Review 2022

Annual roundup | Investment companies | January 2023

Kindly sponsored by abrdn

A year to forget?

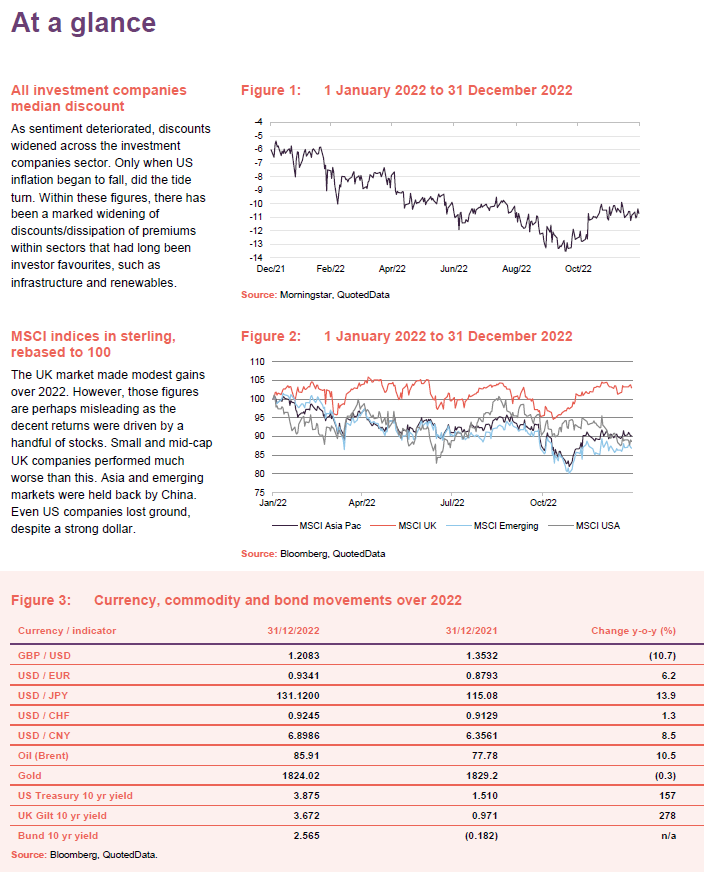

Any optimism that investors felt going into 2022 was dashed in February with Russia’s invasion of Ukraine. Resultant jumps in energy and food prices helped entrench inflation, requiring more aggressive interest rate hikes from central banks. Investments valued on a discounted cash flow basis had to factor in higher discount rates. That reinforced the shift in sentiment away from growth and towards value. Tighter monetary conditions and the depressive effect of China’s mishandling of COVID raised expectations of recession. That spelled potential bad news for lenders, meaning that debt funds had to cope with higher base rates and higher risk premiums. Top that off with some bizarre political decisions in the UK and you can see why many investors might want to forget 2022.

But, does that just set us up for a much better 2023?

At QuotedData, we:

- moved into our new home in the City – 50 Gresham Street;

- continued our prolific output of news, notes, and investment company and real estate monthly and quarterly roundups, plus our many contributions to third-party publications;

- shared the thoughts of our four analysts in our regular ‘QD view’ column, and added an external voice in the form of Cherry Reynard;

- continued our weekly Friday news round-up and interview show, bringing together fund managers and experts from across the industry and giving you the opportunity to ask them questions; and

- welcomed investors back to physical events at Master Investor Show and the London Investor show.

Investment company notes published in 2022

Figure 4: Notes published in 2022

| GCP Infrastructure – The future is brighter and greener | Temple Bar – Time to shine |

| Edinburgh Worldwide – Tomorrow’s winners | abrdn Private Equity Opportunities – Laying the foundations for future returns |

| Tritax EuroBox – Fast-tracked | Chrysalis Investments – Shepherding its portfolio through the storm |

| Herald Investment Trust – The future is bright | Baillie Gifford UK Growth – Patience will be rewarded |

| NextEnergy Solar Fund – Climbing inflation and power prices driving NAV uplift | JLEN Environmental Assets – Further portfolio diversification |

| AVI Japan Opportunity – The tortoise triumphs | Urban Logistics REIT – Long-term dynamics remain strong |

| abrdn European Logistics Income – Logistics safe haven with growth on the horizon | AVI Japan Opportunity – Maintaining its firepower |

| Henderson Diversified Income – Ahead of the curve | What the logistics is going on? |

| Strategic Equity Capital – Time to look forward | Alliance Trust – Stability in troubled waters |

| Montanaro European Smaller Companies – Unfazed by market turmoil | Tritax EuroBox – Opportunity knocks |

| Ecofin US Renewables Infrastructure – Clear path to growth | Ecofin Global Utilities and Infrastructure – A portfolio for all seasons |

| JLEN Environmental Assets – It’s all about renewables | Conviction Life Sciences – CLSC Initial Public Offering |

| Polar Capital Global Financials – Riding out the storm | BlackRock Throgmorton – The strong have only gotten cheaper |

| Henderson High Income – Last man standing | Polar Capital Global Financials – Don’t fear the dog that is yet to bark |

| Polar Capital Technology – Eyes on the prize | Polar Capital Technology – Jockeying for position |

| CQS New City High Yield – Interest rate rises maybe too little, too late | Pacific Horizon – Convergence opportunity |

| Standard Life Investments Property Income – Resilient income in uncertain times | NextEnergy Solar – Earnings visibility underpins dividend target |

| AVI Global Trust – Bargain hunting | Vietnam Holding – A real growth story that remains intact |

| Downing Renewables and Infrastructure – Proving its mettle | Abrdn Property Income – Laser focus on the basics |

| Civitas Social Housing – Fundamentals remain strong | Grit Real Estate Income – Going for growth |

| abrdn New Dawn – Over the trough | Henderson High Income – Does what it says on the tin |

| Montanaro UK Smaller Companies – Selloff provides opportunities | JPMorgan Multi Asset Growth & Income – Navigating a changed landscape |

| Grit Real Estate Income – Transition underway | Gulf Investment Fund – Much more than just oil and gas |

| JPMorgan Japanese – Unjustified sell off creates opportunities | North American Income Trust – Next generation dividend hero |

| GCP Infrastructure – Improving outlook and room to grow | |

Source: QuotedData

State of play at the end of 2022

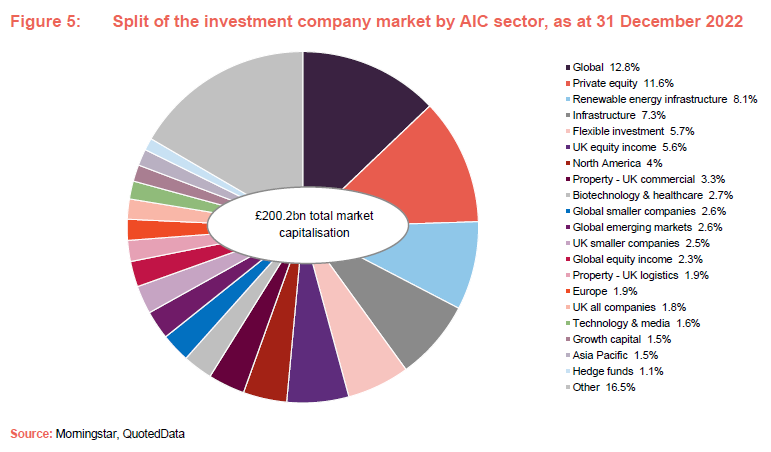

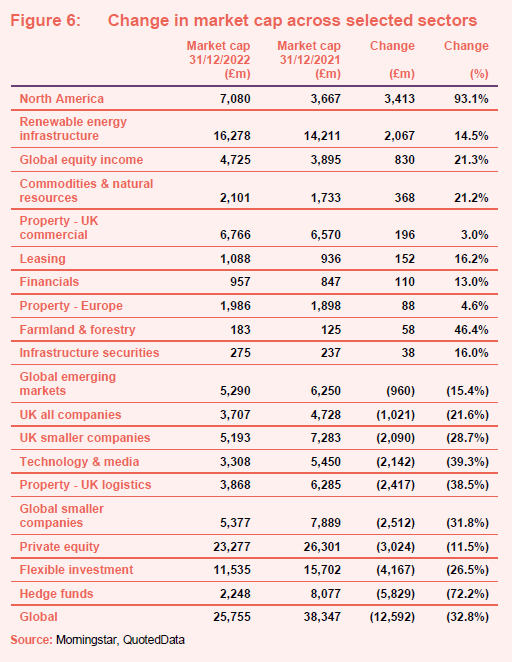

The investment companies sector shrank from £239.2bn to £200.2bn over 2022 in market capitalisation terms, driven by market movements and underperformance in some sectors. Figure 5 displays the relative composition of the industry by sector.

As we list on page 15, 12 funds were lost in 2022 and no new funds joined the sector.

Proportionately, the North American and farmland & forestry sectors were those that grew the most over 2022, increasing by 93% and 47% respectively (see Figure 6). The North American, renewable energy and global equity income sectors grew the most in market cap value terms. These figures were distorted by the reclassification of Pershing Square Holdings from hedge funds to North America and, in global equity income, JPMorgan Global Growth and Income’s absorption of Scottish Investment Trust from the global sector and JPMorgan Elect from the global and UK equity income sectors.

Farmland and forestry’s Foresight Sustainable Forestry and a clutch of funds in the renewable energy infrastructure sector were among the few funds to raise net new money in 2022 (see page 15).

On the negative side, buybacks, poor performance from titans such as Scottish Mortgage and the aforementioned loss of Scottish Investment Trust saw that sector shrink by about £2.6bn.

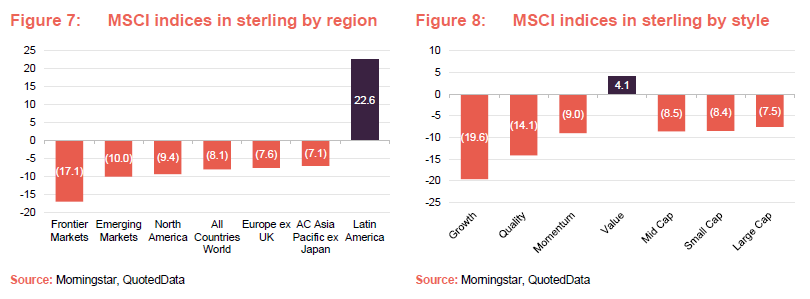

The median total share price return for all investment companies over 2022 was -11.1%, which – as Figure 7 shows – compares to a return of -8.1% for the MSCI All Countries World Index (MSCI ACWI), but remember that large parts of the investment companies market are invested in asset classes other than equities.

Performance data

As we highlighted on the front page, the main factors influencing markets over 2022 were inflation, rising interest rates, the war in Ukraine and China’s zero-COVID policy. A lot of these factors are interconnected.

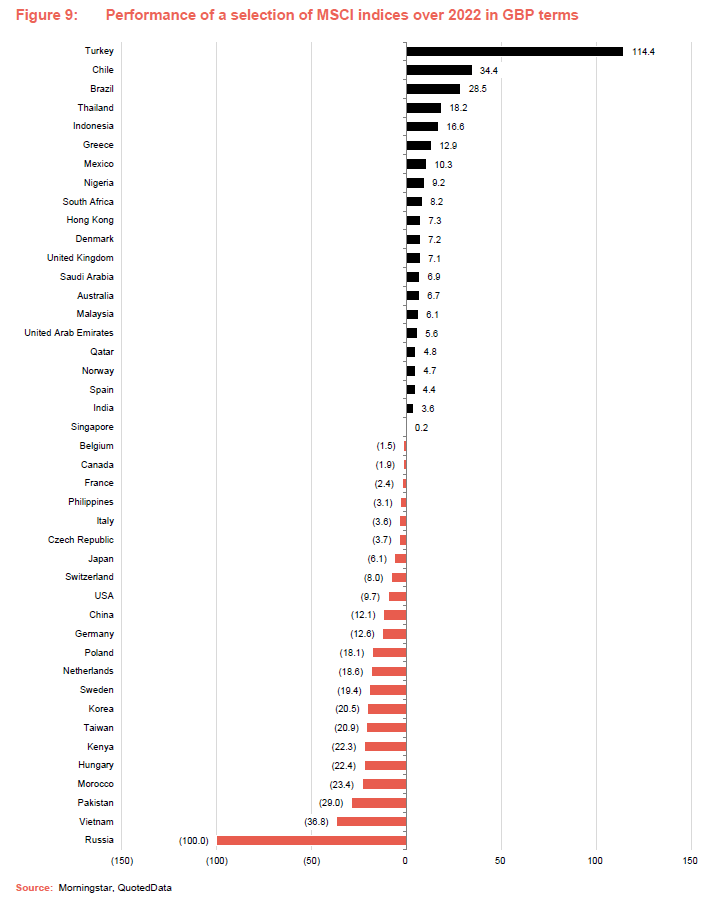

Looking at Figure 7, for a UK-based investor the only part of the world to make headway in 2022 was Latin America. The region has been unloved for many years, and was perhaps oversold, but rising commodity and energy prices were good news for this region and correspondingly bad news for areas dependent on commodity or energy imports, such as Europe. Investors were also looking for alternatives to Russia (once sanctions started to bite) and China. The dominant markets of Chile, Brazil and Mexico all did well.

Mexico is also a beneficiary of an increasing trend to switch manufacturing activity away from China. The constant disruption to supply chains associated with lockdowns in that country and growing distrust between China and the US, exacerbated by sabre-rattling over Taiwan, encouraged a search for alternatives.

Elsewhere, the positive commodities/energy story is reflected in the returns generated by countries such as Indonesia, South Africa and the Gulf states.

Adverse sentiment towards the Chinese market (not helped by the run-up to the 20th National People’s Congress) dragged down both the Asia Pacific and emerging markets indices.

Risk aversion and a strong dollar were also unhelpful for emerging and frontier markets.

The interest rate hikes prolonged and deepened a switch from growth to value-style investing that had begun in 2021. This hit a swathe of large cap companies in the US, driving that market down.

The surprise might be the underperformance of quality, which you might have thought would be in demand in the face of potential recession. However, it seems as though valuations in this part of the market were just too stretched going into this new phase of the cycle.

Risk aversion meant that large cap beat small cap, but globally the gap between the two was not as wide as it was in selected markets such as the UK.

Performance by sector and fund

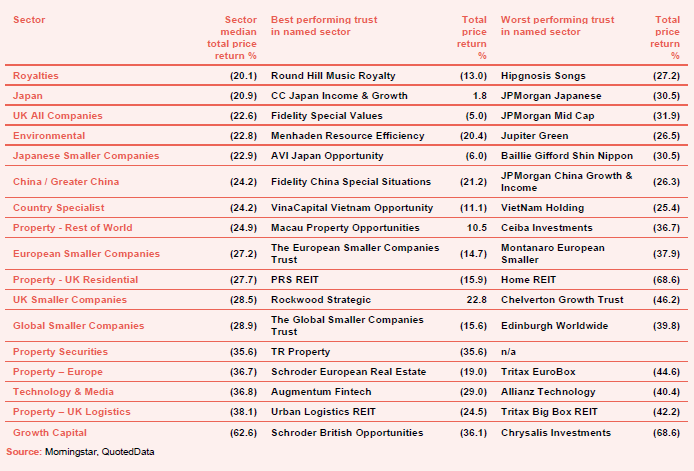

Looking at Figure 10, the best-performing sector by some distance was insurance and reinsurance but this was driven by a remarkable recovery in the share price of CatCo Reinsurance Opportunities, which is in wind up mode. However, the figures are misleading as, in April, ahead of the jump in the share price, the company redeemed 99% of its ordinary and C shares. The remaining NAV in the fund related to funds locked-up in side-pockets – money set aside to meet certain reinsurance claims. Sufficient money was released from these to redeem a further 92.3% of ordinary shares and 90.5% of C shares in December 2022.

Leasing funds also did relatively well. In this case, the driver was the post-COVID recovery in the aviation market and, in particular, Emirates’ decision to retain its fleet of Airbus A380 aircraft. The first of the Doric Nimrod funds succeeded in selling its sole aircraft to Emirates and will wind up shortly.

We have talked about the relative success of Latin America already. Foresight Sustainable Forestry appears to have got off to a good start – it recently announced that it has invested all of the money that it has raised in line with targets.

Trian Investors jumped in price after investors persuaded the board to shift the fund into realisation mode.

At the other end of the table, the shift in sentiment towards growth stocks, particularly untried and unprofitable companies, is reflected in the selloff in the growth capital sector, where even the best performer fell by 36%. Towards the end of the year, as US inflation started to fall and hopes that an end to interest rate rises could be in sight, these stocks started to pick up, and that recovery has continued into 2023.

Rising interest rates also triggered sharp falls across most property stocks as investors reasoned that yields would have to rise (implying that capital values would have to fall), while some companies also faced rising interest costs. The logistics sector found itself at the sharp end of the sell off. Previously, it had been a favoured destination for investors’ capital and yields had been driven down to what turned out to be unsustainable levels. Comments from Amazon, which had been growing its operations aggressively and had been a major source of occupier-demand, that it had over-extended itself were another blow to sentiment. However, there is some hope here as a shortage of suitable space is still driving rent increases in the sector.

Unsurprisingly, in an environment where growth was unloved, technology stocks were amongst the worst affected.

Best performing trusts

We have discussed the rally in the leasing sector already. Riverstone Energy has been gradually shifting its portfolio towards projects that support decarbonisation. However, the big jump in energy prices that accompanied Russia’s invasion of Ukraine was good news for the fund’s legacy positions in the oil and gas sector. JZ Capital Partners had lost a lot of credibility with an expensive and unsuccessful diversification into property. Concern was also building over its ability to meet debts as they fell due. In the event, some profitable disposals from its private equity portfolio helped calm nerves. SME Credit Realisation is making progress with its wind up.

Higher commodity and energy prices were good news for both BlackRock Energy and Resources Income and CQS Natural Resources Growth and Income. Gresham House Energy Storage is not widely exposed to the level of electricity prices but can benefit from volatility within these. Its good returns were also driven by the successful rollout of its portfolio of battery storage investments and attractively priced contracts from the National Grid to help stabilise the energy network.

Turning to Figure 12, which shows NAV moves, aircraft leasing fund Amedeo Air Four plus tops the table, for reasons already discussed. UK small cap trust Rockwood Strategic had a turbulent start to the year as management groups competed for the right to run the fund. However, it was takeover bids for a number of its portfolio companies that were the main driver of its decent NAV return for the year. Its strategy of assessing companies through the eyes of a potential private equity acquiror paid off.

Riverstone Energy was discussed above. Taylor Maritime has been a significant beneficiary of a relatively buoyant shipping market. It bought and sold ships well and is chartering its fleet on attractive yields.

Literacy Capital was the standout winner within the private equity sector. A number of funds made progress as profitable disposals drove NAVs higher. Literacy Capital seems to have listed with a relatively mature portfolio but all credit must go to its management team for its stock selection.

BH Macro is a hedge fund that benefits from volatility and there was no shortage of that in 2022.

Hipgnosis Songs is an interesting inclusion in this list as its share price went in the opposite direction to its NAV. Some commentators have queried why the discount rate used to value its portfolio has not risen as interest rates have increased. However, in the absence of this, increased royalty rates for songwriters, a return to public performances, price hikes implemented by music streaming sites such as Spotify and Apple, and some good results from the manager’s activities in promoting the use of the catalogue in areas such as films and advertising, pushed the NAV higher.

Riverstone Credit Opportunities has, like its sister fund Riverstone Energy, been shifting its portfolio towards funding decarbonising businesses. However, it is further along the road in this process and benefited as a number of borrowers refinanced their loans early, incurring pre-payment penalties, which benefit the fund.

Worst performing trusts

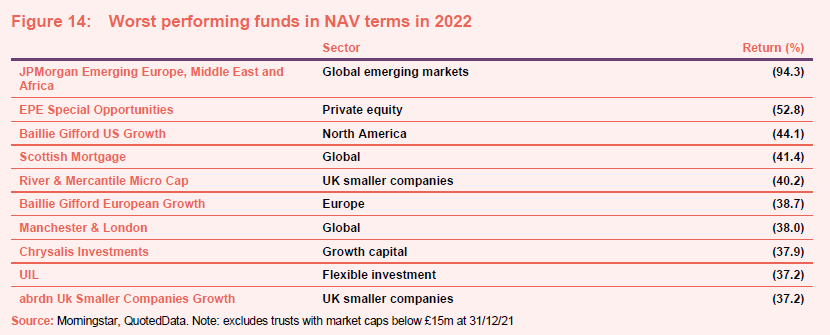

On the negative side, the standout loser was the former JPMorgan Russian securities, now renamed JPMorgan Emerging Europe, Middle East and Africa. Sanctions imposed on Russia and a ban on foreigners taking money out of the country left its Russian investments practically worthless. A rump of cash and investments outside Russia has been repurposed to a new mandate.

Next-worst performer was Chrysalis Investments. Investors were already disgruntled by the size of the managers’ performance fee (which attracted a lot of criticism, leading to some significant improvements in the way it will be calculated going froward), but write-downs in the values of some of its largest investments unnerved them and contributed to sharp falls in its share price. However, the stock is well off its lows as the company has drawn attention to the considerable potential of many of the companies in the portfolio and hopes have grown that interest rates will soon peak.

Home REIT was a darling of investors, offering a way to invest in something socially useful while receiving an attractive and growing dividend. However, a short-seller attack, with serious governance questions being raised; a class action lawsuit; tenants withholding rents; and a share suspension on the back of a failure to produce accounts have combined to erode faith in the company.

Seraphim Space’s portfolio contains many exciting investments but the majority of these are yet to make a profit. Shifting sentiment knocked it for six. The same could also be said of Schiehallion, but it also suffered from having previously traded on what we thought was an unsustainable premium. It is still relatively highly rated within its sector and may have further to fall.

EPE Special Opportunities has a large exposure to lighting company Luceco, its share price fell over 2022. Schroder UK Public Private is what remains of Woodford Patient Capital. It was forced to write off what was once its largest investment – Rutherford Health – during the year. We had previously argued that Woodford had taken too big a bet on the company.

Baillie Gifford US Growth, which was the worst performing trust in the North American sector over the year, suffered from the growth selloff. Sharp falls in the share prices of stocks such as Tesla, Shopify and Amazon took their toll on its NAV. Its relatively high exposure to unquoted companies was also seen as a potential problem. This was replicated for Scottish Mortgage.

As was the case for UK logistics companies, European logistics companies also suffered from rising yields and shifting sentiment, hitting Tritax EuroBox.

Turning to Figure 14 (which shows losers in NAV terms), we see many of the same names as in Figure 13. River and Mercantile Micro Cap makes the list. A general aversion to domestically-focused UK stocks was compounded by the many political missteps of 2022, and a growing recognition that the UK economy was likely to be amongst the hardest hit of all developed markets. Small cap stocks were perceived to be more sensitive to the UK economy and the problem was compounded by a preference for stocks with better liquidity.

Another Baillie Gifford fund, Baillie Gifford European Growth, makes this list. Manchester and London has a high exposure to the unloved technology sector. UIL has an eclectic portfolio but its NAV moves are also amplified by its share capital structure.

The former Standard Life UK Smaller Companies, now abrdn UK Smaller Companies Growth, suffered from its exposure to UK and small cap – as was the case for River and Mercantile Micro Cap – but it also has a growth bias to its portfolio, which was as an additional headwind.

Money in and out

The market turmoil of 2022 proved an insurmountable obstacle for funds looking to IPO. There were no new issues over the year despite quite a few attempts. Nevertheless, by our reckoning more money still flowed into the sector than out of it over the year – about £1bn in aggregate.

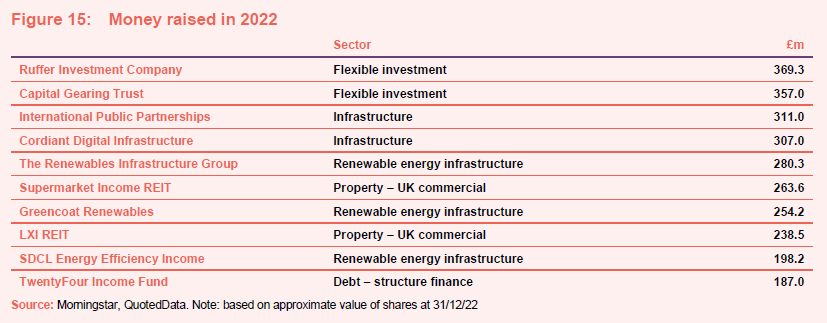

Money coming into existing funds

Unsurprisingly, given the market backdrop, money flowed into trusts designed to protect investors’ capital such as Ruffer and Capital Gearing. In the first half of the year, there was also demand for infrastructure and renewable energy infrastructure funds. However, as the year progressed concerns about the potential impact of higher interest rates on these funds’ NAVs led to them being de-rated. For example, International Public Partnerships, Cordiant Digital Infrastructure and The Renewables Infrastructure Group all finished the year trading on a discount.

A further 8 investment companies issued shares worth at least £100m over 2022 including Personal Assets, Gresham House Energy Storage, Bluefield Solar Income Fund, HICL Infrastructure, Gore Street Energy Storage, Digital 9 Infrastructure, City of London, and VH Global Sustainable Energy Opportunities.

Money going out of existing funds

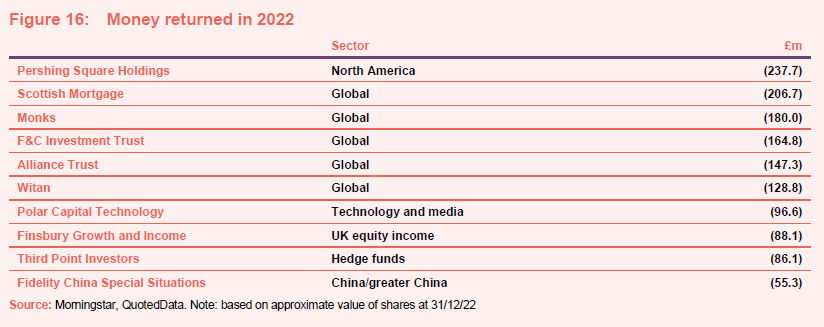

In an effort to reduce discount volatility and provide some liquidity to investors, a number of large funds bought back stock in 2022, led by Pershing Square Holdings. The list continues to be dominated by global equity trusts. Top of the list for these though were Scottish Mortgage and Monks, reversing the direction of flows into those companies. In terms of controlling the absolute levels of discounts, there were mixed results from these buybacks. F&C, Alliance, Witan, and Finsbury Growth and Income succeeded in narrowing their discounts. Scottish Mortgage, Monks and Pershing Square were less successful.

Liquidations, de-listings and trading cancellations

In 2022, we said goodbye to Cambium Global Timberland, CIP Merchant Capital, Fundsmith Emerging Equities, Jupiter Emerging and Frontier Income, ScotGems, UK Mortgages and Yew Grove REIT. In addition, Electra became a trading company – Unbound.

Honeycomb merged with its manager to become Pollen Street. In addition, Independent Investment Trust was absorbed by Monks, Secure Income REIT was absorbed by LXI REIT, and both Scottish Investment Trust and JPMorgan Elect were absorbed by JPMorgan Global Growth and Income.

Significant ratings changes

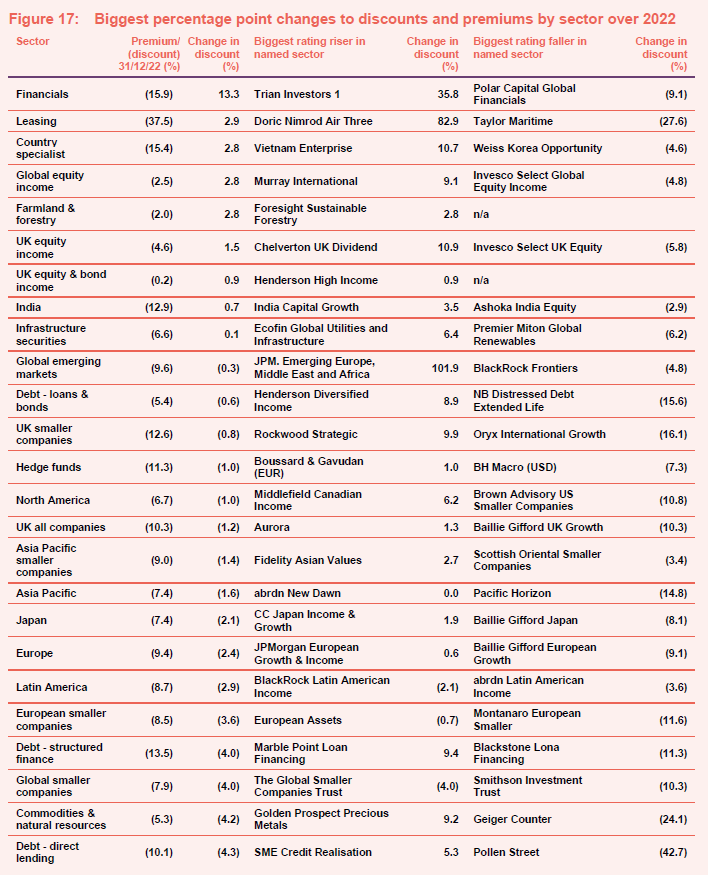

Figure 16 breaks the investment companies universe down by sector and looks at the biggest rating improvements and deteriorations over the course of 2022 within each sector.

The first couple of these – financials and leasing – have been discussed already. In the relatively small country specialist sector, which now has just four constituents, Vietnam Enterprise narrowed its discount despite enduring a relatively disappointing period of performance, both for that trust and the Vietnamese market in general. We recently interviewed Thao Ngo, one of its managers, to get some insight into this.

The value versus growth shift is evident in the re-rating of Murray Income relative to some of the other funds in the global equity income sector, many of which opted to invest in lower yielding stocks and top up distributions from capital, rather than invest in higher yielding stocks. Consequently, Murray Income had a higher to value stocks than they did.

Sometimes the relative re-rating reflects underlying performance, as was the case for India Capital Growth or Ecofin Global Utilities and Infrastructure, which led their respective sectors in NAV performance terms over 2022.

The huge premium ascribed to JPMorgan Emerging Europe, Middle East and Africa reflects the option value in its portfolio of Russian stocks. Investors are gambling on a normalisation of relations with Russia, which looks to us as a distant prospect.

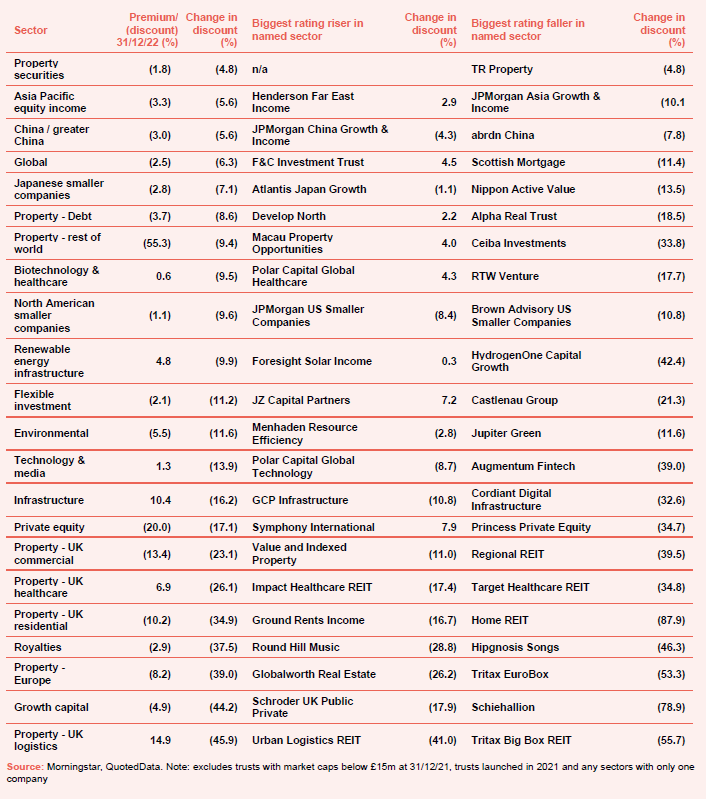

At the other end of the table, we have already discussed those sectors with most pronounced discount widening – Property – Europe, Growth capital, and Property – UK logistics.

We also mentioned the Royalties sector when talking about how Hipgnosis had made the list of best-performing companies in NAV terms. Its share price went in the other direction. There is the question mark over the discount rate used to calculate its NAV (on a discounted cash flow basis) but the company also seemed to be caught out by rising interest rates. At the start of 2022, the debt it had used to boost its exposure to song catalogues was floating rate. By the time that it was able to fix this, rates had risen to the point where we reckon the songs that it bought with debt are only just throwing off enough cash to meet the interest cost. However, there is a hope that cash flow from the portfolio will pick up and this could help get the fund re-rated in time.

QD views from 2022

Source: Visit www.quoteddata.com or more on these and other stories plus in-depth analysis on some funds, the tools to compare similar funds and basic information, key documents and regulatory news announcements on every investment company quoted in London

Manager interviews from 2022

Click on the company name to view the interview, or visit our youtube channel.

| Manager interviews from the weekly show | ||

| 7 January | Andrew McHattie | 2021 roundup |

| 14 January | Jason Baggaley | Standard Life Investments Property Income |

| 21 January | Keith Watson | Geiger Counter |

| 28 January | Jonathan Maxwell | SDCL Energy Efficiency |

| 4 February | Sebastian Lyon | Personal Assets |

| 11 February | Richard Aston | CC Japan Income & Growth |

| 18 February | Carlos Hardenberg | Mobius |

| 25 February | Ian Francis | New City High Yield |

| 4 March | Thomas Moore | abrdn Equity Income |

| 11 March | James Harries | Securities Trust of Scotland |

| 18 March | Tom Moore & Henrik Dahlström | Downing Renewables & Infrastructure |

| 25 March | Blake Hutchins | Troy Income & Growth |

| 1 April | Ian Lance | Temple Bar |

| 8 April | Yoojeong Oh | abrdn Asian Income |

| 22 April | Viktor Szabó | abrdn Latin American Income |

| 29 April | Robert Guest | Foresight Sustainable Forestry |

| 6 May | Gary Moglione | Momentum Multi-Asset Value Trust |

| 13 May | Richard Sem | Pantheon Infrastructure |

| 20 May | James Thom | Aberdeen New Dawn |

| 27 May | Paul Bridge | Civitas Social Housing |

| 10 June | Craig Martin | Vietnam Holding |

| 17 June | Laura Elkin | AEW UK REIT |

| 24 June | Pedro Gonzalez de Cosio | BioPharma Credit |

| 1 July | Andrew Beal | Schroder BSC Social Impact |

| 8 July | David Conlon & Joanne Fisk | GCP Asset-Backed Income |

| 22 July | Philip Kent | GCP Infrastructure |

| 29 July | Stuart Widdowson | Odyssean Investment Trust |

| 5 August | Kamal Warraich | Canaccord Genuity Wealth Mgmt |

| 12 August | David Smith | Henderson High Income |

| 19 August | Fiona Yang | Invesco Asia |

| 26 August | Nick Brind | Polar Capital Global Financials |

| 2 September | Tim Levine | Augmentum Fintech |

| 9 September | Joe Bauernfreund | AVI Global |

| 16 September | Stuart Gray | Alliance Trust |

| 23 September | Matthias Siller | Baring Emerging EMEA Opportunities |

| 30 September | Masaki Taketsume | Schroder Japan Growth |

| 7 October | Simon Farnsworth | Life Science REIT |

| 14 October | Jonathan Maxwell | SDCL Energy Efficiency |

| 21 October | Ross Driver | Foresight Solar Fund |

| 28 October | Joe Bauernfreund | AVI Japan Opportunity |

| 4 November | Jason Baggaley | abrdn Property Income |

| 11 November | James de Uphaugh | Edinburgh Investment Trust |

| 18 November | Jeff O’Dwyer | Schroder European Real Estate |

| 25 November | Bruce Stout | Murray International |

| 2 December | Rhys Davies | Invesco Bond Income Plus |

| 9 December | Stuart Widdowson | Odyssean |

| 16 December | Richard Aston | CC Japan Income and Growth |

Source: Visit www.quoteddata.com or more on these and other stories plus in-depth analysis on some funds, the tools to compare similar funds and basic information, key documents and regulatory news announcements on every investment company quoted in London

Outlook for 2023

Here are some recent comments from managers and directors drawn from our latest economic and political summary that you may find interesting.

On the global economy

Our January 2023 economic and political roundup has much more detail and many more comments on sectors including Europe, Japan, private equity, biotechnology & healthcare and renewable energy infrastructure.

Nalaka De Silva, Heather McKay, Simon Fox, and Nic Baddeley, managers, Aberdeen Diversified Income and Growth: “The global economy continues to face many headwinds, which is likely to lead to a deeper and earlier global recession than previously forecast. The UK and EU economies are facing a commodity price induced real income squeeze, amplified by central bank actions. We expect interest rate hikes from the US Federal Reserve, the European Central Bank and the Bank of England, as they seek to control inflation. To a degree, markets have already responded to this uncertainty: equity valuations are cheaper and credit spreads wider than they were at the start of the year – as such, many asset classes look more attractive now on a 5-year view. However, the compounding effects of these various shocks will mean that the investment environment will remain volatile and we may see further weakness across asset classes in the shorter-term.”

On the UK

Robert Talbut, chairman, Shires Income: “Recent months have been challenging for financial markets and there are a number of economic dark clouds impacting the investment outlook, with the Bank of England now predicting a “prolonged recession”. While this is certainly a challenging time for equities, there are reasons to be more constructive. Firstly, a recession is now largely expected by financial markets; and secondly many companies are significantly cheaper than they were at the start of the year. In addition, there are reasons to support a view that we are close to the peak of inflation and interest rate fears, and as these factors moderate, valuations can find support. Hence a time of widespread gloom could well be providing investors with attractive opportunities, and we have already seen signs of this with the strong rally across global equity markets since the middle of October.

In the shorter term, there is the likelihood of continued market turbulence. However, for those willing to take a longer-term view, there are strong supportive arguments that UK equity valuations look attractive. The market is on a multi-year high discount to other developed markets and has a record high yield premium. Furthermore, as the majority of company earnings come from overseas, any earnings downgrades will largely be offset by the currency benefit of weak Sterling.”

On Europe

Tom O’Hara and John Bennett, managers, Henderson European Focus Trust: “There are more reasons than ever to dismiss Europe as a region worthy of equity investment. And dismissed it is. We have never known it to be more disliked than it is now, which is quite a feat. The constraints to doing business we have referenced since the onset of Covid are now even more acute due to Russian aggression next door. Consumers face a tougher set of disposable income choices than they have for decades, with the further possibility of winter blackouts leaving households without heat and power and our industrial complex compromised.

Added to this, we cannot rule out the potential for an accident in a financial system increasingly under stress due to: 1) the speed of retreat from the free money era, and 2) the multiples of debt now in existence compared to the last time interest rates reached these levels. The tantrum caused in UK gilts and sterling by the fiscal ill-discipline of the uniquely short-lived Truss premiership, may well just be a dress rehearsal for something bigger on other shores. It goes without saying that such an event would be bad news for most assets in the short term.

And so, taking a dispassionate view of what is in front of us today, while acknowledging the many short-term tangible and tail risks, we can only conclude one thing: Europe is too cheap. Not all of it, of course, certainly not many of the darlings of the low interest rate paradigm, where investors appear to be in denial as to just how seismic the shift in the valuation regime really is. Muscle memory exerts strong influence in markets and we expect many investors to keep returning to the familiarity of what made them warm and cosy before. Eventually they will learn new behaviours. Where we see opportunity is in the sectors so brutally jettisoned that they already price in a ‘normal’ recession and worse in some cases: quality, cash generative champions across energy, materials and industrials, with strong management teams and, most importantly, pricing power. This latter point is critical for us since we continue to believe inflation will settle at structurally higher rates than pre-Covid, driven by socio-political and geo-political factors; labour will command a bigger share of the economic pie as the Western world ‘onshores’ critical aspects of industrial supply chains, energy included.”

On Japan

Nicholas Weindling and Miyako Urabe, managers, JPMorgan Japanese: “With the vaccine programme having been rolled out effectively, the Government has recently lifted the last of its Covid restrictions and the country is now fully reopened to foreign tourism. Furthermore, exporters will receive a fillip from the yen’s recent depreciation thanks to the wide disparity between US and Japanese interest rates. While the US has rapidly increased rates, the Bank of Japan (BoJ) has so far maintained an ultra-loose monetary policy stance.

Conversely, the weak yen makes imports more expensive – a particular problem for Japan as it has almost no natural resources, so it must import energy and other commodities. The weaker yen has increased the cost of these imports, adding to price increases triggered by pandemic-related shortages and the war in Ukraine. As a result, inflation has begun to rise in Japan, but remains lower than in most other developed countries.

Despite a tight labour market, wage growth remains low and there has been no significant increase in property rents. While we do not expect these developments yet to elicit any change in BoJ policy, we are aware that policy may shift with the likely appointment of a new BoJ governor next spring.

Improvements in Japan’s corporate governance continue, with more companies focused on improving shareholder returns. The country is in the process of a major technological transformation that should deliver growth and productivity gains over the medium term. Japanese equity markets are more vibrant than some investors appreciate, with many new and interesting listings on the Tokyo Stock Exchange each year.”

On Technology

Ben Rogoff, manager, Polar Capital Technology Trust: “Markets continue to reprice risk against a backdrop of an unusually wide range of outcomes. However, we have not given up on the hope that this period will – in time – be understood as another Covid-related episode where excess liquidity, supply shortages and collective trauma have left demand and supply in a state of disequilibrium. The risk of inflation becoming embedded has left policymakers with little choice, their own credibility and personal legacies dependent on the war against inflation. Until there is more certainty about the outcome of this battle, our interests are likely to remain uncomfortably at odds with policymakers. However, we also know that market narratives can change quickly should macroeconomic headwinds and/or exogenous risks subside. Less than three years ago, we were faced with one of the world’s deadliest pandemics. Technology kept the world spinning while biotechnology and AI developed vaccines that broke the link between Covid cases and deaths. Even if technology stocks have struggled to live up to their pandemic billing, we remain believers in the primacy of technology and excited about humankind’s ability to innovate and reimagine industries. This – above all else – should provide a fertile backdrop against which to invest.

We wish you good luck and good health with all your endeavours in 2022!

Ed, James, Matt, Richard, David, Dave, Padraig, Aiman, Emma, Robin, Colin, Nick, Trevor, Brice, Jemima and Veronica

The legal bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.