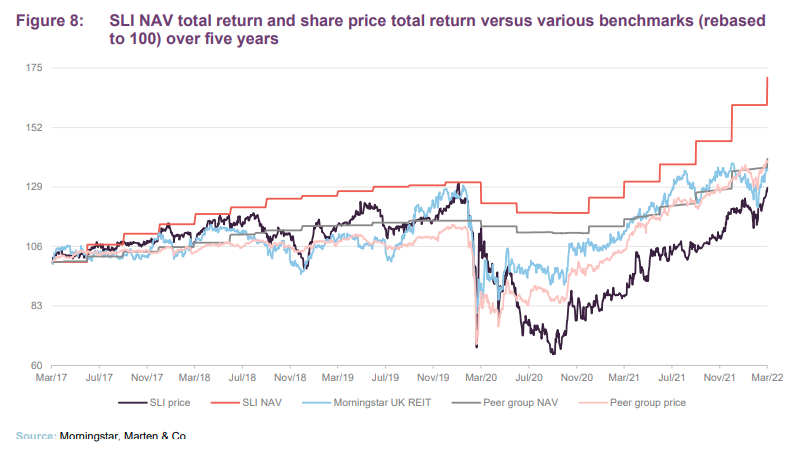

SLI’s NAV total return has bounced back strongly from its pandemic lows, with the company reporting an 5.5% uplift in NAV in the first quarter of 2022 alone. The group’s weighting to the industrial and logistics sector has helped, with valuations in this sector outpacing the rest of the market. As Figure 8 shows, SLI’s NAV total return has markedly outperformed that of its Property – UK Commercial peer group over the five-year period. Despite SLI’s superior NAV performance, its share price continues to lag that of its peer group and the Morningstar UK REIT index, which seems perverse in our view.

Peer group analysis

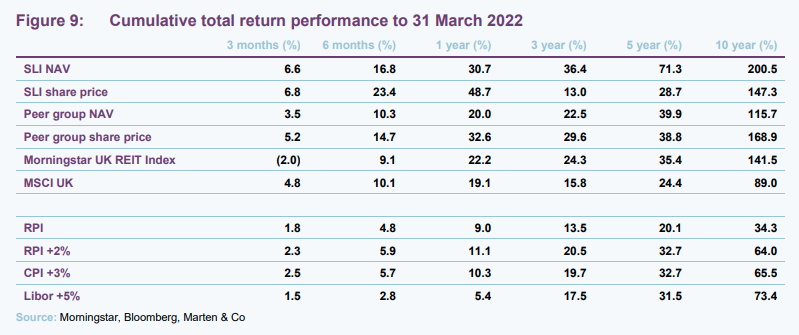

SLI’s NAV total return has, for all periods from three months to 10 years, comfortably beaten that of the Property – UK Commercial peer group average, as illustrated in Figure 9. For a strategy such as SLI’s, where assets tend to be held for the long term, we consider that the longer-term periods are the most relevant when assessing the effectiveness of the strategy. In this regard, SLI has clearly outperformed the peer group averages. Its share price performance also compares favourably to the peer group and the Morningstar UK REIT Index and MSCI UK Index over the past year.

From an inflation comparison, SLI’s NAV total return has been significantly ahead of inflation (as measured by both RPI and CPI) over all periods. In Figure 9, we have used RPI, RPI + 2%, CPI + 3% and Libor + 5%.

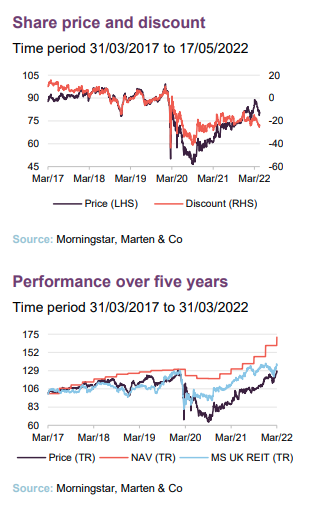

Premium/(discount)

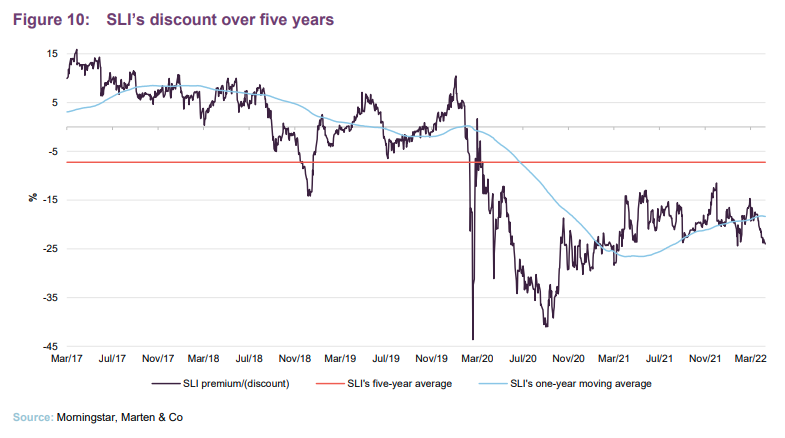

As illustrated in Figure 10, SLI’s discount has yet to recover to its pre-pandemic premium rating, with large quarterly NAV uplifts not immediately reciprocated in its share price performance. As at 17 May 2022, SLI was trading on a discount of 23.7%. SLI traded at a premium for much of the time pre-pandemic, but the outbreak of COVID-19 saw SLI’s rating fall from a 9.8% premium to a 43.6% discount in a matter of days, with a mass stock market sell-off. After recovering somewhat, the discount widened again as the fund cut its dividend in August 2020.

Fund profile

SLI launched on 19 December 2003. It is domiciled in Guernsey, has a premium main market listing on the London Stock Exchange and, to maintain a tax-efficient structure, migrated its tax residence to the UK on 1 January 2015, when it also became a UK Real Estate Investment Trust (REIT).

SLI aims to provide investors with an attractive level of income, together with the prospect of income and capital growth. It intends to achieve this by investing in a diversified portfolio of UK commercial property. These are principally direct holdings within the industrial, office and retail sectors, although it can also hold assets in the alternatives sector.

The board’s and manager’s preference is towards properties that are in good, but not necessarily prime, locations, where it is perceived that there will be good continuing tenant demand. The manager also looks for properties where it can add value using asset management initiatives. There is a focus on tenant quality, and as part of SLI’s strategy, tenants are treated as key stakeholders and the manager works closely to understand their needs. The aim is to achieve greater tenant satisfaction and retention, and therefore lower voids, higher rental values and stronger returns.

SLI has full use of the wider abrdn team, which has 270 people globally working on property. This provides access to specialist transactions, ESG, debt and research teams, as well as providing a strong risk management framework.

Previous publications

QuotedData has published five previous notes on SLI. You can read these by clicking the links in the table below.

Figure 11: QuotedData’s previously published notes on SLI

Source: Marten & Co |

The legal bit

This marketing communication has been prepared for Standard Life Investments Property Income Trust by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.