Third quarter of 2023

Investment Companies | Quarterly roundup | October 2023

Kindly sponsored by abrdn

‘Uncomfortable’

Following a fast start to the first half of the year, globally equities took a breather in Q3, as markets assessed the implications of the worst bond sell-off in a generation. Yields on 10-year US treasuries and UK gilts closed the quarter at fresh highs and are quickly approaching levels last seen in the lead up to the global financial crisis.

Coupled with rising interest rates, the ensuing tightening of financial conditions appears to have finally begun to work its way through to inflation outcomes, particularly in the US, although it seems highly unlikely that the Federal Reserve’s broadly defined target for 2% price growth is compatible with current labour market strength and unemployment rates of under 4%. After several months of slowing data, inflation has shown signs of trending upwards once more, giving more credence to the expectation of ‘higher for longer’ rates.

In the UK, fears of stagflation eased moderately in July as inflation data for the previous month fell sharply to 7.9% (core 6.9%), although with GDP running at a rounding error away from zero, there appears little to celebrate, particularly given the direction of several leading economic indicators which continue to point towards stagnation.

It was a similar story in the Eurozone. While the region has been one of the better performing sectors over the course of the year, returns have fallen over the last few months as growth has slowed and inflation has remained stubbornly elevated. European Composite PMIs fell for the fourth consecutive month in September, while inflation continued to track over 5%. The outlook has improved slightly in October, with flash inflation data offering a welcome reprieve, coming in below expectations at 4.3%, however there remains a long way to go in the economy’s fight for price stability.

New research

So far in Q3, we have published notes on: Bluefield Solar Income Fund, Henderson High Income/Henderson Diversified Income, Baillie Gifford UK Growth, Grit Real Estate Income Group, Ecofin US Renewables, Pantheon Infrastructure, GCP Infrastructure, abrdn Property Income Trust, Montanaro European Smaller Companies, NextEnergy Solar Fund, Tritax EuroBox, AVI Japan, and Chrysalis Investments.

At a glance

Winners and losers

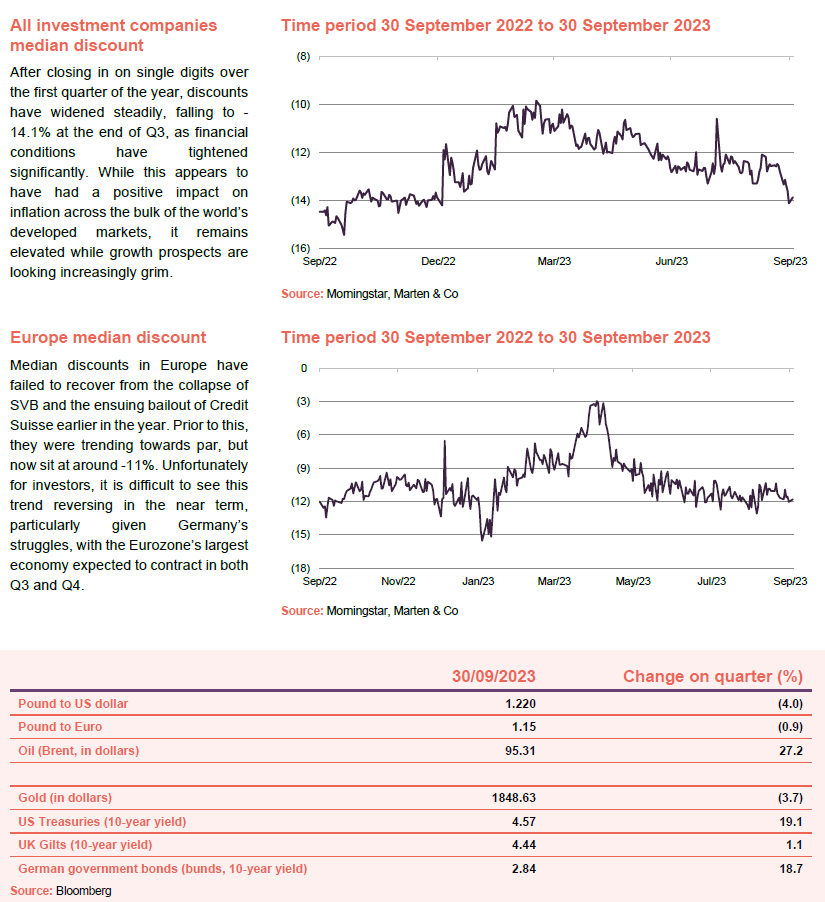

Despite broader market falls, NAVs grew 1% at the median although discounts widened from 12.8% in Q2 to 14.1% in Q3.

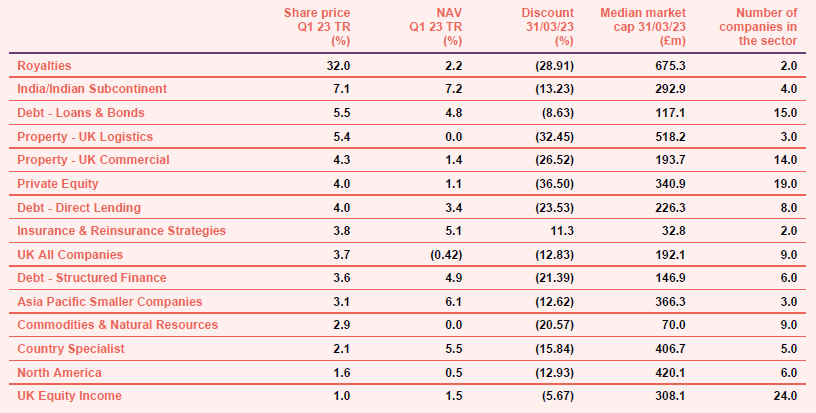

By sector

Q3 was defined by the ongoing long end bond sell off, with global markets trending down in sympathy. Investment trust returns were negative on average, although several sectors still achieved positive returns.

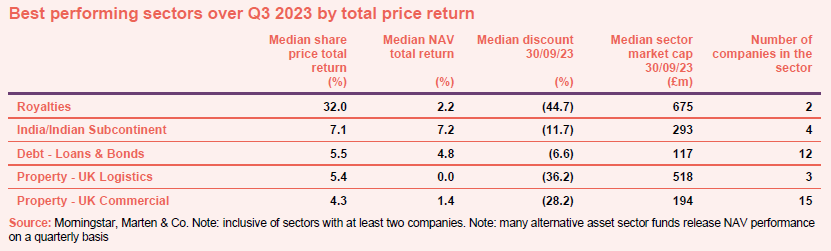

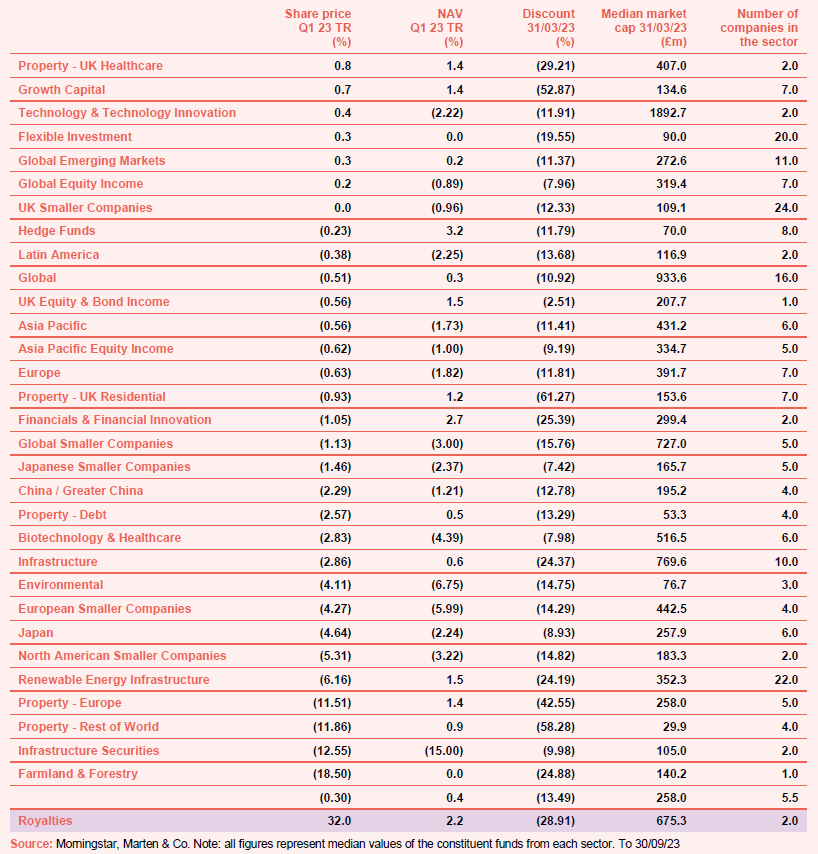

The Royalties sector was the standout performer following a cash offer from independent music company, Concord, for the outstanding share capital of Round Hill Music Royalty which represented a premium of approximately 67.3% to its closing share price.

The India and Indian Subcontinent sector has continued its impressive run over the course of the year, benefiting from buoyant domestic markets. The economy is on track to achieve YOY GDP growth of 7% making it the fastest growing major economy in the world, in stark contrast to the rest of the Asia Pacific region. While the outlook for the region remains positive, recent reports have suggested some areas of the economy, particularly within the mid and smaller cap sectors, have been experiencing a surge in speculative interest which have driven up valuations dramatically, with some commentators comparing the rally to that of the meme stock surge seen in the US in 2021.

While higher rates have generally weighed on returns, the Debt – Loans & Bonds sector has benefited with companies able to roll loans at higher coupon rates, boosting earnings and insulating returns. Although, this has been a double-edged sword in some cases with rising costs putting pressure on the operating abilities of some debtors.

The bulk of the returns in the UK Logistics sector stems from Tritax Big Box, although the growth appears to be more a matter of timing rather than any sustained recovery. Shares in the company hit their low water mark for the year at the beginning of the quarter, corresponding with the peak in UK rate expectations, and have steadily recovered as these have softened.

Returns in the Property – UK Commercial sector have followed a similar trend, although punctuated by a few outsized moves. Ediston Property Investment Company was up 23.2% over the quarter following the sale of its portfolio to US company, Realty Income, while Regional REIT fell 36.7% following the release of its annual report which outlined a significant drop in net rental income and was accompanied by a dividend cut.

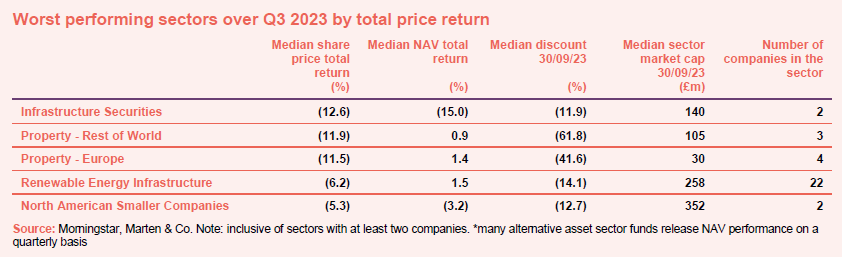

The worst performing funds reflect a continuation of the year’s dominate themes. Higher rates have increased concerns around the availability and cost of financing, in addition to the added competition from money market funds which are now providing steady returns without the associated credit and duration risks. This has been particularly harrowing for the Infrastructure and Renewable Energy Infrastructure sectors which have endured a horrid run, reflected in year-to-date share price losses of 14% and 18% respectively.

Property is another area that has clearly suffered from rising rates, and while there has been some positive news on the inflation front in the US, and to a lesser extent, the UK, the expectation of ‘higher for longer’ rates continue to depress returns, particularly in Europe where the threat of stagflation appears highest.

The fall in the North American Smaller Companies sector is a reflection of the rapid tightening in financial conditions in the US driven by the long end treasury sell off. Generally speaking, smaller companies have weaker balance sheets than their large cap counterparts and are therefore less able to absorb rising interest expenses, with these payments reaching fresh, record highs in Q3 across the small cap index.

Top 10 performers by fund

Geiger Counter topped the list of best performing funds by total NAV return in September as uranium prices surged to their highest level in 12 years, underpinned by a global renaissance in nuclear power, as utilities race to lock in fuel supplies. Prices have been rising steadily over the course of the year. However, recent supply constraints and a growing urgency for energy security have seen these surge toward levels not seen since the 2011 Fukushima disaster.

As noted above, the two small/medium cap Indian funds continue to outperform, boosted by the region’s world leading growth rates. The economy has been a benefactor of the diversification of global supply chains away from China, in addition to long running economic and capital market reforms which began prior to the pandemic. While the outlook for the region remains positive, recent reports have suggested some areas of the economy, particularly within the mid and smaller cap sectors, have been experiencing a surge in speculative interest which have driven up valuations dramatically, with some commentators comparing the rally to that of the meme stock surge seen in the US in 2021.

CVC Income & Growth was the best performing fund within the Debt – Loans & Bonds sector with regard to NAV growth. As noted above, the company has been able to leverage rising rates by reinvesting into attractive new primary issuance as existing positions are exited or repaid. Similar tailwinds have also contributed to the outperformance of VPC Specialty Lending.

Vietnamese markets have experienced an impressive period of growth through 2023 following a challenging few years following the pandemic. The economy has benefited from ongoing economic reforms, increasingly global export relationships, and ongoing consumer strength in the US, its largest export market. The region has also benefited from relatively low inflation and increased tourist activity which has boosted the returns of VietNam Holding.

CQS Natural Resources declined over the first half of the quarter as industrial metals fell, though subsequently recovered as weak economic data and still hawkish central bank commentary gave way to prospects for more meaningful Chinese stimulus. The company, along with peer, Riverstone Energy, was also buoyed by climbing oil prices which were supported by OPEC’s decision to extend production cuts. These dynamics also had a positive impact on Temple Bar, although returns have suffered following the end of the quarter due in part to a rising USD which weighs on commodity prices.

Nippon Active Value was also up strongly, bucking the trend of its Japanese smaller companies counterparts. The company is merging with Atlantis Japan Growth and abrdn Japan, and has secured a Premium main market listing on the London Stock Exchange. The release of its interim report reaffirmed the underlying quality of the portfolio.

The returns of BH Macro were thanks predominantly to USD appreciation stemming from the rally in long end USD treasuries.

On the share price side, Round Hill Music leapt when a bidder emerged for the company. Seraphim Space rallied following a trading update which showed that 11 companies in the trust’s investment portfolio had closed investment rounds at higher valuations than previous rounds.

Symphony International rallied on the back of an announcement that the fund will begin to return capital to shareholders following a strategic review. It Is not immediately clear what drove the returns of Private Equity peer, EPE Special Opportunities, but Pantheon International announced a planned £200m share buyback.

The Schroders Capital Global Innovation trust saw its discount close as shares rallied over the course of the month. However, this comes on the back of relatively thin volume and should be put in context with the fund’s steadily falling NAV.

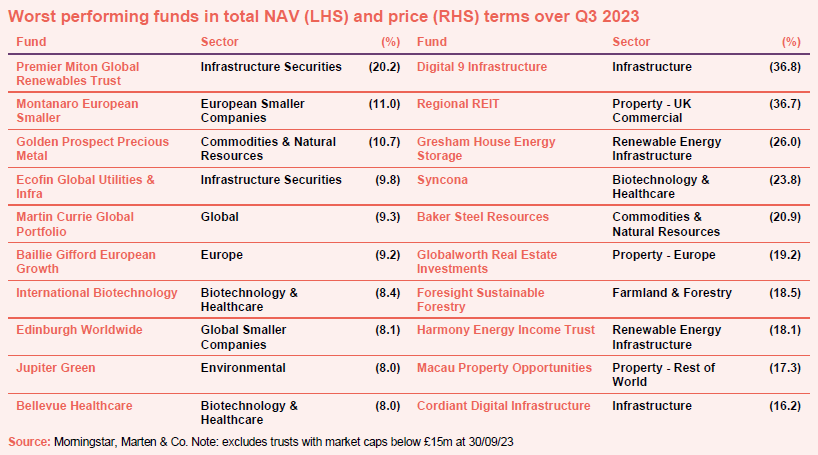

Bottom 10 performers by fund

The worst performing funds are very much a reflection of the dynamics discussed on page five, with a clear representation of funds struggling with the growing cost of capital and rising discount rates, which includes growth-focused companies like Montanaro European Smaller Companies, and Edinburgh Worldwide. Income-focused alternative asset funds, particularly in infrastructure sectors have also suffered from rising risk-free rates, as capital has flown into money markets and longer duration debt.

On the NAV side, Golden Prospect Precious Metals has suffered from the latest surge in real bond yields and the ensuing rise in USD which has weighed heavily on gold with the precious metal falling almost 5% at the end of the quarter. Surging rates in the US have also dragged down the returns of Martin Currie Global Portfolio due to a large overweight in US tech. The company’s largest holding, NVDIA, which makes up 10% of the fund, was down 12% over the last month of the quarter.

Europe has been one of the better performing sectors over the course of the year, however the region has struggled over the last few months with the selloff a reflection of the growing sense of stagflation in the region. Composite PMIs spent their fourth consecutive month in contraction while inflation has continued to track over 5%. The outlook has improved slightly in October, with flash inflation data offering a welcome reprieve, coming in below expectations at 4.3%, however there remains a long way to go in the economy’s fight for price stability.

Jupiter Green has suffered from the broader selloff in renewable energy driven by rising costs of production and finance.

It was somewhat of a surprise to see Bellevue Healthcare on the list of worst performers, although the fund’s exposure leans towards the more growth-oriented end of the spectrum with exposure to subsectors like med tech and diagnostics which have sold off over the last few months. For example, its largest holding, Exact Sciences, fell 32% in August. International Biotechnology was hit too.

In terms of share price moves, Digital 9 Infrastructure announced a delay in its planned part-disposal of one of its investments and the resultant pressure on cash flow meant a planned dividend was cancelled. Gresham House Energy Storage warned that rates of return available from its British battery storage assets were weak, which weighed on other battery companies including Harmony. Syncona has suffered from similar headwinds to Bellevue Healthcare. As mentioned on page seven, Baker Steel Resources has been impacted by weak Chinese demand for steel, without the ballast from energy exposure that helped drive returns for CQS Natural Resources.

Foresight Sustainable Forestry’s share price fall may be related to the collapse in UK carbon credit prices that followed the government’s watering down of its climate policies.

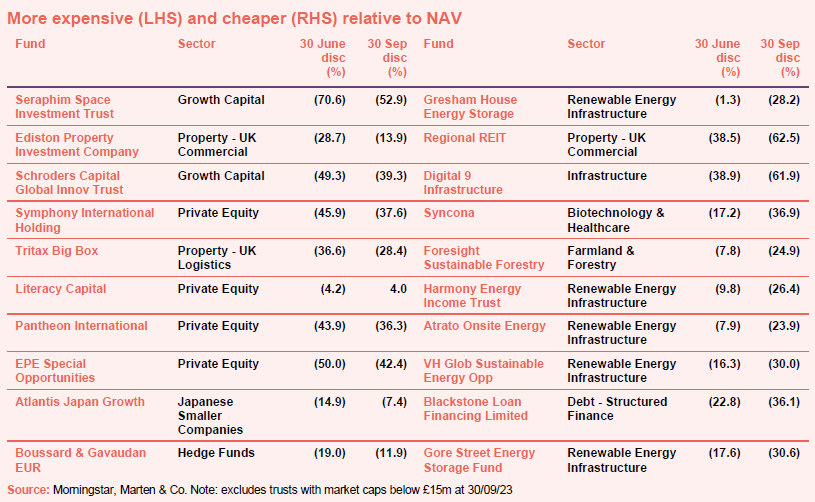

Getting more expensive

Of the funds not referenced above, Literacy Capital rallied on news of the sale of one of its largest assets for a 53.8% premium to carrying value while Atlantis Japan Growth rallied following its merger with Nippon Active Value.

Boussard & Gavaudan is undergoing a realisation of the existing assets, and any movements are a symptom of very thin volume.

Getting cheaper

Atrato Onsite Energy and VH Global Sustainable Energy Opportunities have been caught up in the general selloff in the renewables sector.

Blackstone Loan Financing has likely been affected by a combination of rising interest rates and gears of higher defaults within the underlying loan portfolios that it is exposed to.

Gore Street Energy Storage was hit by the selloff in battery funds that we referred to earlier. This reached such an extreme that in recent weeks the manager and board have published detailed reasons why they feel that this has been overdone.

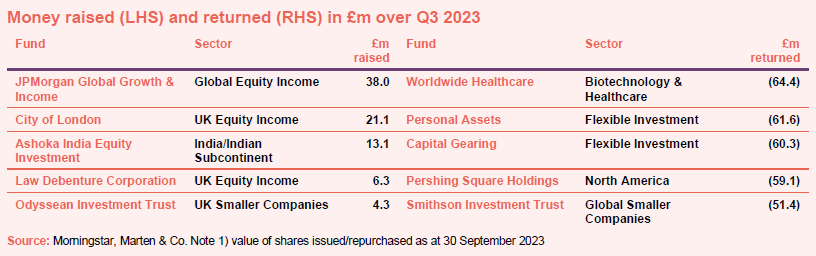

Money raised and returned

Money coming in

JPMorgan Global Growth and Income has been successfully raising capital along with usual suspects, City of London, and Law Debenture. Ashoka India Equity Investment has continued to benefit from the stability provided by markets in India and has been able to sustain a stable premium over the past six months. As has Odyssean, which has managed to buck the trend of the bulk of its smaller company peers and has been able to access the market for capital.

Money going out

In terms of money going out it was a case of the usual suspects as a number of larger trusts continued to operate their respective buy back policies. Personal Assets and Capital Gearing both try to maintain a zero discount. However, they are out of favour currently having lost investors money over the past year or so (they target absolute returns).

Upcoming events

Here is a selection of what is coming up. Please refer to the Events section of our website for updates between now and when they are scheduled.

Interviews

Every Friday at 11 am, we run through the more interesting bits of the week’s news, and we usually have a special guest discussing a particular investment company.

| Friday | The news show | Special Guest | Topic |

| 7 July | FP | Steve Marshall | Cordiant Digital Infrastructure |

| 14 July | SONG, TLEI, USF | David Smith | Henderson High Income |

| 21 July | DGN, DGI9, ABD | Ian Lance | Temple Bar |

| 28 July | RNEW, HDIV, ASCI | Uzo Ekwue & Pav Sriharan | Schroders British Opportunity Trust |

| 4 August | BPCR, TLEI | Fotis Chatzimichalakis | Impax Asset Management |

| 11 August | GCP/GABI/RMII, HGEN, NAVF/AJG | Helen Steers | Pantheon International |

| 18 August | TLEI, RSE, BSIF, NESF, EPIC, ESP | Richard Moffit | Urban Logistics |

| 25 August | USF, RICA, TLEI, EPIC, HOME | Iain Pyle | Shires Income |

| 1 September | HEIT, SOHO | Ed Simpson | GCP Infrastructure |

| 8 September | RNEW, RHM, RMII | Prashant Khemka | Ashoka WhiteOak |

| 15 September | EPIC, SONG, SUPR, TLEI | Dean Orrico | Middlefield Canadian Income |

| 22 September | AIG, GABI, GCP, HICL | Andrew Jones | LondonMetric Property |

| 29 September | DGI9, GIF, HICL, SONG | Carlos Hardenberg | Mobius Investment Trust |

| 6 October | ORIT, PSH, RGL | Alan Gauld | abrdn Private Equity |

| 13 October | EOT, GSF, CHRY | James de Uphaugh | Edinburgh Investment Trust |

| Coming Up | |||

| 20 October | Tom Williams | Downing Renewables | |

| 27 October | Richard Sem | Pantheon Infrastructure | |

| 3 November | Craig Martin | Vietnam Holding |

Research notes published over Q3 2023

From an operational standpoint, NextEnergy Solar Fund (NESF) is doing well. As we discuss on page 5 of this note, the board, encouraged by a high proportion of predictable revenue, has felt comfortable in declaring an inflation-matching 11% increase in NESF’s dividend per share, and is confident that this will be well-covered by earnings.

The rapid readjustment of valuations in the European logistics sector has encouraged investors seeking quality assets to return to the market, bringing optimism to Tritax EuroBox’s (EBOX’s) manager that values are stabilising. The company’s portfolio yield moved out 70 basis points (bps – equivalent of 0.7%) in the six months to 31 March 2023, but the worst of the declines seem to be over.

The team behind AVI Japan Opportunity (AJOT) continues to champion the tenets of good corporate governance and shareholder alignment. On this front, it recently made some positive progress with one of its investments – NC Holdings – where it put forward some resolutions at that company’s annual general meeting (AGM).

There is no denying that the last 18 months have been a challenge for Chrysalis Investments (CHRY). However, under the hood, the majority of the portfolio assets have actually performed reasonably well given the circumstances, especially when you consider that one company, Klarna, contributed more than half of CHRY’s total NAV adjustment during FY2022. Its other private investments, which make up the majority of the portfolio, fell just 5.6% during the same period.

Despite the headwinds it has faced – chief among them higher interest rates – Montanaro European Smaller Companies (MTE) remains committed to investing in high-quality, high-growth companies. MTE’s manager, George Cooke, has been unflinching in his approach, making little change to MTE’s portfolio other than increasing its concentration by trimming lower-conviction holdings.

Ecofin Global Utilities and Infrastructure Trust – Utilities and infrastructure at low tide

In recent months, macroeconomic conditions have weighed on the utilities and infrastructure sectors and on the returns generated by Ecofin Global Utilities and Infrastructure (EGL). Now, as the peak of interest rates draws nearer and economic growth stutters, the tide may be about to turn in the trust’s favour. EGL’s manager, Jean-Hugues de Lamaze highlights the strong earnings of the companies in its portfolio (see pages 5 and 6), which have made some of these look even more undervalued.

GCP Infrastructure Investments (GCP) has announced a potential three-way merger between it, GCP Asset Backed Income (GABI), and RM Infrastructure Income (RMII). As we explore in this note, this has the potential to address some of the issues that may have given rise to GCP’s exceptionally wide share price discount to its NAV. The outlook for investors remains as promising as ever thanks to a broad range of supportive conditions.

The Negative investor sentiment towards the commercial real estate sector has seen the share price discount to net asset values (NAVs) among REITs and listed property companies remain excessively wide, including abrdn Property Income Trust (API). This is despite a large valuation correction at the end of 2022 and transactional evidence of value stabilisation. A re-rating of the sector and API’s shares should be triggered by market indications that interest rates have peaked (due to their close correlation with property yields), so promising inflation data for June was encouraging.

Having concluded its acquisition of a leading property developer and asset manager, pan-African property company Grit Real Estate Income Group (Grit) has been reborn. Grit 2.0 has a greater and more achievable return target (of between 12% and 15% per annum) thanks to the controlling stake it now owns in Gateway Real Estate Africa (GREA) and its attractive pipeline of net asset value (NAV) accretive, risk-mitigated development projects – most notably diplomatic residences across the continent that are let to the US government.

Bluefield Solar Income Fund – Record year supports growth strategy

While share prices across the whole of the renewable energy infrastructure sector have been under pressure over the past 12–18 months, the execution by Bluefield Solar Income Fund (BSIF) has remained impressive, helping it to maintain its record of sector-leading distributions. The company’s record performance has been driven by locking in higher power prices through power purchase agreements (PPAs – which allow BFSI to sell energy at an agreed price, over a certain period of time). Thanks to the execution of these contracts, the board has good visibility over the bulk of company earnings for the next few years.

Henderson High Income / Henderson Diversified Income – Merger terms agreed

Henderson Diversified Income (HDIV) has agreed heads of terms for a combination with Henderson High Income (HHI). As part of the deal, shareholders in HDIV will have the option to take cash for all or part of their holding if they choose. In July 2023, HDIV’s chairman noted (see our news story here) that the trust had shrunk through share buybacks, and that this was inflating its average running costs and affecting liquidity in its shares. More importantly, he also made some observations about the fund’s investment approach (devised at launch in 2007) and the impact that this might be having on the sustainability of HDIV’s income and shareholders’ total returns (see page 4).

As the fund with most growth-orientated investment style amongst its peers (see page 21), Baillie Gifford UK Growth Trust (BGUK) has faced particularly strong headwinds during the last 18 months, as investors have either sought sanctuary in value and defensive stocks, or pulled money out of equities altogether, often in favour of fixed income stocks which are now offering a better rate of return than they have for some time.

Guide

Our independent guide to quoted investment companies is an invaluable tool for anyone who wants to brush up on their knowledge of the investment companies’ sector. Please register on www.quoteddata.com if you would like it emailed to you directly.

Appendix 1 – median performance by share price return over Q2 2023

The Legal Bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

The analysts who prepared this note may have an interest in any of the securities mentioned within it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.